- Beauty & Personal Care

- Tea-Based Skin Care Products Market

Tea-Based Skin Care Products Market Size, Share, and Growth Forecast, 2026 - 2033

Tea-Based Skin Care Products Market by Tea Type (Green Tea, Black Tea, Others), Product Form Type (Creams & Lotions, Serums, Cleansers & Masks), Application (Facial Care, Body Care, Others), and Regional Analysis 2026 - 2033

Tea-Based Skin Care Products Market Size and Trends Analysis

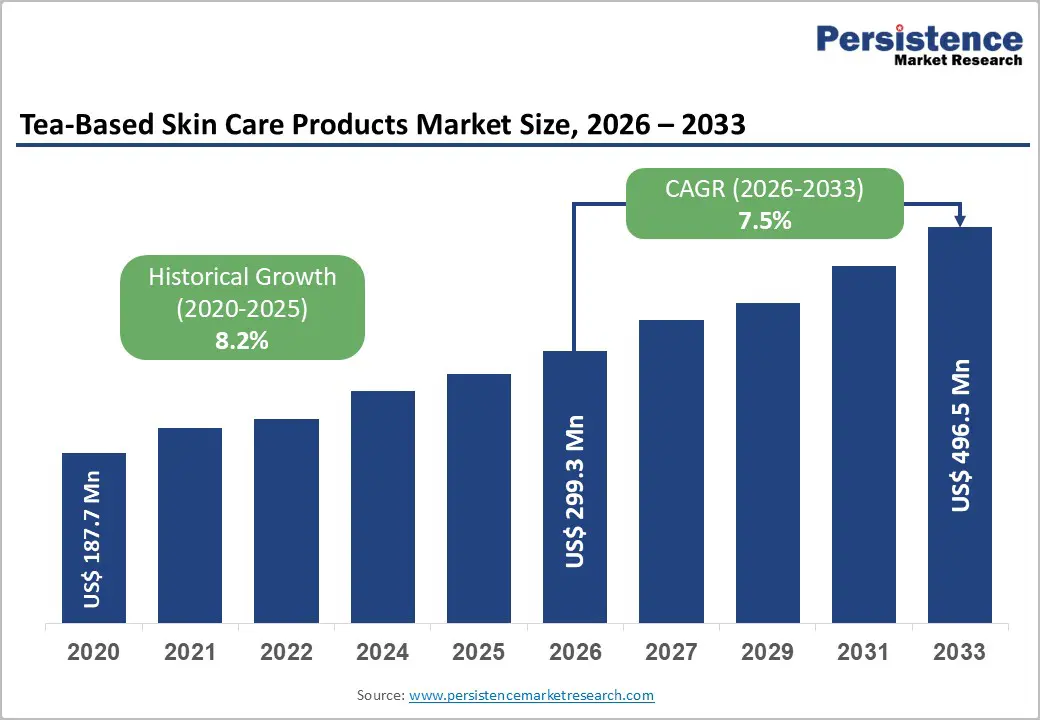

The global tea-based skin care products market size is likely to be valued at US$299.3 million in 2026 and is expected to reach US$496.5 million by 2033, growing at a CAGR of 7.5% during the forecast period from 2026 to 2033, driven by the rising demand for natural antioxidants in skincare, with green tea extracts leading due to their anti-inflammatory properties (specifically Epigallocatechin Gallate or EGCG) and the surging consumer shift toward "Clean Label" beauty formulations.

As urbanization intensifies globally, the demand for anti-pollution skincare solutions where tea extracts play a pivotal role due to their free-radical scavenging abilities has transitioned from a niche trend to a fundamental market driver. The integration of biotechnology in extraction processes is enhancing the bioavailability of tea polyphenols, thereby sustaining high-value growth in the premium dermatological sector.

