- Pharmaceuticals

- Overweight Treatment Market

Overweight Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Overweight Treatment Market by Treatment (Drug Treatment, Supplements, Others), Distribution Channel (Institutional Sales, Retail Sales, Online Sales), and Regional Analysis from 2026 to 2033.

Overweight Treatment Market Size and Trends Analysis

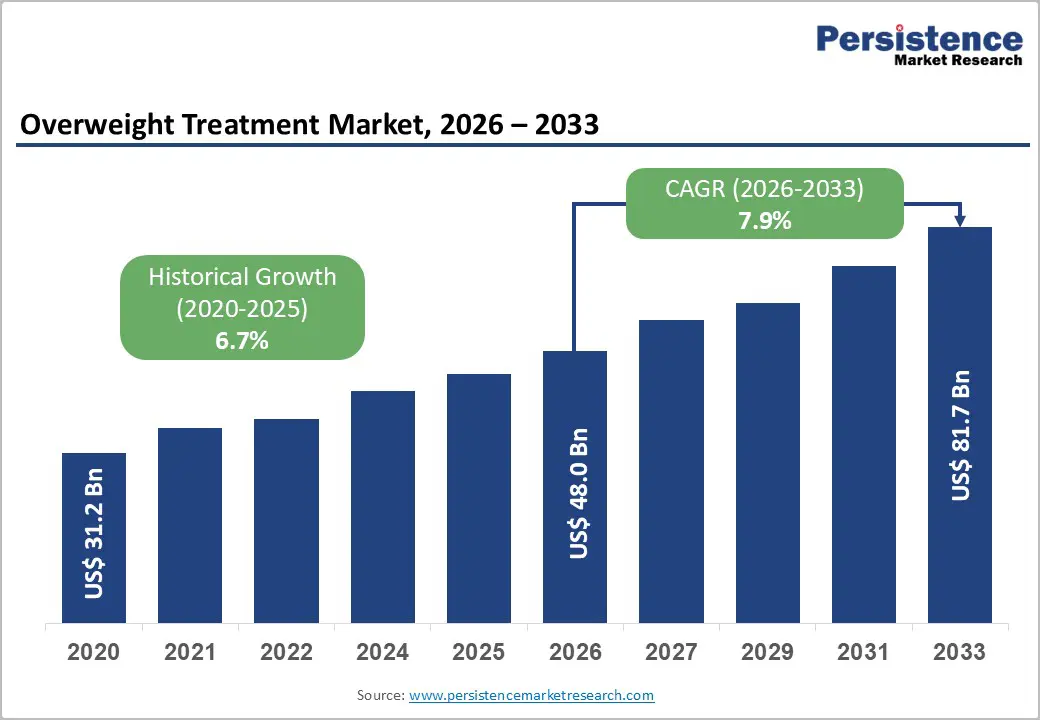

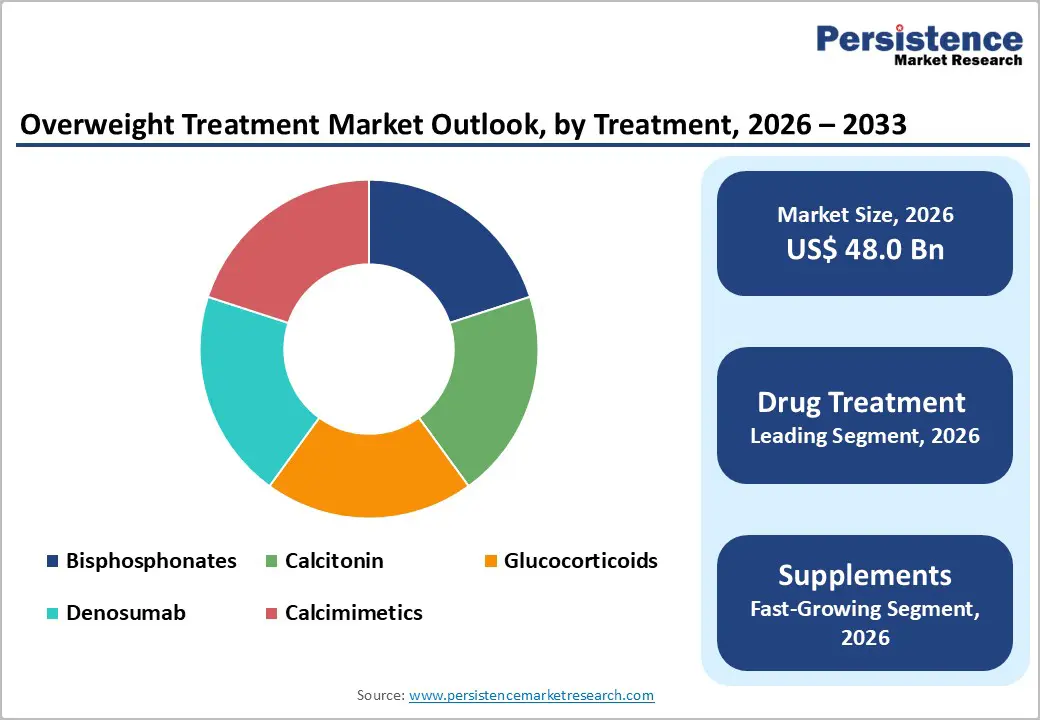

The global overweight treatment market is estimated to grow from US$ 48.0 Bn in 2026 to US$ 81.7 Bn by 