- Off-Road Equipment & Machinery

- Turf Care Equipment Market

Turf Care Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Turf Care Equipment Market By Fuel Type (Gasoline, Diesel), Equipment Type (Turf Sprayers, Mowers, Turf Tractors, Aerators, Utility Vehicles), End-user (Commercial Lawn and Turf, Sports Lawn and Turf), and Regional Analysis for 2025 - 2032

Turf Care Equipment Market Size and Trends Analysis

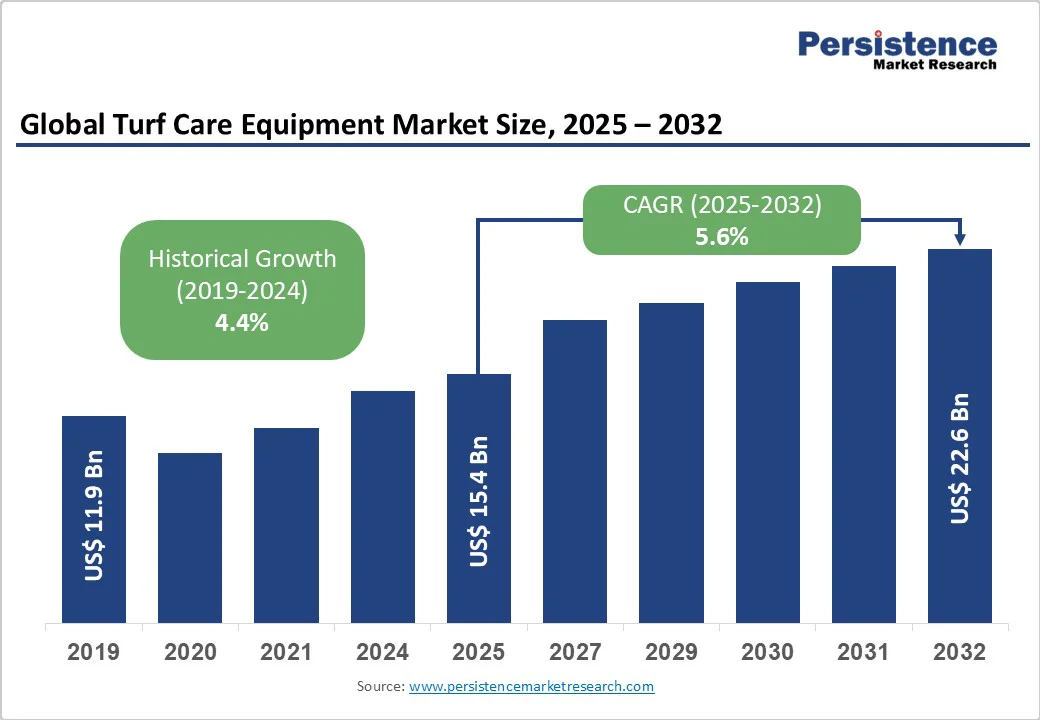

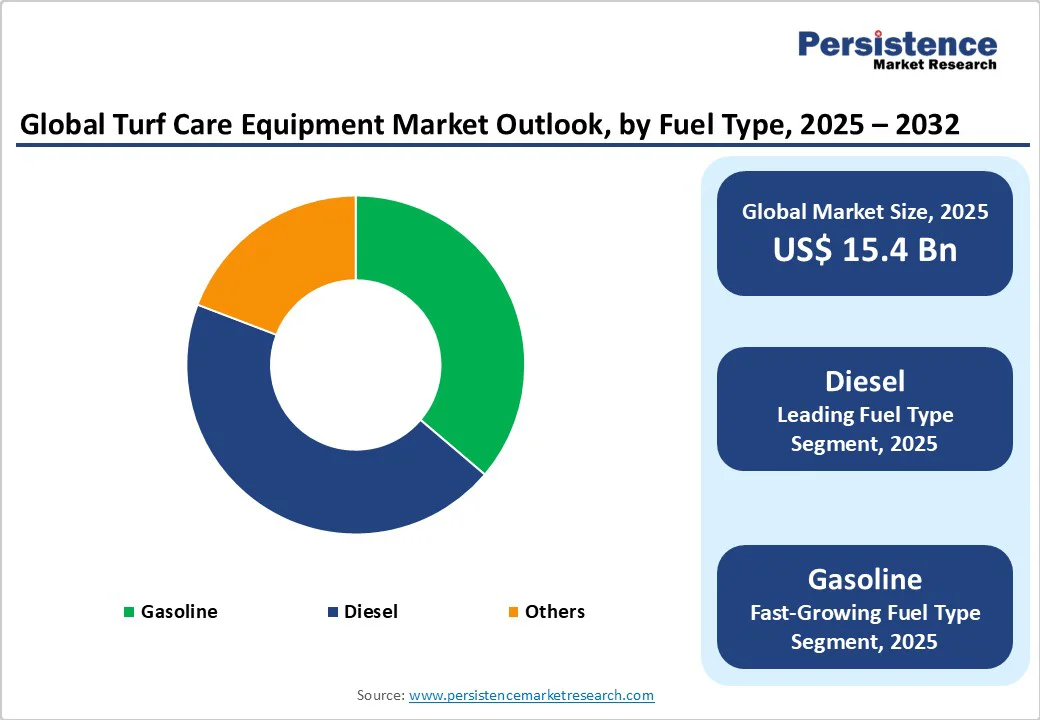

The global turf care equipment market size is likely to be valued at US$15.4 Billion in 2025 and is estimated to reach US$22.6 Billion in 2032, growing at a CAGR of 5.6% during the forecast period 2025 - 2032, driven by rising interest in landscaping, expanding sports infrastructure, and increasing emphasis on outdoor aesthetics. The proliferation of golf courses and stadiums also supports equipment adoption.

Key Industry Highlights

- Leading Fuel Type: Diesel holds nearly 44.6% share in 2025, due to its durability, fuel efficiency, and ability to handle large-scale turf maintenance tasks.

- Dominant Equipment Type: Turf sprayers, approximately 26.3% of the turf care equipment market share in 2025, owing to their precision in ensuring healthy turf while reducing chemical waste and labor costs.

- Key End-user: Sports lawn and turf recorded around 39.1% share in 2025, as they demand consistent maintenance for safety and performance.

