- Bulk Chemicals

- n-Heptane Market

n-Heptane Market Size, Trends, Share, and Growth Forecast 2025 - 2032

n-Heptane Market By Product (Industrial Grade, Solvent Grade, Analytical (HPLC) Grade), Packaging (Bulk, Drums, Intermediate Containers, Others), Distribution Channel (Direct Contact Sales, Chemical Distributors, Laboratory Suppliers), and Regional Analysis 2025 - 2032

n-Heptane Market Share and Trends Analysis

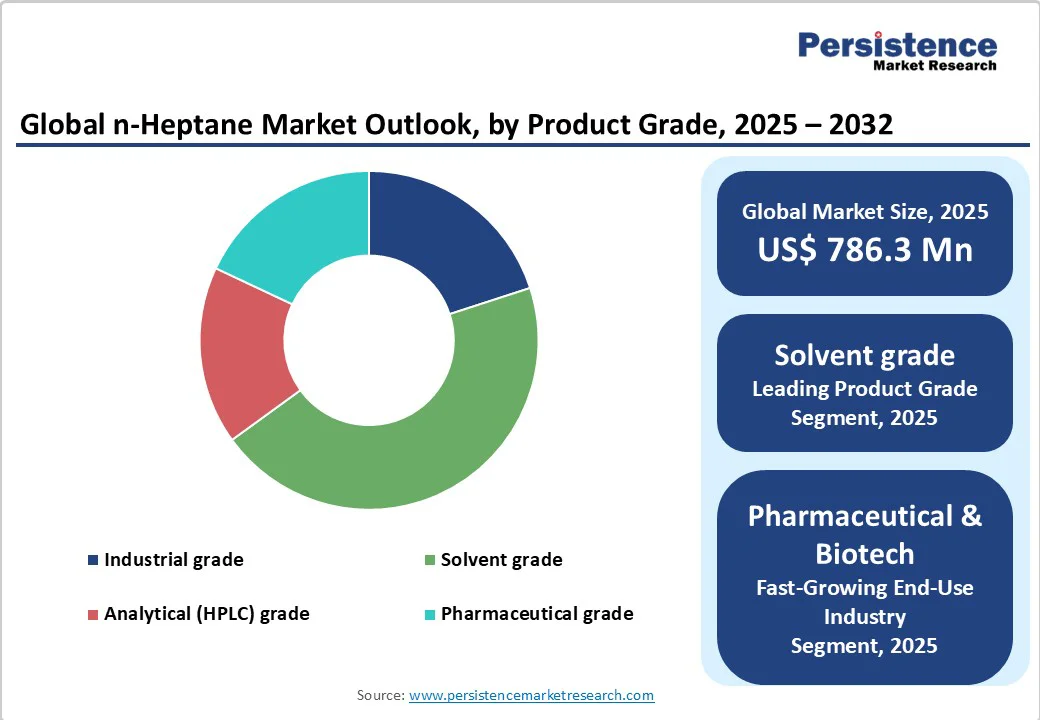

The global n-Heptane market size is likely to be valued at US$786.3 Million in 2025 and is projected to reach US$1,198.0 Million by 2032, growing at a CAGR of 6.2% between 2025 and 2032.

The rise in pharmaceutical manufacturing and analytical (HPLC) grade applications underpins market expansion. Moreover, stringent environmental regulations favor solvents with lower toxicity profiles, bolstering n-Heptane’s appeal in coatings and adhesives sectors. Strategic capacity expansions by leading producers further reinforce supply availability and pricing stability.

