- Specialty & Fine Chemicals

- Opacifying Ingredient Market

Opacifying Ingredient Market Size, Share, and Growth Forecast, 2026 - 2033

Opacifying Ingredient Market by Product Type (Titanium Dioxide, Opaque Polymers, Others), Formulation Type (Solid/Powder, Liquid/Slurry), Application (Paints & Coatings, Personal Care, Others), and Regional Analysis 2026 - 2033

Opacifying Ingredient Market Size and Trends Analysis

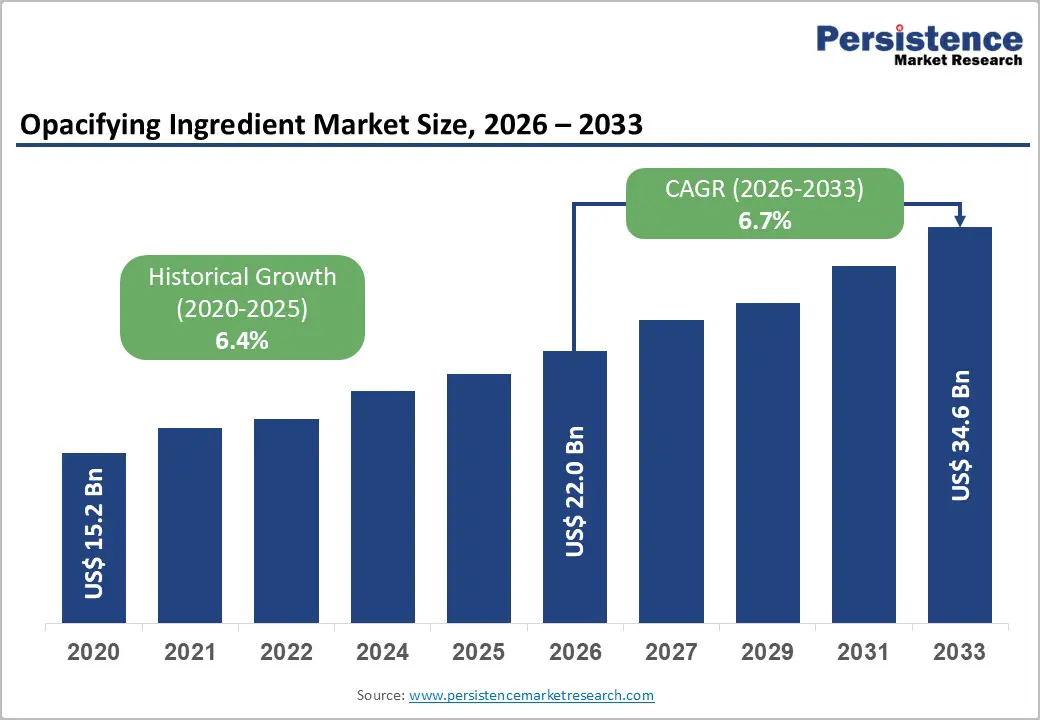

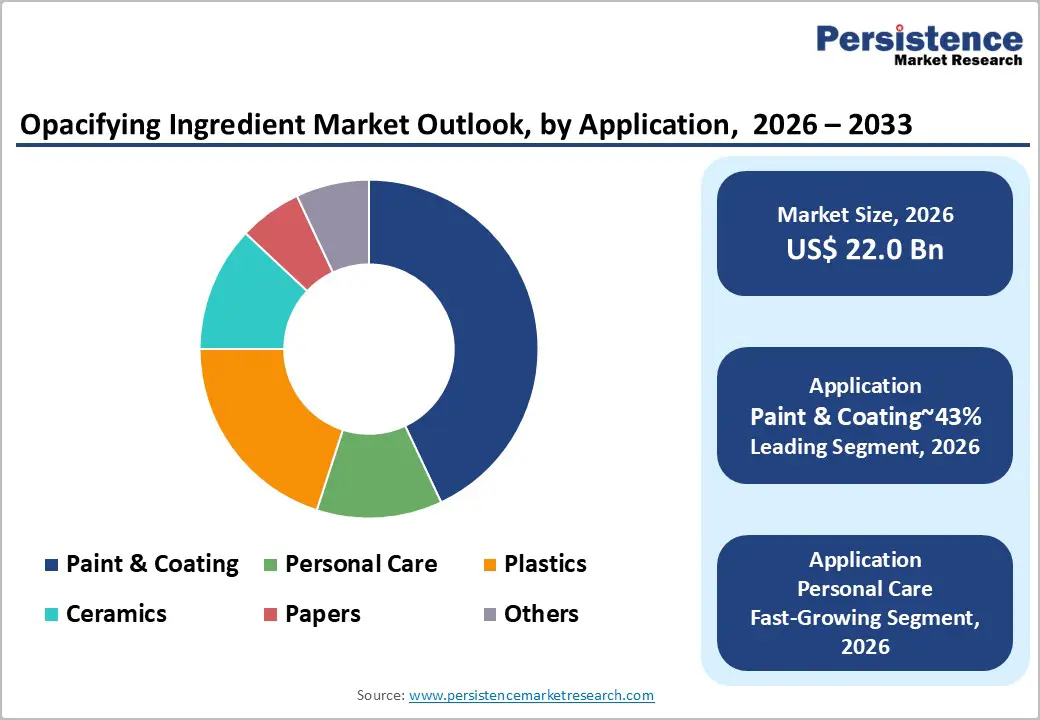

The global opacifying ingredient market size is likely to be valued at US$22.0 billion in 2026 and is expected to reach US$34.6 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033, driven by the escalating demand for high-performance architectural coatings and the premiumization of personal care products requiring superior sensory attributes.

Titanium Dioxide (TiO2) dominates opacity due to its high refractive index, but the market is shifting towards zircon and opaque polymers to address raw material volatility and meet sustainability standards. Regulatory changes drive innovation in eco-friendly opacifiers, while demand in plastics and personal care accelerates the adoption of high-performance materials.

Key Industry Highlights:

