- Retail

- Tobacco Market

Tobacco Market Size, Share, and Growth Forecast 2026 - 2033

Tobacco Market by Leaf Type (Virginia, Burley, Nicotiana rustica, Oriental, Others), by Product Type (Flue-cured Tobacco, Burley Tobacco, Dark-fired Tobacco, Perique, Oriental (Turkish) Tobacco, Connecticut Shade Tobacco, Others), Distribution Channel (Hypermarket & supermarket, Convenience stores, Specialty stores, Online sales channel), End-user, and Regional Analysis, 2026 - 2033

Tobacco Market Size and Trend Analysis

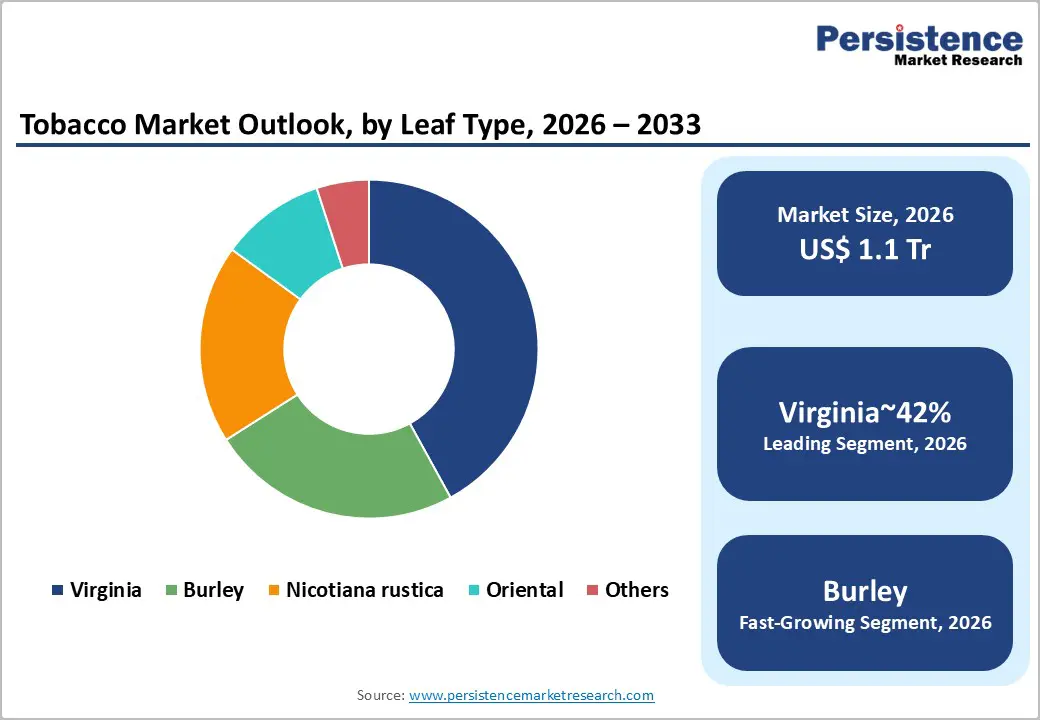

The global Tobacco Market size is likely to be valued at US$ 1.1 Trillion in 2026 and is expected to reach US$ 1.5 Trillion by 2033, growing at a CAGR of 4.1% during the forecast period from 2026 and 2033. Supportive agricultural policies in developing regions sustain raw material supply chains while multinational manufacturers expand into premium and smokeless segments targeting health-conscious demographics transitioning from traditional cigarettes.

Key Industry Highlights:

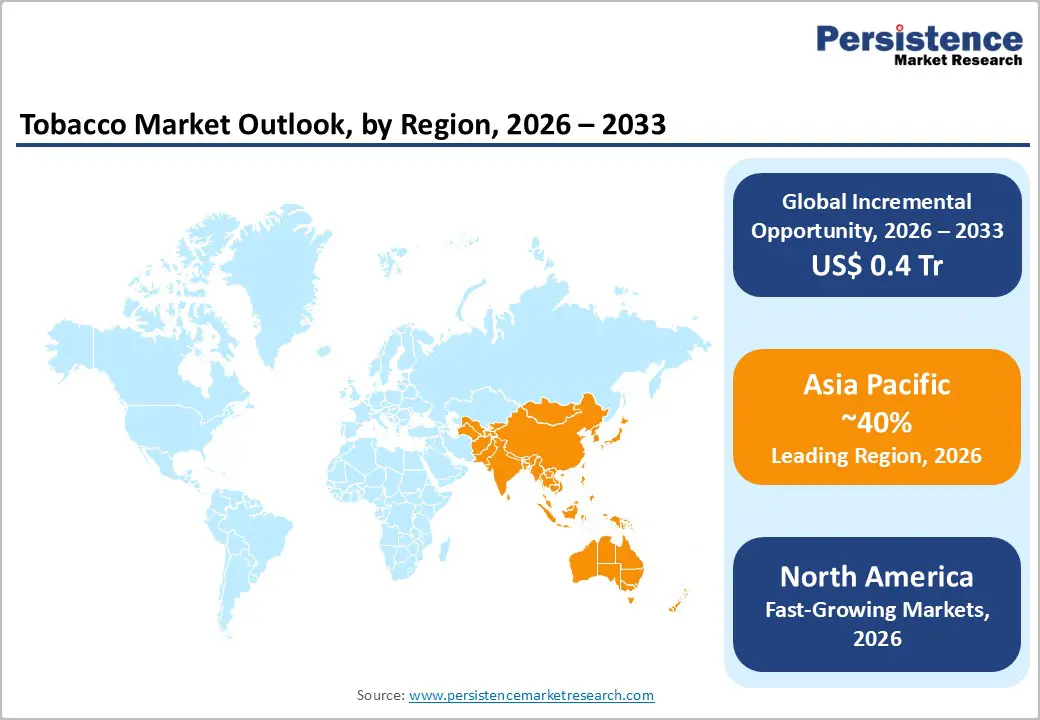

- Leading Region: Asia Pacific dominates Tobacco Market consuming 40% global volume led by China and India. State monopolies and cultural acceptance sustain structural demand.

- Fastest Growing Region: North America is the fastest-growing tobacco market despite an 11.5% adult smoking prevalence, aided by a strong manufacturing and distribution infrastructure.

- Dominant Segment: Cigarettes command 78% volume share among 1.1 billion smokers. Marlboro, Winston multinational infrastructure produces 6 trillion units annually.

- Fastest Growing Segment: Smokeless tobacco expands 12% CAGR through snus, nicotine pouches. Sweden 20% prevalence demonstrates substitution viability.

- Key Market Opportunity: Heated-not-burned products target 500 million smokers willing to switch. Regulatory differentiation enables premium pricing.

| Key Insights | Details |

|---|---|

|

Tobacco Market Size (2026E) |

US$ 1.1 Trillion |

|

Market Value Forecast (2033F) |

US$ 1.5 Trillion |

|

Projected Growth CAGR(2026-2033) |

4.1% |

|

Historical Market Growth (2020-2025) |

3.6% |

Market Dynamics

Drivers - Rising Population and Income Levels Sustain Strong Tobacco Demand across Emerging Asia Pacific Economies

Strong population growth and rising disposable incomes across Asia Pacific continue to support tobacco consumption, even as regulations tighten in developed countries. According to the World Health Organization, there are 1.3 billion tobacco users globally, with nearly 80% living in low- and middle-income countries where cultural acceptance remains high. India has around 120 million adult smokers, with bidi consumption accounting for 45% of total cigarette-equivalent usage, supported by decentralized production and low pricing.

Indonesia has nearly 70 million smokers who prefer kretek cigarettes, driven by their unique flavor and cultural significance. These long-standing consumption habits show resilience against Western-style regulatory measures. At the same time, multinational companies are expanding premium product portfolios to target growing middle-class consumers seeking aspirational and status-oriented brands, strengthening revenue growth opportunities in these high-potential markets.

Rapid Adoption of Smokeless and Heated Products Driving Revenue Diversification for Global Tobacco Companies

Tobacco manufacturers are successfully shifting consumers toward reduced-risk alternatives such as snus, nicotine pouches, and heated tobacco products. Swedish Match has reported a 15% compound annual growth rate in ZYN nicotine pouch sales across 15 markets, capturing a 25% share of the U.S. market within two years of launch. Philip Morris International’s IQOS heated tobacco system recorded 28% global shipment growth in 2025, converting 7 million traditional smokers across 70 markets.

