- Marine

- Rescue Boat Market

Rescue Boat Market Size, Share, and Growth Forecast, 2026 – 2033

Rescue Boats Market by Boat Type (Lifeboats, Fast Rescue Boats, Assault/Combat), Propulsion (Outboard Motors, Inboard Engines, Water Jet), Application (Offshore Energy, Coast Guard/Defense, Commerce), and Regional Analysis 2026 – 2033

Rescue Boat Market Size and Trends Analysis

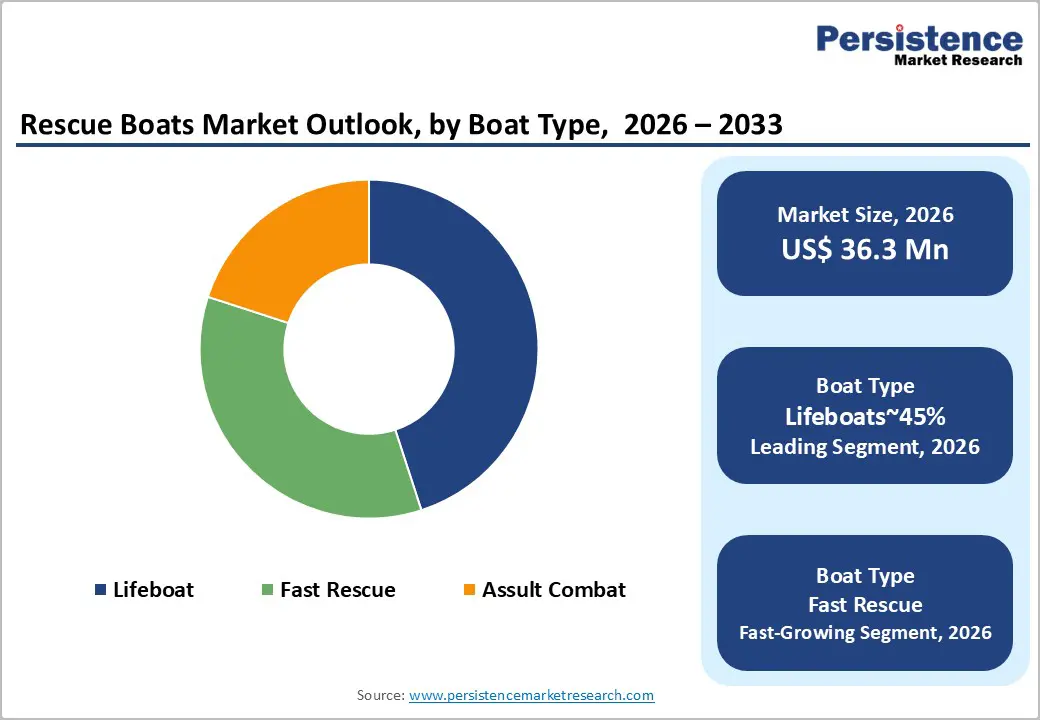

The global rescue boat market size is likely to be valued at US$252 million in 2026 and is expected to reach US$309.9 million by 2033, billion CAGR of 3.0% during the forecast period from 2026 to 2033, driven by technological innovations (e.g., electric propulsion, advanced navigation), expanding offshore wind and oil/gas activities requiring support vessels, and global climate-related disaster preparedness. The market's trajectory is fundamentally underpinned by the rigorous enforcement of International Maritime Organization (IMO) safety mandates and the burgeoning offshore energy sector, particularly in wind farm developments requiring specialized Fast Rescue Boats (FRBs).

Key Industry Highlights:

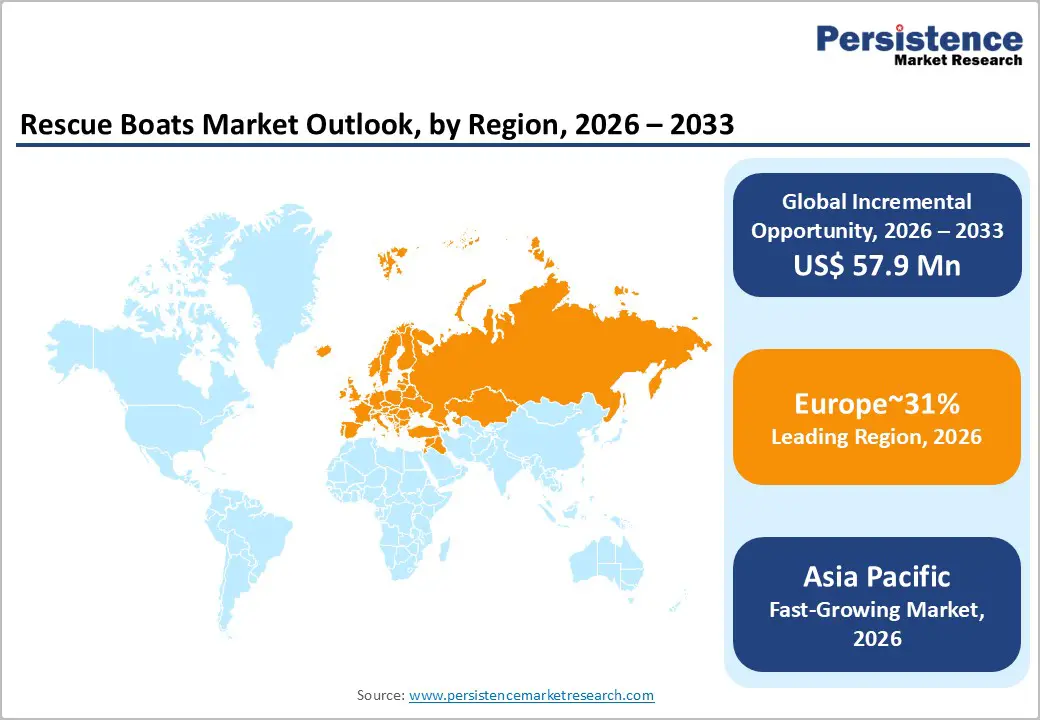

- Leading Region: Europe is expected to lead with approximately 31% share, anchored by stringent maritime safety regulations and strong offshore energy activity.

- Fastest growing Region: Asia Pacific is projected to be the fastest growing, supported by expanding port infrastructure, coastal surveillance investments, and offshore energy development.

- Leading Boat Type: Lifeboats are expected to lead with around 45% share, reflecting mandatory deployment across offshore platforms, commercial shipping, and marine safety regulations.

- Leading Propulsion Type: Outboard motors are expected to lead with approximately 56% share, supported by ease of maintenance, modular replacement, and suitability for multi-mission rescue craft.

| Global Market Attributes | Key Insights |

|---|---|

| Rescue Boat Market Size (2026E) | US$252.0 Mn |

| Market Value Forecast (2033F) | US$309.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 3.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Expansion of the Offshore Renewable Energy Sector

The acceleration of offshore renewable energy deployment is structurally expanding demand for fast rescue boats within offshore wind operations. Wind farms are increasingly located in high-energy sea states and remote offshore zones, creating sustained requirements for rapid-response, high maneuverability rescue craft to support installation, operations, and maintenance activities. Service operation vessels and installation platforms supporting wind assets require certified rescue craft as part of maritime safety compliance frameworks, embedding FRB procurement into project-level marine logistics and safety budgets.

This demand profile is reshaping propulsion and design preferences within the FRB segment. Operators prioritize configurations that enable safe personnel recovery in adverse sea conditions, favoring water jet propulsion systems due to reduced propeller-related hazards during persons-in-water recovery operations and superior low-speed maneuverability near structures. As offshore wind capacity scales across mature and emerging maritime basins, the sector is becoming a stable, non-cyclical demand anchor for FRBs, diversifying the historical dependence on oil and gas offshore activity and rebalancing the propulsion mix toward jet-driven platforms.

Stringent Maritime Safety Regulations under SOLAS and LSA Code

The rescue boat market is structurally anchored to mandatory compliance frameworks governing maritime safety, with SOLAS provisions and the Life Saving Appliances Code embedding rescue craft as non-discretionary components of commercial vessel equipment. Regulatory prescriptions define minimum carriage requirements, performance specifications, and safety-critical design features, translating statutory compliance into baseline, inelastic demand across the global merchant fleet. Periodic regulatory updates addressing release mechanisms, hull integrity, and operational safety elevate technical thresholds for installed equipment, converting compliance revisions into accelerated replacement and retrofit cycles across existing fleets. This embeds regulatory change as a continuous demand catalyst rather than a cyclical procurement driver.

Compliance-driven demand shapes procurement toward certified designs, audited manufacturing processes, and traceable component sourcing, raising entry barriers and compliance costs for suppliers. Retrofit obligations reallocate spending from newbuild programs toward aftermarket replacement and recertification services, strengthening service-led revenue streams alongside equipment sales. Regulatory enforcement regimes and port state control inspections increase the economic penalty of non-compliance, elevating reliability and certification continuity as core purchasing criteria. As fleet capacity expands, the regulatory linkage between vessel count and rescue craft provisioning structurally scales the addressable market in direct proportion to maritime safety obligations.

