- Specialty & Fine Chemicals

- Xanthates Market

Xanthates Market Size, Share, and Growth Forecast, 2025 - 2032

Xanthates Market by Product Type (Sodium Ethyl Xanthate, Sodium Isopropyl Xanthate, Sodium Isobutyl Xanthate, Potassium Amyl Xanthate, Others), Application (Mining, Rubber Processing, Agrochemicals, Others), and Regional Analysis for 2025 - 2032

Xanthates Market Share and Trends Analysis

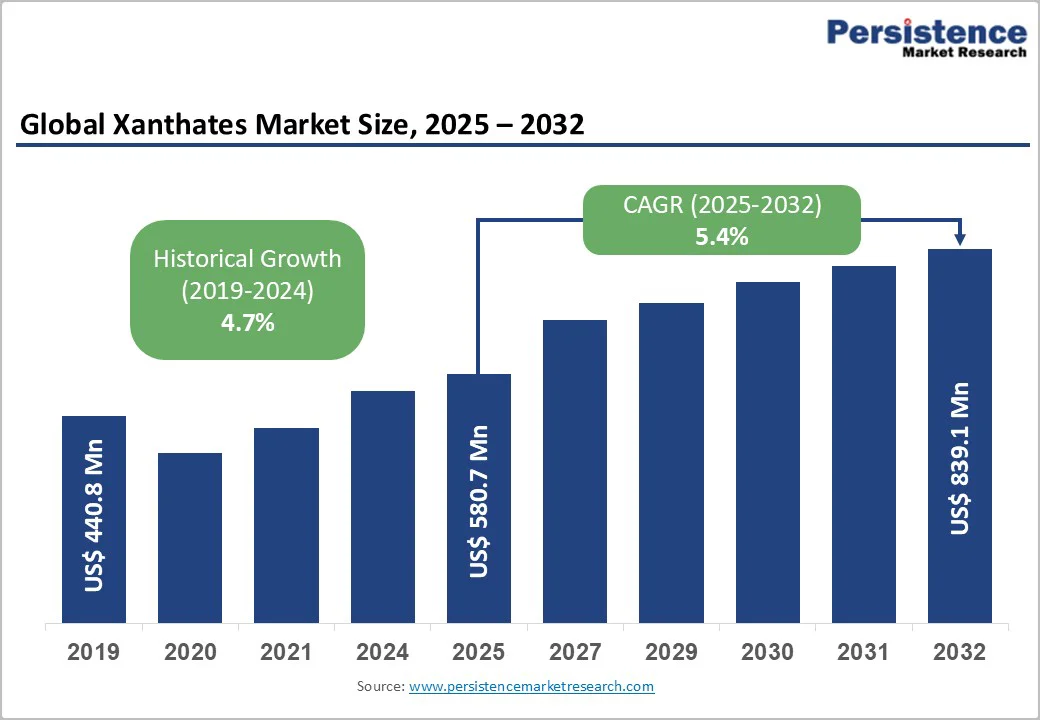

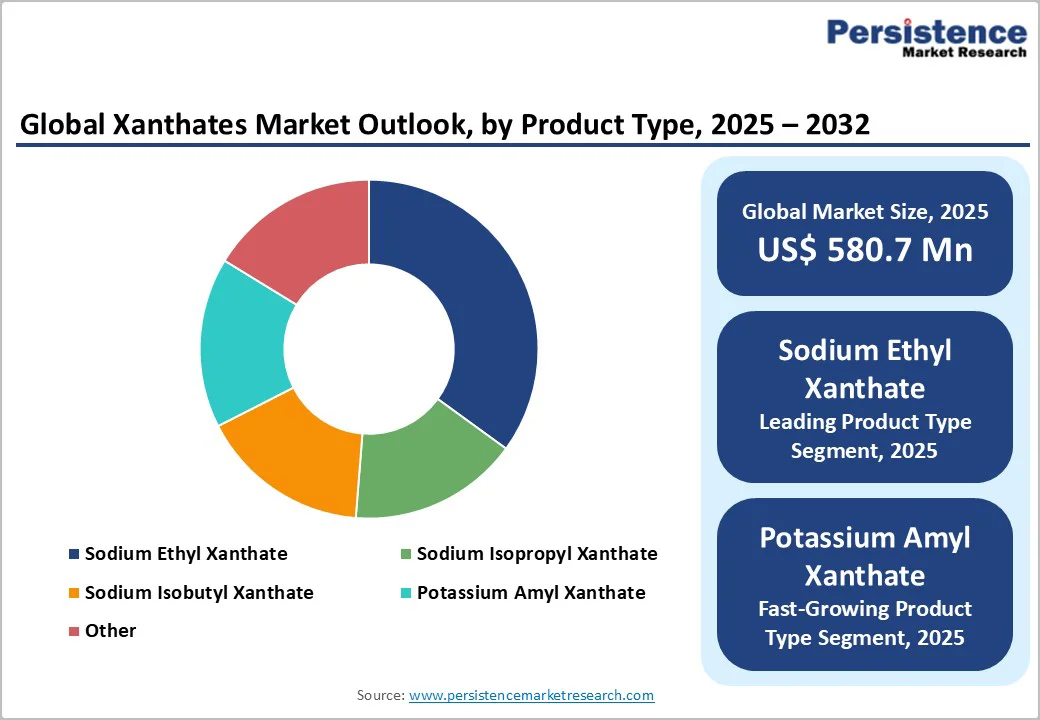

The global xanthates market size is likely to be valued at US$ 580.7 million in 2025, and is projected to reach US$ 839.1 million by 2032, growing at a CAGR of 5.4% during the forecast period 2025-2032.

