- Specialty & Fine Chemicals

- Polyisoprene Latex Market

Polyisoprene Latex Market Size, Share, Trends, and Growth Forecast 2025 - 2032

Polyisoprene Latex market by Application (Gloves, Condoms, Medical Balloons, Catheters, Others), End-use (Medical, Consumer Goods), Industrial and Regional Analysis 2025 - 2032

Polyisoprene Latex Market Size and Trend Analysis

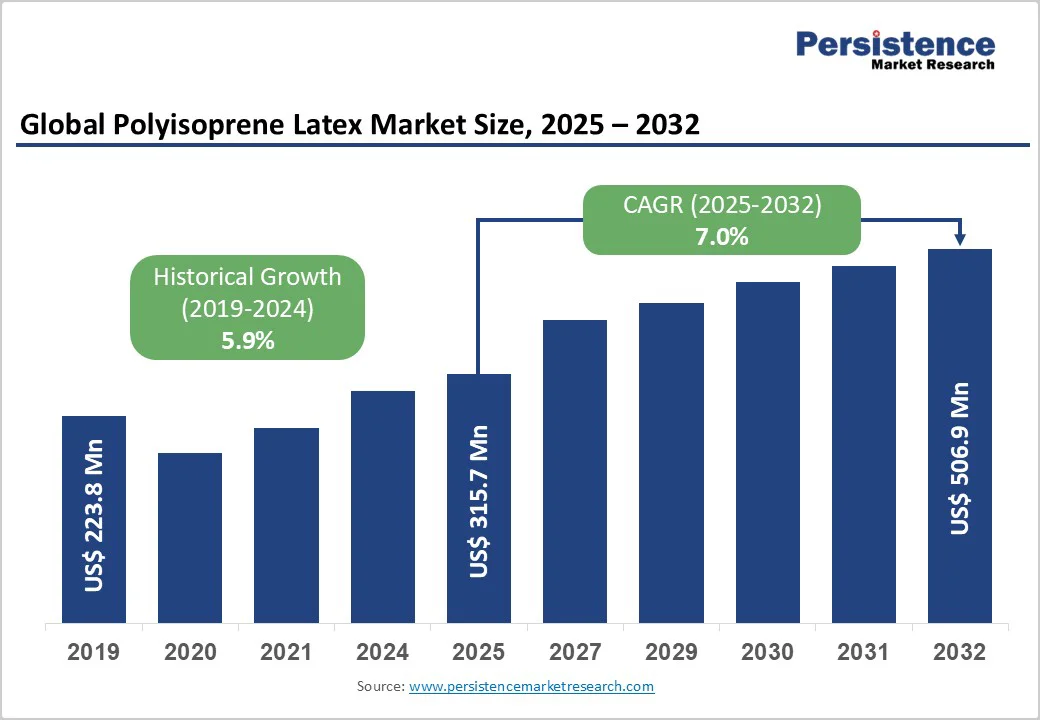

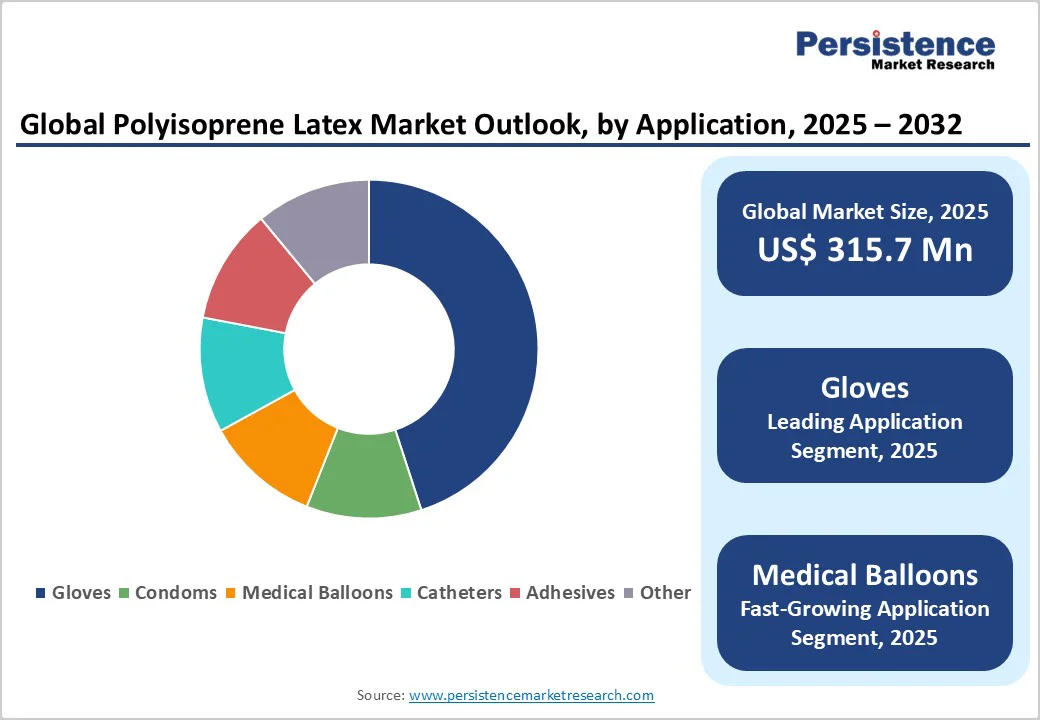

The global polyisoprene latex market size is likely to value at US$ 315.7 Mn in 2025 and is projected to reach US$ 506.9 Mn by 2032, growing at a CAGR of 7.0% between 2025 and 2032.

The surging demand for hypoallergenic materials in healthcare applications, particularly for protective gear such as gloves and catheters benefit from polyisoprene latex's superior elasticity and biocompatibility.