2033. The market is projected to record a CAGR of 7.9% during the forecast period from 2026 to 2033.

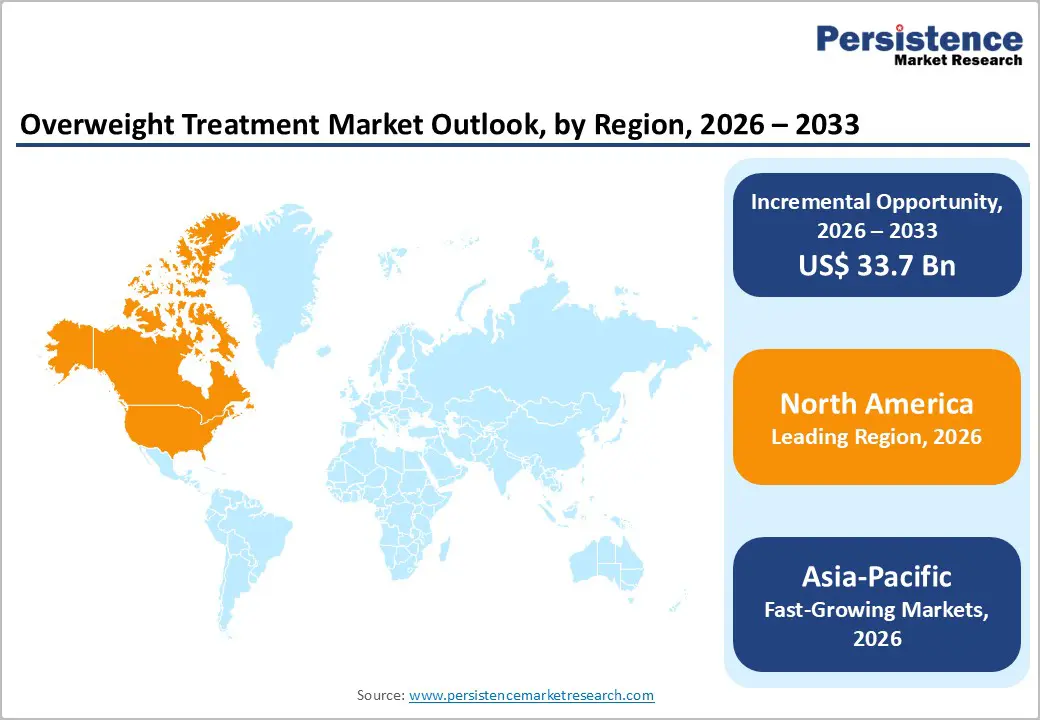

The global overweight treatment market is expanding steadily, driven by rising obesity prevalence, increasing awareness of lifestyle-related disorders, and strong demand for effective weight management therapies. North America leads due to high treatment adoption and favorable reimbursement, while Asia-Pacific is growing rapidly with improving healthcare access, urbanization, and rising disposable incomes.

