- Semiconductor Materials & Components

- Point-of-Sale (POS) Machines Market

Point-of-Sale (POS) Machines Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Point-of-Sale (POS) Machines Market by POS Terminal Type (Fixed POS Terminals, Mobile POS Terminals, Pocket POS Terminals, POS GPS/GPRS), End-user (Restaurants, Retail, Hospitality, Entertainment, Warehouse, Healthcare, Others), and Regional Analysis, 2026 - 2033

Point-of-Sale (POS) Machines Market Size and Trend Analysis

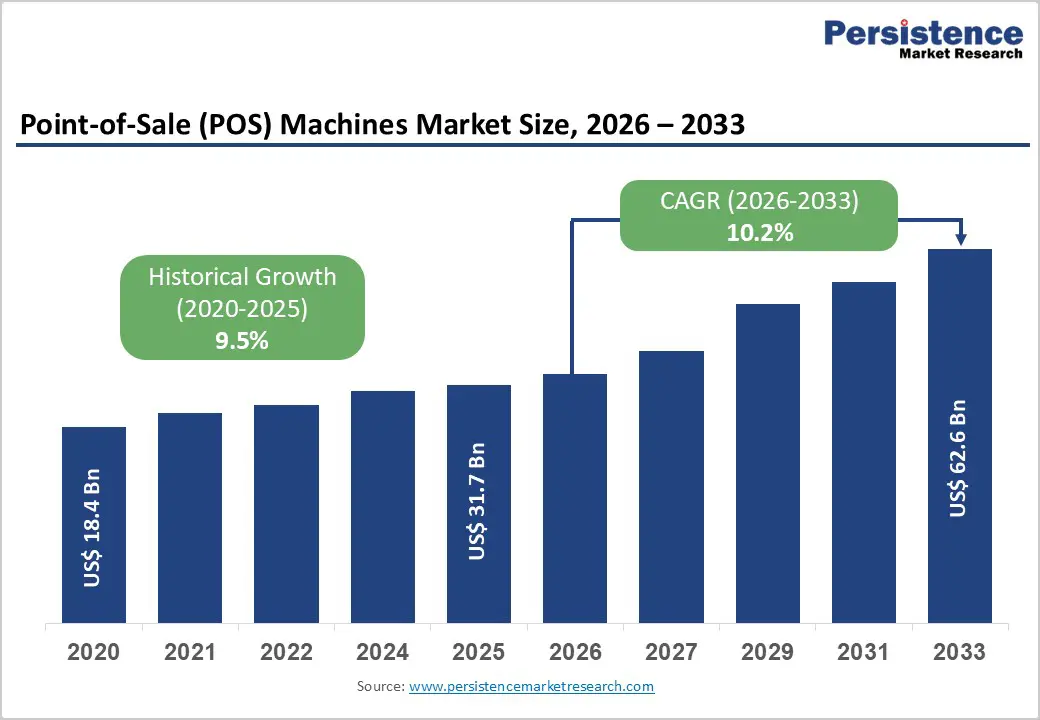

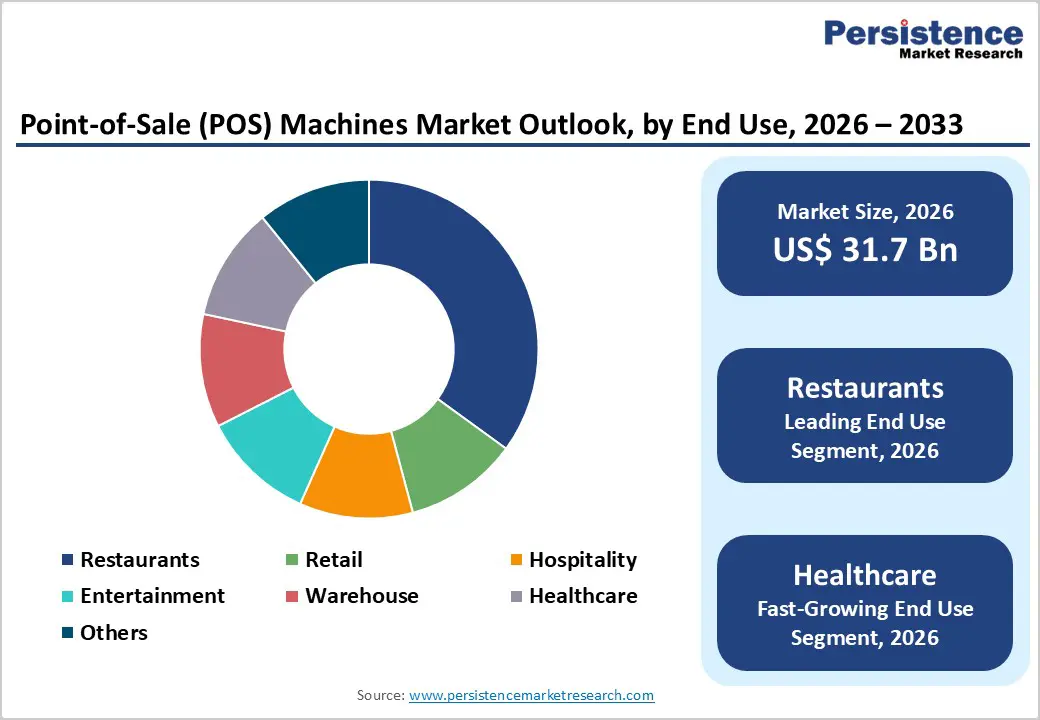

The global point-of-sale (POS) machines market is expected to be valued at US$ 31.7 billion in 2026 and projected to reach US$ 62.6 billion by 2033, growing at a CAGR of 10.2% between 2026 and 2033. This significant growth trajectory reflects the accelerating digital transformation across retail, hospitality, and service sectors.

The market expansion is driven by escalating adoption of contactless payment technologies, particularly Near Field Communication (NFC) and mobile wallet integration, which have become essential in response to consumer preferences for safer, faster transactions. Additionally, the increasing penetration of cloud-based POS systems and AI-powered analytics is enabling businesses to enhance operational efficiency, gain real-time insights into customer behavior, and streamline inventory management across omnichannel environments.

