- Medical Devices

- Neurointerventional Device Market

Neurointerventional Device Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Neurointerventional Device Market by Product (Embolic Coils, Carotid Stents, Intracranial Stents, Neurovascular Thrombectomy, Embolic Protection Device, Flow Diverters Device, Intrasaccular Device, Stent Retrievers, Others), Technique (Neurothrombectomy Procedure, Cerebral Angiography, Stenting, Coiling Procedures, Flow Disruption), End-user (Hospitals, Ambulatory Surgical Centers, Others), and Regional Analysis from 2025 - 2032

Neurointerventional Device Market Share and Trends Analysis

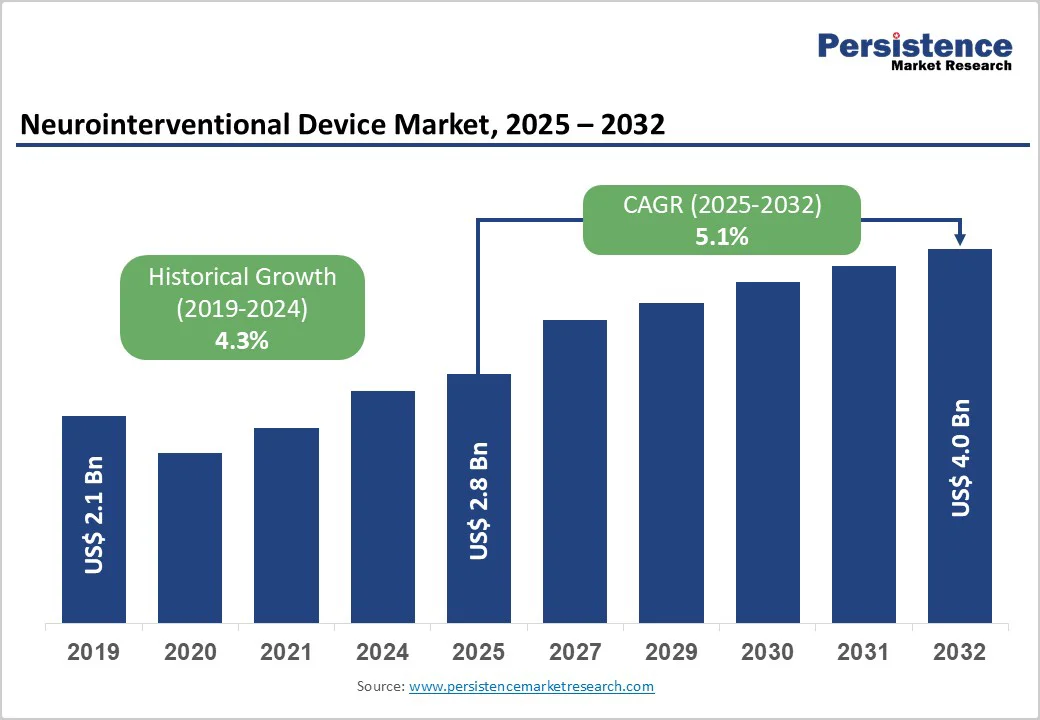

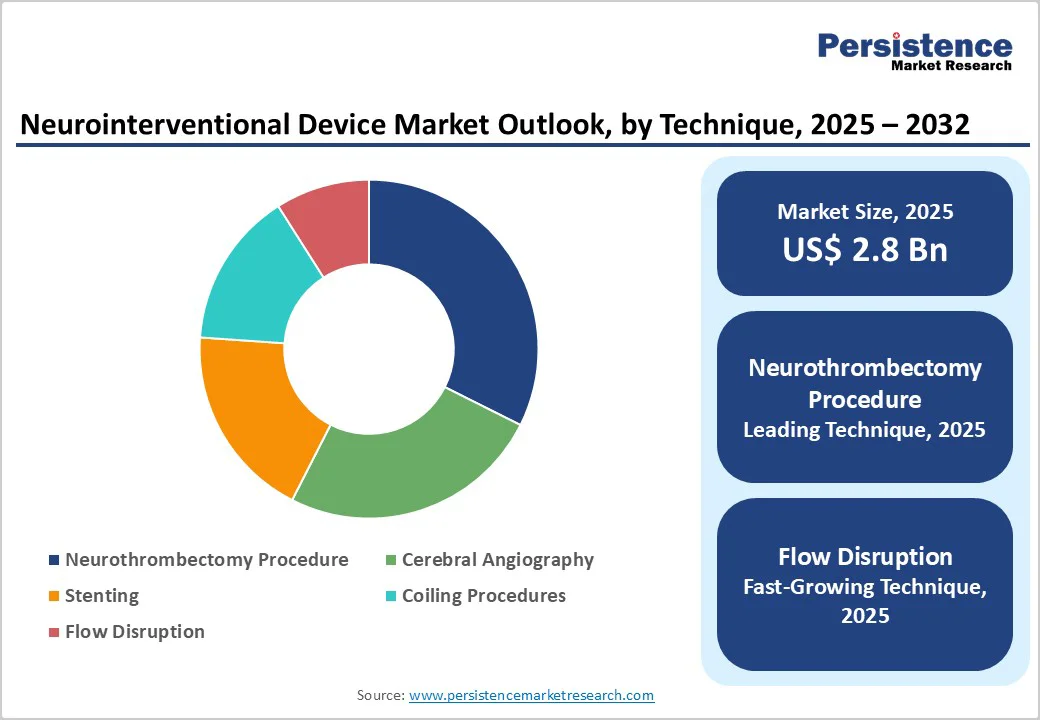

The global neurointerventional device market size is valued at US$ 2.8 billion in 2025 and projected to reach US$ 4.0 billion growing at a CAGR of 5.1% during the forecast period from 2025 to 2032.

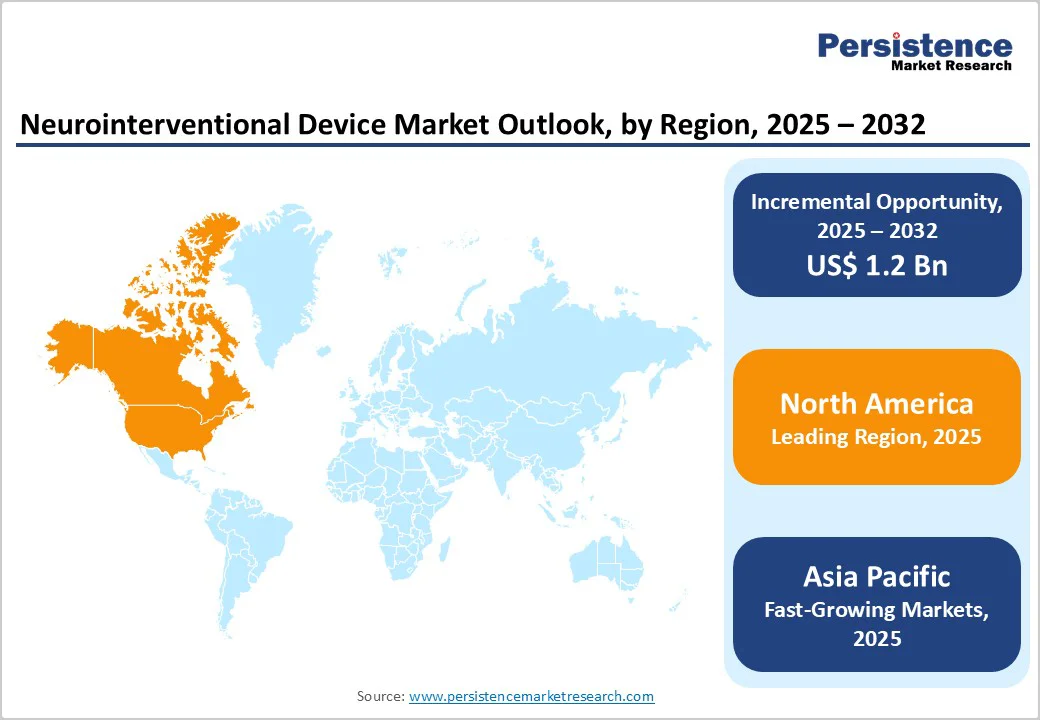

The rise in stroke and aneurysm cases, rapid technological advancements, and technological adoption in hospitals and specialized neurocenters encourage the need for neurointerventional device in healthcare institutions. North America leads due to strong healthcare infrastructure and reimbursement systems, while Asia-Pacific is the fastest-growing region, supported by a large patient pool, improving diagnostics, and increasing neurointerventional procedure volumes.

Key Industry Highlights:

- Leading Region: North America, holding around 43.0% share in 2025, driven by high stroke incidence, strong neuroimaging infrastructure, early adoption of advanced devices, and favorable reimbursement for neurointerventional procedures.

- Fastest-Growing Region: Asia-Pacific, fueled by a rising burden of cerebrovascular diseases, expanding tertiary care hospitals, increasing neurointerventional specialists, and rapid adoption of minimally invasive stroke treatments.

- Investment Plans: Europe, prioritizing R&D in next-generation stents, flow diverters, and thrombectomy systems, along with strategic collaborations and strict adherence to EU MDR standards for safety and performance.

