- Medical Devices

- Urolithiasis Management Devices Market

Urolithiasis Management Devices Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Urolithiasis Management Devices Market by Product Type (Lithotripsy Devices, Ureteroscopes, Stone Retrieval Devices, Ureteral Stents, Catheters, Ancillary Devices, and Others), Treatment Type (Extracorporeal Shock Wave Lithotripsy (ESWL), Intracorporeal Lithotripsy, Percutaneous Nephrolithotomy (PCNL), Ureteroscopy-based Stone Removal, and Others), Application (Kidney Stone Management, Ureteral Stones, Bladder Stones, and General Urinary Tract Stone Management) End-user, and Regional Analysis from 2026 - 2033

Urolithiasis Management Devices Market Share and Trend Analysis

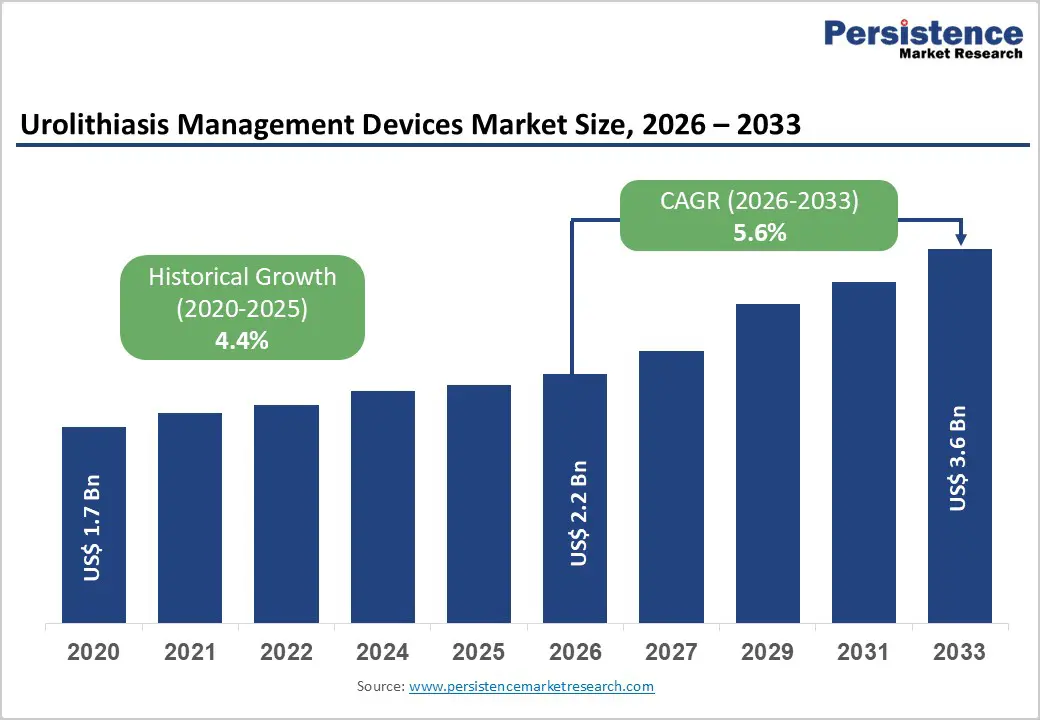

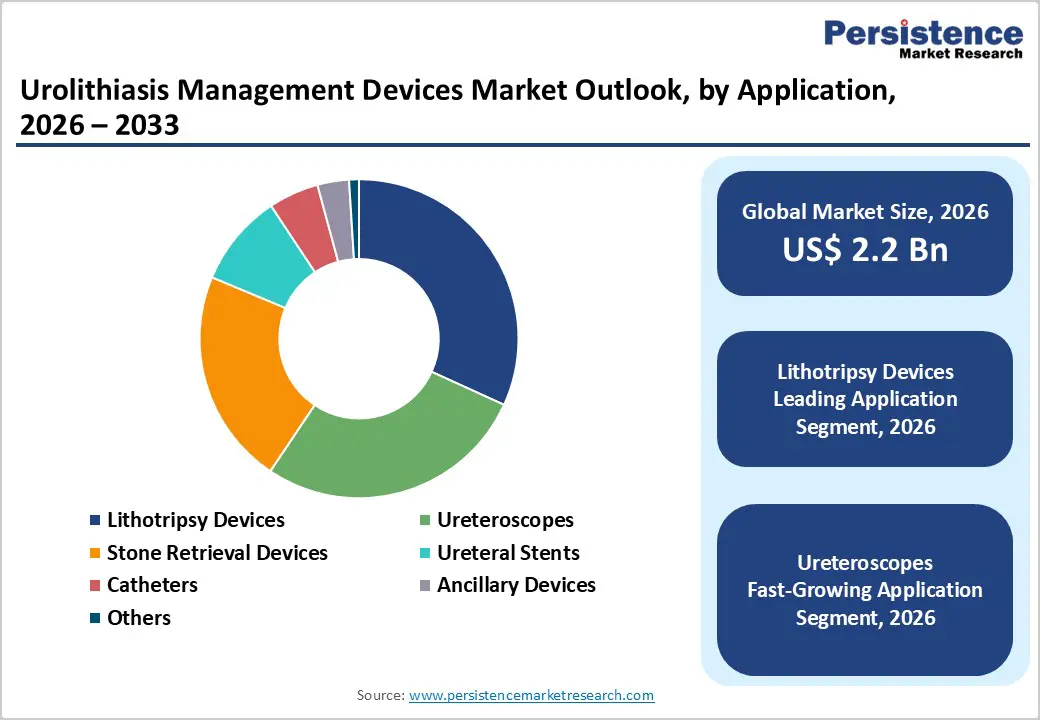

The global urolithiasis management devices market size is estimated to grow from US$ 2.2 billion in 2026 to US$ 3.6 billion by 2033. The market is projected to record a CAGR of 5.6% during the forecast period from 2026 to 2033. The growing incidence of urinary stone disease is significantly influencing the demand for advanced urolithiasis management solutions across healthcare systems. Increasing prevalence of kidney and ureteral stones, largely driven by lifestyle changes, dehydration, dietary habits, and metabolic disorders, is resulting in higher procedural volumes globally. Healthcare providers are increasingly adopting minimally invasive treatment techniques such as ureteroscopy, laser lithotripsy, and extracorporeal shock wave lithotripsy (ESWL), as these approaches offer reduced recovery time, lower complication rates, and improved patient comfort compared to conventional surgical methods. Advancements in endourology technologies are further accelerating this trend. Innovations, including high-power holmium and thulium fiber lasers, enhanced flexible ureteroscopes, and improved stone retrieval systems, are enabling precise fragmentation and efficient stone clearance.

These technologies also support better visualization and maneuverability during procedures, contributing to higher success rates. Additionally, the growing availability of specialized urology centers and expanding access to advanced healthcare infrastructure are supporting increased adoption of these devices.

Key Industry Highlights:

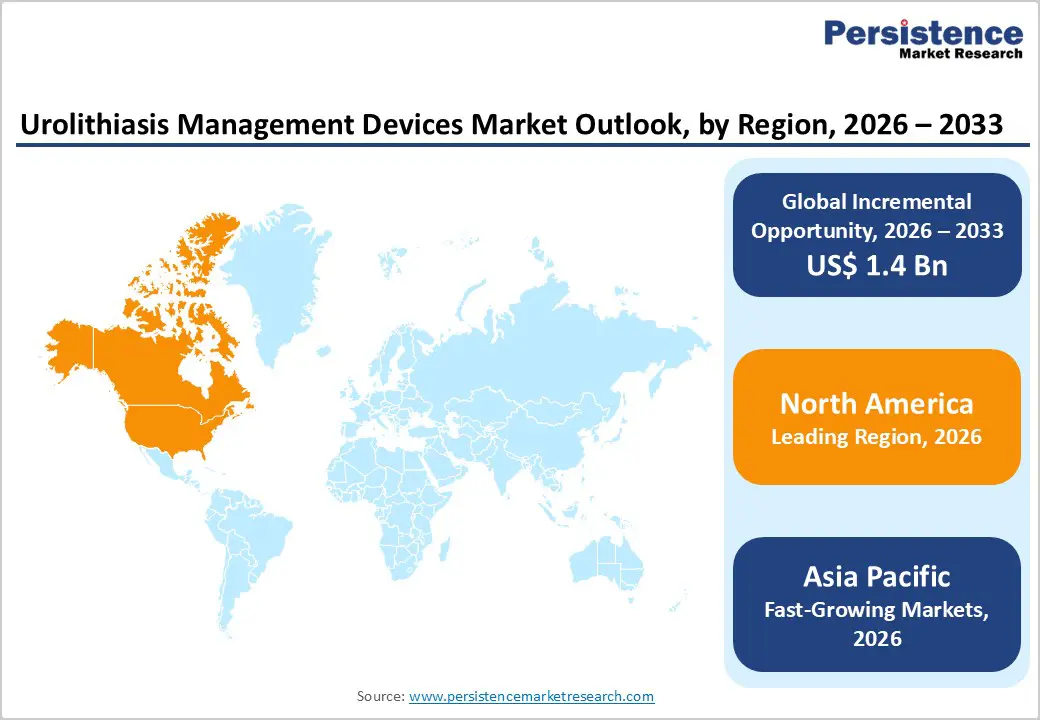

- Leading Region: North America accounts for 48.5% of global revenue, supported by advanced urology infrastructure, widespread adoption of minimally invasive procedures, strong reimbursement frameworks, and the presence of major medical device manufacturers.

- Fastest-Growing Region: Asia Pacific is witnessing the fastest growth, driven by rising healthcare expenditure, expanding hospital networks, increasing patient awareness, and a growing burden of kidney stone disease across densely populated countries.

- Leading Product Segment: Lithotripsy devices dominate the market due to their extensive use in non-invasive and minimally invasive stone fragmentation procedures, particularly in hospital-based urology departments.

- Fastest-Growing Product Segment: Ureteroscopes are gaining rapid traction as demand increases for minimally invasive endoscopic procedures that offer higher precision, improved patient outcomes, and shorter recovery durations.

- Leading Application Segment: Kidney stone management holds the largest share, supported by high global prevalence and the significant number of procedures performed for renal calculi treatment.

- Fastest-Growing Application Segment: Ureteral stones are expanding at a notable pace due to increasing adoption of ureteroscopy and laser-based treatments for effective and targeted stone removal.

| Key Insights | Details |

|---|---|

|

Urolithiasis Management Devices Market Size (2026E) |

US$ 2.2 Bn |

|

Market Value Forecast (2033F) |

US$ 3.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.4% |

Market Dynamics

Driver - Rising Global Burden of Urolithiasis and Increasing Preference for Minimally Invasive Treatment Approaches

A key factor accelerating demand for advanced stone management solutions is the steady increase in urolithiasis incidence worldwide, driven by changing dietary habits, sedentary lifestyles, dehydration, and metabolic disorders. The condition has become highly recurrent in nature, requiring repeated clinical intervention and long-term management, thereby increasing procedural volumes across healthcare systems. At the same time, there is a clear clinical shift away from open surgical approaches toward minimally invasive and non-invasive techniques such as ureteroscopy, laser lithotripsy, and extracorporeal shock wave lithotripsy (ESWL). These procedures offer reduced post-operative complications, shorter hospital stays, and faster recovery, making them highly preferred by both clinicians and patients.