Key Market Highlights

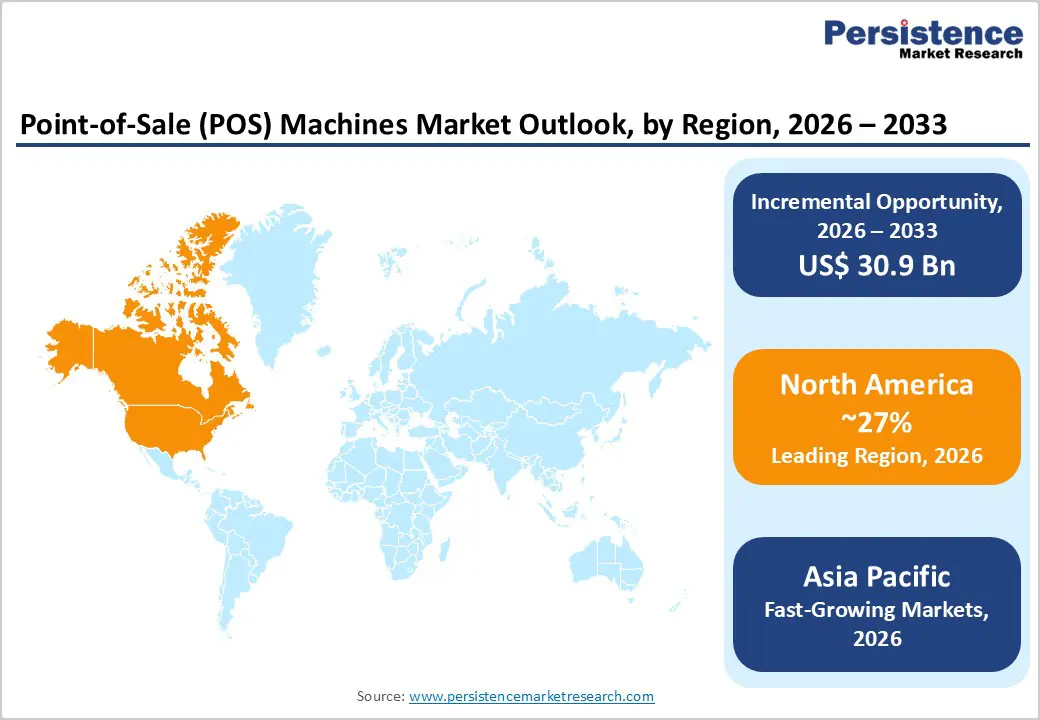

- Leading Region: North America leads the global market with a 27% share in 2025 due to advanced POS infrastructure, high contactless payment usage, and strong vendor presence.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a 12.8% CAGR through 2033, driven by rapid digital payment adoption, government digitalization, and mobile-first ecosystems.

- Dominant Segment: Mobile POS Terminals dominate with about 48% market share in 2025 as businesses prefer portable, low-cost, cloud-integrated payment solutions.

- Fastest Growing Segment: Healthcare and Pharmacy are the fastest-growing end-use segments with a 13.2% CAGR owing to rising e-prescription requirements and broader digital healthcare adoption.

- Key Market Opportunity: The QSR sector offers a major opportunity as AI-driven ordering, delivery platform integration, and high NFC usage transform digital payment workflows.

| Key Insights | Details |

|---|---|

|

POS Machines Market Size (2026E) |

US$ 31.7 billion |

|

Market Value Forecast (2033F) |

US$ 62.6 billion |

|

Projected Growth CAGR(2026-2033) |

10.2% |

|

Historical Market Growth (2020-2025) |

9.5% |

Market Dynamics

Drivers - Digital Payment Adoption and Cashless Economy Initiatives

The transition toward digital and contactless payments represents one of the most compelling growth catalysts for the POS Machines market. According to recent data, mobile wallet usage is projected to reach 5.6 billion users globally by 2025, representing a 7% year-over-year growth, with digital wallets accounting for 50% of global e-commerce transactions. The proliferation of NFC-enabled devices, expected to approach 4.5 billion units by end-2025, underscores the market’s momentum.

In developed markets, over 90% of major U.S. retailers now accept tap-to-pay options, while in emerging economies, particularly India, the momentum is equally impressive, with UPI transactions constituting 49% of global real-time payments and 83% of all digital payments in India as of 2024. This surge in contactless payment preference has compelled retailers, restaurants, and service providers to upgrade their POS infrastructure to support NFC, mobile wallets, and digital payment gateways, directly fueling demand for modern POS Terminals equipped with advanced payment processing capabilities. Furthermore, government mandates for formalization of the unorganized retail sector through digitalization are incentivizing SMEs to adopt POS systems, creating a substantial addressable market in emerging regions.

Rising Demand for Omnichannel Retail Integration and Real-Time Business Intelligence

Modern consumers expect seamless shopping experiences across multiple touchpoints—in-store, online, mobile, and social commerce—creating an imperative for retailers to implement integrated POS systems that synchronize inventory, pricing, and customer data in real time. Cloud-based POS systems are experiencing exceptional growth, with the market projected to reach US$ 30 billion by 2033 at a CAGR of 18.3%, significantly outpacing the broader POS Machines market. The integration of artificial intelligence and machine learning into POS solutions enables businesses to perform predictive analytics, optimize dynamic pricing, detect fraudulent transactions, and personalize customer engagement at scale.