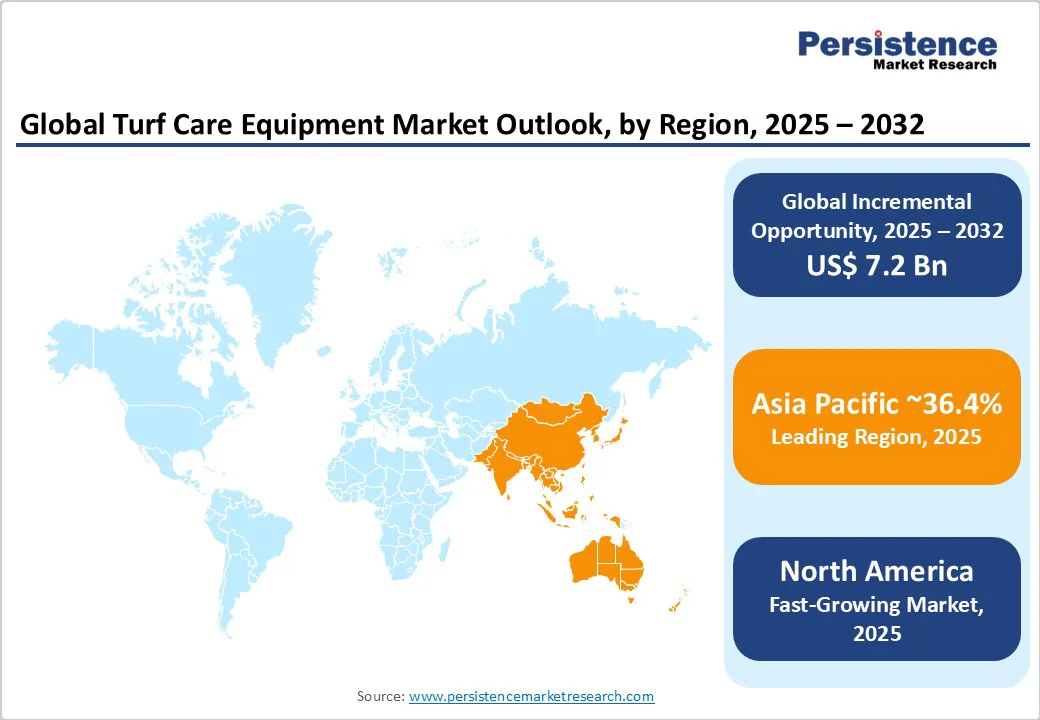

- Leading Region: Asia Pacific with about 36.4% share in 2025, spurred by expansion of golf courses and government-led landscaping projects.

- Fastest-growing Region: North America, nearly 30.1% share in 2025, due to novel sports infrastructure and widespread adoption of smart equipment.

- New Brand Launch: In October 2025, Denmark-based Traqnology, a pioneer in GPS-driven turf management systems, announced its official U.K. launch. It aims to bring two innovations to the country, namely, a unique GPS line marking system and Turftraq, a precision mowing solution.

| Key Insights | Details |

|---|---|

| Turf Care Equipment Market Size (2025E) | US$15.4 Bn |

| Market Value Forecast (2032F) | US$22.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Improved Property Appeal and Market Value

Maintaining well-groomed lawns and landscapes plays a key role in boosting the attractiveness and perceived value of a property. For residential homes, neatly trimmed lawns and vibrant gardens not only create a welcoming atmosphere but also improve curb appeal, making properties more appealing to potential buyers.

In the commercial sector, visually appealing outdoor spaces such as hotel gardens, corporate campuses, or retail complexes can improve customer impressions and satisfaction. This trend has prompted property owners and facility managers to invest in unique turf care equipment to ensure consistent maintenance.

High Efficiency in Maintaining Large Areas

The demand for commercial-grade turf equipment is rising due to its ability to manage expansive areas quickly and effectively. Ride-on mowers, professional aerators, and high-capacity sprayers drastically reduce the labor and time required for upkeep, which is mainly important for sports facilities, resorts, and large public parks.

These tools allow groundskeepers to maintain consistent turf quality over vast spaces without compromising efficiency. For instance, in 2023, several golf courses in France integrated hybrid-electric ride-on mowers, enabling them to cover extensive fairways while reducing fuel consumption and operational time. This focus on efficiency and performance is pushing the adoption of professional turf care machinery across various regions.

Barrier Analysis - High Costs of Unique Turf Equipment

The financial barrier associated with professional-grade turf care machinery can restrain market expansion, particularly for small property owners or community facilities. Novel ride-on mowers, robotic equipment, and precision sprayers require substantial upfront investment, while ongoing maintenance, fuel, and spare parts add to operating costs. This can discourage adoption among small-scale users or organizations with limited budgets.

In 2024, several UK-based municipal parks reported delaying purchases of hybrid-electric turf mowers due to high procurement costs, despite recognizing the efficiency and sustainability benefits these machines provide. Consequently, cost sensitivity remains a key restraint in the widespread adoption of modern turf care equipment.

Seasonal Dependence Limiting Equipment Utilization

The demand for turf care equipment is heavily influenced by seasonal variations that restrict consistent sales and usage throughout the year. In cold regions of Europe and North America, lawn maintenance activities decline sharply during winter, leading to idle equipment and reduced income for service providers. This uneven demand cycle makes it difficult for manufacturers and dealers to maintain stable production and inventory levels.

Small landscaping businesses often delay purchases due to limited year-round work. For example, in Canada and the northern parts of the U.S., turf care equipment rentals drop significantly between November and March, affecting market turnover. Such seasonality also discourages long-term investments in novel machines such as robotic mowers or sprayers.