- Dominant Technique: Neurothrombectomy procedures, leading the market due to rising acute ischemic stroke cases, strong clinical evidence supporting mechanical clot retrieval, faster patient recovery times, and widespread adoption of stent retrievers and aspiration systems as first-line treatment in major stroke centers.

| Key Insights | Details |

|---|---|

|

Global Neurointerventional Device Market Size (2025E) |

US$ 2.8 Bn |

|

Market Value Forecast (2032F) |

US$ 4.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.3% |

Market Dynamics

Driver - Rising Stroke and Aneurysm Incidence

Rising stroke and aneurysm incidence is a major driver of the neurointerventional device market, significantly increasing the need for minimally invasive neurovascular procedures. Globally, stroke remains one of the most common and severe medical emergencies, with around 11.9 million new stroke cases reported annually and more than 132 million disability-adjusted life years lost due to stroke-related complications. The global burden of stroke has risen sharply, with a 70% increase in incident cases since 1990 and more than a two-fold rise in stroke prevalence as populations age and lifestyle-related risk factors grow. In addition, unruptured intracranial aneurysms have a prevalence of about 2.8% in the general population and are detected in nearly 5% of patients admitted with ischemic stroke. This growing disease burden directly supports the adoption of neurointerventional devices such as stent retrievers, flow diverters, and intrasaccular implants to enable faster, safer, and more effective cerebrovascular treatments.

Restraints - Risk of Procedural Complications

Risk of procedural complications remains a major restraint for the neurointerventional device market, as even advanced minimally invasive techniques carry notable clinical risks. Studies on mechanical thrombectomy show that approximately 11% of treated stroke patients experience procedure-related complications, including around 5% developing symptomatic intracranial hemorrhage, about 2% facing vessel dissection, and nearly 3% encountering vasospasm during or after the intervention.

Similarly, flow-diverter procedures, widely used for complex aneurysms, report neurological complication rates of about 18% within the first year, with some patients experiencing ischemic events or delayed hemorrhage. Severe outcomes, such as delayed intraparenchymal hemorrhage or aneurysm rupture after flow-diverter placement, are associated with over 80% mortality or poor neurological recovery. These risks make both clinicians and patients cautious, particularly in centers lacking highly experienced neurointerventional teams or advanced postoperative monitoring, ultimately limiting broader adoption of these procedures and restraining market growth.

Opportunity - Growing Adoption of AI & Robotics

Growing adoption of AI and robotics is a major opportunity for the neurointerventional device market, as these technologies can dramatically improve procedural safety, precision, and access. For example, a real-time AI system used during mechanical thrombectomy achieved 97% precision and 99% recall in detecting catheter movement, prompting operators to correct catheter position quickly, without delaying procedures.

Robotic systems have also proven their worth: in a randomized trial involving 260 patients, a robot-assisted cerebral angiography system matched conventional angiography in success rate (100%) and safety, while allowing the operator to work from outside the X-ray room. AI-powered image-analysis models now detect aneurysms, vessel occlusions, and catheter tips with high accuracy, reducing the cognitive load on clinicians. Together, these advances promise lower radiation exposure, enhanced navigation in complex vascular anatomy, and the potential for remote or semi-autonomous interventions especially in underserved or rural regions.

Category-wise Analysis

By Product Insights

Embolic Coils dominates the market with 34.1% share in 2025, because they present a less invasive and safer alternative to surgical clipping for treating intracranial aneurysms. Clinical data shows that coiling is associated with significantly lower peri-operative morbidity: for example, in ruptured aneurysms, coiling patients had fewer unfavorable outcomes (including discharge to long-term care) than those undergoing clipping.

Meta-analyses indicate a roughly 33% lower risk of poor outcome (death or dependence) at one year with coiling versus clipping, along with reduced ischemic complications. Moreover, coiling typically results in shorter hospital stays and similar 1-year costs, making it more cost-effective. Although the risk of aneurysm recurrence after coiling is higher about 14.6% versus 1.4% for clipping the favorable safety profile sustains its widespread adoption, driving its leadership among neurointerventional products.

By Technique Insights

Neurothrombectomy procedures dominate the neurointerventional device market because they deliver strong, evidence-backed improvements in acute ischemic stroke outcomes. Clinical studies show that about 45.7% of patients undergoing mechanical thrombectomy achieve functional independence at 90 days, compared with 27.5% receiving only medical therapy. The procedure also achieves high rates of arterial revascularization, with success in approximately 76% of cases, compared with around 34% without thrombectomy. Mortality improves as well, with rates of 16.8% versus 20.1% in medically managed patients, while symptomatic intracranial hemorrhage remains similar at around 4–5%. These benefits rapid clot removal, better long-term recovery, and proven survival advantage, make neurothrombectomy the preferred and most widely adopted technique, ensuring its dominance in the market.