Key Industry Highlights

- Dominant Segment: Drug treatment accounts for 59.7% share of the overweight treatment market in 2025, driven by strong clinical efficacy of GLP-1 receptor agonists and combination therapies, increasing physician prescriptions, proven weight-loss outcomes, and expanding regulatory approvals across major markets.

- Dominant Region: North America leads the overweight treatment market with 44.2% share in 2025, supported by high obesity prevalence, favorable reimbursement frameworks, strong pharmaceutical adoption, and advanced healthcare infrastructure. Asia-Pacific is the fastest-growing region, driven by urbanization, rising obesity rates, improving healthcare access, and increasing awareness of weight management therapies.

- Market Drivers: Rising global obesity prevalence, increasing awareness of lifestyle-related disorders, growing demand for non-invasive weight management solutions, expanding pharmacological innovations, supportive regulatory approvals, and higher healthcare spending are key factors driving market growth.

- Market Opportunity: Key opportunities include development of next-generation anti-obesity drugs, oral formulations, personalized weight management programs, digital health integration, expansion of minimally invasive bariatric devices, and increased penetration across emerging markets with improving healthcare infrastructure.

| Key Insights | Details |

|---|---|

| Global Overweight Treatment Market Size (2026E) | US$ 48.0 Bn |

| Market Value Forecast (2033F) | US$ 81.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.7% |

Market Dynamics

Driver: Growing Awareness of Lifestyle-Related Metabolic Disorders

One of the primary drivers of the Overweight Treatment Market is the growing awareness of lifestyle-related metabolic disorders and their links to overweight and obesity. Governments and health agencies have documented a steep rise in these conditions. In the United States, CDC data show that about 42% of adults are obese, with obesity strongly associated with metabolic disorders such as type 2 diabetes, hypertension, and dyslipidemia conditions that collectively comprise metabolic syndrome and significantly increase cardiovascular risk. This awareness has risen due to public health campaigns and large epidemiological studies highlighting the morbidity and mortality associated with obesity-related metabolic dysfunction. As clinicians and populations recognize that overweight is not merely cosmetic but a gateway to chronic disease, demand for structured medical interventions grows.

Moreover, overweight and obesity dramatically elevate the odds of metabolic syndrome. A CDC-supported meta-analysis found that obese adults have about 5 times higher odds of having metabolic syndrome compared with normal-weight adults. This stark association motivates public health systems to emphasize early intervention, contributing to expanded clinical screening, guideline updates recommending therapy, and more proactive referral to pharmacological or lifestyle management strategies. In turn, this drives demand for prescription weight-loss drugs, hormone-modulating therapies, and integrated care programs covered under healthcare policies, thereby fueling market growth.

Restraints: Safety Concerns and Long-Term Side Effect Risks

A significant restraint in the overweight treatment market stems from ongoing safety concerns and uncertainties around long-term side effects of pharmacological treatments. While newer classes of weight-loss drugs such as GLP-1 receptor agonists have shown remarkable efficacy, regulatory and scientific sources have highlighted side effect profiles that complicate widespread prescribing. For example, numerous reports and regulatory notices have pointed to gastrointestinal issues (nausea, vomiting, diarrhea) as common adverse events in GLP-1 therapy trials. In addition, rare but serious events such as acute pancreatitis and optic nerve issues have been flagged by health authorities, prompting vigilance and heightened patient monitoring. These safety signals temper clinician enthusiasm and can slow guideline adoption or reimbursement approvals in certain regions.

Long-term safety data for many anti-obesity medications remain incomplete, particularly because many therapies are relatively new to widespread clinical use. Peer-reviewed analyses observe that while weight-loss drugs improve metabolic outcomes and cardiometabolic markers, there is ongoing evaluation of their impact on psychological outcomes and long-term physiological effects. Concern about potential rare but serious effects such as those implied in post-marketing surveillance or regulatory warnings can create hesitation among prescribers and patients alike, particularly when drugs are used outside tightly controlled trials. Such restraint limits broader market uptake, especially in populations with complex comorbidities or in healthcare systems prioritizing long-term safety evidence.

