- Medical Devices

- Nebulizer Devices Market

Nebulizer Devices Market Size, Share, and Growth Forecast, 2025 - 2032

Nebulizer Devices Market By Product Type (Jet/Pneumatic Nebulizers, Mesh Nebulizers, Ultrasonic Nebulizers, Others), Application (COPD, Asthma, Cystic Fibrosis (CF), Others), End-user (Hospitals & Clinics, Emergency Centers, Home Healthcare, Others), and Regional Analysis for 2025 - 2032

Nebulizer Devices Market Share and Trends Analysis

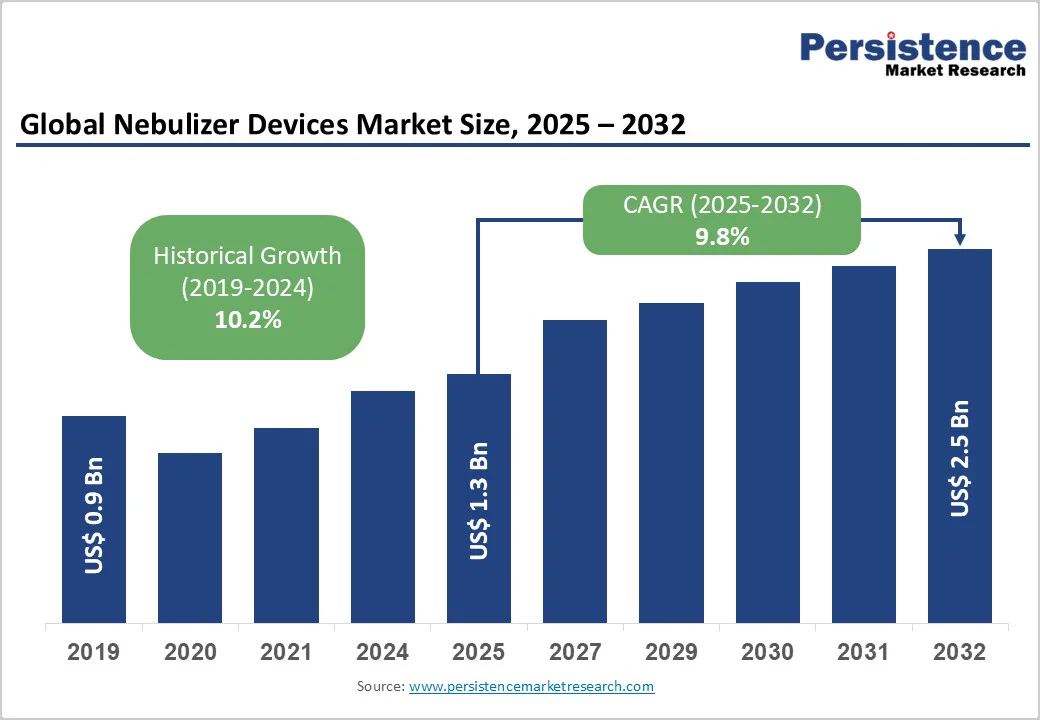

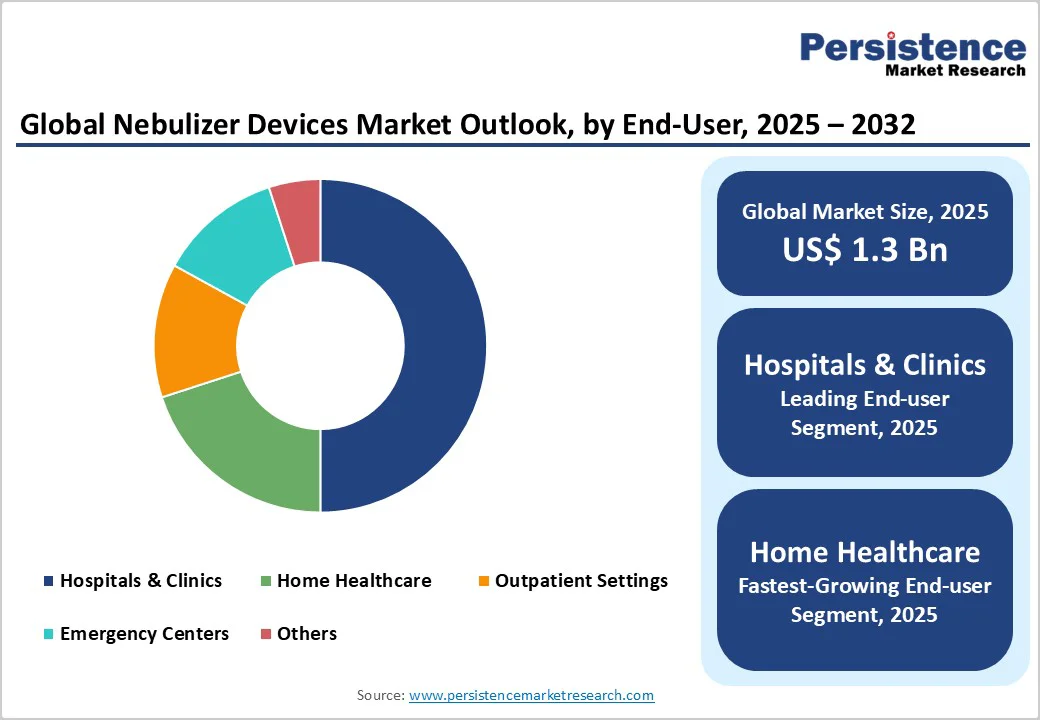

The global nebulizer devices market size is likely to be valued at US$1.3 Billion in 2025, and is estimated to reach US$2.5 Billion by 2032, growing at a CAGR of 