- Metals & Minerals

- Spiral Steel Pipes Market

Spiral Steel Pipes Market Size, Share, and Growth Forecast, 2026 - 2033

Spiral Steel Pipes Market by Product Type (Q345B, X40-X80, L245, L360, 16Mn, and Others), By Application (Petrochemical Industry, Water Engineering, Chemical Industry, Power Industry, Agricultural Irrigation, Urban Construction, and Others), and Regional Analysis for 2026 - 2033

Spiral Steel Pipes Market Size and Trends Analysis

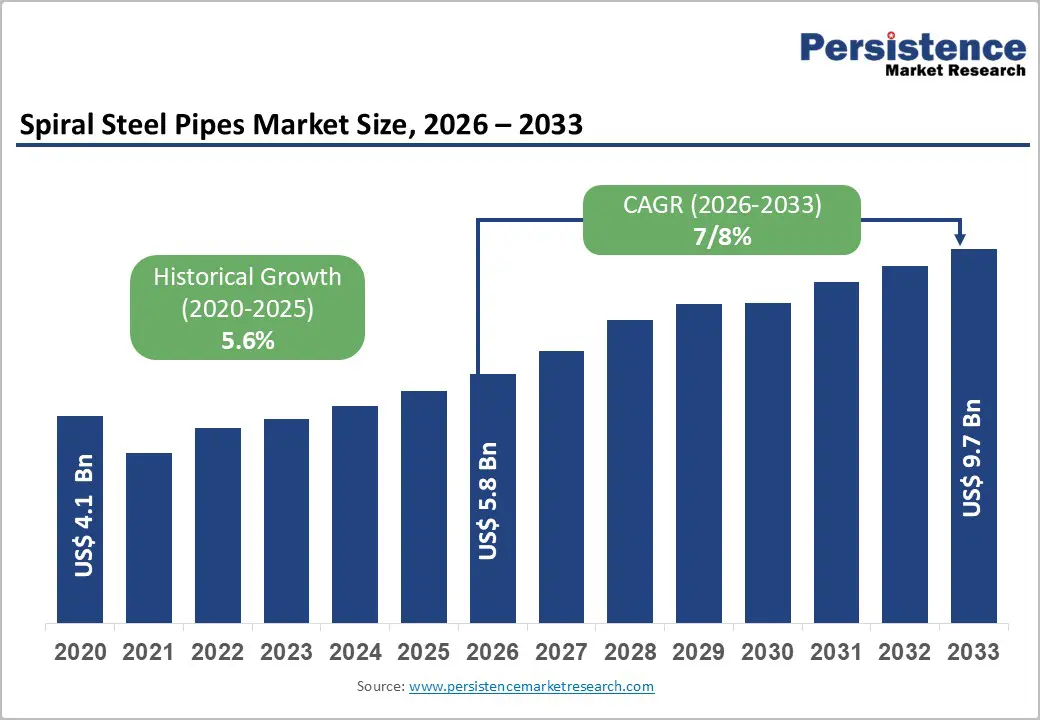

The global spiral steel pipes market size is likely to be valued at US$ 4.8 billion in 2026 and is projected to reach US$ 9.7 billion by 2033, expanding at a CAGR of 7.8% during the 2026 - 2033 forecast period.

The growing demand from the petrochemical and water engineering sectors, along with accelerating infrastructure development across the Asia Pacific and the Middle East, has driven growth. Additionally, technological advancements in manufacturing processes have also catalysed the demand for spiral steel pipes in the past.

Key Industry Highlights:

- Leading Product Segment: Q345B-grade pipes command 30%+ market share, while X40-X80 grades demonstrate the fastest growth at an 8.5% CAGR, reflecting a shift toward high-strength specifications in petrochemical and infrastructure applications.

