- Pharmaceuticals

- Phenylketonuria Treatment Market

Phenylketonuria Treatment Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Phenylketonuria Treatment Market by Drug Type (Kuvan, Palynziq), Route of Administration (Oral, Parenteral), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Online), Regional Analysis, from 2025 - 2032

Phenylketonuria Treatment Market Share and Trends Analysis

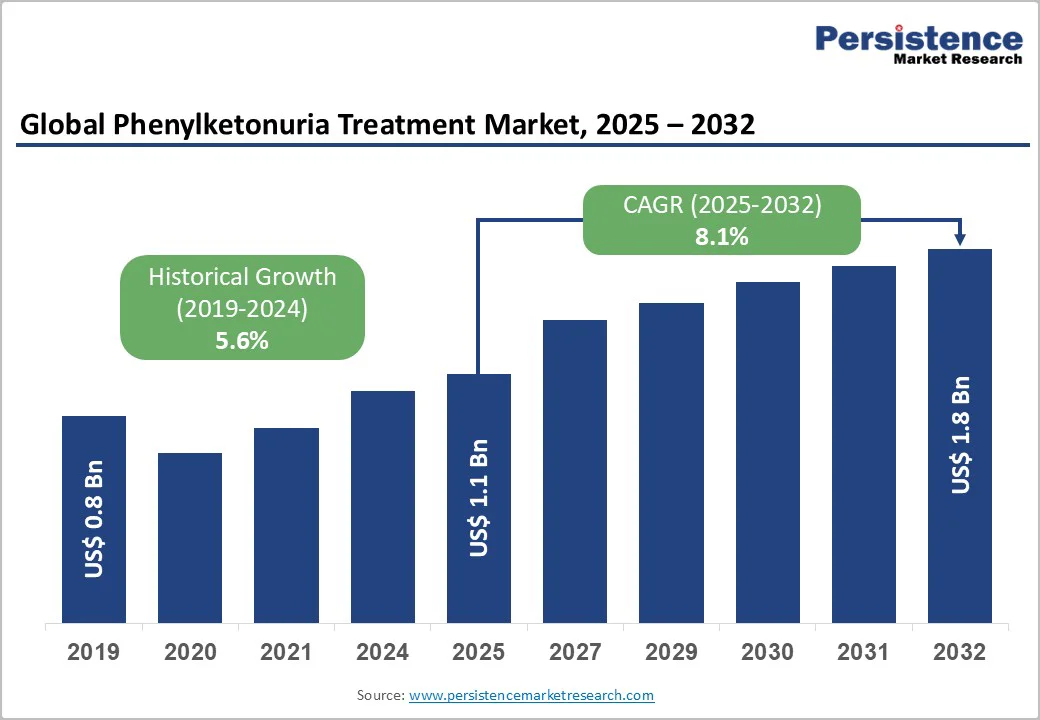

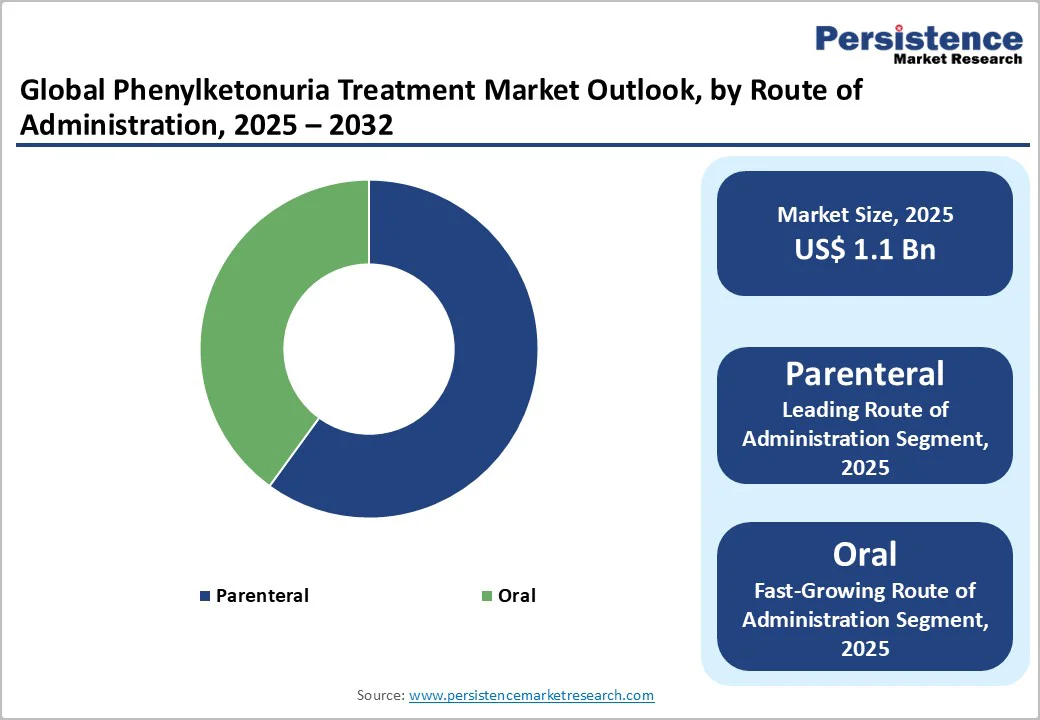

The global phenylketonuria treatment market is valued at US$1.1 billion in 2025 and is projected to reach US$1.8 billion, growing at a CAGR of 8.1% from 2025 to 2032. Phenylketonuria (PKU) Treatment, a rare metabolic