Opportunity: Development of Next-Generation Oral and Long-Acting Therapies

A major opportunity in the overweight treatment market lies in the development of next-generation oral and long-acting therapies that improve convenience, adherence, and overall patient outcomes. Traditional injectable therapies while effective face barriers related to administration route, frequency, and patient preference, especially in populations with needle aversion. The recent approval by the U.S. FDA of a daily oral obesity drug (oral semaglutide) represents a pivotal advance, showing comparable weight loss efficacy (~13.6% body weight reduction over 15 months) to injectables but in pill form. This development broadens therapy accessibility and could significantly increase adoption among individuals unwilling or unable to use injections.

Beyond semaglutide, clinical pipelines include novel oral agents such as orforglipron in Phase III trials and multi-receptor agonists like retatrutide that produce substantial weight reductions (15–24% in trials) with manageable side effect profiles. The movement toward oral, long-acting, and combined mechanism therapies addresses key unmet needs in adherence and long-term weight management. If these next-generation drugs demonstrate durability, safety, and broader real-world effectiveness, they will expand the market by attracting patients and healthcare providers seeking more versatile treatment options. This innovation also drives competitive differentiation among pharmaceutical companies and attracts investment in research, offering substantial growth potential for the market at large.

Category-wise Analysis

By Treatment, Drug Treatment Dominates the Overweight Treatment Market

Drug Treatment occupies 59.7% share of the global market in 2025, because pharmaceutical therapies offer clinically validated efficacy and are widely integrated into medical practice for obesity and related metabolic disorders. According to the U.S. Centers for Disease Control and Prevention (CDC), obesity affects about 42% of U.S. adults, with overweight and obesity strongly linked to type 2 diabetes, hypertension, and cardiovascular disease, conditions where medical intervention is standard. Prescription drugs such as GLP-1 receptor agonists not only produce significant weight loss but also improve glycemic control, which reinforces physician prescribing behavior. Peer-reviewed evidence shows that newer pharmacotherapies can reduce body weight by approximately 10–15% or more in controlled trials, far exceeding typical outcomes from diet alone. Because of this strong clinical evidence and guideline recommendations, drug treatment accounts for the majority of spending and adoption in the market.

By Distribution Channel, Institutional Sales dominates due to physician-supervised prescription therapies

Institutional sales dominate the distribution of overweight treatments because most high-efficacy therapies require healthcare provider involvement and are dispensed through clinical settings. In the United States, medicines with significant clinical risk profiles, including GLP-1 receptor agonists and other prescription obesity treatments must be prescribed and monitored by physicians, and dispensed through hospital or clinic pharmacies. Data from the CDC indicate that medical visits for obesity management and comorbid conditions occur most frequently in clinical settings. Additionally, many weight-loss drugs require initial screening and ongoing monitoring (e.g., for cardiovascular effects or glucose metabolism), reinforcing institutional channels. Institutional sales also include hospital formularies and outpatient clinics, where insurance reimbursement policies are structured. This health system integration elevates institutional sales over retail or online channels for prescription-based overweight treatments.

Regional Insights

North America Overweight Treatment Market Trends

North America leads the overweight treatment market due to the exceptionally high prevalence of overweight and obesity. WHO data indicate that in the Region of the Americas, 67.5% of adults were overweight or obese in 2022, the highest among all global regions. Within the United States, CDC statistics show state-level adult obesity rates reaching 35–40% or higher, with some regions exceeding 40%. Such elevated prevalence drives strong clinical demand for medical management, including prescription weight-loss therapies. Structural factors further reinforce this dominance: North America has well-established healthcare infrastructure, extensive clinical screening programs for metabolic and cardiovascular comorbidities, and comparatively broad reimbursement frameworks that support novel pharmacological interventions. These epidemiologic and system characteristics combine to create both high utilization and spending on overweight treatments, making North America the largest regional market globally.

