- Non-food Packaging

- Returnable Plastic Crate Market

Returnable Plastic Crate Market Size, Share, and Growth Forecast 2026 - 2033

Returnable Plastic Crate Market by Capacity (Less than 10 Kg, 10 Kg to 20 Kg, 21 Kg to 35 Kg, 36 Kg to 50 Kg), by Product Type (Stackable, Nestable, Collapsible), Material (High Density Polyethylene (HDPE), Polypropylene (PP), Others), Application (Agriculture, Grocery, Dairy, Bakery, Seafood & Meat, Others), and Regional Analysis, 2026 - 2033

Returnable Plastic Crate Market Size and Trend Analysis

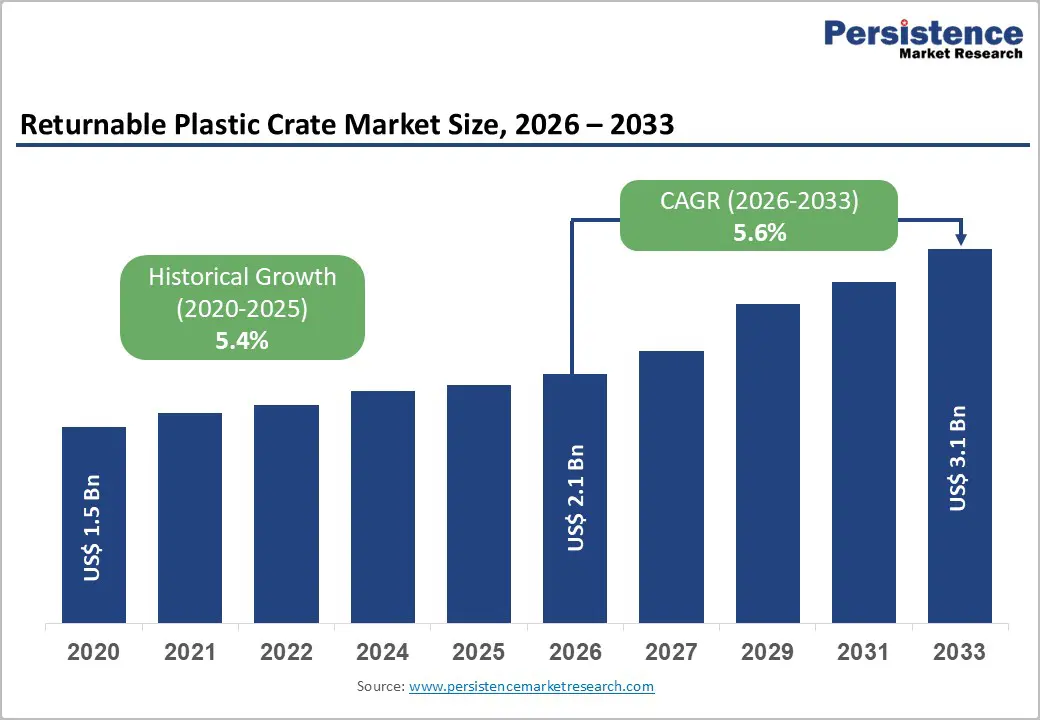

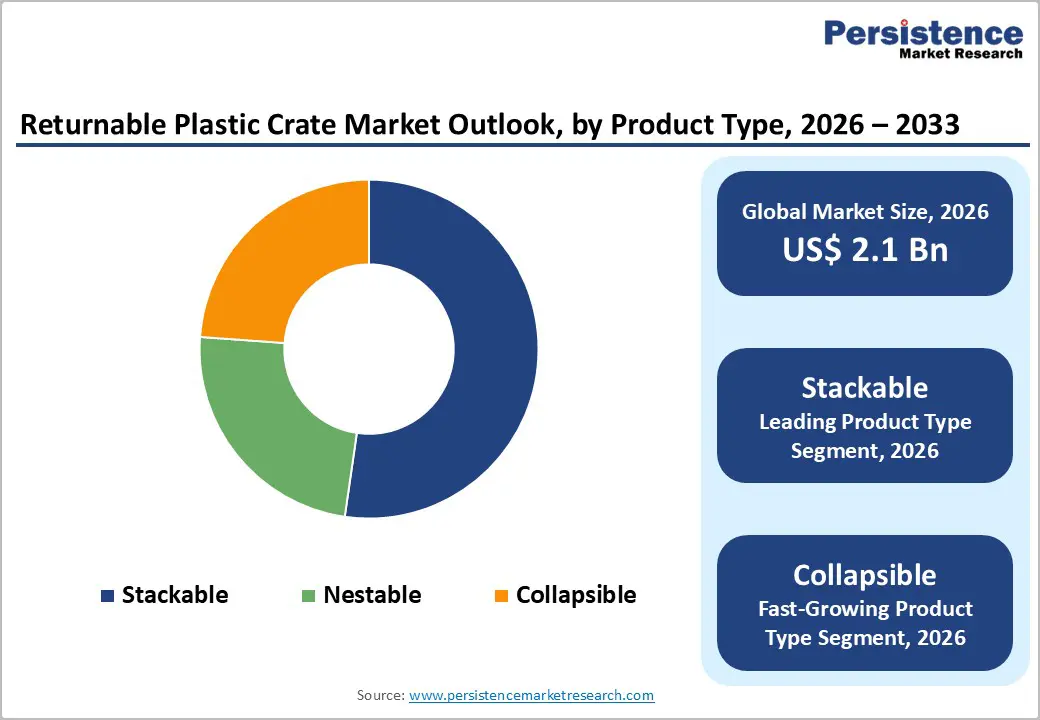

The global returnable plastic crate market size is expected to be valued at US$ 2.1 billion in 2026 and projected to reach US$ 3.1 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. The market growth is driven by the rise in packaging waste regulations, particularly the European Union’s Packaging and Packaging Waste Regulation (PPWR), which mandates increasing shares of reusable transport packaging by 2030 and 2040.

Additionally, major retailers and FMCG companies are adopting returnable plastic crate systems to reduce their environmental footprint, optimize supply chain efficiency, and lower the total cost of ownership across global fresh food and grocery distribution networks.

Key Industry Highlights:

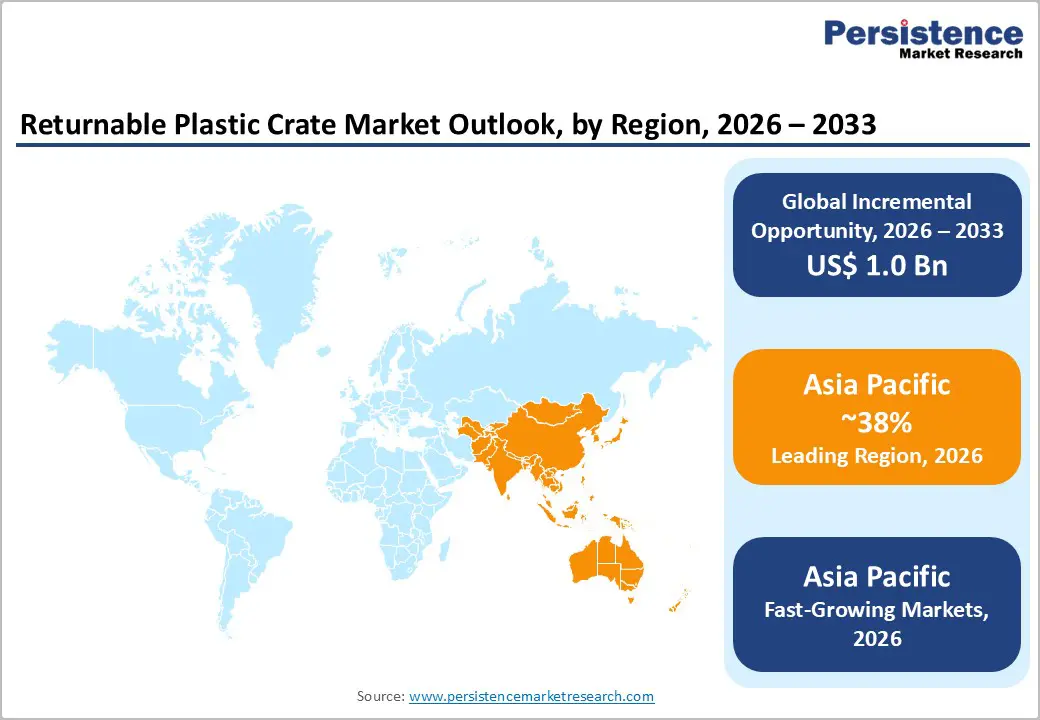

- Leading Region: Europe leads global adoption with 28% market share driven by EU PPWR regulatory mandates requiring 40-70% reusable transport packaging by 2030-2040, accelerating retailer and producer transitions from single-use corrugated packaging toward standardized returnable crate systems across food logistics.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, with a projected 6.8% CAGR through 2033, supported by the explosive expansion of modern retail formats, e-commerce grocery platforms, and cold-chain infrastructure in China, India, and ASEAN countries, which is

- driving returnable crate adoption.

- Leading Capacity: The 10 Kg to 20 Kg capacity segment dominates with 37% market share due to its optimal suitability for grocery and fresh produce, while the 21 Kg to 35 Kg band is the fastest-growing at a 6.2% CAGR, addressing heavier applications in meat, seafood, and industrial segments.

- Leading Material Type: Stackable HDPE crates remain dominant with a 52% share, reflecting automation compatibility and food-logistics suitability, whereas collapsible PP crates are the fastest-growing at a 6.5% CAGR, providing 70-75% empty-return space savings, vital for long-distance and e-commerce supply chains.

- Key Opportunity: Smart reusable transport packaging integrating RFID/IoT tracking, post-consumer recycled (PCR) content, and platform-based pooling services represents the key market opportunity, enabling optimized asset utilization, lower lifecycle emissions, and alignment with tightening global regulatory requirements.

| Key Insights | Details |

|---|---|

|

Returnable Plastic Crate Market Size (2026E) |

US$ 2.1 billion |

|

Market Value Forecast (2033F) |

US$ 3.1 billion |

|

Projected Growth CAGR (2026-2033) |

5.6% |

|

Historical Market Growth (2020-2025) |

5.4% |

Market Dynamics

Drivers - Regulatory Compliance and Circular Economy Mandates

Packaging waste regulations are emerging as a dominant growth catalyst for the returnable plastic crate market worldwide. The European Commission’s PPWR, effective from 2025, establishes legally binding reuse targets requiring 40% of most transport packaging to be reusable by 2030, escalating to 70% by 2040. These regulations are coupled with strict landfill and incineration bans, effectively penalizing single-use corrugated and film packaging solutions.