Key Industry Highlights:

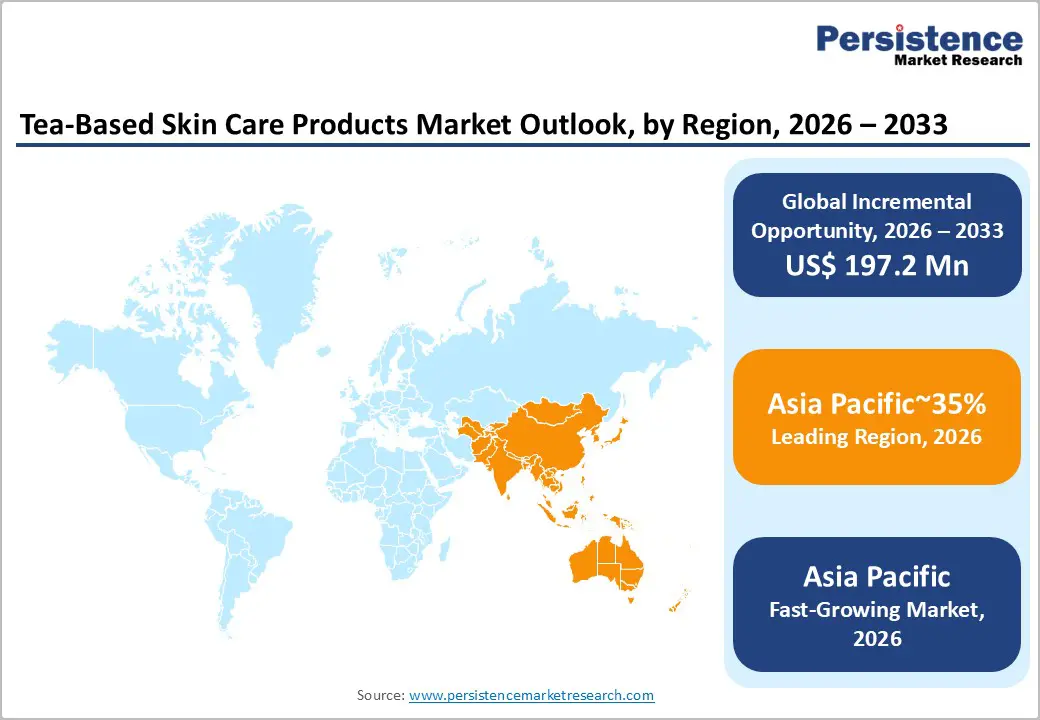

- Leading Region: Asia Pacific is projected to lead due to strong cultural affinity toward botanical formulations, expanding beauty and personal care consumption, and established herbal skincare traditions, accounting for approximately 35% share.

- Fastest-Growing Region: Asia Pacific is anticipated to grow THE fastest due to rising disposable income, K-beauty and J-beauty influence, and rapid digital commerce penetration.