9.8% during the forecast period from 2025 to 2032, driven by the rising incidence of chronic respiratory diseases such as chronic obstructive pulmonary disease (COPD) and asthma worldwide, the increasing adoption of portable and smart nebulizer devices, and expanding healthcare infrastructure in emerging economies.

Digital health integration and remote monitoring, along with supportive regulations and rising public awareness, are driving market growth, despite challenges in approvals and pricing.

Key Industry Highlights

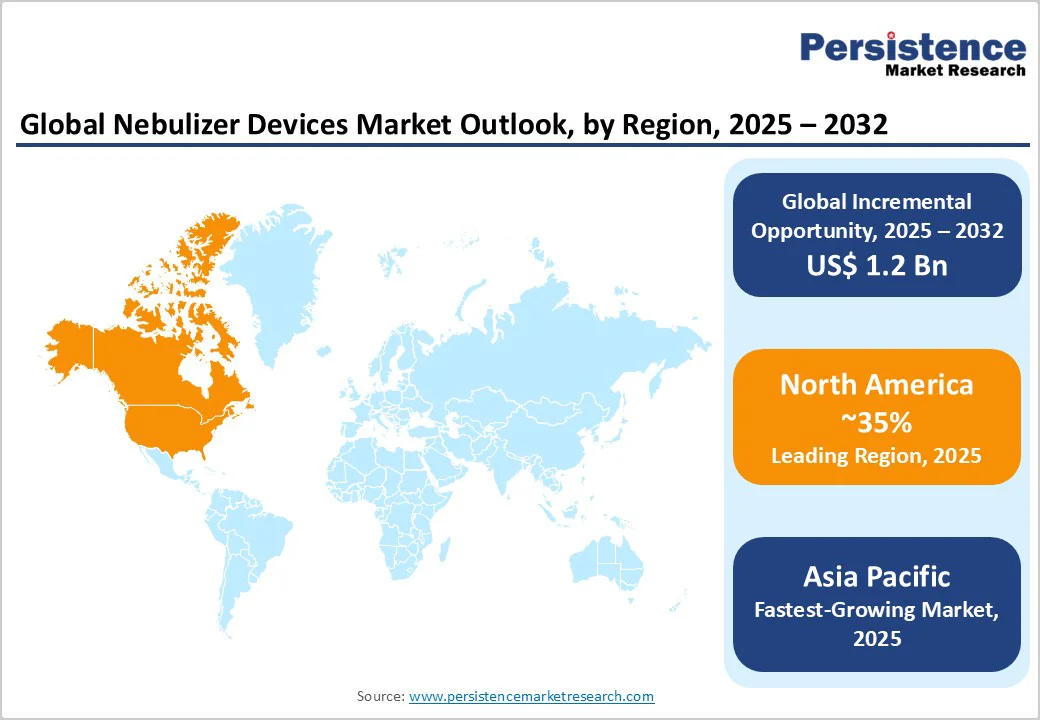

- Dominant Region: North America is expected to hold an estimated 35% market share, led by innovation and regulatory support in the U.S.