Opportunity Analysis - Emergence of Autonomous Mowing Systems for Commercial Use

The development of autonomous mowing systems is creating new growth opportunities for the market. These systems, equipped with GPS navigation, AI-based obstacle detection, and adaptive cutting algorithms, allow large-scale turf areas such as sports complexes, resorts, and golf courses to be maintained with minimal human intervention.

They improve operational efficiency, reduce labor costs, and ensure consistent mowing quality. With rising labor shortages and the demand for precision turf care, the shift toward autonomous solutions is gaining momentum across Europe and North America.

Integration of IoT and Cloud-based Fleet Management

IoT-enabled fleet management software is transforming how large-scale turf care operations are conducted. These platforms allow operators to track, schedule, and monitor multiple machines such as mowers, sprayers, and aerators across extensive landscapes in real time.

Cloud-based analytics provide insights into fuel consumption, maintenance schedules, and equipment performance, helping users reduce downtime and optimize productivity. Companies such as John Deere have already integrated connected technologies into their turf care portfolios, allowing remote diagnostics and predictive maintenance.

Category-wise Analysis

Fuel Type Insights

Diesel-powered turf care equipment is predicted to account for approximately 44.6% of the share in 2025, spurred by its durability, high torque, and efficiency for large-scale and professional turf maintenance tasks. Diesel engines can handle prolonged heavy-duty operations, making them ideal for golf courses, sports fields, and commercial landscaping.

For example, John Deere’s diesel-powered large mowers remain popular in golf courses across Europe and North America due to their fuel efficiency and reliability in continuous operations.

Gasoline-powered turf care equipment is gaining traction as it delivers light and compact solutions suitable for residential and small commercial applications. Gasoline engines allow greater maneuverability and are easier to start and maintain compared to diesel.

Companies, such as Husqvarna and Toro, have reported increased sales of gasoline-powered ride-on mowers in urban areas, mainly where small plots of land require flexible and easy-to-use equipment.

Equipment Type Insights

Turf sprayers are projected to lead with a share of nearly 26.3% in 2025 as they provide precise application of fertilizers, herbicides, and pesticides, ensuring healthy and uniform turf growth. Professional groundskeepers and golf courses favor sprayers for their efficiency in covering large areas while minimizing chemical waste.

For instance, Toro’s Precision Sprayer series, launched in 2023, integrates GPS mapping and variable-rate application technology, allowing operators to treat specific sections of turf accurately, which reduces costs and environmental impact.

Mowers are speculated to capture a share of around 19.7% in 2025, backed by their essential role in maintaining aesthetic and functional turf quality across residential, commercial, and sports landscapes. The consistent demand for well-manicured lawns, parks, and sports fields propels ongoing adoption.

Recent trends show a shift toward battery-powered and robotic mowers. Husqvarna’s Automower 535 AWD, for example, has gained popularity in golf courses and urban estates across Europe for its ability to operate autonomously on uneven terrains, showcasing a blend of reliability and technological development.

End-user Insights

Sports lawn and turf are poised to lead with a share of about 39.1% in 2025, as they require consistent, high-quality maintenance to ensure safety, performance, and visual appeal. Stadiums, football fields, and public sports grounds demand specialized equipment for mowing, aeration, fertilization, and pest control.

For example, in 2024, Arsenal FC upgraded its Emirates Stadium turf management program using automated turf care systems, highlighting the surging reliance on novel equipment to maintain premium playing surfaces.

Golf turfs are a key end user due to the stringent standards for smoothness, density, and health of the grass, which directly affect play quality and aesthetics. Golf courses use a combination of mowers, sprayers, and aerators to maintain greens, fairways, and tees.

Various companies have introduced GPS-enabled, hybrid-electric mowing and spraying equipment specifically for golf courses, allowing precise turf care while reducing labor and environmental impact. The premium nature of golf facilities augments continuous investment in high-performance turf care equipment.