Key Market Highlights

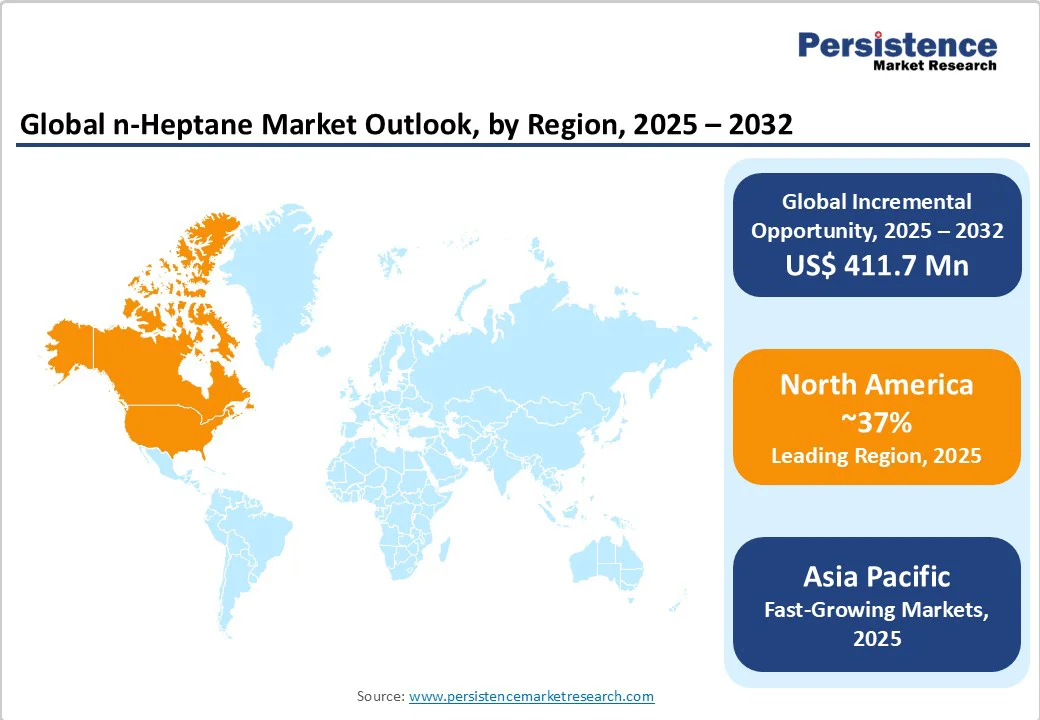

- Leading region: North America dominates due to high pharmaceutical and petrochemical testing lab activity, stringent regulations, and advanced solvent recovery infrastructure.

- Fastest Growing Region: Asia Pacific is expanding rapidly, driven by industrialization in China and specialty chemicals growth in India.

- Dominant Segment: Solvent grade held the largest share, owing to its balance of purity and cost-effectiveness for coatings and laboratory use.

- Fastest Growing Segment: Agrochemical formulations are set to surge, reflecting rising global food demand and new pesticide launches.

- Key Market Opportunity: Advancements in solvent recycling technologies present cost savings and environmental benefits, attracting investments in closed-loop systems.

| Key Insights | Details |

|---|---|

| n-Heptane Market Size (2025E) | US$ 786.3 Million |

| Market Value Forecast (2032F) | US$ 1,198.0 Million |

| Projected Growth CAGR (2025-2032) | 6.2% |

| Historical Market Growth (2019-2024) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Driver - Growing Pharmaceutical Manufacturing and High-Purity Solvent Demand

The pharmaceutical industry is the primary growth catalyst for the n-Heptane market, with demand for analytical (HPLC) and pharmaceutical grade variants expanding at unprecedented levels. N-Heptane's exceptional purity, above 99%, makes it indispensable for chromatographic separations, active pharmaceutical ingredient synthesis, and quality control processes.

The compound's low aromatic content and minimal toxicity profile align perfectly with stringent pharmacopeia standards enforced by the FDA, EMA, and other regulatory bodies.

Major pharmaceutical hubs in North America and Europe have collectively invested over US$ 12 Billion in new manufacturing facilities between 2023-2025, with each facility requiring approximately 50-100 tons of high-purity solvents annually. The increasing prevalence of chronic diseases and an aging population further amplify this demand, as pharmaceutical companies scale production to address global health challenges.

Expansion of Coatings & Adhesives Industry

The coatings and adhesives sector accounts for approximately 28% of total n-Heptane consumption, driven by its superior volatility and excellent solvency, which enhance formulation performance. Global paint and coatings market growth at 5.8% CAGR directly correlates with solvent demand, particularly as manufacturers transition toward low-VOC formulations where n-Heptane serves as an effective reactive diluent.

The construction industry's post-pandemic recovery has generated substantial demand for architectural coatings, while automotive sector growth in emerging economies is fueling industrial coating applications. Shell Chemicals and Total Petrochemicals report that their n-Heptane sales to coatings manufacturers increased by 12% year over year in 2024.

In addition, the agrochemical formulations segment leverages n-Heptane as a carrier solvent for pesticides and herbicides, with the global agrochemical market expected to reach US$350 billion by 2027. This growth is underpinned by rising food security concerns and the need for more effective crop protection solutions in developing regions.

Restraints - Stringent Environmental Regulation

Environmental regulatory frameworks present the most significant challenge to n-Heptane Market expansion, as governing bodies worldwide implement increasingly restrictive volatile organic compound emission standards. The U.S. Environmental Protection Agency and European Chemicals Agency have established maximum emission thresholds that require substantial capital investments in solvent recovery and emission control systems.

Implementation costs for compliant solvent recovery units can reach US$2-5 million per manufacturing facility, disproportionately impacting small and medium-sized enterprises. The EU's REACH Regulation mandates comprehensive chemical safety assessments, while similar frameworks in Canada, Japan, and Australia impose additional compliance burdens.