Beyond Europe, similar extended producer responsibility (EPR) schemes are spreading across North America, the Asia Pacific, and other regions, compelling brand owners and logistics providers to transition toward standardized reusable transport packaging systems. Leading pooling operators report that returnable plastic crate systems prevent millions of tonnes of packaging waste annually while reducing carbon emissions by approximately 40-50% compared to single-use alternatives, providing quantifiable environmental justification for investment in reusable infrastructure.

Operational Efficiency and Supply Chain Cost Reduction

Returnable plastic crates deliver substantial operational advantages that extend beyond environmental benefits, including significant cost savings and improved product quality across supply chains. HDPE and PP-based crates provide superior durability, standardized dimensions for automated handling, and a reusable design that dramatically reduces per-unit packaging costs over multiple trips compared to disposable alternatives. Studies demonstrate that returnable crate systems improve truck fill factors by 15-25%, reduce product damage in fresh food logistics by 30-40%, and enable direct store delivery in shelf-ready crates, eliminating secondary unpacking and reducing labor requirements.

Retailers increasingly integrate returnable crates with RFID and barcode tracking systems, enabling real-time asset visibility and optimizing pool sizes. The cumulative effect of reduced material consumption, improved logistics density, lower labor costs, and enhanced product quality creates compelling business cases that drive accelerating adoption across grocery, produce, dairy, and meat distribution networks.

Restraint - High Capital Requirements and Reverse Logistics Complexity

Establishing effective returnable crate systems requires substantial upfront capital investment in multiple areas, including crate manufacturing, cleaning facilities, IT infrastructure, and logistics networks for reverse flows. Small and mid-sized producers, particularly in developing economies with limited capital availability, face significant barriers to adopting returnable crate systems despite attractive lifecycle economics.