For instance, retailers implementing omnichannel POS systems report 27% faster transaction speeds and 45% reduction in order errors, while chains leveraging integrated loyalty programs see 30% higher average customer spend. The emergence of Buy Online, Pickup In-Store (BOPIS) and ship-from-store fulfillment models necessitates sophisticated POS infrastructure capable of managing complex inventory hierarchies and multi-channel order routing. Additionally, the ability to consolidate data from in-store, delivery, and mobile channels into unified business intelligence dashboards is driving widespread adoption of cloud-connected POS Terminals, particularly among retail and quick-service restaurant (QSR) chains seeking a competitive advantage through data-driven decision-making.

Restraints - High Initial Capital Investment and Legacy System Migration Challenges

Despite strong demand fundamentals, the POS Machines market faces headwinds from the substantial upfront capital expenditure required for hardware procurement, software licensing, and system integration. While cloud-based POS systems have reduced the total cost of ownership, many SMEs and independent retailers operate under tight margin constraints, limiting their ability to invest in infrastructure upgrades.

The migration from legacy on-premise POS systems to modern cloud or hybrid cloud solutions introduces operational complexity, requiring staff retraining and potential business disruption during implementation. Additionally, smaller merchant segments, which represent a significant portion of the addressable market, often lack the technical expertise and IT resources to manage cloud-connected POS infrastructure, creating adoption barriers despite the long-term economic benefits of these solutions.

Data Security Concerns and Regulatory Compliance Requirements

The increasing sophistication of cyber threats targeting point-of-sale systems presents a significant market constraint. PCI DSS (Payment Card Industry Data Security Standard) compliance requirements impose substantial ongoing costs for security upgrades, encryption protocols, and regular audits, particularly for merchants operating across multiple jurisdictions with varying regulatory frameworks.

High-profile data breaches affecting major retailers have amplified customer concerns regarding payment security, creating reluctance among consumers to adopt new payment technologies despite the enhanced security features of modern POS systems. Furthermore, the proliferation of regulations governing payment data protection in regions such as the European Union and emerging markets adds complexity and cost burden on POS solution providers and merchants, potentially slowing market expansion among price-sensitive customer segments.

Opportunity - Rapid Growth in Quick-Service Restaurant (QSR) and Fast-Casual Segments with Advanced Order Management

The global QSR market is projected to grow at 4.6% CAGR through 2030, with 74% of QSR transactions in 2023 involving NFC-based methods like Apple Pay and Google Wallet, up from 43% in 2020. This segment represents a high-value opportunity for POS solution providers offering integrated platforms combining tableside ordering, payment processing, kitchen display systems, and customer loyalty management. Leading chains such as Starbucks and KFC demonstrate the commercial viability of advanced POS systems in this space.

The convergence of mobile ordering, third-party delivery integration, and consumer demand for personalization creates compelling demand for cloud-based, API-enabled POS platforms capable of orchestrating complex omnichannel workflows. Moreover, the adoption of Buy Now, Pay Later (BNPL) solutions integrated into POS systems is expanding payment optionality, with merchants like Burger King and Subway reporting 19% increase in average transaction value through installment payment enablement.

Healthcare and Pharmacy Sector Digitalization with Integrated Prescription and Billing Systems

The healthcare sector, particularly pharmacies and medical clinics, represents an underexploited growth opportunity as regulatory frameworks increasingly mandate electronic prescription processing and digital billing systems. Pharmacy POS systems integrating e-prescription handling, insurance claim automation, and patient data management are driving operational efficiency gains, with implementations showing 25% reduction in inventory discrepancies and 15% increase in prescription processing speed.

The emergence of telepharmacy and digital health services is creating demand for mobile and cloud-based POS solutions capable of supporting remote consultations and contactless dispensing. The integration of AI-powered predictive analytics into healthcare POS systems enables pharmacists to optimize inventory levels based on demand forecasting, reducing medication stockouts and improving patient satisfaction. Government initiatives promoting healthcare digitalization in emerging markets, particularly India with its emphasis on digital payment infrastructure through initiatives like the Payments Infrastructure Development Fund (PIDF), which has deployed 5.45 crore digital touchpoints in tier-3 to tier-6 centers, are expected to accelerate adoption of healthcare POS solutions among clinics and pharmacies.