Barrier Analysis – Transition to Green Propulsion Cost and Weight Constraints

Decarbonization pressures within maritime safety equipment are introducing structural cost and engineering barriers for rescue boat platforms as electric and hybrid propulsion architectures are evaluated against stringent performance and certification requirements. Battery-based systems materially increase mass and volume relative to conventional propulsion, conflicting with davit load limits and launch envelope constraints embedded within vessel safety systems. These physical trade-offs complicate compliance with stability, buoyancy, and deployment performance standards, raising redesign and requalification burdens across hull structures, lifting interfaces, and propulsion integration. The resulting engineering complexity elevates development cost and lengthens certification cycles, constraining near-term adoption across safety-critical craft.

At the value-chain level, propulsion electrification shifts cost structures toward higher upfront capital intensity and specialized component sourcing, including energy storage, power management electronics, and lightweight composite integration. Regulatory certification frameworks for life-saving appliances impose conservative validation thresholds for new propulsion technologies, increasing testing scope and compliance expenditure. Infrastructure limitations for charging and maintenance across diverse port environments further complicate lifecycle economics and service readiness. Collectively, these constraints slow diffusion of green propulsion within rescue boat fleets by embedding weight, cost, and certification frictions into procurement decisions for safety-mandated equipment.

Long Replacement Cycles

Fast rescue boats are engineered for extreme durability and regulatory compliance in harsh offshore environments, resulting in long operational lifecycles before fleet replacement becomes necessary. Extended service lives materially reduce the cadence of new-build procurement across commercial offshore operators, public safety agencies, and renewable energy service fleets. As a result, original equipment demand is inherently cyclical and tied more closely to capacity additions and regulatory step-changes than to routine replacement-driven growth.

These structural dynamics compress addressable demand for new vessels and shift revenue dependence toward aftermarket, refit, and service activities. While maintenance, certification, and life-extension programs provide recurring cash flows, these streams typically carry lower margins and higher operational intensity than new-build contracts. Manufacturers, therefore, face a constrained growth ceiling in mature markets, with scale expansion increasingly contingent on penetration into new offshore wind projects, regulatory-driven fleet standard upgrades, and technology-led differentiation that can justify early replacement or mid-life retrofits.

Opportunity Analysis – Electrification of Rescue Craft

Decarbonization mandates within maritime transport are extending into auxiliary and safety equipment, creating a structurally underpenetrated opportunity for electric and hybrid rescue craft aligned with low-emission vessel architectures. As fleet operators and shipbuilders internalize emissions accounting across entire vessel systems, rescue boats are increasingly evaluated for compatibility with environmental compliance frameworks governing noise, discharge risk, and localized air quality. Electric outboards and waterjet propulsion offer operational advantages in torque delivery and reduced mechanical complexity, aligning with emergency-response requirements while lowering maintenance intensity across safety fleets. This positions electrified rescue craft within broader vessel decarbonization pathways rather than as isolated sustainability add-ons.

The adoption of electric rescue craft reallocates demand toward propulsion electronics, energy storage integration, and lightweight structural engineering to preserve launch envelope compliance. The current supply gap for compliant electric rescue platforms embeds first-mover advantages for manufacturers capable of integrating propulsion electrification with davit compatibility and safety certification. These dynamics structurally expand the addressable market for electrified rescue solutions across regulated coastal and inland waterways.

Digital Integration and Remote Monitoring

The integration of digital technologies into rescue boat platforms presents a high-value opportunity to move from asset-centric procurement toward capability-led fleet modernization. Embedding advanced navigation, situational awareness, and connectivity systems into fast rescue boats enables operators to improve mission effectiveness in low-visibility and high-sea-state conditions while strengthening coordination with shore-based command centers. Integrated GPS, thermal imaging payloads, and high-bandwidth connectivity support faster target acquisition, safer maneuvering near persons in the water, and continuous telemetry of vessel health and mission status. This elevates rescue craft from standalone response assets to nodes within a connected maritime safety network.

From a commercial perspective, digitalization expands the addressable value per vessel and opens recurring revenue streams through software, analytics, and service contracts. Remote monitoring supports predictive maintenance, compliance reporting, and fleet optimization, reducing downtime and total cost of ownership for operators. Vendors that offer modular digital retrofit kits can monetize existing fleets, mitigating long replacement cycles while accelerating adoption. Strategic partnerships with connectivity providers and sensor manufacturers further enable bundled solutions, positioning OEMs and integrators to capture premium margins in offshore wind support, coast guard operations, and industrial maritime safety segments.