This growth is supported by post-pandemic health protocols emphasizing infection control, with the U.S. Department of Labor projecting over 2.4 million new healthcare jobs by 2030, amplifying the need for reliable synthetic latex alternatives to natural rubber.

Key Market Highlights:

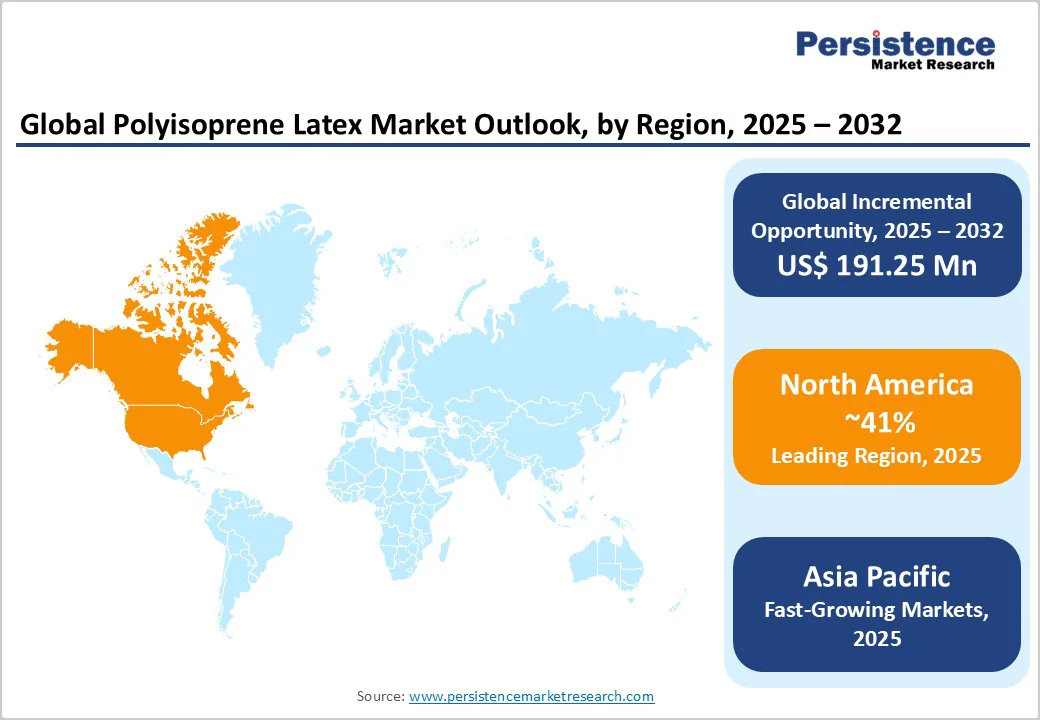

- Regional Leader: North America leads the polyisoprene latex market, with 41%, fueled by U.S. R&D investments and EV sector demands for resilient components.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, due to manufacturing hubs in China and India, supported by rapid healthcare infrastructure growth and cost advantages.