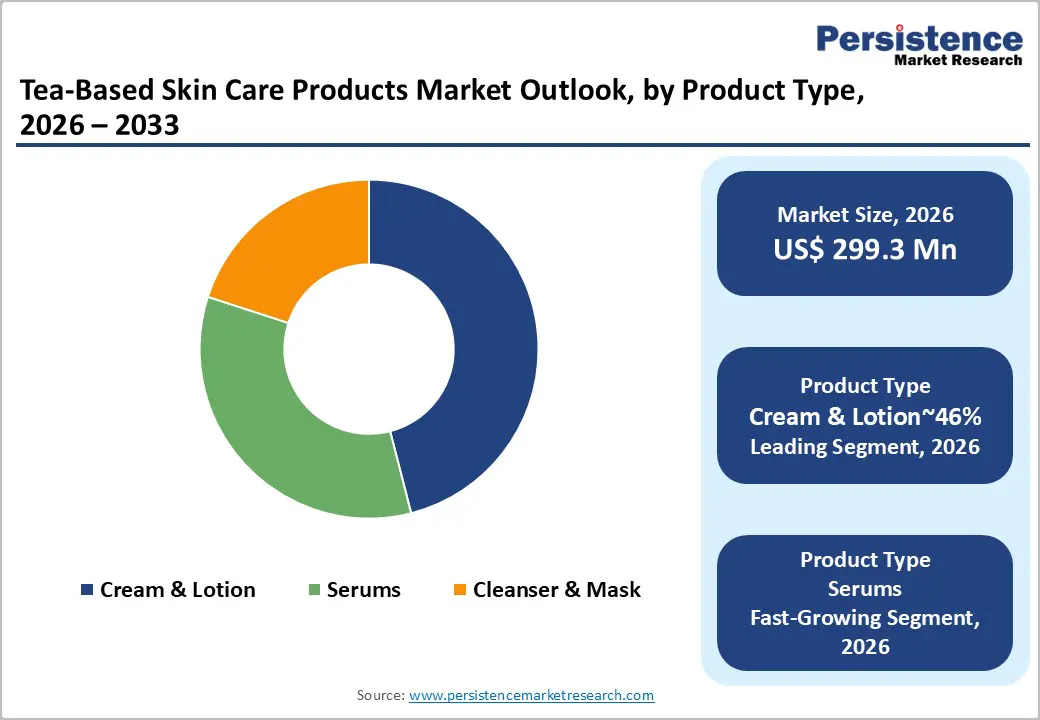

- Leading Product: Creams & Lotions are projected to dominate with approximately 46%, driven by daily-use versatility, broad skin compatibility, and integration into standard skincare routines.

- Leading Tea Type: Green Tea is projected to dominate, accounting for approximately 50%, supported by strong antioxidant recognition, anti-inflammatory benefits, and wide formulation compatibility.

| Key Insights | Details |

|---|---|

|

Tea-Based Skin Care Products Market Size (2026E) |

US$299.3 Mn |

|

Market Value Forecast (2033F) |

US$496.5 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

7.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Clinical Validation of Tea Polyphenols in Dermatology

The market for tea-based skin care products is structurally propelled by robust clinical validation of tea polyphenols, which differentiates these botanicals from conventionally anecdotal plant extracts. Green and black tea compounds, particularly Epigallocatechin Gallate (EGCG), exhibit documented inhibition of collagenase, mitigating collagen degradation and supporting measurable anti-aging outcomes. This scientific substantiation enhances formulators’ confidence in incorporating tea-derived actives into dermo cosmetic and premium personal care portfolios, influencing procurement strategies across ingredient suppliers, contract manufacturers, and finished-goods producers. From a value-chain perspective, validated efficacy enables higher-margin positioning, justifying formulation complexity and integration of standardized extract concentrations, while also attracting regulatory attention toward substantiated claims in regions with stringent cosmetic labeling standards.

Simultaneously, tea tannins’ regulatory effect on sebum synthesis drives adoption in acne-targeted applications, reinforcing market penetration in clinical and consumer segments that prioritize evidence-based outcomes. Rising consumer scrutiny, with an estimated majority researching ingredient efficacy before purchase, amplifies the commercial leverage of clinically verified tea extracts. Together, these factors reinforce tea polyphenols as strategic growth drivers across natural skincare and dermo cosmetic sectors, encouraging innovation and premiumization while aligning product claims with consumer trust and regulatory scrutiny.

Commerce and Wellness Trends

Online platforms are not just sales channels; they actively shape purchasing decisions through reviews, social content, and curated recommendations, creating a more informed and selective consumer base. The broader wellness trend has prompted consumers to allocate more of their personal care budgets to natural and premium formulations, extending the appeal of tea-derived actives beyond conventional female demographics and into men’s skincare routines. This convergence of accessibility, information, and lifestyle-driven spending has elevated tea-based products as both aspirational and evidence-backed choices in personal care portfolios. The post-pandemic wellness movement has elevated disposable income allocation toward natural and organic personal care products, broadening the addressable market for tea-derived formulations and stimulating higher-margin online sales.

At the regional and strategic level, sustainability considerations are increasingly central to market expansion. Eco-conscious consumers, particularly in the Asia Pacific region, are influencing sourcing practices, demanding traceable ingredients, responsible packaging, and certifications that align with ethical and environmental standards. These expectations create pressure across the value chain from ingredient suppliers to finished-product brands to integrate transparency and responsibility without compromising formulation efficacy. The interplay of digital channel expansion and wellness-led preferences materially elevates market accessibility, translating into incremental online growth while concurrently reinforcing traditional offline sales, thereby strengthening overall sector revenue streams and validating tea-based formulations as a strategically scalable segment.

