- Healthcare Services

- Musculoskeletal Medicine Market

Musculoskeletal Medicine Market Size, Share, and Growth Forecast, 2026 - 2033

Musculoskeletal Medicine Market by Drug Type (Muscle Relaxants, Analgesics, Others), Route of Administration Type (Oral, Intravenous, Topical), End-user (Hospitals, Clinics, Home Healthcare, Long-Term Care Facilities), and Regional Analysis for 2026 - 2033

Musculoskeletal Medicine Market Size and Trends Analysis

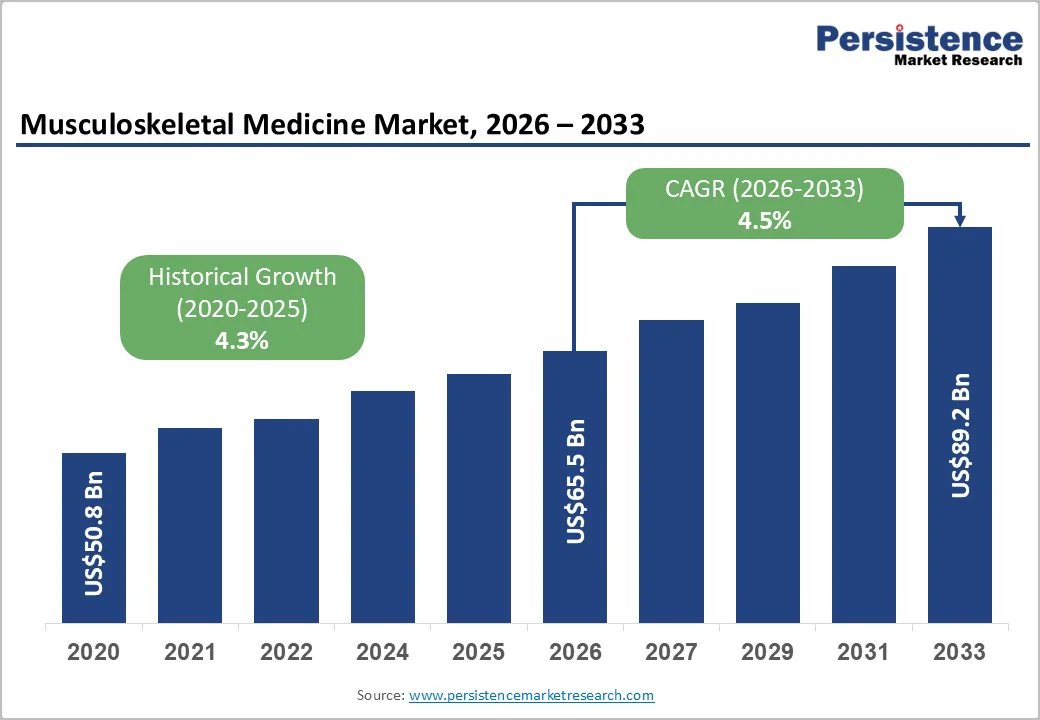

The global musculoskeletal medicine market size is likely to be valued at US$65.5 billion in 2026 and is expected to reach US$89.2 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of musculoskeletal (MSK) disorders, which affect approximately 1.71 billion people worldwide according to the World Health Organization.

The rising geriatric population is significantly increasing the incidence of chronic conditions such as osteoarthritis, osteoporosis, and rheumatoid arthritis. Growing awareness of early diagnosis and long-term disease management is supporting demand for musculoskeletal medicines. Biologic drugs and disease-modifying anti-rheumatic therapies are improving treatment efficacy and patient outcomes.