The primary drivers of this growth stem from escalating global mining activities that demand efficient flotation reagents for mineral extraction, coupled with expanding applications in rubber processing and agrochemicals. Supporting this, worldwide sulfide mineral processing has spiked xanthate consumption, fueled by the increased production of metals such as copper and gold in emerging economies. The push for sustainable rubber vulcanization and pesticide intermediates further aligns with broader industrial trends, enhancing market resilience despite environmental challenges.

Key Industry Highlights

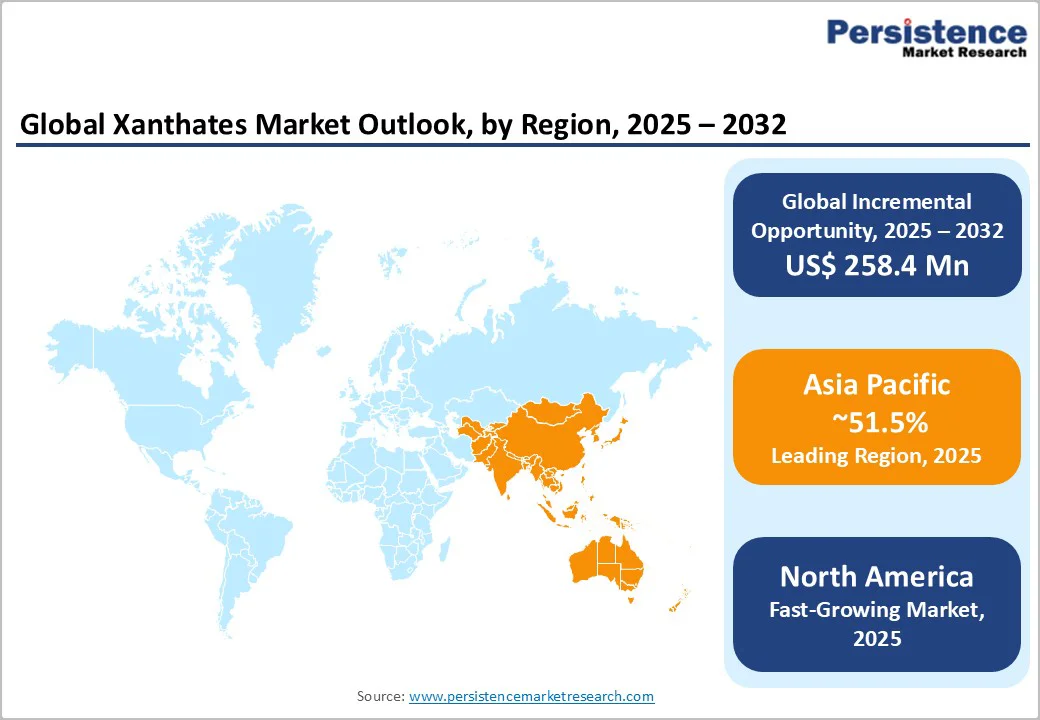

- Regional Leader: Asia Pacific leads with around 51.5% of the xanthates market share, driven by China's dominant production and mining expansions.