Building effective reverse logistics requires close coordination among growers, packers, retailers, and logistics providers; inefficiencies in return flows result in crate loss, theft, and damage, eroding the business case. Regional manufacturers and smaller distribution networks often lack the scale to justify investment in dedicated cleaning facilities and asset management systems, leading to fragmentation in returnable crate adoption across geographic markets and limiting overall market penetration.

Material Sustainability Concerns and Recycling Infrastructure Gaps

While returnable plastic crates demonstrate superior lifecycle environmental performance compared to single-use packaging, public and regulatory scrutiny of plastic materials remains intense globally. HDPE and PP are derived from fossil feedstocks, and ensuring high end-of-life recycling rates is critical to delivering promised circular economy benefits. Many regions, particularly in developing economies and parts of Latin America and Africa, lack adequate plastics recycling infrastructure, limiting material recovery and raising concerns about actual circular performance.

New EU regulations mandating minimum recycled content and enhanced recyclability create compliance complexity and increase manufacturing costs. Market participants must invest in design-for-recycling initiatives and establish partnerships with certified recyclers to demonstrate closed-loop systems, adding cost and complexity to operations.

Opportunity - E-commerce, Cold Chain, and Last-Mile Delivery Expansion

The explosive growth of e-commerce grocery, meal kit delivery services, and organized cold-chain logistics creates substantial new demand drivers for returnable plastic crates. Modern fulfillment centers, automated warehouses, and dark stores increasingly specify standardized, stackable plastic crates that integrate seamlessly with conveyor systems, robotic picking equipment, and automated sorting networks. Quick-commerce and last-mile delivery models require lightweight, collapsible crate designs that minimize return logistics costs and empty vehicle space, creating specific demand for advanced PP collapsible configurations.

Pooling service providers are developing specialized crate designs for temperature-controlled logistics, enabling seamless movement of fresh, frozen, and perishable products through extended supply chains. This emerging ecosystem of reusable transport packaging solutions for modern logistics creates multi-billion-dollar addressable markets for manufacturers offering integrated crate systems, pooling services, and digital asset management capabilities optimized for e-commerce and cold-chain applications.

Advanced Materials, Digital Integration, and Sustainability Certification

Innovation in materials science and digital technologies presents compelling growth opportunities for returnable plastic crate manufacturers. The development of high-recycled-content HDPE and PP formulations that utilize post-consumer recycled (PCR) plastics while maintaining performance standards directly addresses regulatory requirements and customer sustainability objectives. Integration of RFID tags, IoT sensors, and artificial intelligence-driven analytics enables real-time crate pool optimization, predictive maintenance, and data-driven asset management, improving utilization rates by 15-20%.

Advanced crate designs incorporating lightweight materials, optimized geometries, and durable surface coatings extend service life while reducing weight and transport emissions. Third-party sustainability certifications and transparent lifecycle assessment documentation enable market differentiation and justify premium pricing. Market participants investing in certified circular design, recycled content sourcing, and smart logistics integration are positioned to capture substantial value as regulations tighten and corporate sustainability commitments drive procurement decisions.

Category-wise Analysis

Capacity Insights

The 10-20 Kg capacity segment is the leading category, commanding approximately 37% market share in 2025, reflecting its optimal suitability for grocery, fresh produce, and dairy applications. This capacity range aligns with ergonomic handling standards, typical consumer unit sizes, and pallet efficiency requirements in retail distribution. Retailers and producers specify crates in this range for shelf-ready merchandising and standardized backroom operations.

The 21 Kg to 35 Kg segment is the fastest-growing capacity band, with a projected 6.2% CAGR through 2033, driven by expanding adoption in meat, seafood, beverage, and heavier industrial components. As supply chains consolidate into larger regional hubs and longer distribution routes become economically viable, higher-capacity crates reduce per-unit handling costs and trip frequencies while remaining compatible with automated warehouse systems, creating accelerating demand in this segment.

Product Type Insights

Stackable returnable plastic crates represent the dominant product configuration, accounting for approximately 52% market share in 2025, reflecting their critical role in food and grocery logistics. Stackable crates provide robust vertical load capacity, standardized pallet compatibility, and seamless integration with racking systems and automated warehousing equipment. This configuration is the standard for major pooling systems operated by Brambles, CHEP, and IFCO across the global fresh produce, meat, and dairy supply chains.