Key Industry Highlights:

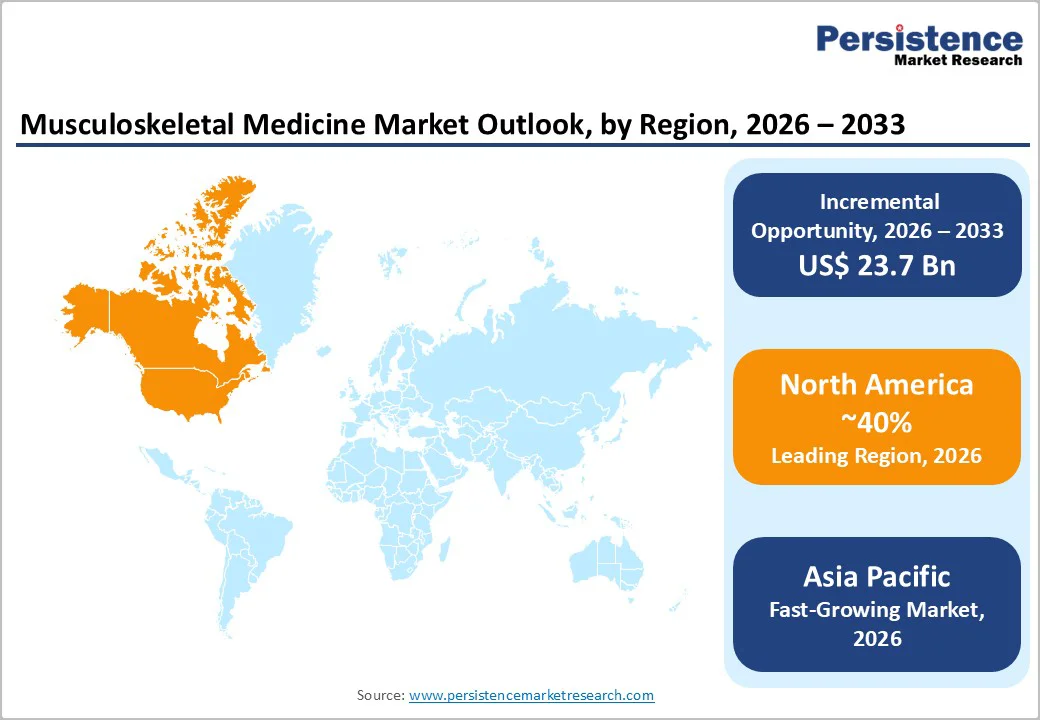

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by high disease prevalence, advanced healthcare infrastructure, strong innovation and reimbursement frameworks in the U.S., and supportive regulatory policies for biologics.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rising disease prevalence, expanding healthcare access, and supportive government initiatives.