Technological advancements have significantly strengthened this transition. Innovations such as high-power holmium and thulium fiber lasers, flexible digital ureteroscopes, and improved stone retrieval devices have enhanced precision, stone-free rates, and procedural efficiency. Furthermore, the increasing availability of advanced urology infrastructure in hospitals and specialty clinics is supporting the adoption of these devices. Growing awareness regarding early diagnosis and treatment, coupled with improved access to healthcare services, is further contributing to demand. As healthcare systems continue to emphasize patient-centric care and better clinical outcomes, the reliance on technologically advanced urolithiasis management devices is expected to rise steadily.

Restraints - High Capital Investment and Procedural Complexity Limiting Adoption Across Smaller Healthcare Facilities

The adoption of advanced urolithiasis management devices is constrained by the substantial capital investment required for acquiring and maintaining sophisticated equipment. Devices such as laser lithotripters, flexible ureteroscopes, and imaging-integrated systems involve high upfront costs, along with recurring expenses related to maintenance, sterilization, and replacement of delicate components. For smaller hospitals, ambulatory centers, and healthcare facilities in cost-sensitive regions, these financial requirements can act as a significant barrier, often delaying procurement decisions or limiting access to advanced treatment options.

Additionally, procedural complexity presents another challenge. Many minimally invasive stone removal techniques require specialized training, technical expertise, and experience to achieve optimal outcomes. A shortage of skilled urologists and trained support staff in certain regions restricts the effective utilization of these devices. Furthermore, concerns related to equipment durability, especially with reusable flexible scopes, and the need for stringent sterilization protocols add to operational burdens. Regulatory compliance, including safety standards and quality assurance requirements, also increases administrative and operational complexity. These combined financial and logistical challenges can slow the adoption rate, particularly in emerging healthcare systems where resource allocation remains a critical concern.

Opportunity - Expansion of Endourology in Emerging Markets and Advancements in Single-Use and Laser Technologies

Significant growth opportunities are emerging from the rapid expansion of healthcare infrastructure in developing regions, where access to specialized urology care is improving. Countries across Asia Pacific, Latin America, and the Middle East are investing in hospital upgrades, surgical capabilities, and medical technology adoption, creating a favorable environment for advanced stone management devices. As awareness regarding urolithiasis and its complications increases, more patients are seeking timely and effective treatment, leading to higher procedural volumes. Portable and versatile devices that can be integrated into diverse clinical settings are gaining importance in these evolving healthcare ecosystems.

Another major opportunity lies in the development and adoption of single-use (disposable) ureteroscopes and next-generation laser systems. Single-use devices help eliminate cross-contamination risks, reduce reprocessing costs, and ensure consistent performance, making them particularly attractive for high-volume centers and facilities with limited sterilization infrastructure. Meanwhile, innovations such as thulium fiber lasers offer improved efficiency, finer stone dusting capabilities, and reduced operative time. Integration of digital imaging, real-time visualization, and enhanced ergonomics is further improving procedural outcomes. As manufacturers continue to focus on innovation, cost optimization, and geographic expansion, these advancements are expected to unlock substantial growth potential in the global market.

Category-wise Analysis

By Product Insights

Lithotripsy devices are projected to account for 31.8% of global revenue in 2026, establishing them as the leading product category in the urolithiasis management devices market. Their dominance is primarily driven by the widespread preference for non-invasive and minimally invasive stone treatment approaches, particularly extracorporeal shock wave lithotripsy (ESWL) and laser-based systems. These technologies enable effective fragmentation of urinary stones with reduced patient discomfort, shorter hospital stays, and minimal procedural complications. Continuous advancements in laser lithotripsy, including improved precision and compatibility with flexible ureteroscopes, have further strengthened their clinical utility. Additionally, increasing incidence of kidney stones, growing awareness regarding early treatment, and rising availability of advanced urology infrastructure are accelerating adoption across hospitals and specialty clinics. As healthcare providers prioritize efficient, patient-friendly treatment modalities, lithotripsy devices continue to remain central to modern stone management practices.