Barrier Analysis - High Sensitivity to Oxidation and Ingredient Instability

The primary bioactive component in tea-based skincare is the polyphenol Epigallocatechin Gallate (EGCG), which exhibits antioxidant and anti-aging properties. EGCG demonstrates high chemical instability, reacting rapidly to light, heat, and oxygen. Contact with air accelerates degradation, leading to discoloration and a reduction in biological activity before the product is fully consumed. This instability imposes a technical constraint for manufacturers, requiring airtight and UV-protected packaging to preserve efficacy. Without such measures, the functional activity of tea-derived compounds diminishes, potentially compromising product performance.

Formulation strategies must account for this sensitivity, often incorporating synthetic stabilizers or increased preservative concentrations to extend shelf life. These interventions effectively mitigate degradation but can conflict with consumer expectations for minimally processed products, creating a trade-off between natural formulation and functional stability. Higher levels of stabilizers or preservatives may affect organic or natural claims and invite regulatory scrutiny. Consequently, formulation decisions involve balancing chemical stabilization with the preservation of natural integrity, as these choices directly influence product performance, regulatory compliance, and consumer perception.

High Competition from Synthetic "Bio-Identical" Actives

The tea-based skin care sector encounters pronounced competitive pressure from synthetic and bio-identical actives, which replicate the molecular structure of naturally occurring antioxidants such as those in tea. These lab-engineered compounds, including synthetic analogues of EGCG, offer enhanced chemical stability, predictable bioavailability, and elimination of agricultural variability or pesticide risk. From a market and value-chain perspective, this reduces formulation complexity, lowers long-term production and storage costs, and enables manufacturers to meet consumer demand for rapid, measurable anti-aging results. naturally derived tea extracts ALSO face structural challenges in segments prioritizing high-efficacy, fast-acting interventions, constraining adoption within premium corrective skincare categories, and creating margin pressure relative to stable, scalable synthetic alternatives.

Consumer perception dynamics exacerbate competitive constraints. Tea-based formulations are often positioned as gentle or preventative, in contrast to medical-grade synthetics perceived as corrective or intensive. Marketing emphasis on experiential, holistic, and botanical authenticity must counterbalance the technological appeal of bio-identical alternatives, requiring heightened investment in branding, certification, and efficacy substantiation. Collectively, these factors structurally limit the share of high-performance, evidence-driven market segments accessible to tea-based products, reinforcing the strategic influence of synthetic analogues on sector growth and adoption.

Opportunity Analysis - Expansion into Men’s Grooming and Unisex Formulations

The tea-based skin care market presents a strategic opportunity in the underpenetrated men’s grooming and unisex segment, where formulation requirements differ from conventional female-focused products. Male skin exhibits higher sebum production, increased follicular density, and heightened susceptibility to irritation from routine shaving, creating a structural need for actives that combine astringent, anti-inflammatory, and soothing properties. Black tea polyphenols provide sebum-regulating effects, while green tea catechins mitigate oxidative stress and inflammation, supporting applications in aftershaves, lightweight moisturizers, and beard care products. At the value-chain level, this necessitates tailored extraction standardization, formulation stability assessments, and packaging solutions that accommodate male and gender-neutral preferences, influencing production workflows, ingredient sourcing, and margin allocation.

Consumer adoption is further influenced by perception and positioning dynamics, with performance-oriented and scientifically substantiated claims enabling penetration into demographics historically less engaged with botanical skincare. Marketing and regulatory alignment, including standardized ingredient labeling and efficacy substantiation, can reinforce trust while supporting cross-segment scalability. Collectively, these dynamics expand the accessible market, optimize product lifecycle economics, and create structural incentives for integrating tea-based actives into high-growth male and unisex skincare formulations.