Companies report that regulatory compliance accounts for 15-20% of their total operational costs, and that documentation and testing requirements extend product registration timelines by 6-12 months. Furthermore, 18 hazardous substance reports filed with the EPA regarding n-heptane usage have prompted enhanced scrutiny and potential future restrictions.

These regulatory pressures encourage end-users to explore alternative solvents or invest in closed-loop recycling systems, potentially constraining demand for fresh n-Heptane in traditional applications.

Price Volatility of Feedstock and Supply Chain Dependencies

n-Heptane production relies heavily on petroleum-derived feedstock, making the market susceptible to crude oil price fluctuations that can significantly impact profit margins. Historical analysis reveals Brent crude prices ranged from US$ 30-120 per barrel between 2019-2024, resulting in up to 25% cost variability for downstream chemical producers.

This volatility affects long-term supply contracts and pricing strategies, forcing manufacturers to implement complex hedging strategies or pass costs to end users. Major producers such as ExxonMobil Chemical and Chevron Phillips Chemical Company report that feedstock costs represent 60-70% of their total production expenses.

Geopolitical tensions in key oil-producing regions create supply disruption risks, as witnessed during the 2022 Russia-Ukraine conflict when European chemical producers faced severe supply constraints. The concentration of refining capacity in specific geographic regions compounds this vulnerability, with the Asia Pacific accounting for 45% of global n-Heptane production capacity. Transportation and logistics costs have also increased by 20-25% since 2020, further pressuring margins and potentially limiting market access for price-sensitive applications.

Opportunity - Growth in Agrochemical Formulations

The global agrochemical industry's transformation toward more sophisticated formulations creates unprecedented demand opportunities for n-Heptane as a carrier solvent and processing aid. With the agrochemical market projected to exceed US$350 billion by 2027, growing at a 7.2% CAGR, demand for high-performance solvents in pesticide and herbicide formulations is accelerating rapidly.

N-Heptane's excellent compatibility with active ingredients, controlled evaporation rates, and low phytotoxicity make it ideal for next-generation crop protection products. Emerging economies in Southeast Asia, Latin America, and Africa are undergoing agricultural modernization, driving pesticide adoption, with countries such as India, Brazil, and Vietnam recording 15-20% annual growth in agrochemical consumption.

The shift toward precision agriculture and specialized formulations for drought-resistant crops further elevates solvent requirements. BASF, Bayer, and Syngenta have collectively announced US$8 billion in new agrochemical manufacturing capacity through 2027, primarily in the Asia Pacific and Latin America.

Additionally, the growing focus on sustainable agricultural practices is driving demand for solvent-based extraction of natural biopesticides and plant-derived active ingredients, where n-Heptane's selective solvency properties offer distinct advantages over traditional extraction methods.

Advancements in Solvent Recycling Technologies

The development of next-generation solvent recovery technologies presents substantial growth opportunities for n-Heptane suppliers and end-users seeking sustainable, cost-effective solutions. Advanced recovery processes, including membrane distillation, adsorption-based purification, and LED-enhanced separation technologies, now achieve 95-98% recovery efficiency, significantly reducing the need for fresh solvent.

Honeywell International successfully commercialized a membrane-based recovery system, achieving 97% n-Heptane reclamation efficiency, with payback periods of 18-24 months for large-scale users. These technologies enable closed-loop operations that can reduce fresh n-Heptane purchases by 30-40% while meeting environmental compliance standards.

The European Union's Circular Economy Action Plan provides €5 billion in funding for sustainable chemical processes, incentivizing the adoption of solvent-recycling infrastructure. Major chemical clusters in Germany, the Netherlands, and Texas are establishing shared solvent recovery facilities that serve multiple manufacturers, creating economies of scale.

Companies implementing these technologies report a 20-30% reduction in total solvent costs and enhanced sustainability credentials that improve market positioning. The technology also opens opportunities for specialized service providers offering solvent recovery services, creating new business models within the n-Heptane value chain.

Category-wise Insights

Product Grade Analysis

The solvent grade segment leads with approximately 45% market share, owing to its balanced purity-to-cost ratio, which is ideal for coatings, adhesives, and general industrial applications. Industrial grade follows at 25%, driven by cost-sensitive applications. Solvent grade’s dominance is underpinned by broad end-use applicability and availability from major producers such as ExxonMobil Chemical and Shell Chemicals.

Packaging Analysis

Drums command roughly a 40% share due to ease of handling and protection against contamination. Intermediate bulk containers (IBCs) hold 30% and are favored by bulk consumers. Drum packaging ensures controlled dispensing in laboratories and small plants, aligning with safety protocols and minimizing solvent losses during storage.

Distribution Channel Analysis

Chemical distributors account for 50% share, leveraging extensive logistical networks to supply regional end-users. Direct contract sales account for 20%, primarily with large-scale industrial clients, securing long-term supply at negotiated rates. Distributors’ value-added services, such as custom blending and technical support, reinforce their market position.