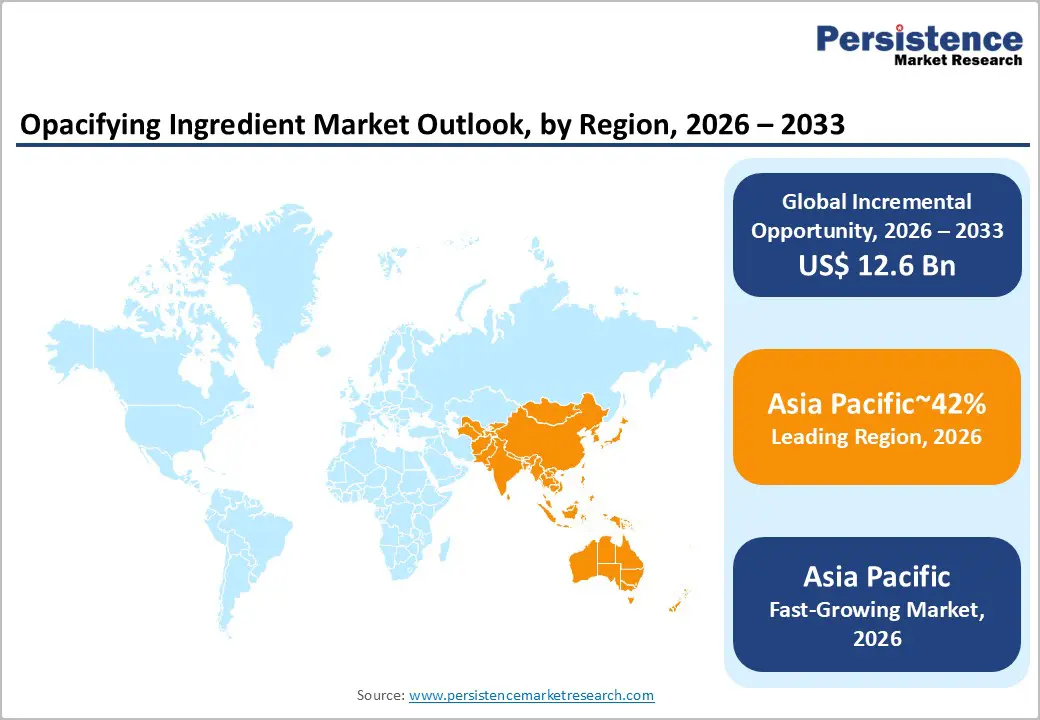

- Leading Region: Asia Pacific with 42% share, underpinned by large-scale manufacturing, construction activity, and downstream coatings and plastics demand.

- Fastest Growing Region: Asia Pacific, led by India and ASEAN, driven by industrialization, urbanization, and expanding consumer goods production.

- Leading Product Type: Titanium dioxide, to lead with 63% share, supported by its superior refractive index and entrenched use as the primary opacifier across coatings, plastics, and paper.

- Leading Application: Paints & coatings to dominate with 43% share, reflecting sustained demand from construction, infrastructure maintenance, and industrial coatings.

| Key Insights | Details |

|---|---|

|

Opacifying Ingredient Market Size (2026E) |

US$22.0 Bn |

|

Market Value Forecast (2033F) |

US$34.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Technological Advancements in Material Science

Advances in material science are structurally reshaping the opacifying ingredient value chain through the development of nano-engineered opacifiers with higher surface-area efficiency and improved dispersion stability across aqueous and solvent-based formulations. Enhanced particle engineering reduces material intensity per unit of opacity delivered, lowering formulation loadings while maintaining optical performance thresholds required in coatings, polymers, ceramics, and paper applications. As formulation chemistries become more complex and regulatory pressure on emissions and material safety intensifies, demand shifts toward engineered opacifiers that can integrate seamlessly into multi-component systems without compromising rheology, durability, or process stability.

From a cost-structure perspective, improved dispersion efficiency alters margin dynamics by compressing raw material consumption per finished unit while elevating the performance ceiling of premium formulations. This enables downstream manufacturers to justify higher-value positioning for advanced coatings and polymer systems, reinforcing differentiation in applications that require enhanced whiteness, hiding power, and long-term stability. Concurrently, intellectual property accumulation around particle morphology and surface treatment technologies raises technical barriers to entry, consolidating competitive advantage around formulation know-how and process integration capabilities rather than scale manufacturing alone.

Premiumization of Personal Care and Cosmetic Formulations

Premiumization dynamics within personal care and cosmetics are structurally elevating demand for opacifying ingredients as visual aesthetics and sensory cues become central to perceived product efficacy and brand differentiation. Formulators increasingly deploy opacifiers to engineer creamy, pearlized, and opaque textures that signal richness and performance across hair care, skin care, and cleansing formats. This shifts opacity from a secondary visual attribute to a core functional parameter within product design, expanding the role of opacifiers in formulation architectures. As product portfolios migrate toward higher sensory complexity and layered visual effects, opacity control becomes embedded in value-added formulation strategies rather than treated as a cosmetic afterthought. This structurally raises the content intensity and performance requirements of opacifying systems across high-volume personal care categories.

At the value-chain level, premium positioning alters cost and margin structures by increasing tolerance for higher-performance opacifying chemistries with tailored dispersion and stability profiles. Concurrent advances in polymer-based opacifiers and biodegradable alternatives enable alignment with evolving ingredient transparency and environmental scrutiny, mitigating substitution risks associated with legacy inorganic systems. Regulatory and consumer-driven safety narratives further elevate the importance of traceability and formulation compliance, reinforcing demand for opacifiers that integrate clean-label positioning with consistent optical performance.