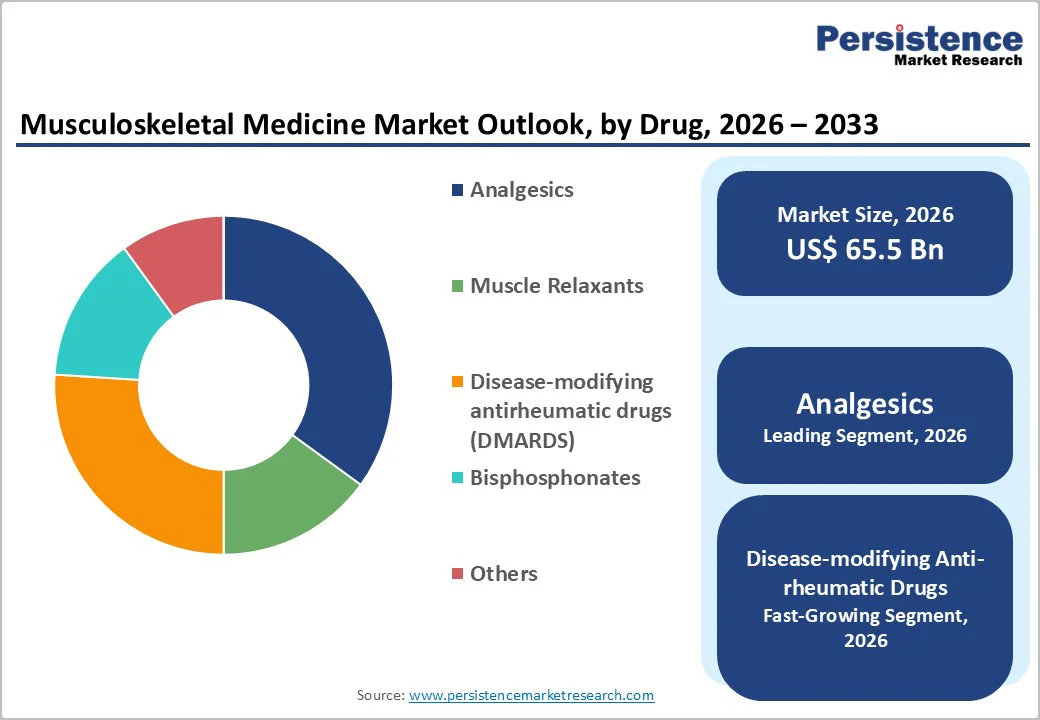

- Leading Drug Type: Analgesics are projected to represent the leading drug type in 2026, accounting for 40% of the revenue share, due to their broad use in pain management.

- Leading Route of Administration: The oral segment is anticipated to be the leading route of administration type, accounting for over 50% of the revenue share in 2026, supported by patient preference for convenience and cost-effectiveness.

- Leading End-user: Hospitals are anticipated to be the leading end-user type, accounting for over 45% of the revenue share in 2026, due to high-volume procedures and acute care requirements.

| Key Insights | Details |

|---|---|

|

Musculoskeletal Medicine Market Size (2026E) |

US$65.5 Bn |

|

Market Value Forecast (2033F) |

US$89.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Musculoskeletal Disorders

According to the World Health Organization, approximately 1.71 billion people worldwide are affected by musculoskeletal (MSK) conditions, including osteoarthritis, rheumatoid arthritis, osteoporosis, and chronic back pain. These disorders are increasingly common due to aging populations, sedentary lifestyles, obesity, and occupational hazards, which together contribute to chronic pain, limited mobility, and reduced quality of life. The growing disease burden directly increases the demand for effective pharmacological treatments, including analgesics, muscle relaxants, disease-modifying anti-rheumatic drugs (DMARDs), and biologics.

The increasing disease burden is accelerating the shift toward integrated care models that combine pharmacotherapy with rehabilitation and digital health solutions. Home healthcare and telemedicine platforms are gaining traction as patients seek cost-effective and convenient treatment options for chronic musculoskeletal conditions. According to the World Health Organization, musculoskeletal conditions account for approximately 17% of all years lived with disability (YLDs) globally, highlighting their substantial long-term health and economic burden. In developed regions such as North America and Europe, aging populations and high incidence of osteoarthritis and degenerative joint diseases are driving sustained demand for long-term pharmacological therapies and biologics.

Stringent Regulatory Requirements

Regulatory authorities such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) impose rigorous approval processes for musculoskeletal drugs, particularly biologics and disease-modifying anti-rheumatic drugs (DMARDs). These therapies require extensive preclinical testing, multi-phase clinical trials, and long-term safety and efficacy data, which significantly increase development timelines and costs. Compliance with evolving regulatory standards, pharmacovigilance obligations, and post-marketing surveillance further adds to the complexity, often delaying product launches and limiting market entry for smaller manufacturers.

High regulatory barriers, particularly in the areas of advanced therapies and biosimilars, significantly impact innovation, slowing their commercialization despite strong clinical demand. For example, biologics within DMARDs represent one of the fastest-growing drug segments, yet their approval timelines remain substantially longer than those of conventional analgesics. Stringent clinical trial requirements and complex manufacturing validations increase development costs, limiting participation by small and mid-sized pharmaceutical companies. Variations in regulatory frameworks across regions delay market entry and increase compliance burdens for manufacturers.

Development of Non-Opioid and Regenerative Therapies

Increasing concerns over opioid dependency and stricter prescribing regulations have accelerated the demand for safer, non-addictive pain management alternatives. This shift is driving innovation in non-opioid analgesics, anti-inflammatory drugs, and disease-modifying treatments that effectively manage pain while reducing the risk of abuse. As musculoskeletal disorders often require long-term treatment, healthcare providers and patients are increasingly favoring therapies that offer sustained relief with improved safety profiles, thereby expanding market adoption.