However, collapsible crates are the fastest-growing product type, with a projected 6.5% CAGR through 2033, driven by e-commerce fulfillment centers and long-distance distribution networks seeking a 70-75% reduction in empty-return volume. Large retailers and logistics providers increasingly specify collapsible formats where transport costs and reverse logistics complexity are significant operational constraints.

Material Insights

High-density polyethylene (HDPE) is the leading material, with approximately 61% market share in 2025. HDPE offers superior impact resistance, excellent low-temperature performance, moisture resistance, and well-established regulatory approvals for food-contact applications. It is the standard material for multi-trip crates used in the supply chains for fruits, vegetables, meat, and dairy.

Polypropylene (PP) accounts for approximately 30% market share and is the fastest-growing material segment, with a projected 6.3% CAGR through 2033. PP provides higher stiffness and superior heat resistance, making it advantageous for high-temperature cleaning processes and demanding industrial environments. Advanced material formulations incorporating recycled content while maintaining performance specifications are enabling sustainable crate designs that align with corporate and regulatory sustainability objectives.

Application Insights

Grocery applications represent the leading segment, commanding approximately 34% market share in 2025, reflecting its role as the largest end-use segment for returnable plastic crates globally. Supermarkets and hypermarkets extensively use returnable plastic crates for fruits, vegetables, bakery products, and dairy products, leveraging their durability, cleanliness, and ability to serve as both transport and display containers.

Major global retailers, including Walmart, Carrefour, and Tesco, have implemented systematic returnable crate programs, reducing packaging waste and improving logistics efficiency across supply chains. The grocery segment benefits from high-volume, frequent-rotation crate utilization, which optimizes economics and justifies pooling infrastructure investment. Standardized crate specifications across grocery retailers enable interoperability and efficient pool management, creating the critical mass necessary for successful returnable transport packaging systems.

Regional Insights

North America Returnable Plastic Crate Market Trends and Insights

North America represents a mature and increasingly sophisticated market for returnable plastic crates. The United States anchors regional growth, supported by well-developed pooling infrastructure, national retail chains, and advanced logistics networks. Brambles operates extensive CHEP and IFCO pooled crate systems serving major retailers and FMCG companies across fresh produce and food categories, enabling significant waste reduction and supply chain optimization.

Growing regulatory pressure from state-level extended producer responsibility (EPR) initiatives and corporate ESG commitments is accelerating the adoption of returnable crates in the region. Leading retailers, including Walmart, Target, and Costco, are expanding reusable packaging programs to reduce waste and minimize emissions. Innovation in North America focuses heavily on integrating crates with digital asset-tracking systems, using RFID and barcoding, to reduce shrinkage and optimize pool management. Emerging e-grocery and last-mile delivery models are piloting reusable containers for click-and-collect and home-delivery operations, creating incremental demand for innovative crate designs suited to modern retail channels.

Europe Returnable Plastic Crate Market Trends and Insights

Europe is the global leader in regulatory-driven adoption of returnable plastic crates. The European Union’s ambitious PPWR and broader Green Deal agenda are fundamentally reshaping packaging practices, with legally binding reuse targets requiring 40% of transport packaging to be placed in certified reuse systems by 2030, rising to 70% by 2040. Germany, France, Spain, and the United Kingdom are leading adoption, with major retailers and producers implementing systematic returnable crate programs across fresh food supply chains.

European manufacturers and pooling operators are investing heavily in design-for-recyclability and development of HDPE/PP crates incorporating significant post-consumer recycled content. The region’s advanced recycling infrastructure and established deposit and reuse traditions create optimal conditions for closed-loop circular systems. Labor costs and space constraints in dense urban areas drive strong demand for automation-compatible crates that stack precisely and integrate with conveyor systems. Environmental NGOs and certification bodies are establishing rigorous lifecycle assessment and circular-economy standards, raising expectations for transparent sustainability documentation and creating opportunities for market-leading participants to differentiate.

Asia Pacific Returnable Plastic Crate Market Trends and Insights

Asia Pacific is projected to be the fastest-growing regional market, with an estimated 6.8% CAGR through 2033 and approximately 38% global market share in 2025. Rapid expansion of modern retail formats, e-commerce grocery platforms, and cold-chain infrastructure in China, India, and ASEAN countries is driving an accelerating demand for standardized returnable crate systems. China represents the largest regional market, with major retailers and e-commerce platforms implementing extensive returnable packaging programs aligned with national resource-efficiency and waste-reduction objectives.