disorder resulting in the inability of the human body to break down the amino acid phenylalanine, causes severe brain damage and other neurological problems.

The treatment is critical, primarily driving the demand in the global market for PKU treatment. The PKU treatment market is projected to grow at a strong rate during the forecast period, driven by the growing prevalence of PKU and the need for awareness campaigns within the healthcare industry and among patients.

Key Industry Highlights

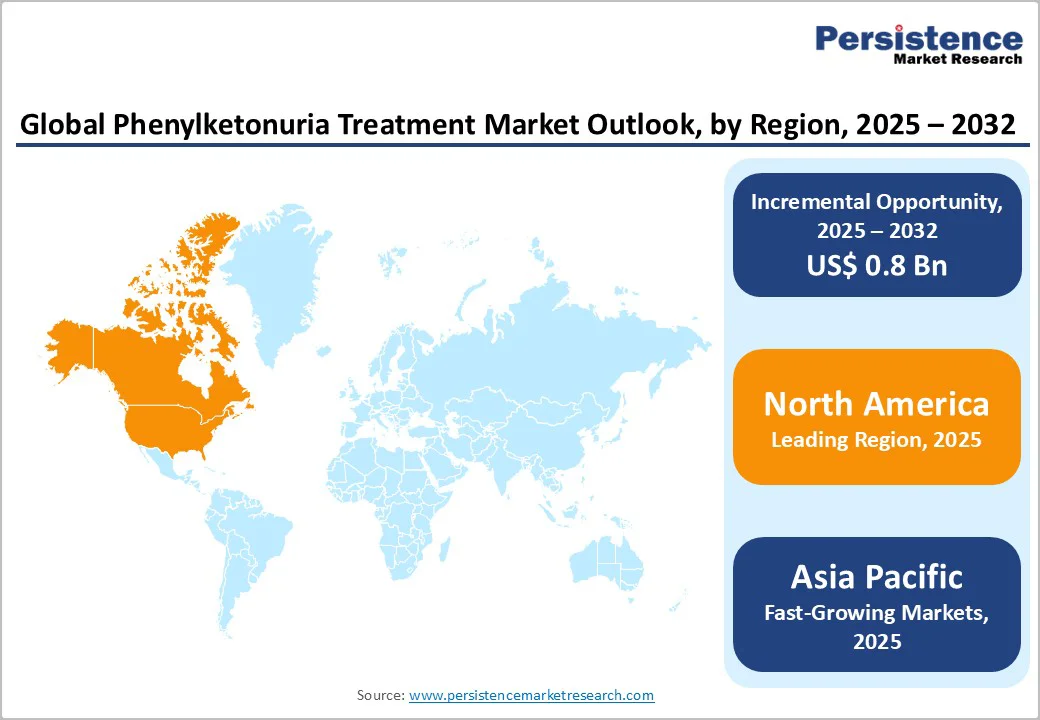

- Leading Region: North America holds a 38.3% share of the global phenylketonuria treatment market, driven by robust healthcare infrastructure and regulatory support.