Category-wise Insights

POS Terminal Type Analysis

Mobile POS Terminals emerge as the leading segment within the POS Terminal Type category, commanding approximately 48% market share in 2025. The dominance of mobile POS solutions reflects the fundamental shift in payment processing from fixed, counter-bound systems to flexible, portable devices that enhance operational efficiency and customer experience. Mobile POS Terminals, including tablet and smartphone-based solutions, offer significant advantages, including lower installation costs, enhanced mobility for tableside payments in restaurants, and seamless integration with modern business management software.

End-Use Sector Analysis

Restaurants command the largest market share within the End-Use category, representing approximately 35% share in 2025. The restaurant sector’s dominance as a POS terminal end-user reflects the critical role of efficient payment processing and order management in hospitality operations.

Quick-Service Restaurants (QSRs), in particular, are adopting POS systems at unprecedented rates to streamline high-volume transaction processing, reduce wait times, and integrate third-party delivery platforms seamlessly. The integration of kitchen display systems with POS terminals has revolutionized order accuracy and kitchen workflow management, with Domino’s Pulse POS system reducing customer support inquiries by 40% through improved order tracking and delivery integration.

Regional Insights

North America Point-of-Sale (POS) Machines Market Trends and Insights

North America maintains the strongest market position globally, commanding approximately 27% of market share in 2025, with the United States leading the region’s adoption trajectory. The U.S. POS market is characterized by high penetration of advanced payment technologies, with over 50% of POS transactions being contactless as of 2025 and projections indicating this share could reach 60% by 2026. The region’s leadership reflects established retail infrastructure, robust technology adoption rates, and the presence of leading POS solution providers. Integration with e-commerce platforms, particularly BOPIS and buy-online-return-in-store capabilities, has become standard requirements in U.S. retail POS deployments, driving demand for sophisticated cloud-connected solutions.

The North American market is also witnessing accelerated adoption of cloud-based POS systems, driven by the region’s high broadband penetration and enterprise software adoption maturity. The shift toward subscription-based POS models rather than perpetual licensing has democratized access to advanced functionality for SMEs, supporting broader market penetration. Furthermore, regulatory initiatives promoting data security and consumer protection, including stringent PCI DSS compliance requirements, have created sustained demand for security-focused POS infrastructure upgrades, positioning North America as a premium market segment with higher average transaction values and advanced feature adoption.

Europe Point-of-Sale (POS) Machines Market Trends and Insights

Europe represents the second-largest regional market, commanding approximately 23% of market share in 2025, with heterogeneous adoption patterns reflecting diverse regulatory environments and retail cultures across member nations. Germany, the United Kingdom, and France lead European adoption, driven by sophisticated retail ecosystems and regulatory harmonization through the EU’s revised Payment Services Directive (PSD2), which has mandated strong customer authentication and open banking standards. The United Kingdom market is particularly advanced, with contactless payment adoption among the highest globally, enabling seamless NFC-based transactions across retail and hospitality sectors. Germany exhibits robust demand for fixed POS Terminals in retail and supermarket applications, with major retailers investing in integrated omnichannel systems to compete with emerging e-commerce threats.

The hospitality sector across Europe is experiencing rapid modernization, with hotels and restaurants implementing cloud-based POS systems integrated with property management and booking platforms. The region is also witnessing strong growth in self-checkout kiosk deployment in supermarkets and hypermarkets, particularly across Scandinavia and Western Europe, where consumer comfort with automated transactions is highest. Moreover, the emphasis on sustainability and digital receipts is reshaping POS system requirements, with solutions incorporating environmental considerations becoming increasingly important in purchasing decisions.

