- Pharmaceuticals

- Myasthenia Gravis Treatment Market

Myasthenia Gravis Treatment Market Size, Share, and Growth Forecast, 2025 - 2032

Myasthenia Gravis Treatment Market by Drug Class (Immunosuppressants, Monoclonal Antibodies, Cholinesterase Inhibitors, Corticosteroids), Disease Type (Generalized Myasthenia Gravis, Ocular Myasthenia Gravis), End-User (Hospital, Online Pharmacies, Specialty Clinics), and Regional Analysis for 2025-2032

Myasthenia Gravis Treatment Market Share and Trends Analysis

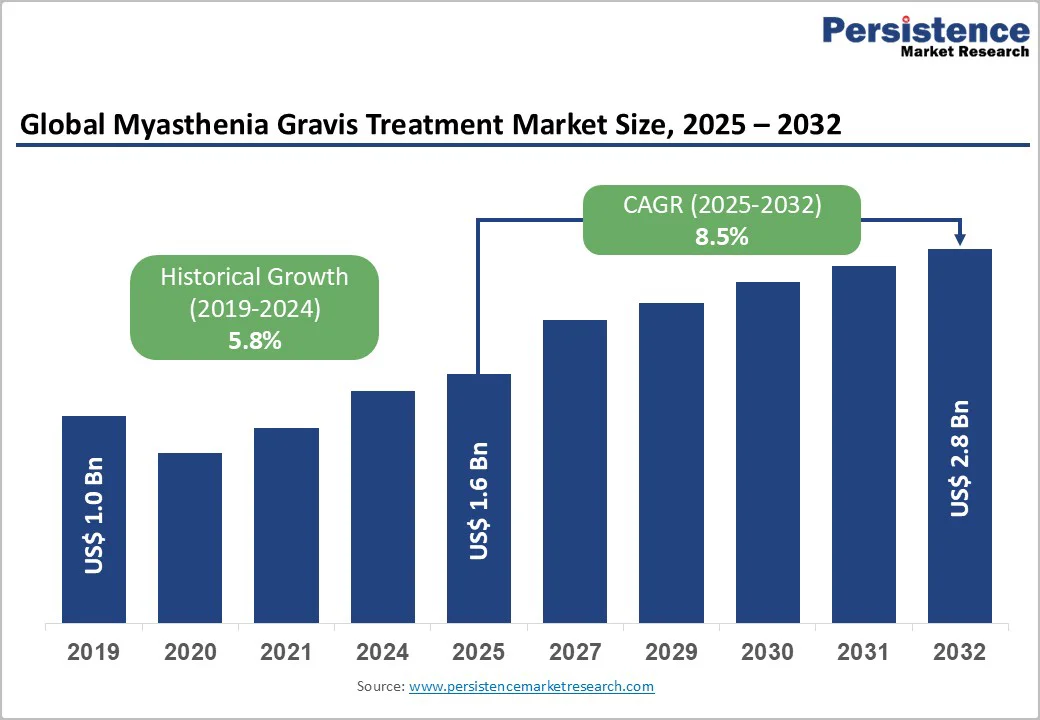

The global myasthenia gravis treatment market size is likely to be valued at US$ 1.6 billion in 2025 and is estimated to reach US$ 2.8 billion by 2032, growing at a CAGR of 8.5% during the forecast period 2025−2032. Market expansion is driven by the increased prevalence of autoimmune neuromuscular disorders, adoption of advanced biologics, approval of novel therapeutic options, and improved rates of early diagnosis. Aging populations and growing awareness of rare diseases further contribute to robust demand, while R&D in monoclonal antibodies and targeted therapies accelerates market growth. Regulatory support and improvements in healthcare infrastructure, especially in emerging economies, reinforce the market's upward trajectory.