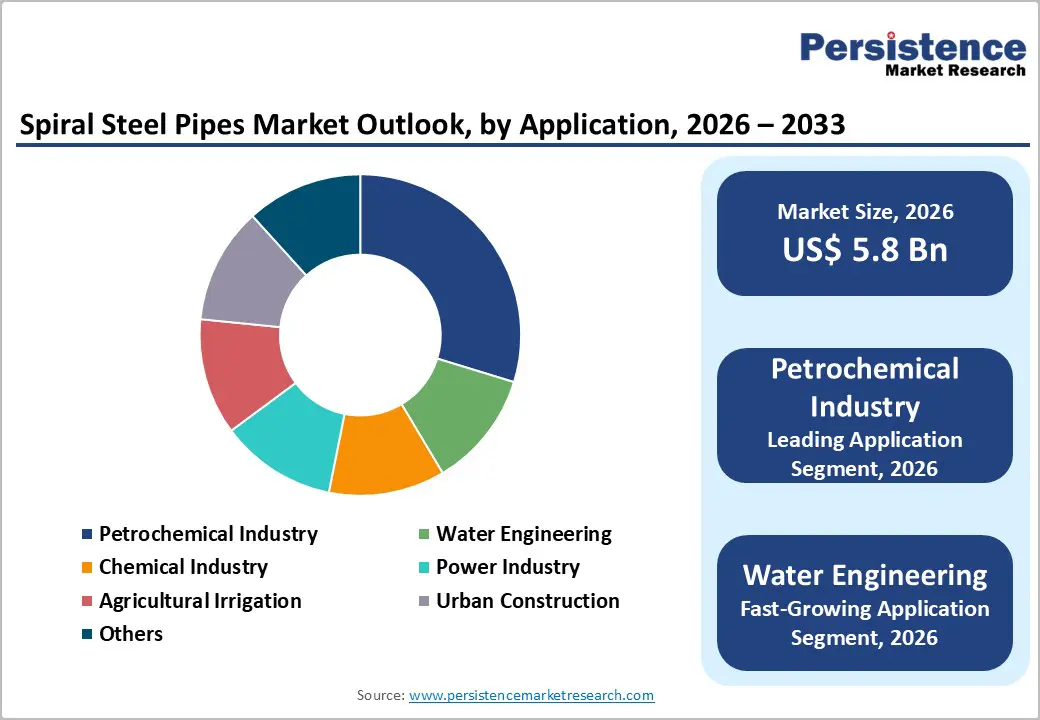

- Dominant Application: The Petrochemical Industry accounts for 35%+ of revenue share and has stable demand, while Water Engineering exhibits the highest growth at a 8.7% CAGR, reflecting accelerating water infrastructure investment in developing regions.