- Fastest-growing Regional Market: Asia Pacific is slated to exhibit the highest 2025 - 2032 CAGR of 11.4%, driven by manufacturing advantages and increasing incidence of respiratory diseases.

- Leading & Fastest-growing Product Types: Jet/Pneumatic nebulizers are likely to capture a dominant 55% market share in 2025, while mesh nebulizers are set to grow the fastest with a 12.3% CAGR through 2032.

- Leading Applications: COPD applications are poised to lead with approximately 40% market share in 2025, whereas asthma-related nebulizer use is predicted to be the fastest growing at 11.5% CAGR during 2025 - 2032.

- Dominant & Fastest-growing End-users: Hospitals will dominate end-user share at 50% in 2025, with home healthcare expanding the fastest between 2025 and 2032.

- Competitive Trends: Top market companies are focusing on innovating smart nebulizer devices, digital integration for patient monitoring, and geographic expansion for gaining a competitive advantage.

| Key Insights | Details |

|---|---|

| Nebulizer Devices Market Size (2025E) | US$1.3 Bn |

| Market Value Forecast (2032F) | US$2.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 9.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Convergence with Digital Health Enhancing Patient Outcomes

The convergence of digital health technologies with nebulizer devices is catalyzing a paradigm shift in respiratory care. IoT-enabled nebulizers now provide remote patient monitoring, adherence tracking, and personalized medication delivery, aligning with the international push for value-based healthcare models supported by entities such as the World Health Organization (WHO) and the U.S. Food and Drug Administration (FDA).

Innovations are presently focused on real-time inhalation pattern analysis and integration with telehealth platforms, improving treatment efficacy and reducing hospitalization rates for chronic respiratory patients. This digital transformation addresses unmet needs in patient adherence and therapy optimization, making IoT-enabled nebulizers a compelling growth vector. It also opens new revenue streams through service subscriptions and data analytics, attracting strategic investments and partnerships in device ecosystems.

Unaffordability of Advanced Devices and Variable Reimbursement Policies

The widespread adoption of cutting-edge nebulizer technologies is constrained by elevated device costs, driven by sophisticated materials, embedded sensors, and software development expenses. In many low- and middle-income countries, out-of-pocket payments account for over 80% of healthcare spending on respiratory devices, limiting accessibility.

Reimbursement frameworks also remain inconsistent globally, with many insurers hesitant to cover premium-priced nebulizers, slowing market penetration and deployment. Supply chain disruptions have further exacerbated manufacturing costs and lead times, compounding affordability challenges. To mitigate, manufacturers must innovate cost-effective production techniques and engage with policymakers to promote reimbursement reforms, ensuring equitable access and sustained market growth.

Expanding Presence in Emerging Economies with Cost-Effective Innovations

The developing economies of India, Southeast Asia, and Latin America are home to significant untapped opportunities for expansion of the nebulizer devices market. Rapid urbanization, worsening air pollution, and increasing lifestyle-related respiratory conditions contribute to a growing patient base. Currently, only a minuscule percentage of patients requiring nebulization therapy in these markets have access to adequate devices.

Improving the availability of affordable, portable, and user-friendly nebulizers tailored for these populations, supplemented by digital health literacy programs and government initiatives, could propel market growth. Business models such as pay-as-you-go and public-private health partnerships are particularly effective in these markets, facilitating access among low-income groups and rural areas. Timely entry into these markets with customized strategies will be decisive for capturing long-term growth momentum.

Category-wise Analysis

Product Type Insights

Jet/pneumatic nebulizers currently dominate the market with an estimated share of approximately 55% in 2025. Their popularity arises from a proven track record in clinical settings, affordability, and wide availability. These devices utilize compressed air to convert liquid medication into aerosols for inhalation and are preferred in hospital environments and many developing countries due to their cost-effectiveness and compatibility with a broad range of medications.