Key Industry Highlights

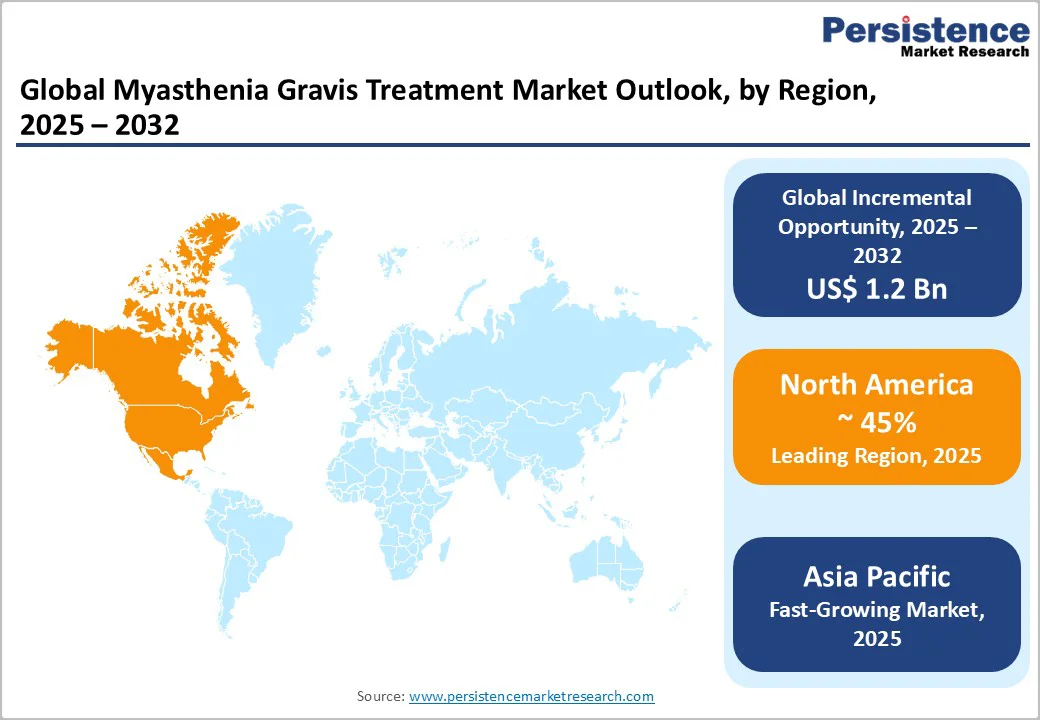

- Dominant Region: North America is set to command a significant portion of the myasthenia gravis treatment market share at approximately 45% in 2025.

- Fastest-growing Region: Asia Pacific stands out as the fastest-growing regional market from 2025 to 2032, fueled by widening recognition of rare neuromuscular diseases in the region.