Regional Insights

Asia Pacific Turf Care Equipment Market Trends

Asia Pacific is estimated to account for approximately 36.4% of the market share in 2025, spurred by increased sports infrastructure and rising interest in landscaping. China is estimated to remain at the forefront of growth. Technological developments are changing the market, with companies introducing electric and hybrid equipment to meet environmental standards and reduce operational costs. These developments are gaining traction in Asia Pacific, specifically in Japan and South Korea, where precision and sustainability are prioritized in turf maintenance.

The competitive landscape in Asia Pacific is marked by a mix of global and regional players. Companies such as Deere & Company, The Toro Company, and Husqvarna AB are expanding their presence through strategic partnerships and acquisitions. For example, in October 2023, Metalcraft of Mayville acquired Bluebird Turf Products, indicating a trend toward consolidation in the market.

North America Turf Care Equipment Market Trends

In 2025, North America is expected to hold a share of about 30.1%. Economic conditions play a key role in influencing the regional market. Factors such as fluctuating fuel prices, interest rates, and economic uncertainties can impact consumer spending and investment in turf care equipment.

For instance, high interest rates and economic uncertainty have led to a decline in demand for large turf equipment, as evidenced by John Deere's reported 30% drop in sales for fiscal 2025 in the U.S. and Canada. Also, the oversupply of used equipment has contributed to the slowdown in sales.

In response to market challenges and opportunities, companies are making strategic investments to strengthen their positions. John Deere, for example, announced a US$20 Billion investment over the next decade to improve its U.S. operations, focusing on product development, technology integration, and manufacturing capabilities. This commitment emphasizes the company's dedication to innovation and meeting the evolving requirements of the turf care equipment market.

Europe Turf Care Equipment Market Trends

In Europe, the integration of technology is transforming the market. Consumers are increasingly seeking equipment that provides efficiency, sustainability, and ease of use. This trend is evident in the high popularity of battery-powered and robotic lawnmowers, which are gaining traction among homeowners and commercial users. Manufacturers are responding by developing unique products that cater to these demands, aiming to improve user experience and reduce environmental impact.

Germany is a dominant hub in Europe. The country's emphasis on environmental sustainability has led to a rising preference for battery-powered and robotic lawnmowers. Companies such as Husqvarna have reported increased sales in the country, propelled by favorable weather conditions and a shift toward eco-friendly products. The U.K. is seeing a steady demand for compact and efficient turf care equipment. In France, the market is broadening owing to increased interest in home gardening and outdoor activities.

Competitive Landscape

Key companies in the turf care equipment market are investing heavily in research and development to introduce unique products. For instance, in 2023, John Deere launched a hybrid electric tractor aimed at reducing emissions in turf maintenance. Similarly, Husqvarna partnered with a tech company in 2024 to integrate AI-based analytics into its mowing equipment, improving efficiency and precision.

Key Industry Developments

- In October 2025, Honda launched Honda ProZision battery-powered ZTR lawn mowers. These are designed for professional-level durability, comfort, and cut quality.

- In September 2025, Vanguard joined hands with Classen to bring powerful, battery-driven solutions to the turf care industry. Classen’s new TR-20eV Turf Rake is now powered by the Vanguard 48V 1.5kWh1 (Si1.5) swappable battery pack, delivering a quiet and emission-free alternative for commercial turf renovation.

Companies Covered in Turf Care Equipment Market

- Husqvarna AB

- The Toro Company

- Deere & Company

- Honda Motor Co.

- MTD Products, Inc.

- Kubota Corporation

- Intimidator Group

- BLACK+DECKER Inc.

- Briggs & Stratton Corporation

- Textron Inc.

Frequently Asked Questions

The turf care equipment market is projected to reach US$15.4 Billion in 2025.

Increasing preference for well-maintained outdoor spaces and expansion of sports infrastructure are the key market drivers.

The turf care equipment market is poised to witness a CAGR of 5.6% from 2025 to 2032.

Development of fully autonomous turf management solutions and digitalization through connected equipment are the key market opportunities.

Husqvarna AB, The Toro Company, and Deere & Company are a few key market players.