Barrier Analysis - High Energy Consumption in Manufacturing

The manufacturing of high-performance opacifying ingredients is structurally constrained by energy-intensive processing routes, particularly for inorganic and mineral-based chemistries that require sustained high-temperature calcination and phase transformation to achieve targeted optical properties. These thermal processing requirements embed elevated energy demand into baseline cost structures across upstream production stages, increasing sensitivity to volatility in power and fuel inputs. As energy pricing dynamics tighten and carbon cost pass-through mechanisms expand across industrial value chains, producers face structurally higher operating cost floors that are difficult to offset solely through incremental process optimization. This constrains the price competitiveness of energy-intensive opacifiers relative to lower-temperature synthetic or polymer-based alternatives, altering formulation economics for downstream users.

At the market level, rising energy and compliance costs propagate through the value chain, compressing margins for opacifier suppliers while elevating input cost pressures for coatings, plastics, and personal care formulators. Carbon pricing and emissions compliance further increase the capital intensity of manufacturing by requiring abatement systems and process electrification, thereby elongating payback cycles for capacity upgrades. These dynamics structurally disadvantage legacy production assets with limited thermal efficiency and raise barriers to cost containment, slowing capacity rationalization and moderating the pace of price-led volume expansion in cost-sensitive end-use segments.

Technical Complexity in Dispersion

The increasing technical sophistication of advanced opacifiers, particularly nano-engineered particles and polymer-based opacity modifiers, introduces greater structural complexity across formulation and compounding stages. Achieving stable, uniform dispersion requires precise control over particle size distribution, surface chemistry, and shear conditions, thereby elevating the reliance on specialized milling, high-energy mixing, and inline dispersion systems. These requirements raise the technical threshold for effectively integrating advanced opacifiers into coatings, plastics, and personal care formulations, increasing formulation risk and failure rates for operators lacking process control capabilities. As optical performance becomes more tightly coupled to dispersion fidelity, downstream manufacturers face higher qualification burdens and longer development cycles, increasing time-to-market friction across application segments.

The capital intensity of dispersion infrastructure structurally raises entry barriers for smaller and mid-scale formulators, concentrating advanced opacifier utilization among players with access to sophisticated processing assets and application engineering expertise. This reinforces asymmetries in formulation capability and shifts bargaining power toward upstream suppliers that can provide pre-dispersed concentrates or application support. The resulting cost layering across equipment, validation, and process controls elevates total system cost for advanced opacity solutions, constraining broader penetration in price-sensitive product tiers despite favorable performance differentials.

Opportunity Analysis - Expansion of Bio-based and Sustainable Opacifiers

Sustainability-driven reformulation agendas are creating a structurally significant opportunity for bio-sourced and biodegradable opacifying ingredients as downstream industries recalibrate material choices in response to green chemistry frameworks and tightening environmental scrutiny. Demand is increasingly shifting toward natural or bio-derived opacity solutions that can integrate into personal care, coatings, and packaging systems without compromising optical performance, stability, or processing compatibility. This transition reflects broader value-chain realignment away from synthetic microplastics and persistent polymers, elevating the strategic relevance of renewable feedstocks such as cellulose- and starch-derived systems and engineered natural mineral alternatives.

From a cost and margin perspective, early-stage bio-based opacifier platforms face greater production complexity and scale inefficiencies than mature synthetic chemistries, constraining near-term price competitiveness. However, progressive improvements in feedstock processing, surface functionalization, and dispersion performance are narrowing historical performance gaps, enabling substitution in visually demanding applications. As sustainability commitments translate into procurement mandates across consumer-facing value chains, compliant opacifiers gain structural pricing power and strategic importance, creating a pathway for value capture through differentiated performance within regulated formulation ecosystems.

Nanotechnology and Smart Coatings

Advances in nanotechnology are expanding addressable application space for opacifying ingredients through the integration of nano-engineered titanium dioxide and functional nano coatings within high-performance coating systems. These material innovations enable simultaneous delivery of opacity, ultraviolet shielding, and surface durability within thin-film architectures, aligning with structural requirements in aerospace and automotive coatings where weight management and functional density are critical design constraints. As coating systems evolve toward multifunctional performance layers, opacity is increasingly embedded within engineered surface chemistries rather than applied as bulk pigmentation, elevating the technical role of opacifiers within advanced coating stacks.