Category–wise Analysis

Boat Type Insights

Lifeboats are projected to dominate the boat type segment of the marine safety equipment market, accounting for approximately 45% share in 2026, underpinned by mandatory carriage requirements under SOLAS and LSA codes across commercial shipping, offshore energy assets, and large passenger vessels. Adoption remains anchored by regulatory compliance, proven survivability performance, and lifecycle reliability, with fleet operators prioritizing standardized lifeboat configurations to streamline certification, spares provisioning, and crew training across multi-vessel fleets. Ongoing platform evolution, including totally enclosed motor-propelled survival craft, fire-protected hulls for tanker applications, and davit integration upgrades, continues to reinforce replacement cycles and utilization intensity in regulated environments.

Fast rescue boats (FRBs) are anticipated to be the fastest-growing boat type within the marine safety equipment market, driven by operational response gaps that conventional lifeboats cannot address across offshore wind farms, cruise operations, and high-traffic port environments. Growth is being catalyzed by advances in lightweight composites, high-output propulsion systems, and hull forms optimized for rapid launch and recovery, which materially improve response time, maneuverability, and crew safety during man-overboard and emergency response scenarios. Accelerating adoption is supported by tighter safety management systems, integrated launch-and-recovery automation, and interoperability with vessel safety architectures, lowering operational friction for first-time adopters.

Propulsion Type Insights

Outboard motors are projected to dominate the marine safety boats propulsion market, accounting for approximately 56% share in 2026, underpinned by their entrenched role in SOLAS-compliant rescue boats, rigid inflatable boats, and light-duty patrol craft across commercial shipping, port authorities, and nearshore coast guard operations. Ongoing platform evolution, including higher power-to-weight ratios, digital engine management, and electrified outboard variants for low-emission zones, continues to reinforce replacement cycles and utilization intensity. Vendors such as Yamaha, Mercury Marine, and Honda Marine are expanding propulsion portfolios with modular platforms and service ecosystems to lock in fleet workflows and long-term service contracts.

Water jet propulsion is anticipated to be the fastest-growing segment within the marine safety boats propulsion market, driven by safety-critical operational gaps and maneuverability limitations associated with conventional propeller systems across offshore energy, naval, and complex nearshore response scenarios. Accelerating adoption is supported by tighter safety management systems, digital vessel control integration, and interoperability with launch-and-recovery automation, lowering operational friction for first-time adopters. Companies, Hamilton Jet, Kongsberg Maritime, and Rolls-Royce Power Systems, are scaling water jet platforms and service models to capture early-cycle demand and embed switching costs.

Regional Insights

Europe Rescue Boat Market Trends

Europe is expected to lead the global maritime rescue boats and lifeboat systems market, with an estimated share of around 31% in 2026, anchored by its concentration of offshore energy assets and technologically advanced maritime fleets. The North Sea operating environment continues to shape demand for high-sea-state capable rescue craft, as offshore wind farms and legacy oil and gas platforms require purpose-built tenders for crew transfer, emergency evacuation, and rapid-response search and rescue. Germany, Norway, and the U.K. remain the primary demand centers, where large offshore wind project pipelines and dense shipping corridors sustain steady replacement and upgrade cycles for safety fleets.

The regional market is also defined by its early adoption of low-emission propulsion architectures for rescue craft, with electric and hybrid configurations increasingly specified for offshore service vessels operating near wind farms and environmentally sensitive coastal zones. This transition is expected to reshape procurement specifications toward higher power electronics content, advanced energy management systems, and modular propulsion layouts suited for harsh-weather operations. Europe’s leadership in offshore engineering and high-reliability marine systems positions the region to remain the reference market for advanced rescue craft designs optimized for rough-sea performance, operational endurance, and low-emission compliance.

Asia Pacific Rescue Boat Market Trends

Asia Pacific is expected to be the fastest-growing region in the global maritime rescue and lifeboat market, driven by its position as the world’s dominant shipbuilding and marine manufacturing base. China, South Korea, and Japan anchor demand through continuous newbuild activity across commercial shipping, offshore support vessels, and coastal fleets, creating a sustained original-equipment requirement for certified lifeboats and rescue craft. This newbuild-driven baseline is reinforced by expanding retrofit demand as regional fleets modernize safety equipment to align with evolving international safety norms. Rising port throughput, denser coastal traffic, and increasing offshore activity in regional energy and subsea construction also extend the addressable market beyond shipyards into port authorities, coast guards, and offshore service operators.