Despite newer technologies emerging, the manufacturing infrastructure supporting jet nebulizers is extensive, contributing to lower prices and easy maintenance, making them an accessible choice for healthcare providers and patients alike.

Mesh nebulizers represent the fastest-growing product category, expected to register a CAGR of 12.3% from 2025 to 2032. The widening acceptance of these devices is driven by advances in miniaturization, portability, and efficiency, enabling quieter operation and more precise drug delivery than jet nebulizers.

These nebulizers are also being preferred for home healthcare due to their convenience, battery-powered operation, and suitability for pediatric and elderly patients. Innovations include integration with smartphones for dosing reminders and usage tracking, aligning with telehealth trends. High patient compliance and adaptability to emerging digital ecosystems position mesh nebulizers as a key driver of market innovation and growth.

Application Insights

COPD is likely to account for approximately 40% of the nebulizer devices market revenue share in 2025, reflecting the substantial global burden of this chronic respiratory disorder. The rising incidence of COPD, particularly in aging populations across North America and Europe, has reinforced the demand for nebulizers embedded with cutting-edge technologies such as IoT.

Nebulizers serve as a vital component of COPD management by delivering bronchodilators and corticosteroids efficiently, improving lung function, and reducing exacerbations. Public health policies focused on chronic disease management and smoking cessation have also indirectly influenced device adoption and market stability.

Asthma applications are expected to expand with a CAGR of approximately 11.5% from 2025 to 2032. Factors propelling growth include increasing asthma prevalence, urban pollution, and heightened pediatric diagnosis.

Early intervention protocols supported by pediatricians emphasize nebulized delivery for severe and poorly controlled cases, enhancing patient outcomes. Asthma nebulizer devices with compact designs and allergen-specific treatment options are also being developed and introduced, catering to outpatient and homecare services, further accelerating this segment’s growth trajectory.

End-user Insights

Hospitals and clinics represent the largest end-user segment, anticipated to secure about 50% of the global market share in 2025. Nebulizers are integral to acute respiratory care in these settings, supported by trained personnel and standardized procedures.

Public and private hospitals utilize nebulization therapy for pre-surgical, emergency, and chronic treatment regimes. Extensive procurement budgets and bulk purchasing also contribute to this segment’s dominance. The trend toward advanced nebulizer models embedded with patient monitoring systems is more prevalent here, enhancing therapeutic precision and administrative efficiency.

Home healthcare is gaining momentum, forecasted to register an estimated CAGR of 13% during 2025 - 2032. This surge is driven by aging populations preferring home-based treatments, cost containment initiatives by payers, and the proliferation of portable, battery-operated nebulizers.

The COVID-19 pandemic accelerated remote patient management adoption, evidencing benefits such as decreased hospital visits and patient convenience. Ministries of health and insurers are increasingly supporting homecare models, creating reimbursement pathways and health education programs that sustain growth. The deployment of connected nebulizers in home settings also fosters adherence, improving clinical outcomes and lowering costs.

Regional Insights

North America Nebulizer Devices Market Trends

North America is poised to dominate with approximately 35% of the nebulizer devices market share in 2025 and is forecasted to grow at a CAGR of 8.7% through 2032. The U.S. leads, supported by a mature healthcare infrastructure accommodating advanced therapeutic technologies and reimbursement policies encouraging innovation.

The FDA’s proactive stance on digital health promotion, including guidance from its Digital Health Center of Excellence, is accelerating smart nebulizer adoption. COPD prevalence remains high in the region, with about 11.7 million Americans having been diagnosed with COPD in 2022, according to the American Lung Association, boosting the demand for optimized respiratory care solutions. Strong investment flows are being channeled into R&D and digital health initiatives, fostering partnerships between medical device manufacturers and telehealth providers.

Europe Nebulizer Devices Market Trends

Europe is slated to hold around 30% of the market share in 2025. Key markets of Germany, the U.K., France, and Spain reflect mature healthcare regulations, strong public health infrastructures, and increasing prevalence of respiratory illnesses. The European Union (EU)’s Medical Device Regulation (MDR) framework ensures uniform safety and quality standards, easing cross-border device market entry and enhancing patient safety.