Personalized Skincare via AI and Data

The integration of AI-driven diagnostics with tea-based skin care formulations presents a structurally significant opportunity to advance mass-customized product offerings. By leveraging algorithmic analysis of individual skin parameters, including sebum levels, sensitivity, and age-related biomarkers, formulators can optimize the concentration of active tea polyphenols such as green tea catechins for oil regulation and white tea extracts for anti-aging efficacy. This value-chain adaptation necessitates investment in predictive analytics, formulation modularity, and flexible production systems capable of accommodating small-batch, personalized outputs, impacting cost structures, ingredient inventory management, and margin optimization across production and distribution tiers.

Environmental and geospatial data integration further enhances market relevance, enabling targeted recommendations based on local UV exposure, pollution levels, or climatic conditions, such as high-antioxidant matcha formulations for high-pollution urban centers. These capabilities reinforce consumer engagement, retention, and willingness to pay a premium while aligning with regulatory and quality standards for personalized cosmetic products. Collectively, the convergence of AI diagnostics and tea-based actives establishes a technologically differentiated pathway for precision skincare at scale.

Category–wise Analysis

Tea Type Insights

Green tea is expected to lead, accounting for approximately 50% share in 2026, underpinned by its entrenched role in facial care and mass-market skincare formulations. Adoption remains anchored by EGCG antioxidants’ proven efficacy in reducing inflammation, regulating sebum, and protecting against UV-induced damage, which drives preference across acne-prone and oily skin segments.

Operational advantages include versatile sourcing from Japanese Matcha to Chinese Sencha, enabling scale integration across price tiers and product formats. Ongoing innovation in extraction and stabilization technologies continues to reinforce formulation consistency and active retention. Vendors such as Innisfree, Origins, and The Body Shop are expanding green tea-infused serums, moisturizers, and masks to consolidate consumer loyalty and embed brand-specific workflows. This combination of validated efficacy, mature ingredient infrastructure, and broad consumer acceptance sustains Green Tea’s dominance within structured skincare deployment models.

Black tea is expected to be the fastest-growing segment, driven by emerging demand for firming, anti-aging, and depuffing applications across facial and body care products. Growth is catalyzed by oxidation-derived compounds such as theaflavins and caffeine, which materially improve skin tightening and elasticity outcomes.

Accelerating adoption is supported by advanced formulation techniques, fermented black tea complexes, and preimmunized product positioning that reduce operational friction for first-time adopters. Companies including AmorePacific, Estée Lauder, and Shiseido are scaling black tea serums and luxury masks to capture early-cycle demand and embed switching costs. As clinical validation and consumer awareness of non-irritating firming botanicals improve, Black Tea is expected to outpace overall market growth over the forecast period.

Product Type Insights

Creams & lotions are expected to lead, accounting for approximately 50% share in 2026, underpinned by their entrenched role as the foundational daily skincare format across facial and body routines. Adoption remains anchored by the lipid-rich matrix, which stabilizes tea polyphenols, mitigates oxidative degradation, and enhances dermal absorption, ensuring consistent bioactive delivery. Operational advantages include high repurchase rates and cross-segment applicability, appealing to preventative and hydration-focused consumer demographics.

Ongoing formulation innovations, including microemulsion and encapsulation technologies, reinforce product efficacy and shelf-life. Vendors such as Innisfree, Origins, and Kiehl’s are expanding cream and lotion portfolios infused with green and black tea extracts, locking in consumer routines and reinforcing brand loyalty. This combination of formulation robustness, daily utility, and broad consumer alignment sustains Creams & Lotions’ dominance within structured skincare deployment models.

Serums are expected to be the fastest-growing segment, driven by rising demand for high-potency, minimalistic formulations under the “Skinimalism” trend. Growth is catalyzed by advanced absorption technologies and water-free (anhydrous) formulations that preserve delicate tea antioxidants, enabling targeted delivery at higher extract concentrations.