Application Analysis

In solvent applications, coatings, inks & adhesives lead with 28% share, driven by strong demand in automotive and construction sectors. Laboratory solvent use follows at 22%, owing to HPLC and analytical applications. The high volatility and compatibility of n-Heptane make it indispensable in precision testing labs.

Industry Analysis

Pharmaceuticals & Biotech dominate with a 35% share, driven by rigorous purity requirements for active pharmaceutical ingredient synthesis and analytical testing. Academic & Research Laboratories account for 18% and emphasize chromatographic and extraction processes. Pharmaceuticals’ growth fuels sustained demand for solvents.

Regional Insights

North America n-Heptane Trends

The U.S. leads the North American market due to the concentration of substantial pharmaceutical and petrochemical testing labs. The FDA’s stringent solvent guidelines bolster demand for high-purity n-Heptane. Investments exceeding US$1 billion in new drug development hubs in 2024 have further elevated solvent procurement.

Canada’s growing coatings sector, driven by infrastructure projects worth US$ 150 Billion, has spurred local solvent consumption. The region’s strong recycling regulations incentivize adoption of closed-loop solvent recovery units, reducing raw n-Heptane imports.

European n-Heptane Trends

Germany accounts for nearly 25% of Europe’s demand, supported by its robust chemical manufacturing base. The EU’s REACH regulations have prompted a shift towards lower-toxicity solvents such as n-Heptane.

The UK’s pharmaceutical hubs in Kent and London increased solvent use by 8% in 2024, while France’s agrochemical reformulations used n-Heptane to optimize pesticide efficacy. Regulatory harmonization across Spain and France ensures consistent quality standards, enhancing cross-border trade.

Asia Pacific n-Heptane Trends

China dominates with over 40% share, driven by rapid industrialization and expansion of paint & coatings plants in Guangdong and Jiangsu provinces. Japan’s stringent industrial solvent regulations favor high-purity imports, sustaining n-Heptane demand from electronics manufacturers. ASEAN countries are leveraging lower labor costs to establish new blending facilities, reflecting shifting manufacturing landscapes.

Competitive Landscape

The n-Heptane market is moderately consolidated, with top players such as SABIC, Chevron Phillips Chemical Company, and Reliance Industries accounting for over 60% of global capacity. Key strategies include capacity expansions, joint ventures for regional production, and R&D collaborations on solvent recycling. Leading firms differentiate via advanced purification technologies and integrated supply chains, while niche players focus on specialty grades and custom packaging solutions.

Key Market Developments

- In March 2025, ExxonMobil Chemical commissioned a state-of-the-art 50,000 tonnes per annum solvent purification facility in Baytown, Texas, featuring advanced membrane separation technology that achieves 99.8% purity levels while reducing energy consumption by 25% compared to conventional distillation processes.

- In January 2025, Shell Chemicals announced a strategic US$200 million joint venture with AkzoNobel to develop next-generation low-VOC coating formulations utilizing high-purity n-Heptane as a key solvent component, targeting the rapidly growing sustainable coatings market in Europe and North America.

- In November 2024, Honeywell International successfully launched its revolutionary HoneySolv Recovery System, a membrane-based n-Heptane reclamation technology achieving 97% recovery efficiency, with the first commercial installation at a Bayer pharmaceutical facility in Germany, reporting a 35% reduction in fresh solvent consumption.

- In September 2024, SABIC completed a US$150 million capacity expansion at its Jubail facility in Saudi Arabia, increasing n-Heptane production by 30,000 tonnes annually to serve growing demand from Asia Pacific pharmaceutical and agrochemical markets.

Companies Covered in n-Heptane Market

- ExxonMobil Chemical

- Shell Chemicals

- SABIC

- Chevron Phillips Chemical Company

- Honeywell International

- LG Chem

- Total Petrochemicals

- Reliance Industries

- Maruzen Petrochemical

- Zhejiang Materials Industry Group

- Chuzhou Runda Solvents

- DHC Solvent Chemie

- Gadiv Petrochemical Industries

- Haltermann Carless Deutschland

- Shenyang Huifeng Petrochemical

Frequently Asked Questions

The n-Heptane Market size was US$ 786.3 Million in 2025.

Key demand drivers include rising pharmaceutical manufacturing requiring analytical grade solvents and growth in coatings & adhesives due to low-VOC regulations.

The solvent grade segment leads with around 45% market share, balancing purity and cost for industrial and lab uses.

North America leads, driven by robust pharmaceutical hubs, stringent regulatory frameworks, and advanced recycling infrastructure.

Advancements in solvent recycling technologies, achieving up to 95% recovery, represent significant cost and environmental benefits.

Leading companies include ExxonMobil Chemical, Shell Chemicals, and SABIC, noted for integrated supply chains and R&D investments.