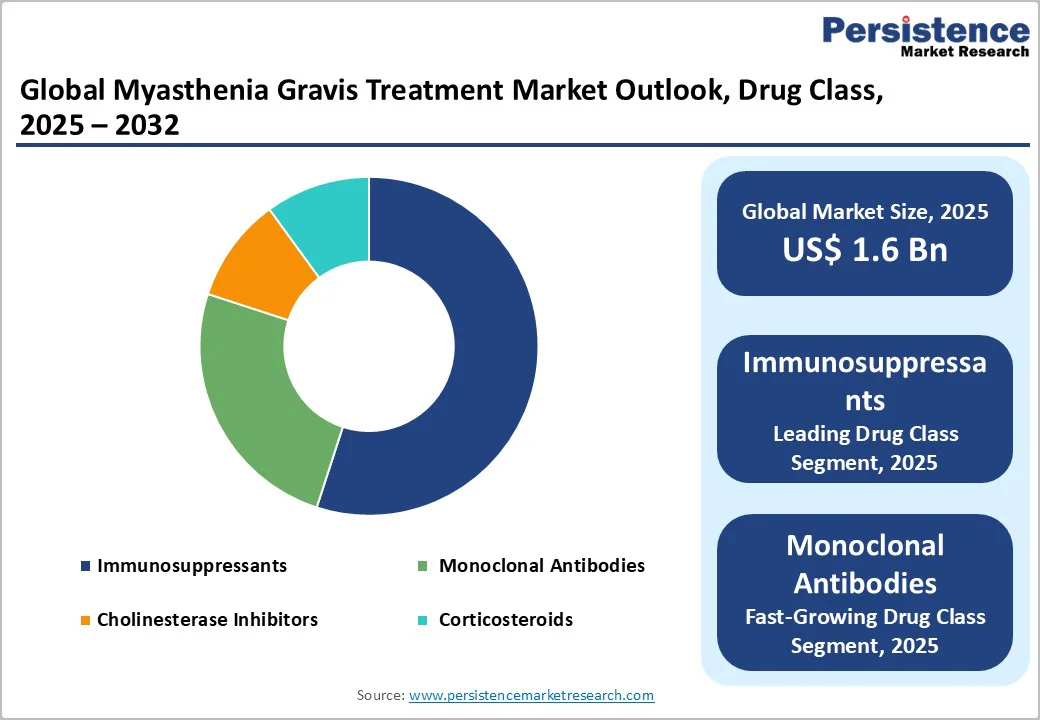

- Leading Drug Class: Immunosuppressants currently lead with 35% market share in 2025, owing to their direct ability to suppress the immune system and decrease the production of autoantibodies that contribute to the underlying disease mechanism.

- Fastest-growing Drug Class: Monoclonal antibodies are likely to be the fastest-growing segment through 2032 due to their capacity to address patients unresponsive to conventional therapies.

- Leading & Fastest-growing Disease Types: Generalized myasthenia gravis segment dominates with approximately 70% market share in 2025, while ocular myasthenia gravis (oMG) is emerging as the fastest-growing through 2032, driven by enhanced recognition among clinicians.

| Key Insights | Details |

|---|---|

| Myasthenia Gravis Treatment Market Size (2025E) | US$1.6 Bn |

| Market Value Forecast (2032F) | US$2.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Advancements in Biologic and Targeted Therapies

The treatment paradigm for myasthenia gravis (MG) has undergone a fundamental shift in recent years, driven by the emergence of biologic and targeted therapeutic agents that address specific immunologic mechanisms underlying the disease. Patients who demonstrate inadequate response to conventional immunosuppressive regimens or acetylcholinesterase inhibitors now have access to monoclonal antibodies and complement inhibitors that deliver precision targeting of pathogenic pathways, resulting in substantially improved clinical outcomes compared to historical standards. These mechanistically distinct therapies represent a significant advancement in disease management, enabling clinicians to transition away from broad-spectrum immunosuppression toward interventions with enhanced specificity and reduced collateral toxicity, thereby improving tolerability and quality of life for affected populations.

Regulatory agencies worldwide, including the U.S. Food and Drug Administration (FDA) and European Medicines Agency (EMA), have recognized the clinical significance of these advances by granting orphan drug designations and expedited review pathways to novel biologic candidates, thereby accelerating market availability and patient access. Approvals have been substantiated by compelling evidence from rigorous randomized controlled trials and real-world patient registries demonstrating sustained symptom amelioration, reduced hospitalization frequency, and diminished corticosteroid dependency. Heavy investments by pharmaceutical manufacturers in expanding R&D pipelines and manufacturing infrastructure has intensified competitive dynamics, spurred continued innovation, widened accessibility for advanced treatment options, and collectively reduced disease burden.

Supply Chain and Manufacturing Challenges

The production of biologic agents and advanced immunosuppressive therapeutics for myasthenia gravis involves extraordinarily complex manufacturing operations, comprehensive quality assurance systems, and geographically dispersed supply chain networks that demand rigorous coordination and specialized expertise. Supply chain vulnerabilities stemming from global pandemics, constraints in raw material availability, regulatory policy shifts, or geopolitical disruptions can precipitate significant interruptions in the continuity of drug supply and market distribution. These operational vulnerabilities create material risks to therapeutic continuity for patients currently on stabilized treatment regimens and can postpone market entry and commercial scale-up of novel therapies in emerging or high-growth pockets.

The technical complexity and elevated capital requirements inherent in biologic production create formidable scaling challenges that constrain the ability of manufacturers to rapidly expand output in response to surging global demand. This constraint is compounded by geographic disparities in pharmaceutical manufacturing capacity and regulatory infrastructure, creating significant barriers to equitable patient access and timely therapeutic delivery across developed and resource-limited healthcare systems. This combination of manufacturing constraints, supply chain fragility, and infrastructural limitations across certain regions necessitates strategic capacity planning, geographic diversification of production facilities, and robust supply chain resilience initiatives.