- Leading Segment: Gloves dominate the application category, holding 45% share from essential PPE roles in medical settings worldwide.

- Fastest Growing Segment: Medical end-use grows fastest, driven by biocompatibility needs in catheters and balloons amid rising procedural volumes.

- Growth Opportunities: Sustainable bio-based formulations offer key opportunities, aligning with global green policies and capturing premium eco-market segments.

| Key Insights | Details |

|---|---|

| Polyisoprene Latex Size (2025E) | US$ 315.7 Mn |

| Market Value Forecast (2032F) | US$ 506.9 Mn |

| Projected Growth CAGR (2025 - 2032) | 7.0% |

| Historical Market Growth (2019 - 2024) | 5.9% |

Market Dynamics

Driver - Surging Demand in Healthcare Applications

The growing need for hypoallergenic protective equipment in medical settings is a pivotal growth driver for the polyisoprene latex market. Polyisoprene latex offers exceptional tactile sensitivity and comfort, making it ideal for products like examination gloves and surgical devices, where natural latex allergies affect up to 10-17% of healthcare workers according to studies from the National Institute for Occupational Safety and Health (NIOSH).

This demand has intensified following global health crises, with increased protocols for personal protective equipment (PPE) usage driving adoption.

For instance, the material's biocompatibility ensures low extractables and particulates, aligning with stringent standards from the U.S. Food and Drug Administration (FDA) for medical-grade applications. As healthcare infrastructure expands, particularly in aging populations, this driver is expected to sustain robust growth, enhancing market penetration in disposable medical supplies and fostering innovation in latex formulations for enhanced durability and skin-friendliness.

Advancements in Automotive and Industrial Components

Innovation in synthetic rubber technologies is propelling polyisoprene latex usage in automotive and industrial sectors, where its flexibility and aging resistance outperform traditional materials.

The automotive industry, contributing approximately USD 1.1 trillion to the U.S. economy in 2022 as per the U.S. Bureau of Economic Analysis, increasingly incorporates polyisoprene for seals, gaskets, and vibration dampeners to meet fuel efficiency standards. This trend is reflected in the increase in electric vehicle (EV) production, which necessitates lightweight and resilient components.

According to the International Energy Agency (IEA), global EV sales reached 14 million units in 2023, thereby indirectly elevating the demand for latex. Polyisoprene's processability allows for precise molding, reducing manufacturing defects and costs, while its chemical stability supports harsh environmental exposures. These attributes position it as a key enabler for industrial expansion, particularly as manufacturers prioritize sustainable, high-performance alternatives amid supply chain disruptions.

Restraint - Volatility in Petrochemical Raw Material Prices

Fluctuations in crude oil prices pose a significant restraint on the polyisoprene latex market, as the material is derived from petrochemical feedstocks like isoprene monomers. The U.S. Energy Information Administration reported average crude oil prices of USD 94 per barrel in 2022, leading to unpredictable production costs that squeeze manufacturer margins by up to 15-20% in volatile periods.

This instability disrupts supply chains, particularly for small-scale producers reliant on imported monomers, and discourages long-term investments in capacity expansion.

Furthermore, geopolitical tensions in oil-producing regions exacerbate shortages, forcing reliance on costlier alternatives and delaying product launches. As a result, this restraint hampers market predictability, compelling companies to hedge against price swings and potentially passing increased costs to end-users in price-sensitive sectors such as consumer goods.

Environmental and Sustainability Concerns

Growing regulatory scrutiny on synthetic rubber production environmental footprint is restraining the polyisoprene latex market growth. Manufacturing processes emit volatile organic compounds (VOCs) and consume substantial energy, contributing to carbon emissions estimated at 1.5 tons CO2 equivalent per ton of latex produced, based on data from the European Chemicals Agency (ECHA).

This has led to stricter emissions standards under frameworks such as the EU's REACH regulation, increasing compliance costs by 10-15% for producers. Consumer and industry shifts toward bio-based alternatives further pressure traditional polyisoprene, as sustainability certifications become mandatory for exports to eco-conscious markets.

These challenges limit scalability, particularly in regions with aggressive green policies, and risk alienating stakeholders focused on circular economy principles.