Regulatory authorities increasingly treat these alternatives differently from combustible cigarettes, enabling premium pricing strategies. Health agencies also acknowledge significantly lower exposure to harmful constituents compared to cigarette smoke. This shift supports sustainable revenue diversification, as companies leverage their established distribution networks, brand loyalty, and product innovation capabilities to accelerate the adoption of next-generation offerings worldwide.

Restraints - Strict Global Regulations and High Taxation Continue to Pressure Tobacco Industry Profitability Worldwide

The WHO Framework Convention on Tobacco Control, ratified by 182 countries, has introduced strict advertising bans, higher taxation, and plain packaging requirements that significantly limit industry profitability. Australia removed brand descriptors entirely, while European regulations mandate health warnings covering 65% of the primary packaging area. India increased GST on cigarettes from 28% to 38% between 2024 and 2025, and the Philippines banned single-stick sales, reducing impulse purchases by 30%.

These regulatory actions increase compliance costs, which now average 12% of gross revenue for manufacturers. In addition, excise taxes account for nearly 75% of retail prices across G20 countries, directly compressing margins. Together, these measures create sustained financial pressure on tobacco companies and restrict traditional marketing strategies, forcing firms to continuously adjust pricing, packaging, and supply chain structures to maintain profitability in an increasingly regulated environment.

Falling Smoking Rates in Developed Markets Reduce Volumes and Reshape Industry Growth Strategies

Public health initiatives and sustained awareness campaigns have significantly reduced smoking rates across developed markets. The U.S. Centers for Disease Control reports that adult smoking prevalence declined from 20.9% in 2005 to 11.5% in 2025. In the United Kingdom, smoking rates have fallen to 12.9%, representing 6.2 million adults. Japan has experienced a 25% volume decline over the past decade due to generational changes and strict workplace smoking bans.

Australia now records one of the world’s lowest smoking prevalence rates at 8.3%, driven by consistent taxation policies and public education programs. These structural declines reduce cigarette volumes and weaken economies of scale in mature production facilities. As a result, manufacturers face increasing pressure to reformulate products, optimize costs, and shift investments toward alternative nicotine categories to offset shrinking demand in traditional combustible segments.

Opportunity - Innovation in Reduced-Risk Products Creates Long-Term Growth Opportunities Through Regulatory Differentiation

Significant growth opportunities exist in heated tobacco and oral nicotine categories that receive comparatively favorable regulatory treatment. Philip Morris International projects that IQOS conversion rates could exceed 50% among existing smokers by 2030. British American Tobacco’s glo platform has expanded into 40 markets, achieving 12% user retention after 12 months. The U.S. FDA’s modified risk tobacco product authorization allows companies to communicate substantiated reduced-risk claims, supporting premium pricing with an average 25% price uplift.

Consumer studies show that 70% of smokers are willing to switch to scientifically validated alternatives. This combination of innovation, regulatory differentiation, and evolving consumer preferences creates strong long-term revenue potential. Established manufacturers benefit from scale, research capabilities, and distribution strength, positioning them to lead portfolio transformation while defending market share against emerging competitors.

Premiumization and Digital Distribution Expansion Strengthen Revenue Potential Across Emerging Tobacco Markets

Premium cigarette segments across Asia Pacific are growing at 8–10% annually in value, even as overall volumes face pressure. Consumers are increasingly trading up to international and aspirational brands. KT&G expanded its Mevius premium portfolio, achieving 15% market share gains in Vietnam, while Japan Tobacco’s Winston and Camel brands secured 22% penetration in India’s premium segment.

E-commerce penetration increased by 45% across Southeast Asia during 2024–2025, improving direct-to-consumer access and supporting premium product visibility. China Tobacco’s selective premiumization strategy delivered an 18% gross margin expansion through high-grade “zhongcao” offerings. These developments create scalable revenue opportunities through brand enhancement, digital distribution infrastructure, and targeted marketing toward nearly 300 million middle-income consumers across India, Indonesia, Bangladesh, and Pakistan, reinforcing long-term growth momentum in the region.

Category-wise Analysis

Leaf Type Insights

Virginia tobacco holds a strong 42% share of the global market, supported by its superior processing qualities and high compatibility in cigarette blends. Flue-cured Virginia makes up nearly 75% of international cigarette blends because of its high sugar content, which delivers a smooth and balanced flavor. This characteristic makes it essential for light and ultra-light cigarette segments that account for 65% of global cigarette volume.