The region’s structural advantage lies in manufacturing depth and cost efficiency, with China functioning as a central production hub for hulls, davits, and core components, enabling shorter lead times and competitive pricing for both domestic and export markets. Product demand is gradually shifting toward higher-speed rescue craft and more versatile multipurpose boats suited for tourism-heavy coastlines, offshore wind support, and emergency response in congested littoral zones. As regulatory enforcement tightens across major ports and flag states align more closely with global maritime safety conventions, retrofit cycles are expected to intensify, further reinforcing Asia Pacific’s role as the primary growth engine for the global rescue and lifeboat ecosystem.

North America Rescue Boat Market Trends

North America is expected to remain a mature, high-value market for maritime rescue boats and lifeboat systems, supported by sustained public-sector procurement and a strong defense and homeland security orientation. Programs such as the U.S. Coast Guard’s Over-the-Horizon boat deployments illustrate how rescue boats are embedded within multi-platform procurement strategies rather than treated as standalone assets. Demand is therefore structurally resilient, tied to replacement cycles, life-extension programs, and mission upgrades across federal agencies, port authorities, and offshore operators. Canada complements this base through Arctic and coastal safety requirements, where harsh operating environments necessitate higher-specification hulls, cold-weather operability, and reliability in remote-response scenarios.

The region also functions as a technology and systems-integration center for advanced rescue platforms. Innovation is concentrated around high-speed interception craft, advanced navigation and situational-awareness suites, and the early adoption of autonomous and remotely operated rescue concepts for hazardous missions. Investment priorities are increasingly aligned with multi-mission architectures, where rescue craft are configured to support surveillance, interdiction, and emergency response within a single modular platform, improving fleet utilization and lifecycle economics.

Competitive Landscape

The global rescue boat market shows a moderately consolidated structure, with a small group of global maritime safety specialists forming the upper tier, while a broad base of regional and niche manufacturers occupies the long tail. The leading players are integrated safety solution providers that combine rescue boats, launch and recovery systems, and lifecycle service offerings, allowing them to embed deeply into fleet procurement and compliance workflows.

Competitive positioning is driven less by unit pricing and more by global service network reach, regulatory compliance capabilities, and platform reliability in harsh operating environments. Mid-tier and regional shipyards compete by addressing localized defense and patrol requirements, customized hull designs, and faster delivery cycles, but remain structurally disadvantaged in international tenders due to limited service infrastructure and certification depth.

Key Industry Developments

- In May 2025, Palfinger Marine successfully tested the "Electric Jib Crane (DKJ)" for rescue operations. This reduces hydraulic oil leak risks and noise levels, aligning with the industry's shift toward "all-electric" deck equipment. Its Factory Acceptance Test (FAT) was officially scheduled for June 2025.

- In April 2025, Survitec released the "Seahaven" system validation study at Seatrade Global. Confirms the feasibility of a single 1,060-person inflatable system, potentially replacing up to four traditional lifeboats.

- In Feb 2024, Ocean Craft Marine introduced the "Amphibious Search and Rescue" 4WD boat. Integrated high-torque 4WD wheels into the hull, allowing rescue teams to drive directly from land into water without a trailer.

Companies Covered in Rescue Boat Market

- VIKING Life-Saving Equipment (Norsafe)

- Palfinger Marine

- Survitec Group

- Zodiac Milpro

- Fassmer

- Hatecke GmbH

- Sealegs International

- ASIS Boats

- Boomeranger Boats

- HLB Co., Ltd.

- Jiangsu Jiaoyan Marine Equipment

- Gemini Marine

- Maritime Partner AS

- Willard Marine

- Narwhal Boats

- Titan Boats

Frequently Asked Questions

The global rescue boat market is projected to be valued at US$252.0 million in 2026 and is expected to reach US$309.9 million by 2033, driven by rigorous IMO safety mandates and expanding offshore energy activity, particularly in offshore wind.

The rapid build-out of offshore wind farms, often located in remote, high-sea-state zones, creates sustained demand for Fast Rescue Boats (FRBs) to support installation, maintenance, and emergency response.]

The global rescue boat market is forecast to grow at a CAGR of 3.0% from 2026 to 2033, reflecting steady, compliance-driven demand tempered by long equipment replacement cycles.

Europe is the leading regional market, accounting for approximately 31% share, anchored by its concentration of offshore wind assets, port expansion, and increasing coastal surveillance investments.

The rescue boat market is moderately consolidated, led by integrated maritime safety specialists such as VIKING Life-Saving Equipment (Norsafe), Palfinger Marine, and Survitec Group, which compete through global service networks, regulatory certification depth, and complete launch-and-recovery system solutions.