By Application Insights

Kidney stone management is expected to capture 52.6% of the market in 2026, making it the largest application segment. The high share is attributed to the significant global prevalence of nephrolithiasis, which continues to rise due to dietary patterns, dehydration, and metabolic disorders. A large proportion of urological procedures, including lithotripsy and ureteroscopy, are performed for kidney stones, driving consistent demand for related devices. Technological advancements such as high-power laser systems and improved imaging guidance have enhanced treatment success rates and reduced recurrence risks. Furthermore, increasing awareness about early diagnosis and the availability of minimally invasive treatment options have encouraged more patients to seek timely intervention. Healthcare systems are also focusing on reducing complications associated with untreated stones, further supporting procedural volumes. As a result, kidney stone management remains the primary revenue-generating application within the market.

By End-user Insights

Hospitals are anticipated to hold 56.8% of total market revenue in 2026, reinforcing their position as the leading end-user segment. This dominance is largely due to the availability of advanced surgical infrastructure, skilled urologists, and the capacity to handle complex stone cases requiring multidisciplinary care. Hospitals serve as primary centers for procedures such as percutaneous nephrolithotomy (PCNL) and advanced ureteroscopy, which require specialized equipment and post-operative monitoring. Additionally, they manage high patient inflow, including emergency and recurrent stone cases, contributing significantly to device utilization rates. Integration of advanced imaging systems, operating room technologies, and digital health platforms further enhances procedural efficiency and outcomes. Hospitals also have greater financial capacity to invest in high-end lithotripsy and endourology systems. With rising hospitalization rates and expanding urology departments globally, hospitals continue to be the key contributors to market revenue.

Regional Insights

North America Urolithiasis Management Devices Market Trends

North America is projected to account for 48.5% of global revenue in 2026, maintaining its leadership in the urolithiasis management devices market. The United States represents the largest contributor, supported by a highly advanced healthcare system and strong adoption of minimally invasive urological procedures. High prevalence of kidney stones, influenced by dietary habits and lifestyle factors, continues to drive procedural demand across the region. Healthcare providers extensively utilize advanced technologies such as laser lithotripsy and flexible ureteroscopy to improve treatment outcomes and reduce recovery time.

The region benefits from the strong presence of leading medical device manufacturers and continuous innovation in endourology solutions, including single-use ureteroscopes and high-power laser systems. Favorable reimbursement policies and high healthcare expenditure further support adoption of advanced treatment modalities. Additionally, increasing preference for outpatient procedures is driving growth in ambulatory surgical centers, expanding the overall treatment landscape. Ongoing investments in healthcare infrastructure, combined with a focus on improving patient outcomes and reducing hospital stays, continue to strengthen North America’s dominant position in the market.

Europe Urolithiasis Management Devices Market Trends

Europe represents a well-established yet steadily growing market for urolithiasis management devices, supported by strong public healthcare systems and increasing focus on minimally invasive treatments. Countries such as Germany, the United Kingdom, France, Italy, and Spain are key contributors, with widespread availability of advanced urology services. The region is witnessing increasing adoption of laser-based lithotripsy and flexible ureteroscopy, driven by their clinical effectiveness and reduced complication rates.

Rising incidence of urolithiasis, particularly among the aging population, is contributing to sustained procedural demand. Lifestyle-related factors, including dietary habits and obesity, are also influencing disease prevalence. European healthcare providers emphasize cost-effective treatment approaches, encouraging the use of technologies that reduce hospitalization duration and improve patient throughput. Additionally, regulatory standardization across the European Union supports the introduction of innovative medical devices. Investments in hospital modernization, training programs for urologists, and increasing awareness of early diagnosis further contribute to market expansion. Although growth is moderate compared to emerging regions, consistent demand and technological adoption ensure long-term stability.