Accelerating adoption is supported by premiumization and willingness to pay per milliliter, allowing brands to command higher margins while demonstrating clinical efficacy. Companies, including AmorePacific, Shiseido, and Estée Lauder, are scaling black and green tea serum lines to capture early-cycle demand and embed switching costs. As formulation technology and consumer education improve, serums are expected to outpace overall market growth over the forecast period.

Regional Insights

Asia Pacific Tea-Based Skin Care Products Market Trends

The Asia Pacific region is expected to be the leading region, to be the one to register the fastest growth trajectory, approximating 35% of the global revenue in 2026, driven by its integration of cultural heritage, functional skincare priorities, and manufacturing scale. Market dynamics are structurally influenced by traditional practices such as Traditional Chinese Medicine and Ayurveda, which guide formulation of tea-based actives for brightening, hydration, and skin-tone evening rather than purely anti-aging outcomes.

Industrial expansion in South Korea and Japan supports high-volume production and innovation diffusion, enabling APAC-originated products such as green tea seed serums and matcha masks to penetrate global markets. E-commerce adoption, localized supply chains, and relatively flexible regulatory frameworks allow rapid product rollout, while tightening quality-control measures ensure efficacy and safety, reinforcing regional credibility and premiumization. Competitive positioning favors vertically integrated brands capable of managing extraction, formulation, and distribution across multi-country operations.

China anchors regional momentum, accounting for a substantial share of APAC activity through concentrated manufacturing and domestic consumption. Regulatory alignment, FDI inflows, and investment in R&D for natural and herbal fusion products drive product sophistication and market visibility. The rising disposable income, K-beauty and J-beauty influence, and rapid digital commerce penetration. Brands such as AmorePacific leverage advanced extraction technologies and cross-border distribution networks, while local e-commerce penetration accelerates the adoption of functional tea-based skincare. Forward-looking trends include leveraging culturally embedded ingredients, scalable formulation platforms, and consumer education to consolidate APAC’s leading role, structurally enhancing regional influence on global product innovation and market expansion.

North America Tea-Based Skin Care Products Market Trends

North America is expected to remain the mature market, supported by a sophisticated innovation ecosystem, premiumization strategies, and deep integration of clean-clinical beauty principles. Demand is structurally driven by the convergence of natural ingredient adoption and scientific substantiation, particularly through tea-based actives combined with Niacinamide and Hyaluronic Acid. Regulatory vigilance on marketing claims incentivizes rigorous clinical validation, while retailer specialization in superfood skincare reinforces product visibility. The market is further reinforced by consumer alignment with wellness-oriented lifestyle trends, where tea consumption habits translate into elevated interest in ingredient-driven formulations. Enterprise investments in R&D, formulation technology, and ingredient traceability underpin product differentiation, sustaining North America’s structural dominance in both premium and evidence-based botanical skincare.

The U.S. anchors regional momentum, accounting for the majority of market activity, and shapes the competitive landscape through concentrated brand presence and regulatory influence. FDA oversight of claims and certification pathways drives adoption of validated, high-purity formulations, while brands such as Estée Lauder and Origins demonstrate forward-looking alignment with MoCRA transparency requirements. Retail channel specialization, investment in clinical substantiation, and integration of wellness-driven messaging position the U.S. to structurally reinforce North America’s leadership, optimize margin capture through premium product positioning, and consolidate influence over global tea-based skincare innovation trajectories.

Europe Tea-Based Skin Care Products Market Trends

Europe is expected to remain a mature and structurally stable market, anchored in regulatory harmonization, sustainability mandates, and premium organic certification frameworks. Market dynamics are structurally shaped by stringent regulations under EC No 1223/2009 and the European Green Deal, which enforce comprehensive safety assessments, allergen labeling, and environmental compliance across the value chain. This regulatory landscape favors players capable of ensuring traceable, high-purity tea extracts while driving investment in supply-chain certification, formulation standardization, and sustainable packaging solutions.

Demand is structurally reinforced by consumer preference for bio-certified and eco-conscious products, particularly within pharmacy-led channels targeting sensitive and reactive skin applications. Technology adoption in extraction, stabilization, and product testing supports compliance, enhances ingredient efficacy retention, and underpins premiumization strategies, sustaining enterprise differentiation and long-term regional resilience.