At the value-chain level, smart coating architectures incorporating self-healing and adaptive surface functionalities raise performance thresholds and qualification requirements for opacifying components, increasing reliance on precision-engineered materials with validated long-term stability. The integration of opacity with protective and energy-management functions alters procurement logic toward system-level performance rather than unit-cost optimization, supporting higher value capture for advanced opacifier platforms. Concurrently, regulatory oversight of nanomaterials and evolving safety assessment protocols introduce additional compliance costs and validation timelines, shaping adoption curves and reinforcing the importance of traceable, application-specific material engineering within regulated coating ecosystems.

Category-wise Analysis

Product Type Insights

Titanium Dioxide (TiO2) is expected to lead, accounting for approximately 62% share in 2026, underpinned by its unmatched refractive index, optical brightness, and broad formulation compatibility across architectural coatings, industrial paints, and plastics compounding workflows. Adoption remains anchored by performance-critical requirements for hiding power, whiteness retention, and weatherability in high-solids and exterior-grade systems, where TiO2 continues to function as the benchmark white pigment. Portfolio depth from suppliers such as The Chemours Company, Tronox, and KRONOS Worldwide sustains ecosystem lock-in through application-specific grades optimized for gloss, tint strength, and process stability. This combination of entrenched installed base, qualification inertia, and predictable high-volume demand sustains TiO2 dominance within mature coating and polymer value chains.

Opaque polymers are expected to be the fastest-growing segment, driven by formulation economics and sustainability-led redesign of water-based coatings and personal care systems seeking to partially displace mineral pigments. Growth is catalyzed by hollow-sphere polymer technologies that enhance light scattering efficiency while reducing pigment loading, improving cost-performance trade-offs in premium interior paints and sensorial personal care formats. Accelerating uptake is supported by compatibility with low-VOC chemistries and process flexibility in high-shear dispersion environments, lowering integration friction for first-time adopters. Platforms advanced by suppliers such as Dow, Arkema, and Ashland embed opaque polymers into multifunctional additive systems, increasing switching costs through workflow integration.

Application Insights

The paints & coatings segment is expected to lead, accounting for approximately 43% share, underpinned by its structurally entrenched role in architectural, infrastructure, and industrial maintenance workflows where hiding power, film uniformity, and durability are core performance parameters. Demand remains anchored by high-throughput coating lines and DIY repaint cycles that prioritize one-coat coverage and material efficiency to control applied cost per surface area. Ongoing platform evolution toward cool-roof and energy-reflective coatings reinforces opacity requirements within multifunctional coating stacks. Portfolio strategies from suppliers such as The Chemours Company, Dow, and Venator Materials embed opacifiers into standardized paint systems optimized for sheen control, solar reflectance, and dispersion efficiency.

The personal care segment is expected to be the fastest-growing segment, driven by the premiumization of sensorial formats and the functionalization of visual aesthetics across hair care, skin cleansing, and sun care workflows. Growth is catalyzed by hollow-sphere polymer technologies and surfactant-based opacifiers that deliver creamy opacity without mineral heaviness, improving texture perception and formulation stability in water-based systems. Accelerating adoption is supported by cold-process-compatible opacifiers and SPF-boosting platforms that reduce processing friction while expanding multifunctionality. As brands prioritize sensorial differentiation and clean-label compatible opacity solutions, personal care is set to outpace overall market growth.