Regional Insights

North America Neurointerventional Device Market Trends

North America dominates the neurointerventional device market with 43.0 % share in 2025, due to its high stroke incidence, advanced healthcare infrastructure, and strong adoption of endovascular procedures. In the U.S. alone, about 795,000 people experience a stroke each year, and nearly 87% are ischemic, creating strong demand for neurothrombectomy and aneurysm repair devices. Access to treatment is also higher than in most regions, with nearly 49% of ischemic stroke patients initially reaching hospitals capable of performing mechanical thrombectomy. Following major clinical trial evidence, thrombectomy utilization in the U.S. more than doubled within a few years, reflecting rapid clinical adoption. Combined with well-established reimbursement systems and widespread availability of specialized stroke centers, these factors reinforce North America’s leading share.

Europe Neurointerventional Device Market Trends

Europe is a key region in the neurointerventional device market because of its high and rising stroke burden coupled with strong health-care systems. Each year, Europe records over 1 million new stroke cases, with nearly 10 million stroke survivors across the continent. Stroke causes around 460,000 deaths in Europe annually, making it a leading cause of death and long-term disability. Despite improvements, prevalence is projected to increase as populations age, with incidence rates estimated at 191.9 per 100,000 people per year. These statistics highlight massive demand for neurointerventional care such as thrombectomy and aneurysm repair, which incentivizes infrastructure upgrades, investment in specialized centers, and adoption of advanced neurovascular devices.

Asia-Pacific Neurointerventional Device Market Trends

Asia-Pacific is the fastest-growing region in the neurointerventional device market due to its very high and increasing burden of stroke. In East Asia, stroke incidence is as high as 226 per 100,000 people per year, with China’s northern regions reporting over 400 strokes per 100,000 person-years. The region also has a large population exposed to key risk factors hypertension affects 15–35% of urban adults, and rates of stroke-related deaths are climbing. Neurological disease burden in Asia was estimated to cause more than 109 million DALYs from stroke in 2021, making stroke one of the leading causes of disability. With improving neuro-care infrastructure in countries such as China, India, and Southeast Asia, demand for neurointerventional treatments like thrombectomy and aneurysm repair is expanding rapidly.

Competitive Landscape

The global neurointerventional device market is expanding steadily, driven by rising stroke and aneurysm cases and increasing preference for minimally invasive neurovascular procedures. Hospitals and stroke centers are rapidly adopting thrombectomy systems, stents, flow diverters, and embolic coils for faster, safer interventions. North America leads with advanced stroke care networks, while Asia-Pacific grows fastest due to high disease burden and improving healthcare access.

Key Industry Developments:

- In April 2025, Abbott launched its next-generation delivery system for the Proclaim DRG neurostimulation platform, enhancing procedural control and improving targeted pain relief for clinicians. The upgrade was introduced as a significant advancement aimed at simplifying implantation workflows and providing more precise therapy delivery for patients with chronic neuropathic pain.

- In April 2025, Medtronic advanced its collaboration with Abbott by submitting its interoperable insulin pump to the FDA for review. The company stated that the pump had been designed to integrate with Abbott’s continuous glucose monitoring (CGM) technology, enabling more seamless automated insulin delivery.

- In January 2024, Abbott launched the world’s smallest rechargeable neuromodulation system with remote programming capabilities to treat movement disorders. The company announced that the system had been designed to offer patients greater comfort, longer device life, and the convenience of remote adjustments without frequent hospital visits.

Companies Covered in Neurointerventional Device Market

- Abbott Laboratories

- Medtronic plc

- Stryker Corporation

- Penumbra, Inc.

- Terumo Corporation

- Johnson & Johnson (Cerenovus)

- Phenox GmbH

- Rapid Medical

- Others

Frequently Asked Questions

The global neurointerventional device market is projected to be valued at US$ 2.8 Bn in 2025.

Rising stroke and aneurysm cases, technological advancements, expanding stroke centers, growing minimally invasive adoption, and improved neuroimaging drive the neurointerventional device market.

The global neurointerventional device market is poised to witness a CAGR of 5.1% between 2025 and 2032.

Rising demand for minimally invasive stroke treatment, emerging markets, AI-enabled imaging, device innovation, and expanding ambulatory neurointervention centers create major opportunities.

Abbott Laboratories, Medtronic plc, Stryker Corporation, Penumbra, Inc., Terumo Corporation.