- Fastest Growing Region: Asia Pacific is the fastest growing region due to expanding screening programs and increasing healthcare access in emerging economies.

- Dominant Segment: Palynziq dominates the drug type category with around 60% market share, owing to its superior clinical efficacy and patient compliance.

| Key Insights | Details |

|---|---|

|

Phenylketonuria Treatment Market Size (2025E) |

US$1.1 Bn |

|

Market Value Forecast (2032F) |

US$1.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.6% |

Market Dynamics

Driver - Increasing Prevalence of Phenylketonuria

The increasing prevalence of phenylketonuria (PKU) is a significant driver of the phenylketonuria treatment market. PKU is a rare genetic disorder characterized by the body's inability to metabolize the amino acid phenylalanine, leading to its accumulation, which can cause severe intellectual disability and other complications if untreated. The estimated incidence of PKU varies globally but is reported to be about 1 in 15,000 live births in the United States, with higher rates in certain populations like Caucasians and Native Americans. Newborn screening programs have become more widespread, leading to more diagnoses and earlier treatment initiation. This heightened detection is increasing the number of patients seeking effective treatment options.

As a result, demand for advancements in treatment, including enzyme substitution therapies such as Kuvan and Palynziq, is expected to grow rapidly. The need to manage blood phenylalanine levels effectively to prevent cognitive impairments reinforces the importance of these treatments. Moreover, rising awareness among healthcare providers and patients about the long-term benefits of sustained treatment adherence further accelerates market expansion. Altogether, the growing patient pool, driven by rising PKU prevalence and improved diagnosis, is fueling demand for efficient, innovative therapies, positioning this as a prominent market growth factor for the forecast period.

Restraints - High-Cost of Treatment

The only major restraining factor for the phenylketonuria treatment market is the high cost of treatment, making it difficult for patients to afford it. Expensive diet plans, including medical foods and supplements, can increase the overall cost of PKU treatment, making treatment more costly for patients. Further, many insurance companies do not cover the total cost of PKU treatment, which is another factor that will hinder the phenylketonuria market size over the forecast period.

Patients diagnosed with PKU have fewer treatment alternatives, and many of these treatments do not react well to the current therapies. The phenylketonuria treatment market confronts several difficulties, such as low diagnosis and awareness, expensive therapy, few treatment options, problems with compliance, and social stigma and isolation. To overcome these obstacles, cooperation between patients, medical professionals, researchers, and legislators will be necessary to enhance diagnosis, create more accessible and efficient therapies, and offer patient and family resources. Another major challenge for the growth of the market is the lack of awareness and the prevalence of underdiagnosis, as several patients are completely unaware of the disorder and are left undiagnosed, leading to poor health conditions and delayed treatment.

Opportunity - Robust R&D Activity

Ongoing research and development activities to create efficient medications, treatments, and early diagnosis methods develop a pool of opportunities for the market. Due to the lack of awareness and high costs incurred, several patients are unable to receive treatment for the disorder, and many patients are undiagnosed for PKU, which creates a wide range of opportunities for the key market players. With the continuous R&D activities for the diagnosis and treatment methods for PKU disorder, it will be easier for patients to get an early diagnosis of their disorder and get the necessary treatment as early as possible.

Category-wise Analysis

By Distribution Channel Insights

Based on the distribution channels, the market is further sub-segmented into hospital, retail, and online, where the hospital sub-segment dominates the market share. Hospitals and specialty clinics that offer expert care, diagnostic resources, and treatment to patients with PKU are the initial point of contact for patients.

Additionally, patients with complex or severe instances of PKU might receive complete care from these clinics due to their experience and resources. Furthermore, a lot of phenylketonuria therapies need to be administered or monitored by specialists, like intravitreal injections or electroretinography tests, which are usually carried out in hospitals or specialty clinics. Due to the specialized treatment and knowledge offered by hospitals and specialty clinics, these are expected to dominate the market share over the forecast period.