- Fastest-growing Regional Market: North America emerges as the fastest-growing regional market for xanthates, supported by technological leadership in mineral processing and stringent environmental frameworks of the U.S. and Canada.

- Leading Application: Mining dominates, holding a 72% share due to the indispensable role of xanthates in sulfide ore processing for critical metals such as copper and gold worldwide.

- Fastest-growing Product Type: Sodium ethyl xanthate is likely to grow the fastest through 2032, propelled by innovations in selectivity for complex ores in emerging markets.

- Growth Opportunities: The adoption of eco-friendly formulations presents a key opportunity, targeting sustainability mandates to boost recovery and reduce emissions in the expanding mining sector.

| Key Insights | Details |

|---|---|

|

Xanthates Size (2025E) |

US$ 580.7 Mn |

|

Market Value Forecast (2032F) |

US$ 839.1 Mn |

|

Projected Growth CAGR (2025-2032) |

5.4% |

|

Historical Market Growth (2019-2024) |

4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Xanthates in Mineral Flotation Processes

Xanthates serve as critical collector compounds in froth flotation processes for extracting sulfide ores such as copper and zinc, particularly as global mining operations expand across resource-rich regions. By selectively attaching to sulfide minerals and enhancing their hydrophobicity, xanthates significantly improve mineral recovery rates and processing efficiency. This application has driven sustained demand across mining-dependent economies, with technological advancements enabling selective flotation methods to achieve commercial-scale success worldwide. The market for xanthates continues to expand as mining output increases to meet growing industrial demand for base metals.

Beyond mining, xanthates play an equally important role as vulcanization accelerators in the rubber industry, enhancing production efficiency for automotive and tire applications. Research demonstrates that xanthate-based compounds, including eco-friendly variants such as starch-supported sodium isobutyl xanthate, improve mechanical properties and thermal stability of rubber materials while reducing production times. This dual application, combined with the growing emphasis on sustainability and recycled materials, positions xanthates as essential compounds across both resource extraction and manufacturing sectors, supporting market growth driven by industrial expansion and technological innovation.

Stringent Environmental and Toxicity Regulations

Xanthate products face significant environmental and regulatory headwinds due to their decomposition into toxic byproducts, particularly carbon disulfide, which poses risks to aquatic ecosystems and human health. Regulatory authorities across the European Union (EU) and Australia have flagged xanthates for aquatic toxicity, leading to stricter water quality directives and potential usage restrictions in environmentally sensitive regions. The ability of xanthates to infiltrate water systems through mining discharge and runoff, combined with bioaccumulation concerns, has intensified pressure on manufacturers to transition toward biodegradable and eco-friendly alternatives. These regulatory barriers increase compliance costs for producers and limit market penetration in regions with stringent environmental standards.

The xanthate manufacturing process is heavily dependent on volatile raw material supplies, including carbon disulfide, alcohols, and alkali hydroxides, which experience significant price fluctuations driven by geopolitical tensions and trade dynamics. Production facilities are geographically concentrated, creating supply chain vulnerabilities during periods of geopolitical stress or natural disasters that disrupt output and delay deliveries to end-users. These constraints collectively erode profit margins for manufacturers, drive pricing instability in the market, and create barriers for smaller mining and rubber operations seeking to adopt premium-grade xanthate products. The combination of regulatory pressures and supply chain unreliability presents ongoing challenges to market stability and growth.