China consumes around 2.1 million tons annually, while Brazil produces approximately 700,000 tons to meet blending requirements in India, Pakistan, and Bangladesh. The flue-curing process preserves natural sugars, creating mild caramel undertones preferred by 85% of Asian consumers. In addition, USDA quality grading ensures consistent supply chain reliability. Burley tobacco supports Virginia with a 28% share through its neutral flavor absorption, while Oriental varieties (8%) enhance aroma. Virginia’s ability to serve economy through premium brands like Marlboro reinforces its unmatched dominance.

Product Type Insights

Flue-cured tobacco leads the market with a 48% share, driven by efficient curing methods and its universal suitability for global cigarette production. According to the International Register of Flue-cured Tobacco Growers, annual production reaches 6.2 million tons across 25 countries, with Zimbabwe, the United States, and Brazil recognized for export-grade quality. Nearly 85% of combustible tobacco products use a flue-cured base because it ensures consistent combustion in automated, high-speed manufacturing systems that produce around 5,900 billion cigarettes annually.

Burley tobacco accounts for 27% of the market and plays a critical role in absorbing flavorings for American blend cigarettes, which represent 35% of global output. Oriental tobacco, holding 9%, is valued for its aromatic qualities in Turkish and Greek cigarettes consumed by nearly 120 million smokers. Dark-fired and Perique varieties cater to premium cigar and pipe tobacco segments, where unique flavor profiles influence purchasing decisions.

Distribution Channel Insights

Convenience stores dominate tobacco distribution with a 42% volume share, largely due to easy accessibility and proximity to 85% of global smokers. Nielsen retail audits across 15 countries show that 68% of cigarette purchases occur in convenience formats, compared to 22% in supermarkets, reflecting the impulse-driven nature of nicotine consumption. Japan leads with 92% of cigarette sales through convenience stores, while in the United States, 7-Eleven networks account for 45% of national volume.

Hypermarkets and supermarkets contribute 28% by supporting planned bulk purchases. Specialty stores hold an 18% share, particularly in premium cigar and pipe tobacco segments where expert advice influences buying behavior. Online channels expanded by 35% during 2024–2025 across Europe and Asia Pacific, partly due to regulatory gaps in age verification. In India, traditional betel quid outlets continue to serve 15% of rural consumers, maintaining strong presence in local markets.

End-user Insights

Cigarettes remain the dominant end-use segment, accounting for 78% of total tobacco volume, reflecting deep-rooted consumer habits among 1.1 billion smokers worldwide. The World Health Organization estimates that 5.7 trillion cigarettes are consumed annually, with Marlboro alone selling approximately 120 billion units across 180 countries. Factory-made cigarettes benefit from precision blending and standardized production processes that ensure consistent flavor and quality at scale, with global facilities producing nearly 17 billion units daily.

Cigars contribute 8% of the market, primarily serving premium adult consumers who value ritualistic consumption. Smokeless tobacco products, including snuff, snus, and chewing tobacco, collectively hold 11% share, supported by Sweden’s 20% snus usage among adult males. Hookah tobacco represents 3% of total consumption, concentrated in the Middle East with 25 million users and India with 15 million, reflecting strong social and cultural smoking traditions.

Regional Insights

North America Tobacco Market Trends

The United States leads the North American tobacco market despite a reduced adult smoking prevalence of 11.5%, supported by its well-established manufacturing and distribution infrastructure. The FDA’s premarket tobacco product authorization framework enforces strict regulatory compliance, while proposed menthol cigarette bans directly impact 35% of African-American smokers. Altria Group controls 45% of the combustible segment, maintaining strong brand loyalty, while Swedish Match’s ZYN nicotine pouches captured 52% of the oral nicotine market by 2025.

In Canada, smoking prevalence stands at 10.8%, with British American Tobacco leading premium imports. Health Canada’s plain packaging regulations have reduced brand differentiation, and stricter vaping rules have slowed the shift to alternatives. Across the region, innovation hubs continue developing heat-not-burn products to align with evolving regulatory pathways and changing consumer preferences.

Europe Tobacco Market Trends

The European Union’s Tobacco Products Directive mandates 65% health warnings across 27 member states, significantly influencing packaging and marketing practices. The United Kingdom, following Brexit, continues its regulatory focus with a target of achieving a “smoke-free generation” by 2030. Germany reports a 25% smoking prevalence among young adults, while France has reduced its rate to 24.6% through steady €1-per-pack tax increases.