A strong emphasis on outpatient and homecare respiratory services across Europe is stimulating the adoption of portable nebulizers and accompanying digital health platforms. Health technology assessment bodies are beginning to value data-driven nebulization therapy improvements, supporting reimbursement approvals across multiple countries. Investment capital flows lean toward digital transformation projects and partnerships targeting personalized respiratory care.

Asia Pacific Nebulizer Devices Market Trends

Asia Pacific is the fastest-expanding regional market for nebulizer devices, forecast to grow at a CAGR of 11.4% between 2025 and 2032. Rapid industrialization, increased urban air pollution, and rising smoking rates contribute to escalating respiratory disease incidence.

China, Japan, India, and ASEAN countries are strategic epicenters of growth, supported by government policies incentivizing local medical device manufacturing via initiatives such as Make in India and Made in China 2025. Expanding middle-class demographics with higher disposable incomes and rising health awareness are driving device adoption.

The Asia Pacific market also benefits from a cost-competitive manufacturing base, attracting multinational investments and fostering cross-border supply chains. Furthermore, healthcare infrastructure investments and telemedicine growth are enabling broader access to nebulizer devices across rural and urban areas, with increasing emphasis on affordable, portable models suited to diverse patient needs.

Competitive Landscape

The global nebulizer devices market structure is characterized by moderate consolidation, with the top five market players - Philips Respironics, PARI Pharma GmbH, Omron Healthcare, 3M Company, and Teleflex Incorporated - dominating the competitive landscape. These companies possess well-entrenched R&D capabilities, global distribution networks, and strategic partnerships that enable them to maintain market leadership.

The remaining portion of the market is fragmented among niche manufacturers and regional players catering to specialized applications or cost-sensitive segments. Barriers to entry include rigorous regulatory approvals, technological innovation requirements, and significant capital investments.

Competitive positioning focuses on expanding product portfolios with IoT-enabled and portable devices, geographic expansion into emerging markets, and strengthening after-sales service and digital health integrations. Partnerships and acquisitions are common strategies to capture fast-evolving digital health niches and enhance market access.

Key Industry Developments

- In October 2025, BiomX addressed FDA queries on the nebulizer for its BX004 cystic fibrosis therapy. The U.S. Phase 2b trial remains on hold, but European dosing continues, with topline results expected early 2026. The FDA provided Phase 3 guidance, which BiomX is integrating to advance BX004 and lift the hold.

- In July 2025, AeroRx Therapeutics reported positive Phase 2a results for AERO-007, a nebulized LABA/LAMA for COPD, showing strong bronchodilation, good tolerability, and improved lung function, addressing inhaler dosing challenges and supporting advancement to late-stage development.

- In April 2025, Baby Mom Retail launched Corvell in India, featuring a smart nebulizer as its flagship product. The brand focuses on advanced, user-friendly healthcare devices, catering to the rising demand for connected, home-based, and digital health solutions.

Companies Covered in Nebulizer Devices Market

- Philips Respironics

- PARI Pharma GmbH

- Omron Healthcare Co., Ltd.

- 3M Company

- Teleflex Incorporated

- Medtronic plc

- Smiths Medical

- DeVilbiss Healthcare LLC

- AADCO Medical, Inc.

- Vyaire Medical, Inc.

- Invacare Corporation

- Becton, Dickinson and Company (BD)

- ResMed Inc.

- Fisher & Paykel Healthcare

- Drive DeVilbiss Healthcare

Frequently Asked Questions

The nebulizer devices market is projected to reach US$1.3 Billion in 2025.

The rising incidence of chronic respiratory diseases such as COPD and asthma worldwide, increasing adoption of portable and smart nebulizer devices, and expanding healthcare infrastructure in emerging economies are driving the market.

The nebulizer devices market is poised to witness a CAGR of 9.8% from 2025 to 2032.

Advances in digital health integration and remote monitoring capabilities, growing homecare and elderly patient populations, and regulatory support for medical innovation are key market opportunities.

Philips Respironics, PARI Pharma GmbH, and Omron Healthcare Co., Ltd. are a few of the key players in the nebulizer devices market.