Europe Overweight Treatment Market Trends

Europe is a significant region in the overweight treatment market due to its substantial overweight and obesity burden and robust public health response. WHO estimates indicate that almost 60% of adults in the European Region live with overweight or obesity, and these conditions contribute to over 1.2 million deaths annually through associated noncommunicable diseases (NCDs). High prevalence among both adults and children drives clinical demand for weight management therapies, including drugs, lifestyle interventions, and integrated care programs. Europe’s developed healthcare systems, with widespread preventive screening and structured chronic disease management, support early diagnosis and treatment adoption. Additionally, strong public health initiatives and regulatory frameworks aim to curb metabolic disorders, incentivizing both provider and patient engagement. These epidemiologic and healthcare dynamics make Europe a strategically important and high-value region within the global market.

Asia-Pacific Overweight Treatment Market Trends

Asia-Pacific is the fastest-growing region in the overweight treatment market because overweight and obesity are rising rapidly alongside urbanization and economic development. OECD/WHO data show that in Asia-Pacific, overweight prevalence among adults has increased substantially across both low- and middle-income countries, with notable rises over the past decade. High and upper-middle-income Asia-Pacific countries report adult overweight rates nearing 49%, with obesity exceeding 30% in several areas. Moreover, lower-income Asia-Pacific nations have seen sharp growth for example, obesity among adults more than doubled in some countries between 2010 and 2022. Expanding healthcare infrastructure, increasing access to diagnostics, rising disposable incomes, and growing health awareness are further accelerating treatment uptake. These epidemiologic shifts and improving healthcare capacity position Asia-Pacific as the fastest-expanding regional market for overweight treatment solutions.

Market Competitive Landscape

The overweight treatment market is led by major pharmaceutical companies offering advanced anti-obesity drugs and supportive therapies. Competition centers on clinical efficacy, safety profiles, regulatory approvals, and physician adoption. Companies emphasize pipeline innovation, next-generation oral formulations, combination therapies, and strategic partnerships to expand global reach and strengthen institutional presence.

Key Industry Developments:

- In February 2026, VIVUS announced the advancement of patient access to PANCREAZE® through the launch of a new copay assistance program. The initiative was introduced to help reduce out-of-pocket costs for eligible patients prescribed PANCREAZE®, a pancreatic enzyme replacement therapy used to treat exocrine pancreatic insufficiency.

- In November 2025, Currax Pharmaceuticals announced data presented at ObesityWeek® demonstrating that CONTRAVE® (naltrexone HCl/bupropion HCl) helped reduce food cravings and delivered meaningful weight-loss outcomes in specific populations with obesity. The findings highlighted the therapy’s impact on appetite regulation and behavioral drivers of weight gain.

- In March 2025, VIVUS announced the introduction of Qsymia in the United Arab Emirates for the treatment of overweight and obesity in adults and pediatric patients aged 12 years and older. Qsymia, a prescription weight-management medication combining phentermine and topiramate extended-release, was launched to address the growing burden of obesity in the region.

Companies Covered in Overweight Treatment Market

- Novo Nordisk A/S

- VIVUS LLC

- AstraZeneca

- Currax Pharmaceuticals LLC

- Spansules Pharmatech Pvt Ltd

- Atkins Nutritional Inc

- Apollo Endosurgery, Inc

- Herbalife Nutrition Ltd.

- SMP Nutra

- Allurion Technologies

- ReShape Lifesciences, Inc

- Bariatric Solutions GmbH

- Silimed

- ENDALIS

- Districlass Medical

- Medtronic

- Others

Frequently Asked Questions

The global overweight treatment market is projected to be valued at US$ 48.0 Bn in 2026.

Rising obesity prevalence, metabolic disorders, drug innovation, awareness, and expanding healthcare access globally.

The global overweight treatment market is poised to witness a CAGR of 7.9% between 2026 and 2033.

Next-generation oral drugs, digital health integration, emerging markets, and personalized weight management therapies.

Novo Nordisk A/S, VIVUS LLC, AstraZeneca, Currax Pharmaceuticals LLC, Spansules Pharmatech Pvt Ltd, Atkins Nutritional Inc.