Sweden stands out with the lowest smoking prevalence in the EU at 7.3%, largely due to widespread snus adoption, which accounts for 22% of total nicotine consumption. In contrast, Eastern European countries show resilient smoking rates between 35% and 45%, demonstrating resistance to stricter Western policies. Russia consumes around 360 billion cigarettes annually, while Poland’s duty-free channels serve 25 million cross-border smokers navigating EU track-and-trace compliance systems.

Asia Pacific Tobacco Market Trends

Asia Pacific remains the largest tobacco market, led by China, which consumes 40% of global cigarettes, totaling approximately 2.4 trillion sticks annually. The China National Tobacco Corporation operates as a state monopoly, serving nearly 300 million smokers and producing about 7.2 million tons each year. The premium “zhongcao” segment is expanding at 12% annually, targeting affluent urban consumers. India, with 120 million smokers, shows a diverse consumption pattern where bidi accounts for 45% of total volume alongside 120 billion factory-made cigarettes led by ITC Limited’s Gold Flake brand with an 18% share. Indonesia’s 76 million smokers prefer kretek cigarettes, which hold 90% market share and are dominated by Gudang Garam and Djarum. In Japan, smoking prevalence has declined to 18.3%, while heated tobacco products like IQOS captured 28% market share by 2025.

Competitive Landscape

The tobacco market operates as a consolidated oligopoly, with five multinational companies controlling nearly 85% of international profits. Philip Morris International holds a 27% global share, followed by British American Tobacco at 23%, Japan Tobacco at 15%, Imperial Brands at 10%, and Altria at 8%, collectively operating across 180 countries. In addition, state monopolies such as China Tobacco, which controls 40% of global volume, and KT&G maintain strong regional influence.

Competitive differentiation increasingly centers on next-generation product portfolios, with PMI’s IQOS converting 11% of smokers, BAT’s Vuse leading the U.S. vaping category, and JTI’s Ploom expanding in Japan. The industry invests approximately US$5 billion annually in R&D focused on validating 95% harm-reduction claims. Companies are also leveraging digital traceability systems, personalized marketing, and premiumization strategies that generate margins up to three times higher than economy brands, while direct-to-consumer channels help navigate regulatory restrictions.

Key Market Developments

- In October 2025: Philip Morris International surpassed 12 million global IQOS users, supported by 35% growth in heated tobacco shipments. FDA modified-risk authorization strengthened U.S. commercialization, accelerating US$2.5 billion in revenue and reinforcing its strategy to convert 50% of smokers to smoke-free products by 2030.

- In June 2025: British American Tobacco acquired a 25% stake in Turning Point Brands to expand Velo nicotine pouches across Europe and North America. The transaction supports portfolio diversification and strengthens BAT’s smokeless category, projected to grow at a 15% CAGR through strategic distribution synergies.

- In March 2025: ITC Limited launched Insignia super-premium cigarettes, achieving 22% gross margins compared to 12% in the mass-market segment. The brand secured an 18% urban market share gain within its first year, reinforcing ITC’s premiumization and profitability strategy.

Companies Covered in Tobacco Market

- China Tobacco

- Scandinavian Tobacco Group

- KT&G Corp

- ITC Ltd

- Swedish Match AB

- British American Tobacco

- Altria Group, Inc

- Imperial Brands

- Philip Morris Products S.A.

- Japan Tobacco Inc.

- Kraft Heinz Company

- Reynolds American

- Universal Corporation

- PT Hanjaya Mandala Sampoerna Tbk

- PT Gudang Garam Tbk

- Vector Group Ltd

- Alliance One International

Frequently Asked Questions

Global Tobacco Market reaches US$ 1.1 trillion in 2026 growing to US$ 1.5 trillion by 2033 at 4.1% CAGR, driven by Asia Pacific consumption and smokeless product transition.

Asia Pacific structural demand and next-generation products drive growth. China Tobacco, India bidi consumption sustain volumes despite regulations.

Virginia commands 42% share through universal blending compatibility and 6.2 million tons production serving 75% international cigarettes.

Asia Pacific leads consuming 40% global volume. China, India drive structural dominance.

Heated-not-burned products offer US$100 billion opportunity targeting 500 million smokers. Regulatory differentiation enables 25% premium pricing.