Opportunity - Expansion into Emerging Healthcare Markets

Rising healthcare investments in developing economies present a major opportunity for polyisoprene latex providers to capture demand in medical applications. With the World Bank forecasting India's GDP growth at 6.5% in 2023, infrastructure upgrades are projected to add millions of medical facilities, driving the need for affordable, allergy-free PPE like gloves and catheters.

Polyisoprene's hypoallergenic properties align with global standards from the World Health Organization (WHO), enabling penetration into underserved regions where natural latex sensitivities affect treatment efficacy.

Recent developments, such as partnerships between manufacturers and local health ministries, underscore this potential. For example, initiatives in Brazil aim to localize production, reducing import dependencies and creating over 50,000 jobs in related sectors by 2030 per national economic reports. This opportunity not only diversifies revenue streams but also fosters technology transfer, positioning companies for long-term dominance in high-growth areas.

Innovation in Sustainable Formulations

Technological advancements in eco-friendly polyisoprene latex variants offer substantial opportunities for market participants amid global sustainability mandates.

Research from the International Rubber Study Group (IRSG) highlights ongoing R&D into bio-based isoprene from renewable sources, potentially cutting fossil fuel dependency by 30% and meeting demands under policies like the EU Green Deal. This is particularly promising for adhesives and consumer goods segments, where biodegradable formulations could command premium pricing.

Pilot projects in Japan have demonstrated 20% improved recyclability without compromising elasticity. News from industry journals notes collaborations with academic institutions to scale these innovations, targeting a market shift projected to grow 15% annually in green materials.

By investing in such technologies, companies can differentiate offerings, comply with evolving regulations, and tap into consumer preferences for sustainable products, ensuring competitive advantages in both established and emerging applications.

Category-wise Insights

Application Analysis

In the application category, gloves emerge as the leading segment, commanding approximately 45% market share due to their critical role in infection control and surgical procedures. Polyisoprene latex's superior elasticity and powder-free formulation reduce slippage and enhance grip, making it preferable over natural latex, which causes allergic reactions in up to 12% of users as reported by the Centers for Disease Control and Prevention (CDC).

This dominance is justified by heightened PPE demand post-2020, with global glove consumption surging over 300% during peak pandemic periods according to WHO data. The segment's growth is further supported by innovations in thin-walled dipping technologies, improving dexterity for healthcare professionals while maintaining barrier integrity, solidifying gloves' position in medical and industrial hygiene applications.

End-use Analysis

Within the end-use category, the medical segment leads with around 60% share, driven by polyisoprene latex's biocompatibility and compliance with rigorous standards such as USP <381> for elastomeric closures. Its use in devices such as catheters and balloons benefits from low cytotoxicity and high resealability, as evidenced by testing from the U.S. Pharmacopeia, which confirms reduced risk of contamination in injectable applications.

This is underpinned by expanding healthcare access, with the World Health Organization estimating a need for 18 million additional health workers globally by 2030 to meet demand. The segment's resilience stems from ongoing R&D in medical-grade formulations, ensuring purity levels below 1 ppm for extractables, which supports its dominance amid rising chronic disease prevalence and procedural volumes.

Regional Insights

North America Polyisoprene Latex Trends

North America maintains leadership in the polyisoprene latex market, propelled by robust healthcare infrastructure and stringent regulatory frameworks from the FDA and NIOSH.

The U.S., accounting for most of the regional activity, sees high adoption in medical gloves and catheters, with domestic R&D investments exceeding USD 500 million annually in biocompatible materials as per National Institutes of Health (NIH) reports. Innovation ecosystems in hubs like Boston and Silicon Valley focus on advanced polymerization for allergy-free products, aligning with post-pandemic hygiene standards.

This regional strength is further evidenced by vehicle production growth, incorporating polyisoprene in seals. The U.S. automotive output reached 10 million units in 2024 according to the Alliance for Automotive Innovation, driving industrial demand. Regulatory emphasis on sustainability, including EPA guidelines for low-VOC emissions, encourages eco-innovations, positioning North America as a trendsetter for high-purity latex applications.

Europe Polyisoprene Latex Trends

Europe's polyisoprene latex market is characterized by harmonized regulations under REACH and EU Medical Device Regulation (MDR), fostering quality-driven growth in countries like Germany, the U.K., France, and Spain. Germany leads with sophisticated manufacturing in regions like Bavaria, where polyisoprene supports precision medical devices.