Germany anchors European market momentum, shaping regional trajectories through concentrated consumer demand for certified organic tea-based formulations. Regulatory and industry structures incentivize certified sourcing, vegan compliance, and high-integrity labeling, while local manufacturers leverage traceable supply chains and formulation expertise to maintain competitive positioning. Forward-looking strategies include integration of sustainable extraction technologies, targeted product placement within pharmacy and specialty retail, and collaboration with certified plantation networks, collectively reinforcing Europe’s stable market status, supporting predictable growth, and structurally embedding regulatory compliance into the tea-based skincare value chain.

Competitive Landscape

The global tea-based skin care products market is moderately consolidated, with the top five players, including Estée Lauder and L’Oréal, controlling roughly 50 – 55% of market share, while numerous niche and startup brands operate within specialized natural and clean beauty segments. Leading players exert structural influence through vertically integrated sourcing of tea extracts, scale-enabled distribution, and extensive R&D in antioxidant stabilization and formulation technology, shaping both product efficacy and market standards.

Competitive positioning is defined by horizontal differentiation across price tiers and product forms, with mass market players leveraging scale economics and private labels, while premium and online-focused brands emphasize single-origin tea narratives and targeted functional benefits. Industry dynamics are evolving through selective M&A, platform expansion, and service-led initiatives such as subscription models and personalized formulations, reinforcing ecosystem consolidation and creating forward-looking pressure on both incumbents and emerging brands to maintain innovation-driven relevance within the sector.

Key Industry Highlights:

- In January 2026, Teaology launched a blue tea hyaluronic hydra face mask featuring "Tea Infusion Skincare" technology. This innovation replaces 100% of the water content in the mask with antioxidant-rich blue tea infusion, maximizing the potency of active minerals.

- In December 2025, Innisfree launched green tea ceramide cream featuring "Super Green Tea" technology. This product offers hydration five times more potent than Hyaluronic Acid, positioning tea as a superior medical-grade active ingredient.

- In December 2025, Fresh Beauty launched a black tea essentials set featuring "Mauritius Black Tea Extract." The use of geographically specific tea varieties targets the luxury consumer's desire for rare, high-performance botanical origins.

Companies Covered in Tea-Based Skin Care Products Market

- Estée Lauder

- L’Oréal

- AmorePacific

- Shiseido

- Unilever

- Lancôme

- Burt’s Bees

- Innisfree

- Natura &Co

- Avon

- The Body Shop

- Kao Corp

- P&G

- Beiersdorf

- Fresh, Inc.

- Teaology Skincare

Frequently Asked Questions

The global tea-based skin care products market is projected to be valued at US$299.3 million in 2026 and is expected to reach US$496.5 million by 2033, driven by rising demand for natural antioxidants in skincare, the “Clean Label” beauty movement, and clinically validated benefits of tea polyphenols.

Scientific substantiation of compounds such as EGCG (Epigallocatechin Gallate) for their anti-inflammatory, anti-collagenase, and sebum-regulating effects differentiates tea extracts from anecdotal botanicals. This efficacy enables higher-margin premium positioning and builds consumer trust in an era where a majority researches ingredients before purchase.

The tea-based skin care products market is forecast to grow at a CAGR of 7.5% from 2026 to 2033, reflecting steady expansion driven by wellness trends, digital commerce, and the integration of tea extracts into diverse product formats.

Asia Pacific is both the leading and fastest-growing regional market, accounting for approximately 35% share, underpinned by a strong cultural affinity for botanical formulations, the influence of K-beauty and J-beauty, and rapid digital commerce penetration.

The tea-based skin care products market is moderately consolidated, with global beauty conglomerates such as Estée Lauder (Origins), L'Oréal, and Shiseido leading through scale and R&D. Asian specialists such as AmorePacific (Innisfree) leverage cultural heritage and advanced extraction technologies, while niche players, including Fresh, Inc., compete through rare, single-origin tea narratives in the luxury segment.