Regional Insights

Asia Pacific Opacifying Ingredient Market Trends

Asia Pacific is expected to remain both the leading and the fastest-growing region, accounting for approximately 42% share in 2026, supported by the convergence of large-scale consumption growth and structurally advantaged manufacturing economics. The region is positioned as the primary global production hub for mineral and polymer-based opacifiers while simultaneously absorbing and expanding downstream demand from architectural coatings, industrial paints, plastics compounding, and personal care formulation. Rapid urbanization and infrastructure buildout are anticipated to sustain high-volume coatings demand, while industrialization across packaging, consumer goods, and automotive manufacturing is likely to elevate opacity requirements within performance coatings and polymer systems.

Asia Pacific is expected to retain cost leadership through integrated feedstock access, scale manufacturing, and localized processing ecosystems, reinforcing its role in global opacifier supply chains. Technology diffusion is projected to accelerate the shift toward higher-performance grades, including TiO2 extenders and polymer-based opacity modifiers, as regional formulators upgrade toward premium finishes and improved material efficiency within water-based and low-emission systems.

China is expected to function as the regional anchor shaping Asia Pacific’s forward trajectory, given its concentration of pigment processing capacity, coatings manufacturing clusters, and downstream industrial demand. Vendor strategies are projected to pivot toward localized premiumization of coatings and personal care formulations, supported by vertically integrated supply chains and closer coupling between pigment producers and formulation houses. The strategic repositioning of multinational and regional suppliers, including production footprint adjustments by players such as Tronox and capacity expansion by LB Group, is expected to reshape competitive intensity, with China continuing to anchor both supply discipline and demand momentum across the regional opacifier ecosystem.

North America Opacifying Ingredient Market Trends

North America is expected to remain a mature and structurally stable market for opacifying ingredients, approximating the single-digit share you have indicated, with demand anchored in replacement cycles, premiumization, and compliance-driven reformulation rather than greenfield capacity expansion. Demand is likely to be sustained by ongoing residential renovation intensity and refurbishment-led coatings consumption, alongside steady utilization in packaged consumer goods where visual aesthetics and formulation stability remain core performance attributes.

North America region is positioned to maintain high-value production of specialty opacifiers, supported by advanced materials science capabilities, formulation engineering depth, and a concentrated specialty chemicals manufacturing base. Technology adoption is expected to focus on performance optimization and sustainability-aligned reformulation, including lower-emission pigment-processing routes and polymer-based opacity modifiers that enable material efficiency in high-performance coating systems.

The U.S. is expected to function as the regional anchor shaping North America’s forward trajectory, given its concentration of coatings manufacturing, specialty chemical R&D infrastructure, and downstream personal care formulation platforms. Vendor strategies are likely to prioritize platform upgrades in titanium dioxide processing and polymer-based extenders to balance performance thresholds with sustainability objectives, supported by vertically integrated supply chains and application-specific grade development. Investment flows are expected to favor decarbonization of pigment manufacturing and the scaling of compliant dispersion technologies, while downstream formulators continue to embed multifunctional opacity solutions within premium architectural coatings and sensorial personal care formats.

Europe Opacifying Ingredient Market Trends

Europe is expected to remain a mature and structurally stable market, with growth anchored in compliance-driven reformulation, replacement cycles, and sustainability-led portfolio optimization rather than greenfield capacity expansion. The regional market is positioned to consolidate following regulatory clarification around titanium dioxide classification, restoring investment confidence across pigment and specialty additive value chains while maintaining elevated compliance thresholds for material safety and environmental footprint.

Europe’s dense specialty chemicals ecosystem and application engineering capabilities are set to reinforce the premiumization of compliant opacifier platforms, as modernized pigment production assets focus on energy efficiency and emissions abatement. Technology adoption is likely to center on biodegradable polymer opacifiers and TiO2 extension strategies that balance opacity performance with regulatory conformity under harmonized chemicals governance frameworks.