Adoption of Eco-Friendly Xanthate Formulations

Market participants are increasingly positioned to capture growth through the development and adoption of biodegradable and low-toxicity xanthate products, driven by regulatory mandates and sustainability pressures across the mining sector. Industry leaders such as Clariant have pioneered eco-friendly flotation chemicals with significant improvements in environmental performance compared to conventional alternatives, while innovations in liquid formulations reduce handling risks and operational emissions. These green chemistry solutions align with emerging regulatory frameworks, particularly EU initiatives targeting surface water pollutants, creating differentiation opportunities for early adopters. The integration of digitalization and artificial intelligence in reagent optimization enables precise dosing and performance enhancement, with manufacturers investing in bio-based xanthate derivatives from renewable feedstock positioned to capture substantial market share in environmentally conscious regions as global mining operations expand.

Xanthates also present expansion opportunities in the agrochemical sector, where they function as intermediates in pesticide and herbicide formulations and as encapsulating agents for controlled-release agrochemical products. The growing emphasis on sustainable agricultural practices and compliance with organic farming policies creates demand for bio-based xanthate formulations in crop protection applications. This diversification into agrochemicals and specialized agricultural solutions broadens revenue streams for xanthate manufacturers beyond mining-dependent markets, supporting robust growth momentum driven by increasing global food security needs and the transition toward sustainable farming methodologies.

Category-wise Analysis

Product Type Insights

Sodium ethyl xanthate leads the product type segment with approximately 35% market share, owing to its superior selectivity and cost-effectiveness in sulfide mineral flotation, particularly for copper and gold ores. This dominance is justified by its widespread adoption in a large number of mining operations around the globe, where it achieves recovery rates exceeding 90%, as documented in several metallurgical studies. Its stability in aqueous environments and lower dosage requirements, typically 20-100 g/ton, make it preferable over alternatives such as isopropyl variants, supporting efficient processing in high-volume sites.

Yantai Aotong Chemical and other major manufacturers maintain substantial production capacity for sodium ethyl xanthate, ensuring consistent supply to mining operations in different parts of the world. The good selectivity characteristics of the compound make it particularly beneficial for improving concentrate grades, though operators frequently combine it with higher-grade xanthates such as butyl variants to optimize both recovery rates and product quality in complex ore processing scenarios.

Application Insights

The mining application dominates with about 72% of the xanthates market revenue share, driven by its critical role in froth flotation for extracting valuable sulfides such as zinc and lead from ores. This leadership is substantiated by consumption data showing mining accounting for the bulk of xanthates produced annually, with efficiency gains in ore beneficiation reducing waste by a sizable margin. The segment's resilience also stems from global metal demand, ensuring xanthates remain indispensable despite shifts to other uses.

Companies such as Coogee Chemicals operate specialized liquid xanthate manufacturing facilities at major mining sites including Mount Isa in Queensland, providing customized reagent solutions tailored to specific ore characteristics. The increasing complexity of mineral deposits and the processing of increasingly refractory ores continue to drive innovation in xanthate chemistry, supporting the sustained dominance of the segment in market consumption patterns.

Regional Insights

North America Xanthates Market Trends

In North America, the United States leads xanthate consumption due to robust mining in states such as Nevada and Arizona, where gold and copper production has been steady over the past decade, as per U.S. Geological Survey data. Regulatory frameworks established by the U.S. Environmental Protection Agency (EPA) enforce strict effluent limits, pushing innovations in low-residue formulations to comply with Clean Water Act standards, mitigating toxicity risks. This focus has fostered a strong innovation ecosystem, with investments in automated dosing systems enhancing recovery in operations.

Technological advancements, including bio-leaching integrations, align with sustainability goals, reducing environmental footprints in tailings management. Recent developments, such as mine expansions in the Rockies, underscore the emphasis of regional market stakeholders on efficient reagent use amid water scarcity challenges.

Europe Xanthates Market Trends

The Europe xanthate market growth is shaped by stringent regulatory harmonization under REACH and the EU Water Framework Directive, particularly in Germany, the United Kingdom, France, and Spain, where mining output for base metals has been promising. These nations prioritize eco-assessments, leading to a notable shift toward greener alternatives since 2023, as highlighted in parliamentary votes on water pollution controls. Performance analysis reveals optimized usage in polymetallic ores, balancing extraction efficiency with emission reductions. Harmonized policies have stimulated cross-border collaborations, such as joint R&D in Scandinavia for biodegradable variants, supporting the transition of European nations to circular mining economies. This regulatory landscape ensures steady, compliant growth despite volume constraints.