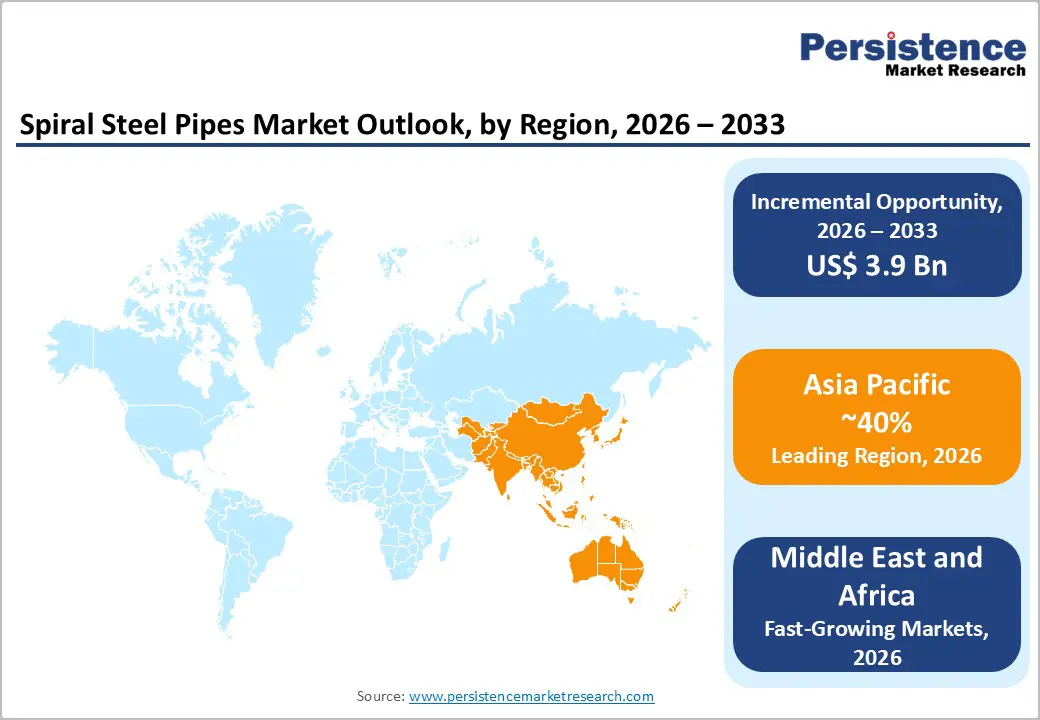

- Regional Leadership: Asia Pacific maintains 40%+ market share as the dominant region, while the Middle East and Africa emerge as the fastest-growing region at 8.8% CAGR, driven by petrochemical expansion and water infrastructure investment.

- Market Consolidation: Top 10 manufacturers control 45-50% of global market share, with ongoing capacity expansions and strategic acquisitions reshaping the competitive landscape, particularly in the Asia Pacific and emerging markets.

- Growth Catalysts: Infrastructure development in Asia Pacific (ADB projections of US$ 1.7 trillion in annual investment), petrochemical capacity expansion (4.2% annual growth), and the emerging hydrogen economy (US$ 180 billion in infrastructure investment through 2030) represent primary demand drivers through 2033.

| Key Insights | Details |

|---|---|

| Spiral Steel Pipes Market Size (2026E) | US$ 5.8 Bn |

| Market Value Forecast (2033F) | US$ 9.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Dynamics

Drivers - Rapid Infrastructure Development and Urbanization in Emerging Economies

Infrastructure expansion across the Asia Pacific and Middle East regions represents a primary growth catalyst for the spiral steel pipes market. According to Asian Development Bank (ADB) projections, the Asia-Pacific region requires approximately US$ 1.7 trillion in infrastructure investment annually through 2030, creating substantial demand for high-capacity pipeline systems. Spiral steel pipes, offering superior structural integrity and pressure-bearing capacity, are increasingly specified for water transmission networks, petrochemical distribution systems, and urban construction applications. India's Smart Cities Mission and China's Belt and Road Initiative have catalyzed major infrastructure projects requiring advanced piping solutions. The Water Engineering segment is the fastest-growing, with a 8.7% CAGR, directly correlating with rising water demand in urbanizing regions. This infrastructure momentum is projected to sustain market expansion through 2033, with emerging economies accounting for approximately 55% of cumulative demand.

Market Restraining Factors

Regulatory Compliance Costs and Complex Certification Requirements

Stringent environmental, safety, and quality regulations across developed markets necessitate expensive certification and testing infrastructure. The European Pressure Equipment Directive (PED), American Society of Mechanical Engineers (ASME) standards, and ISO certifications require dedicated manufacturing facilities and quality assurance protocols, creating barriers to entry for smaller manufacturers. Compliance costs can account for 8-12% of manufacturing expenses, effectively eroding margins for price-competitive segments. Additionally, evolving environmental regulations regarding manufacturing emissions and wastewater treatment are imposing additional capital expenditures on manufacturers, particularly in Europe and North America, potentially moderating supply growth and limiting market expansion in cost-sensitive regions.

Opportunity - Urban Water Infrastructure Replacement and Rehabilitation Programs

Aging water distribution networks across North America and Europe present substantial rehabilitation opportunities. The American Water Works Association (AWWA) estimates that US$ 746 billion in water infrastructure investment is required through 2040, with approximately 40% directed toward distribution system replacement and modernization. Spiral steel pipes, offering longer service life and reduced leakage compared to aging cast-iron and asbestos-cement networks, are increasingly specified in major rehabilitation programs. This replacement cycle, expected to accelerate through 2033, represents US$ 600-800 million in incremental market opportunity, particularly benefiting manufacturers with an established presence in North American and European markets.