Germany is expected to anchor regional momentum through its leadership in specialty chemicals manufacturing and coatings formulation infrastructure, shaping qualification standards and supplier investment priorities across the European value chain. Vendor strategies are expected to pivot toward portfolio decarbonization, efficiency improvements in dispersion, and pre-qualified sustainable grades to align with procurement standards embedded in European industrial and consumer goods supply chains. Technology pathways emphasizing biodegradable polymer opacifiers and low-emission TiO2 grades are likely to accelerate replacement-driven demand, reinforcing Europe’s positioning as a compliance-led reference market for sustainable opacity solutions shaped by innovation intensity and policy-aligned industrial restructuring.

Competitive Landscape

The global opacifying ingredient market is moderately consolidated, with leadership concentrated among global suppliers such as The Chemours Company, Tronox, and Venator Materials, reflecting high structural entry barriers in titanium dioxide production and pigment-grade mineral processing. These leaders exert disproportionate influence over qualification standards, supply reliability expectations, and performance benchmarks across coatings, plastics, and industrial pigment value chains, given the capital intensity of chloride-process capacity, feedstock security requirements, and process know-how embedded in high-purity TiO2 manufacturing. Their technological footprint shapes downstream formulation architectures by defining opacity, durability, and dispersion performance thresholds that cascade into standardized product platforms across architectural and industrial coatings ecosystems.

Competitive positioning increasingly differentiates along vertical integration depth and application-specific formulation support, with scale producers extending control from ore sourcing through pigment finishing, while specialty suppliers emphasize polymer-based opacifiers and multifunctional additives. Companies such as Dow, Arkema, and Ashland anchor the more fragmented opaque polymer and specialty segments through differentiated dispersion technologies, sustainability-aligned chemistries, and application engineering.

Key Industry Highlights:

- In November 2025, Dow launched the DOWSIL™ FC-5012 ID Resin Gum at in-cosmetics Asia, enhancing color cosmetic formulations with superior sebum and water repellency for better rub resistance.

- In May 2025, Venator introduced TIOXIDE TR85, a TMP- and TME-free pigment that met evolving sustainability and regulatory standards for coatings and plastics without sacrificing performance.

- In April 2025, BASF debuted Lamesoft® OP Plus, a wax-based opacifier dispersion for rinse-off personal care, offering a high natural-origin content as a sustainable alternative to synthetic opacifiers without compromising performance.

Companies Covered in Opacifying Ingredient Market

- The Chemours Company

- Tronox Holdings plc

- Kronos Worldwide, Inc.

- Venator Materials PLC

- LB Group

- INEOS Pigments

- Tayca Corporation

- Ishihara Sangyo Kaisha, Ltd.

- Arkema

- Dow

- Evonik Industries AG

- Ashland Global Holdings Inc.

- CNNC Huayuan Titanium Dioxide

- Kumyang

- Precheza A.S.

- Grupa Azoty

Frequently Asked Questions

The global opacifying ingredient market is projected to be valued at US$22.0 billion in 2026 and is expected to reach US$34.6 billion by 2033, driven by demand for high-performance architectural coatings, personal care premiumization, and the structural shift toward sustainable formulation alternatives.

Nano-engineered opacifiers with superior surface-area efficiency and dispersion stability enable lower material loadings while maintaining optical performance. This improves formulation economics and elevates performance ceilings, allowing downstream manufacturers to justify premium positioning and shifting competitive advantage toward formulation expertise rather than scale alone.

The opacifying ingredient market is forecast to grow at a CAGR of 6.7% from 2026 to 2033, reflecting steady expansion in construction activity and increasing opacity content per unit in personal care and performance coating applications.

Asia Pacific is both the leading and fastest-growing regional market, accounting for approximately 42% share, underpinned by its role as the global manufacturing hub for pigments and coatings, rapid urbanization, and expanding consumer goods production across India and ASEAN.

The opacifying ingredient market is moderately consolidated, with leadership concentrated among Titanium Dioxide (TiO₂) majors such as The Chemours Company, Tronox Holdings, and Kronos Worldwide, which dominate through vertically integrated chloride-process capacity and feedstock security. Dow, Arkema, and Ashland lead the faster-growing opaque polymer segment through differentiated dispersion technologies and sustainability-aligned chemistries.