Integration of Personalized and Digital Medicine

Precision medicine and digital health innovation are fundamentally reshaping the clinical management of myasthenia gravis, enabling stratified patient care based on molecular disease phenotypes and individualized therapeutic responsiveness. Advanced serologic diagnostics targeting specific autoantibody profiles now permit clinicians to precisely match pharmacologic interventions to the underlying immunologic mechanisms driving disease in each patient, thereby minimizing exposure to non-selective immunosuppressive agents and reducing cumulative toxicity burden. This mechanistic approach to treatment selection represents a paradigm shift toward a more granular, evidence-informed methodology that enhances efficacy while simultaneously improving the safety and tolerability profile of long-term MG management.

The proliferation of sophisticated digital health infrastructure, encompassing telemedicine platforms, intelligent patient monitoring applications, and AI-enhanced clinical decision systems, is catalyzing meaningful improvements in disease surveillance frequency, intervention responsiveness, and multidisciplinary care coordination. These technological capabilities facilitate continuous collection of real-world patient data, enabling clinicians to detect clinically meaningful changes in disease trajectory, adjust therapeutic regimens with greater precision and temporal responsiveness, and optimize long-term management strategies based on current evidence and evolving clinical guidelines.

Category-wise Analysis

Drug Class Insights

The immunosuppressants segment maintains market leadership with approximately 35% share in 2025, reflecting the enduring clinical utility of this therapeutic category in MG management. This dominance is anchored in the direct immunologic efficacy of these agents, which suppress pathogenic immune responses and decrease circulating autoantibody production that perpetuates disease pathogenesis. Established immunosuppressive agents, including azathioprine, mycophenolate mofetil, and tacrolimus, continue to command widespread clinical adoption for both chronic and treatment-refractory MG cases due to their comprehensively characterized safety profiles, demonstrated durability of clinical benefit, and substantial evidence base supporting long-term tolerability. The broad accessibility of immunosuppressants, favorable insurance coverage policies, and suitability for extended maintenance therapy protocols contribute to their entrenchment as foundational therapeutic options.

Monoclonal antibodies represent the fastest-growing segment, driven by their capacity to address complex and previously difficult-to-treat patient populations, particularly those demonstrating inadequate response to conventional immunosuppressive regimens. These precision biologics leverage sophisticated targeting mechanisms that directly engage pathogenic immune pathways, including selective blockade of autoantibody-generating B cell populations and complement activation cascades, thereby delivering superior symptom control and sustained disease amelioration compared to historical standards. The demonstrable superiority of monoclonal antibodies in achieving meaningful clinical improvement, particularly in refractory MG cases, has expanded their clinical indications, catalyzed rapid adoption among specialist physicians, and fundamentally altered treatment sequencing paradigms.

Disease Type Insights

The generalized myasthenia gravis (gMG) segment commands approximately 70% of the MG market revenue share in 2025, reflecting the substantially greater clinical complexity and therapeutic intensity associated with this disease phenotype. Generalized MG is characterized by progressive involvement of multiple skeletal muscle groups beyond ocular muscles, necessitating comprehensive, prolonged therapeutic interventions that frequently incorporate hospitalization, intensive care management, multidisciplinary specialist coordination, and escalated pharmacologic regimens. The elevated disease severity, heightened risk of life-threatening myasthenic crises, and substantial burden of disease in gMG populations have positioned this segment as the primary development target for advanced therapeutic innovations.

Ocular myasthenia gravis (oMG) is emerging as the fastest-expanding segment, driven by heightened clinical awareness, advancement in diagnostic precision, and systematic implementation of comprehensive neuromuscular screening protocols that detect ocular manifestations earlier in disease courses. Improved recognition among primary care and specialist physicians of oMG as a distinct disease entity, combined with enhanced diagnostic capabilities and patient self-identification through increased health literacy, has expanded the identified patient population substantially. The expanding portfolio of disease-modifying therapies and improved understanding of progression risk from ocular to generalized disease has motivated a more timely and aggressive intervention in oMG cases, thereby increasing treatment utilization.