Category-wise Analysis

Product Type Insights

The global steel pipe market by product type is characterized by a clear distinction between a mature dominant segment and a rapidly expanding high-performance category. Q345B grade pipes currently hold the leading position, accounting for over 30% of total market revenue and representing approximately US$ 1.48 billion of the 2026 market value. Manufactured to the Chinese GB/T standard, Q345B offers tensile strength of 340-380 MPa, making it the preferred specification for petrochemical processing, power generation, and large-scale water infrastructure projects, particularly in the Asia Pacific region. Its designation as a default industrial grade under Chinese national standards has created consistent, predictable demand from domestic and regional manufacturing hubs. Growth in this segment is largely supported by ongoing infrastructure development across China and Southeast Asia, where Q345B is frequently mandated in public project tenders and engineering specifications.

In contrast, X40-X80 grade pipes represent the fastest-growing segment, expanding at a 8.5% CAGR through 2033. Defined by API 5L, these high-strength grades are increasingly specified for high-pressure petrochemical pipelines, offshore installations, and long-distance transmission networks. Rising demand for larger diameters, higher operating pressures, and corrosion resistance, combined with premium pricing that enhances manufacturer margins, is accelerating investments and capacity expansion in this segment.

Application Insights

The petrochemical industry represents the leading application segment, accounting for over 35% of total revenue and an estimated market value of approximately US$ 1.72 billion in 2026. Its dominance stems from extensive use of piping systems across crude oil transportation, refined product distribution, chemical synthesis facilities, and downstream processing operations. Large-scale petrochemical hubs across the Asia Pacific—including Singapore, South Korea, and India—as well as the Middle East and Europe, generate highly concentrated and recurring demand. These applications require high-volume procurement, strict quality compliance, and long-term supply contracts, enabling manufacturers to secure predictable revenues and operational stability. Growth in this segment remains steady, closely aligned with global petrochemical output expansion, which is increasing at an annual rate of around 4.2%, supported largely by capacity additions in emerging economies.

In contrast, water engineering is the fastest-growing application segment, expanding at a robust 8.7% CAGR through 2033. This growth is driven by rising investments in municipal water transmission, wastewater treatment systems, industrial water supply, and agricultural distribution networks. Rapid urbanization across South Asia, Southeast Asia, and Sub-Saharan Africa, coupled with strong funding support from international development institutions, is accelerating large-scale infrastructure projects. Compared to petrochemical applications, water-related demand is less exposed to commodity price volatility, supporting stronger pricing stability and margins. As a result, the water engineering segment is projected to grow from US$ 580-620 million in 2026 to nearly US$ 1.3 billion by 2033, making it a key strategic growth area.

Regional Insights and Trends

Asia Pacific Dominates Global Spiral Steel Pipe Market Through Infrastructure and Manufacturing Expansion

Asia Pacific remains the leading regional market for spiral steel pipes, accounting for over 40% of global revenue, equivalent to approximately US$ 1.92 billion of the total market value in 2026. The region is expected to retain its leadership position through 2033, supported by China’s sustained industrialization, India’s accelerating infrastructure development, and expanding manufacturing activity across ASEAN economies. China alone accounts for 45-50% of regional demand, followed by India at 15-18%, while ASEAN countries such as Indonesia, Vietnam, and Thailand collectively account for 12-15% of consumption.

China’s annual spiral steel pipe consumption is estimated at 8.5-9.2 million tonnes, driven primarily by petrochemical refinery expansions and large-scale urban water infrastructure projects. India is the fastest-growing major market in the region, with demand increasing at an annual rate of 9.2% as government-led water management, urban development, and manufacturing initiatives gain momentum. Japan, in contrast, represents a mature and stable market, consuming approximately 450,000 tonnes annually, largely driven by replacement demand and infrastructure maintenance cycles.

Regional growth is underpinned by strong government infrastructure spending, expanding petrochemical and manufacturing capacities, and export-oriented industrial development across ASEAN. Standardized regulations in China and India are improving manufacturing efficiency, while tightening environmental norms are encouraging investments in cleaner production technologies and modernized facilities.

North America drives rapid Spiral Steel Pipes market growth through regulation and innovation

The Middle East and Africa region represents the fastest-growing market globally, projected to expand at a robust CAGR of 8.8% through 2033, well above the global average. The region currently accounts for approximately 18-20% of global market revenue, valued at nearly US$ 865-960 million in 2026, and is expected to scale rapidly as large-scale infrastructure investments gain momentum. Saudi Arabia is the largest regional market, with annual demand estimated at 1.1-1.3 million tonnes, primarily supported by extensive expansions of petrochemical complexes in the Eastern Province. Meanwhile, the UAE and other GCC nations are accelerating investments in desalination facilities, industrial zones, and utility networks, strengthening demand for advanced piping systems. Across Sub-Saharan Africa, countries such as Nigeria, Kenya, and South Africa are emerging as key growth hubs driven by rising urbanization and industrial development.