Asia Pacific Xanthates Market Trends

Asia Pacific dominates the xanthates market share with explosive growth in China, India, Japan, and ASEAN countries, where manufacturing advantages and mineral reserves propel xanthate demand. China's production, exceeding 30,000 tons yearly from major facilities, supports its status as the top coal and rare earth producer, with output rising annually, as per national statistics. India's mining sector expansion, targeting 500 million tons by 2030, leverages cost-effective supply chains for flotation in iron and bauxite processing. The evolving dynamics of the ASEAN bloc, including Indonesia's nickel boom, amplify opportunities through low-cost production and export hubs. These factors, combined with infrastructure investments, position the region for accelerated adoption of advanced xanthate technologies.

Competitive Landscape

The global xanthates market exhibits a moderately consolidated structure, with top players leading the charge on the back of strategic expansions and R&D partnerships for eco-formulations, while regional suppliers have fragmented the rest of the landscape. Companies are actively focusing on forging collaborations for supply chain resilience and innovation in liquid delivery systems, differentiating via performance in complex ores. Emerging business models emphasize sustainability credentials and digital integration, with manufacturers developing AI-powered dosing optimization systems and biodegradable reagent alternatives to address evolving regulatory requirements and customer preferences in environmentally conscious markets.

Key Industry Developments

- In November 2025, Anglo Asian Mining secured a sales contract with global commodities trader Trafigura for copper concentrates from its newly commissioned Demirli copper mine in Azerbaijan, which is expected to produce 4,000 tons of concentrate in 2025, scaling to 15,000 tons from 2026 onwards. The company has obtained all necessary government approvals and operating licenses, marking a critical milestone in its strategic transition from a primarily gold producer to a copper-focused operation by 2029, with Demirli representing the second copper mine brought online this year alongside the Gilar underground deposit.

- In September 2025, Indonesia's seizure of approximately 148 hectares of the PT Weda Bay Nickel mine, the world's largest nickel operation partly owned by Tsingshan Holding Group, triggered a 1% surge in London Metal Exchange nickel futures to US$ 15,305 per ton due to concerns about supply disruptions from the region, which produces over half of global nickel output. The government action, citing permit violations as part of a broader crackdown on illegal mining, highlighted existing supply constraints from high rainfall and low mining quotas affecting Indonesian smelters, with ripple effects also visible in copper and aluminum prices.

- In January 2025, research conducted on India's Malanjkhand chalcopyrite deposits by a team from IIT Dhanbad demonstrated that integrating an ester-based collector blend with conventional collecting agents significantly enhances flotation performance, achieving copper grade improvements of at least 15% and recovery rates exceeding 93% under optimized conditions. Statistical analysis using Box-Behnken design methodology and response surface optimization validated that precise dosing of sodium silicate, SIPX collector, and the novel ester-based co-collector can substantially increase both ore recovery and concentrate grade.

Companies Covered in Xanthates Market

- Yantai Aotong Chemical Co., Ltd.

- Senmin International (Pty) Ltd

- CTC Mining

- SNF Group

- Coogee Chemicals

- Yantai Humon Chemical Auxiliary Co. Ltd

- Tieling Flotation Reagent Co., Ltd.

- Vanderbilt Holding Company, Inc.

- Rao A. Group of Companies

- QiXia TongDa Flotation Reagent Co., Ltd.

- Orica Australia Pty Ltd

Frequently Asked Questions

The global xanthates market is projected to reach US$ 580.7 million in 2025.

Rising mining activities for sulfide ores and expanding rubber vulcanization needs are driving the market.

The market is poised to witness a CAGR of 5.4% from 2025 to 2032.

The shift to eco-friendly formulations open novel and lucrative opportunities for market players, as they enable recovery improvements while complying with EU and EPA sustainability regulations.