Asia Pacific Urolithiasis Management Devices Market Trends

Asia Pacific is expected to register the fastest growth, with a CAGR of approximately 7.6% between 2026 and 2033, driven by rapid healthcare development and increasing burden of kidney stone disease. Countries such as China, India, Japan, and South Korea are experiencing rising incidence of urolithiasis due to changing dietary patterns, urbanization, and climatic conditions leading to dehydration. This has significantly increased demand for effective and accessible treatment solutions.

Healthcare infrastructure across the region is undergoing substantial transformation, with governments investing in hospital expansion, urology departments, and advanced surgical technologies. The adoption of minimally invasive procedures such as ureteroscopy and laser lithotripsy is increasing, particularly in urban healthcare centers. Private hospitals are also playing a crucial role by investing in advanced devices to enhance patient care and attract medical tourism. Collaborations between global medical device companies and regional healthcare providers are facilitating technology transfer and skill development. Rising healthcare expenditure, growing patient awareness, and improved access to specialized care are collectively positioning Asia Pacific as a high-growth market over the forecast period.

Competitive Landscape

The global urolithiasis management devices market is highly competitive, with strong participation from companies such as Allengers Medical Systems Ltd., Boston Scientific Corporation, Becton, Dickinson and Company, Cook Medical, and CONMED Corporation. These players leverage strong urology portfolios, advanced endourology technologies, established hospital networks, and global distribution capabilities.

Competitive strategies focus on developing minimally invasive solutions such as laser lithotripsy systems and flexible ureteroscopes, enhancing procedural efficiency, and improving patient outcomes. Companies are investing in product innovation, strategic collaborations, and expansion in emerging markets, intensifying competition and driving sustained growth.

Key Developments:

- In January 2026, Ventaris Surgical, Inc., a San Carlos–based firm developing next-generation kidney stone treatment systems, announced the successful close of a $30 million Series A funding round. The round was led by Longitude Capital, with participation from Vensana Capital, along with existing investors Atypical Ventures, Neotribe Ventures, and Boutique Venture Partners.

- In January 2026, SonoMotion, a venture-backed firm focused on non-invasive kidney stone treatments, announced that it received U.S. FDA 510(k) clearance for its Break Wave lithotripsy device. The system utilizes low-pressure focused ultrasound to fragment kidney stones by generating standing stress waves within the stone under real-time ultrasound guidance. This approach enables a completely non-invasive procedure without the need for anesthesia, allowing patients to eat and drink beforehand and resume normal activities, including driving, immediately after treatment.

- In March 2024, Calyxo, Inc. received U.S. FDA clearance for its redesigned CVAC System, which supports a minimally invasive approach to kidney stone treatment. The updated system has already been used in procedures involving more than 50 patients.

Companies Covered in Urolithiasis Management Devices Market

- Allengers Medical Systems Ltd.

- Boston Scientific Corporation

- Becton, Dickinson and Company

- Cook Medical LLC

- CONMED Corporation

- DirexGroup

- Dornier MedTech GmbH

- KARL STORZ SE & Co. KG

- Wuhan Potent Optotronic Technology Co., Ltd.

- HealthTronics, Inc.

- Lumenis Be Ltd.

- Olympus Corporation

- Richard Wolf GmbH

- Siemens Healthineers AG

- Electro Medical Systems S.A. (EMS)

- Others

Frequently Asked Questions

The global urolithiasis management devices market is projected to be valued at US$ 2.2 Bn in 2026.

Rising global prevalence of kidney stones, increasing adoption of minimally invasive procedures (especially laser lithotripsy and ureteroscopy), and growing healthcare infrastructure are driving demand for urolithiasis management devices.

The global urolithiasis management devices market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Expansion in emerging markets, increasing shift toward outpatient settings (ASCs), and technological advancements such as single-use ureteroscopes and thulium fiber lasers present significant growth opportunities.

Allengers Medical Systems Ltd., Boston Scientific Corporation, Becton, Dickinson and Company, Cook Medical, and CONMED Corporation are some of the key players in the urolithiasis management devices market.