Asia Pacific Point-of-Sale (POS) Machines Market Trends and Insights

Asia Pacific emerges as the fastest-growing region, with market growth projected at 12.8% CAGR during 2026-2033, driven by rapid urbanization, increasing consumer spending, and government initiatives promoting digital payments. China, the region’s largest market, has achieved exceptional penetration of mobile payment technologies, with QR code payments accounting for 40% of all digital payments and platforms like Alipay and WeChat Pay processing trillions of transactions annually. India represents the region’s highest-growth market opportunity, driven by extraordinary digital payment momentum, with UPI transactions reaching 129.3 billion transactions, exceeding Brazil’s 37.4 billion and Thailand’s 20.4 billion transactions.

Government initiatives including the Digital India campaign, the Unified Payments Interface (UPI), and the Payments Infrastructure Development Fund (PIDF) have catalyzed rapid POS terminal deployment across tier-2 and tier-3 cities, with 5.45 crore digital touchpoints deployed in smaller centers. The Asia Pacific region is also witnessing explosive growth in Quick-Service Restaurants (QSRs) and organized retail chains, with major brands from Starbucks to Domino’s establishing a significant presence in China, India, and Southeast Asia. The rapid adoption of Android-based smart POS terminals (with 60% of PAX’s sales comprising Android smart terminals in 2024) reflects regional consumer and merchant demand for feature-rich, software-extensible solutions.

Competitive Landscape

The global POS Machines market is moderately consolidated, with a mix of large multinational providers and a growing base of specialized fintech and software-led entrants shaping market competition. Market structure is defined by the dominance of full-stack solution providers that integrate hardware, payment processing, and cloud software, creating strong customer retention through bundled services and high switching costs.

Competitive strategies increasingly revolve around expanding software capabilities, strengthening cloud ecosystems, and developing vertical-specific solutions for retail, hospitality, and healthcare. Consolidation remains a defining trend, with leading players pursuing acquisitions and strategic partnerships to enhance payment gateways, analytics, and omnichannel integration features. At the same time, the rise of Android-based smart terminals and SaaS-driven POS platforms is lowering barriers to entry, enabling smaller providers to compete through agile software innovation. As AI, biometrics, and machine-learning capabilities become core differentiators, market participants are intensifying R&D investments to remain competitive in an increasingly software-centric POS landscape.

Key Market Developments

- March 2025: PAX Technology announced Android smart terminals exceeding 60% of revenue, SaaS solutions up 30.5% to HK$138.2 million, and Huizhou Smart Terminals Industrial Park commencing operations.

- August 2025: PG Electroplast Limited signed a definitive manufacturing agreement with PAX India to produce PAX-branded POS devices in India, marking its entry into fintech hardware and aligning with the Make in India initiative, with production expected to begin by the end of 2025.

Companies Covered in Point-of-Sale (POS) Machines Market

- Verifone Systems, Inc.

- Ingenico Group (Worldline)

- PAX Technology Ltd.

- Shenzhen Xin Ltd.

- SZZT Electronics

- BBPOS Limited

- Fujian Centerm Information Ltd

- Fujian Newlan Co., Ltd

- New POS Technology Ltd

- Cybernet Manufacturing Ltd

- Castles Technology Co Ltd

- Shenzhen Ejet Technology Co Ltd

- HP Development Company, L.P.

- Posiflex Technology Inc

- Xenial, Inc.

Frequently Asked Questions

The POS machine market is expected to reach US$ 31.7 billion by 2026.

Rising digital payments, financial inclusion initiatives, growth of cloud-based POS, and demand for omnichannel retail integration are the key drivers.

North America leads the market, while the Asia Pacific is the fastest-growing region.

Major opportunities lie in QSR automation, healthcare digital processing, mobile POS adoption, and expansion of cloud-based POS platforms.

Key players include Verifone, Ingenico Group, PAX Technology Ltd, and Shenzhen Xin Ltd.