End-User Insights

The hospital care setting dominates the MG treatment landscape, commanding approximately 55% market share in 2025, a position firmly anchored in the clinical imperative for specialized infrastructure, advanced diagnostic capabilities, and integrated multidisciplinary expertise. Hospitals provide the essential environment for administering complex therapeutic interventions, including intravenous biologic agents, immunoglobulin replacement therapies, and acute crisis management protocols, all of which demand rigorous clinical oversight, continuous physiologic monitoring, and immediate access to emergency interventions and critical care resources. The multidisciplinary care model characteristic of hospital-based MG programs facilitates comprehensive patient evaluation through coordinated input from neurology specialists, pulmonology consultants, specialized nursing staff, and allied health professionals, enabling sophisticated diagnostic precision.

Online pharmacy platforms are emerging as the fastest-growing distribution channel, propelled by shifting consumer preferences, regulatory modernization enabling digital prescription processing and electronic fulfillment, and accelerating integration of telehealth services into routine chronic disease management. These digital platforms deliver substantial convenience advantages for MG patients, particularly those with chronic maintenance therapy requirements or physical mobility constraints, by eliminating geographic barriers to medication access, streamlining prescription renewal workflows, and enabling reliable home delivery without necessitating in-person pharmacy visits.

Regional Insights

North America Myasthenia Gravis Treatment Market Trends

North America is positioned to command approximately 45% of the myasthenia gravis treatment market share in 2025, anchored in the region's sophisticated healthcare infrastructure, elevated disease diagnosis and recognition rates, and accelerating adoption of advanced biologic therapeutic agents. The United States, which generates the predominant share of regional market revenue, distinguishes itself through intensive clinical trial infrastructure, proactive regulatory frameworks including FDA orphan drug designation programs that substantially compress approval timelines, and rapid market introduction pathways for novel disease-modifying therapies. This regulatory environment, combined with robust reimbursement systems and established specialty pharmacy networks, has created an exceptionally favorable climate for bringing innovative treatments to the market and ensuring rapid patient access to breakthrough therapies.

The region's dominant market position is further strengthened by high prevalence and incidence of MG, comprehensive diagnostic capacity, and a large, well-characterized patient population that facilitates robust clinical trial enrollment, real-world evidence generation, and post-market surveillance activities. This substantial patient base creates compelling commercial opportunities for pharmaceutical manufacturers and attracts significant capital investment in MG-focused research and development. The regional innovation ecosystem is characterized by dynamic collaboration between multinational pharmaceutical corporations, innovative biotechnology enterprises, and premier academic medical centers, collectively fostering a highly productive clinical trial pipeline and facilitating rapid translation of scientific discovery into clinical practice.

Europe Myasthenia Gravis Treatment Market Trends

Europe commands a substantial and expanding share of the myasthenia gravis treatment market, with Germany, the United Kingdom, France, and Spain functioning as regional growth engines and innovation hubs. The region benefits from harmonized regulatory infrastructure through the EMA, which streamlines drug approval processes, facilitates parallel review of novel therapies across multiple jurisdictions, and accelerates patient access to breakthrough treatments throughout the European Union (EU). Europe's well-established healthcare systems, anchored by world-class academic medical centers and highly integrated clinical delivery networks, provide the institutional foundation necessary for conducting rigorous clinical trials, implementing sophisticated diagnostic protocols, and delivering comprehensive multidisciplinary MG care.

Regional market dynamics are increasingly characterized by accelerating investment in transnational research collaborations, expanding integration of biosimilar therapies into treatment algorithms, and systematic implementation of real-world evidence methodologies to optimize clinical decision-making and therapeutic allocation. Europe's commitment to rigorous pharmacovigilance systems and comprehensive health technology assessment frameworks ensures that therapeutic innovation proceeds in balance with healthcare economic sustainability and long-term resource stewardship. This regulatory philosophy supports the simultaneous availability of cutting-edge disease-modifying agents and cost-effective treatment alternatives, thereby maximizing therapeutic access across diverse healthcare systems while maintaining robust safety surveillance standards.