Its chemical sector invested EUR 2.5 billion in sustainable rubbers in 2024, per German Chemical Industry Association (VCI) data. The U.K. benefits from NHS procurement emphasizing hypoallergenic PPE, while France advances in catheter technologies through public-private partnerships.

Performance analysis reveals steady expansion, with Europe's healthcare expenditure at 10% of GDP as reported by the European Commission, bolstering demand. Regulatory alignment promotes cross-border trade, enabling innovations like bio-compatible formulations that meet ISO 10993 standards, enhancing market resilience amid economic recoveries.

Asia Pacific Polyisoprene Latex Trends

Asia Pacific exhibits dynamic growth in polyisoprene latex, driven by manufacturing advantages and rising demand in China, Japan, India, and ASEAN nations. China dominates production, with facilities leveraging low-cost feedstocks.

Its chemical output grew 7.2% in 2024, per the National Bureau of Statistics of China, supporting exports of medical gloves. India accelerates via healthcare initiatives like Ayushman Bharat, targeting 500 million beneficiaries by 2025 as per government reports, spurring local latex adoption.

Japan excels in high-tech applications, with R&D from firms like Kuraray focusing on EV components. ASEAN's industrialization adds momentum, with Vietnam and Indonesia seeing 15% annual infrastructure growth according to the Asian Development Bank (ADB). These dynamics underscore cost efficiencies and supply chain integrations, positioning the region for sustained expansion in both medical and industrial uses.

Competitive Landscape

The polyisoprene latex market exhibits a moderately consolidated structure through vertical integration and R&D investments. Key strategies include capacity expansions in Asia to counter raw material volatility, alongside partnerships for sustainable innovations like bio-based monomers.

Market leaders differentiate via proprietary formulations offering superior purity for medical uses, while emerging models emphasize circular supply chains and digital tracking for traceability. This concentration fosters competition in high-value segments, with smaller players focusing on niche customizations.

Key Market Developments

- May 2025: Cariflex inaugurates the world's largest polyisoprene latex plant in Singapore with US$355 million investment, boosting global capacity for medical applications.

- November 2024: DL Chemical completes major polyisoprene latex facility on Jurong Island, enhancing supply for healthcare and enhancing regional manufacturing.

- April 2025: Kraton Corporation announces R&D collaboration for eco-friendly polyisoprene variants, targeting reduced emissions in latex production.

Top Companies in Polyisoprene Latex

- KURARAY CO., LTD. (Japan) leads through its advanced synthetic rubber portfolio, generating significant revenue from medical-grade latex; its focus on high-purity innovations and global facilities ensures strong influence and maturity in healthcare segments.

- JSR Corporation (Japan) excels in diversified applications, with robust R&D driving adhesives and gloves; headquartered in Tokyo, it leverages portfolio strength for steady market expansion and technological leadership.

- Exxon Mobil Corporation (USA) dominates via integrated petrochemical operations, supplying isoprene monomers; its scale and influence support consistent revenue growth, emphasizing industrial and consumer uses.

Companies Covered in Polyisoprene Latex Market

- Cariflex Pte Ltd

- Daelim Co., Ltd.

- Kuraray Co., Ltd.

- JSR Corporation

- PJSC SIBUR Holding

- Zeon Corporation

- Eni S.p.A

- Exxon Mobil Corporation

- Fushun Yikesi New Materials Co., Ltd

- Synthomer plc

- Kraton Corporation

- Top Glove Corporation Bhd

- Kent Elastomers

- Precision Dippings

Frequently Asked Questions

The global polyisoprene latex market is expected to reach US$ 506.9 Mn by 2032, reflecting steady growth from healthcare and industrial demands.

Surging healthcare needs for hypoallergenic PPE, like gloves, drive demand, supported by 2.4 million projected U.S. jobs in the sector by 2030.

Gloves lead with 45% share, due to their essential role in medical infection control and biocompatibility advantages.

North America dominates, leveraging U.S. R&D investments and EV sector demands for resilient components.

Developing sustainable bio-based formulations offers significant potential, aligning with EU Green Deal policies for eco-friendly applications.

Leading players include Kuraray Co., Ltd., JSR Corporation, and Exxon Mobil Corporation, known for innovation and capacity in medical-grade latex.