By Parenteral Administration Insights

Based on the route of administration segment, the PKU treatment market is further divided into parenteral and oral routes, with the parenteral route holding the largest market share. The parenteral route of administration is more effective than the oral route, as it delivers medication more quickly and precisely by injecting it directly into the bloodstream or the affected area. Owing to this advantage, the parenteral route of administration, or injectable method, is estimated to hold a substantial market share in the global phenylketonuria treatment market.

Furthermore, when oral medications may not be appropriate, such as for patients who have trouble swallowing or who need larger doses than may be possible with oral medicines, parenteral treatments are also recommended. The parenteral segment is partly dominated by the presence of several well-established parenteral therapies for PKU treatment.

Region-wise Analysis

North America Phenylketonuria Treatment Market Insights

North America dominates the global market share for the market owing to the high level of awareness and understanding of the PKU disorder among US healthcare providers and residents. As a result, there has been an increase in diagnoses and improved treatment and management of PKU, which have contributed to overall patient outcomes and led the North American region to earn a substantial market share in the global PKU treatment market.

Furthermore, the presence of well-established and high-end healthcare facilities in the US, Canada, and other parts helps the region to boost the market’s growth and create a favorable environment for the growth and development of the commercialization of crucial healthcare and diagnosis products or medical electronic devices, which eventually aids the North American region to dominate the global market share.

Asia and Pacific Phenylketonuria Treatment Market Trends

The Asia Pacific region is experiencing rapid market growth, supported by expanding healthcare access and rising PKU diagnosis rates in populous countries such as China, Japan, and India. Improvements in newborn screening infrastructure and government initiatives targeting metabolic disorders are key growth drivers. The manufacturing base in Asia also offers cost advantages and facilitates local production of PKU drugs, increasing affordability.

Emerging economies in ASEAN and South Asia are increasingly incorporating PKU treatment into national health agendas, with expanding reimbursement schemes and public-private partnerships. The rising middle class and increasing healthcare expenditure further stimulate demand. Digital health penetration and telemedicine services are expanding patient reach and facilitating distribution beyond traditional healthcare settings.

Competitive Landscape

The phenylketonuria (PKU) treatment market is highly competitive, driven by continuous advancements in enzyme substitution therapies, gene therapy research, and dietary management solutions. Key players such as BioMarin Pharmaceutical, PTC Therapeutics, Synlogic, and Ultragenyx are focusing on expanding product indications and developing next-generation treatments. Strategic collaborations, clinical trials, and FDA approvals are shaping the market’s growth trajectory. Companies are also emphasizing patient-centric solutions, including medical foods and digital monitoring platforms, to enhance treatment adherence and outcomes. Growing R&D investment and strong regulatory support further strengthen the competitive landscape for PKU treatment worldwide.

Key Industry Developments:

- In October 2025, the U.S. FDA accepted BioMarin’s supplemental Biologics License Application (sBLA) for PALYNZIQ® (pegvaliase-pqpz) for priority review, seeking to extend its approved use to adolescents aged 12–17 years with phenylketonuria.

- In August 2024, Otsuka Holdings Co., Ltd. announced its agreement to acquire Jnana Therapeutics Inc., a biotechnology firm developing investigational therapies for phenylketonuria (PKU), in a transaction valued at up to USD 800 million.

Companies Covered in Phenylketonuria Treatment Market

- BioMarin Pharmaceutical Inc.

- Censa Pharmaceuticals (PTC Therapeutics)

- Synlogic, Inc.

- SOM Innovation Biotech S.A

- Homology Medicines, Inc.

- Codexis, Inc.

- American Gene Technologies International Inc.

- Nestlé Health Science

- Travere Therapeutics, Inc.

- DAIICHI SANKYO COMPANY, LIMITED.

- Others

Frequently Asked Questions

The global phenylketonuria treatment market is projected to be valued at US$ 1.1 Bn in 2025.

Growth is driven by increased prevalence, advancements in treatment options including enzyme substitution therapies, and supportive orphan drug policies.

The global market is poised to witness a CAGR of 8.1% between 2025 and 2032.

Gene therapy and expanding newborn screening programs are significant opportunities expected to drive future market growth.

Companies such as BioMarin Pharmaceutical Inc., Censa Pharmaceuticals (PTC Therapeutics), Synlogic, Inc., and SOM Innovation Biotech S.A. are some of the major players operating in the market.