India is experiencing explosive growth driven by the modernization of agricultural value chains, the expansion of cold storage capacity, and rising export demand for fresh produce and seafood. Regional manufacturers such as Zhejiang Zhengji Plastic Industry Co. Ltd. and Supreme Industries Limited are expanding production capacity to serve rapidly growing domestic and export markets. Across ASEAN, increasing export volumes of fresh produce, seafood, and processed foods are raising packaging standards and hygiene requirements, making returnable plastic crates increasingly attractive for export-oriented supply chains. Manufacturing cost advantages and expanding polymer processing capacity position Asia Pacific as both the fastest-growing consumption center and a critical production hub for returnable plastic crates serving global supply chains.

Competitive Landscape

The returnable plastic crate market displays a moderately fragmented to semi-consolidated structure, shaped by the presence of global pooling operators, established regional manufacturers, and cost-competitive local suppliers. Competition is largely influenced by the ability to manage large circulating crate pools, offer standardized and interoperable designs, and support multi-customer logistics networks. Leading participants focus on pool-based business models that reduce upfront capital requirements for users while improving asset utilization and lifecycle efficiency.

Product strategies emphasize durability, ergonomic handling, automation compatibility, and compliance with food safety and sustainability standards. Increasing use of recycled polymers and lightweight designs supports corporate sustainability goals and regulatory compliance. Digital capabilities such as RFID and IoT-enabled tracking are becoming core differentiators, enabling real-time visibility, loss reduction, and optimized reverse logistics. Regional players compete through customization, localized manufacturing, and responsive service support. Overall, platform-driven pooling, rental, and pay-per-use models are reshaping competitive dynamics and driving long-term customer lock-in.

Key Market Developments

- June 2024: Schoeller Allibert and Coca-Cola Europacific Partners have developed beverage crates made from 97% recycled plastic, reducing CO2 emissions by 66% and promoting a circular economy in the Netherlands, in collaboration with Healix for sustainable packaging innovation.

- March 2025: Tetra Pak and Schoeller Allibert launch innovative transport crates made from polyAl derived from used beverage cartons, integrated with other recycled materials without virgin plastics, currently in field tests for durability to advance sustainable packaging solutions.

- May 2025: Bouncee launches a collapsible, insulated reusable crate for temperature-controlled food and pharmaceutical logistics, offering precise control for transits under 14 hours, a lightweight design, extended durability, and cost efficiency, winning the Transit category at the 2025 WorldStar Global Packaging Awards.

- December 2025: Iperal, an Italian retailer, has adopted reusable plastic crates and bins supplied by Tosca for its fresh produce operations. This follows the opening of a new automated Fresh Food Centre in Giussano, aiming to reduce waste, standardize packaging, improve logistics, minimize losses, and enhance sustainability by replacing single-use materials.

Companies Covered in Returnable Plastic Crate Market

- Brambles Limited

- Myers Industries Inc.

- Supreme Industries Limited

- Schoeller Allibert Services B.V.

- DS Smith PLC

- Rehrig Pacific Company Inc.

- IPL Plastics Inc.

- Craemer UK Limited

- Dynawest Limited

- Zhejiang Zhengji Plastic Industry Co. Ltd.

- Stamford Products Limited

- IFCO Systems

- ORBIS Corporation

- RPC Group

- Georg UTZ Holding AG

- Bekuplast GmbH

- Craemer Group

Frequently Asked Questions

The returnable plastic crate market is projected to reach US$ 2.1 billion in 2026 and grow at a 5.6% CAGR through 2033.

Demand is driven by reusable packaging regulations, sustainability targets, supply chain efficiency needs, and growth in e-commerce and cold-chain logistics.

Europe leads due to strict packaging regulations, while Asia Pacific is the fastest-growing region.

Smart returnable crates with RFID/IoT tracking, recycled materials, and pooling services represent the strongest growth opportunity.

Key market players include Brambles Limited, DS Smith PLC, Schoeller Allibert Services B.V., Supreme Industries Limited, and Myers Industries Inc.