Growth is underpinned by three structural drivers. First, multi-billion-dollar petrochemical expansions led by regional energy giants are generating sustained pipeline demand. Second, chronic water scarcity is accelerating desalination and long-distance water transmission projects, which require specialized, high-durability piping solutions. Third, increasing regional trade integration is driving the development of cross-border pipeline infrastructure linking production and consumption hubs. Regulatory shifts mandating international quality certifications are further supporting premium products, while development finance institutions and rising foreign direct investment are enhancing long-term market attractiveness.

Competitive Landscape

The global spiral steel pipes market demonstrates a moderately consolidated competitive structure, with the top ten manufacturers accounting for approximately 45-50% of total global market share. Competition is largely shaped by regional consolidation patterns, where leading players retain dominant positions within their domestic markets, such as China, Europe, and India, while international manufacturers participate more selectively, primarily targeting premium and specialized application segments. Market concentration levels vary significantly by region. Asia Pacific exhibits higher consolidation, with the top ten players controlling close to 55% of the regional market, driven by large-scale manufacturing bases and strong domestic infrastructure demand. In contrast, Europe and North America show lower concentration levels of around 40-42%, reflecting a more fragmented supplier landscape and the presence of numerous regional producers serving localized demand.

Competitive positioning across the market is strongly influenced by manufacturing scale, adherence to quality and certification standards, operational efficiency within supply chains, and proximity to key end-user industries. Pricing dynamics differ notably by product category. Commodity-grade spiral steel pipes, particularly Q345B, face intense price competition due to high availability and standardized specifications. Conversely, higher-grade and specialized products such as X40-X80 API grades and corrosion-resistant pipes offer manufacturers improved pricing power and healthier profit margins, supported by technical complexity and stricter performance requirements.

Key Industry Developments:

- In July, 2025, PT Southeast Asia Pipe Industries (SEAPI) expanded its spiral and HSAW steel pipe production range from 16 inches to 140 inches in diameter, reinforcing its capability to supply extra-long joints for large-scale infrastructure projects across Southeast Asia.

- In 2025, Kuwait’s US$180 billion Kuwait Vision 2035 infrastructure program significantly boosted demand for large-diameter spiral steel pipes used in water, oil, gas, and sewage networks.

- On August 25, 2024, China Steel Pipe Company successfully trial-produced China’s largest thick-walled spiral SAW pipe (1,820 mm diameter, 28 mm wall thickness), achieving appraisal approval and meeting leading national technical standards.

Companies Covered in Spiral Steel Pipes Market

- Jindal SAW Ltd

- Nucor Skyline

- American SpiralWeld Pipe Company

- Tianjin Youfa Steel Pipe Group

- Baosteel Group

- Cangzhou Spiral Steel Pipes Group

- Welspun Corp

- EVRAZ North America

- SeAH Steel

- ArcelorMittal

- Tenaris

- Naylor Pipe Company

- Yangtze Steel Group

- PSL Limited

- Maharashtra Seamless

- Other Market Players

Frequently Asked Questions

The spiral steel pipes market is estimated to be valued at US$ 5.8 Bn in 2026.

The primary demand driver for the spiral steel pipes market is large-scale infrastructure development, particularly in water transmission, oil and gas pipelines, and urban utility networks.

In 2026, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Spiral Steel Pipes market.

Among applications, the petrochemical industry has the highest preference, capturing beyond 35% of the market revenue share in 2026, surpassing other applications.

Jindal SAW Ltd, Nucor Skyline, American SpiralWeld Pipe Company, Tianjin Youfa, teel Pipe Group, Baosteel Group, Cangzhou Spiral Steel Pipes Group, Welspun Corp, EVRAZ North America, and SeAH Steel are a few leading players in the Spiral Steel Pipes market.