Asia Pacific Myasthenia Gravis Treatment Market Trends

Asia Pacific has emerged as the fastest-expanding regional market for myasthenia gravis treatment, propelled by demographic, economic, and healthcare infrastructure developments across major economies. China, Japan, India, and other rapidly developing Asian markets are experiencing widening MG disease recognition, improved diagnostic capacity, and expanding healthcare delivery infrastructure, collectively enlarging the identifiable patient population and generating substantially increased treatment demand. Simultaneously, regional pharmaceutical manufacturing capabilities have matured substantially, enabling cost-competitive production of generic immunosuppressive agents and biosimilar biologic therapies that substantially reduce treatment costs and expand patient accessibility beyond historically privileged healthcare systems.

Supportive government policies and healthcare system modernization initiatives are further accelerating regional market development and therapeutic penetration in Asia Pacific. Progressive implementation of national rare disease registries, expanded insurance coverage for MG treatments, and systematic implementation of earlier diagnostic protocols are establishing the institutional and financial infrastructure necessary for widespread therapeutic access and improved patient outcomes. These healthcare system investments, combined with rising per capita income levels and growing consumer prioritization of specialized medical care, are creating structural tailwinds for sustained market growth throughout the forecast period.

Competitive Landscape

The global myasthenia gravis treatment market is moderately consolidated, with the top five companies together controlling a substantial share of overall revenue. Leading manufacturers such as Alexion Pharmaceuticals, UCB S.A., Roche Holding AG, argenx SE, and Novartis AG shape the competitive landscape through extensive portfolios of biologics and targeted immunotherapies, backed by sustained investment in clinical development and life-cycle management. Their scale enables broad regulatory coverage, comprehensive global distribution, and strategic collaborations that accelerate innovation and support the introduction of new treatment options across major healthcare markets.

This concentration of market power supports consistent technological advancement, high manufacturing and quality standards, and strong physician confidence in branded therapies, which in turn helps ensure reliable access and continuity of care for patients with myasthenia gravis. At the same time, smaller companies and regional players continue to occupy important roles by offering niche products, generics, and localized services that address specific pricing, access, or formulation needs in particular geographies. The interplay between large multinational innovators and specialized regional firms sustains competitive pressure, encourages differentiated product strategies, and broadens the range of therapeutic choices available to clinicians and patients.

Key Industry Developments

- In December 2025, Johnson & Johnson received European Commission (EC) approval for Imaavy (nipocalimab), a novel FcRn blocker providing sustained disease control in a broad population of adults with generalized myasthenia gravis, expanding treatment options beyond current antibody-positive restrictions.

- In November 2025, Novartis' Phase 3 RELIEVE study (NCT06744920) began evaluating remibrutinib, a potent oral BTK inhibitor, versus placebo in 180 patients with generalized myasthenia gravis. The trial builds on remibrutinib's favorable safety profile across autoimmune disorders such as CSU, where it recently gained FDA approval as the first oral BTKi.

- In April 2025, the FDA approved nipocalimab (IMAAVY™), a fully human monoclonal antibody developed by Johnson & Johnson that blocks the neonatal Fc receptor (FcRn) to reduce circulating IgG levels, for treating generalized myasthenia gravis in adult.

Companies Covered in Myasthenia Gravis Treatment Market

- Alexion Pharmaceutical Inc.

- Grifols SA

- Avadel Pharmaceuticals plc.

- Novartis AG

- Pfizer Inc.

- AbbVie Inc.

- F. Hoffmann-La Roche Ltd.

- GlaxoSmithKline plc

- Bausch Health Companies Inc.

- Shire plc.

- Others

Frequently Asked Questions

The global myasthenia gravis treatment market is projected to reach US$ 1.6 billion in 2025

Key factors that are driving market growth include rising incidence of autoimmune disorders, increasing research and development activities, and growing awareness about myasthenia gravis.

The market is poised to witness a CAGR of 8.5% from 2025 to 2032.

The emergence of targeted therapies, including complement inhibitors like zilucoplan, presents key opportunities for market players.

Alexion Pharmaceuticals, UCB S.A., Roche Holding AG, argenx SE, and Novartis AG are some of the key players in the market.