Regenerative therapies, including biologics, stem cell treatments, and platelet-rich plasma (PRP) therapies, are gaining traction for their ability to repair damaged tissues and slow disease progression rather than merely managing symptoms. These therapies are particularly promising for conditions such as osteoarthritis and rheumatoid arthritis, which contribute significantly to the overall disease burden. Growing investments in research and development, favorable regulatory pathways for innovative treatments, and rising patient awareness are supporting the integration of regenerative approaches into mainstream musculoskeletal care, creating long-term growth opportunities for pharmaceutical and biotechnology companies.

Category-wise Analysis

Drug Type Insights

The analgesics segment is expected to lead the musculoskeletal medicine market, accounting for approximately 40% of total revenue in 2026, driven by widespread use in managing both acute and chronic pain associated with musculoskeletal conditions such as osteoarthritis, lower back pain, fractures, and post-surgical recovery. Analgesics are often the first-line treatment due to their rapid pain relief, broad availability, and cost-effectiveness compared to advanced biologics. Both prescription and over-the-counter analgesics are extensively used across hospitals, clinics, and home care settings, contributing to sustained demand. The high prevalence of pain-related musculoskeletal disorders reinforces this segment’s leadership. For example, Nonsteroidal anti-inflammatory drugs (NSAIDs) such as diclofenac and ibuprofen remain widely prescribed for osteoarthritis and musculoskeletal pain management, particularly in outpatient and primary care settings.

Disease-modifying anti-rheumatic drugs (DMARDS) are likely to represent the fastest-growing segment in 2026, driven by their superior efficacy in treating autoimmune and inflammatory disorders such as rheumatoid arthritis and ankylosing spondylitis. Unlike conventional therapies, biologics target specific inflammatory pathways, leading to better disease control and reduced joint damage. Increasing diagnosis rates, earlier treatment initiation, and rising approvals for new biologic agents are accelerating growth. Although higher costs and regulatory hurdles exist, improved reimbursement coverage in developed markets and expanding access in emerging economies are supporting adoption. For example, tumor necrosis factor (TNF) inhibitors such as adalimumab are increasingly prescribed due to their proven clinical outcomes in moderate-to-severe rheumatoid arthritis.

Route of Administration Insights

The oral administration is projected to lead the market, capturing around 50% of the total revenue share in 2026, owing to its convenience, ease of use, and high patient compliance. Oral formulations are preferred for long-term management of chronic conditions such as arthritis, osteoporosis, and musculoskeletal pain, particularly in outpatient and home care settings. Cost advantages, widespread availability, and simplified dosing regimens further strengthen this segment’s leadership. Oral drugs also reduce the need for hospital visits, making them suitable for aging populations managing chronic disorders. For example, oral bisphosphonates such as alendronate are commonly prescribed for osteoporosis treatment due to ease of administration and long-term effectiveness.

The intravenous segment is likely to be the fastest-growing route of administration in 2026, driven by its distinct therapeutic advantages and expanding treatment settings. Intravenous (IV) therapies are increasingly preferred for managing severe and advanced musculoskeletal conditions, particularly autoimmune and inflammatory disorders, due to their rapid onset of action, precise dosing control, and high bioavailability. The growing adoption of IV and topical therapies is expanding treatment delivery beyond traditional clinics to include outpatient infusion centers and, increasingly, home-based care models. Advances in drug formulation, portable infusion devices, and patient education are supporting this shift. For example, intravenous biologic therapies such as infliximab are widely administered in hospital and infusion center settings for rheumatoid arthritis, while topical NSAID gels are increasingly prescribed for localized osteoarthritis pain management.

End-user Insights

Hospitals are projected to lead the market, capturing around 45% of the total revenue share in 2026, due to their central role in managing acute, complex, and severe musculoskeletal conditions. These facilities are equipped with advanced diagnostic technologies, specialized orthopedic and rheumatology departments, and multidisciplinary care teams, enabling comprehensive treatment for disorders such as rheumatoid arthritis, osteoarthritis, fractures, and post-traumatic injuries. For example, Hospitals are the primary centers for administering intravenous biologics such as infliximab for rheumatoid arthritis, as well as managing post-operative musculoskeletal pain following joint replacement surgeries.

Home healthcare is likely to be the fastest-growing end-user in 2026, driven by aging populations, preference for home-based treatment, and advancements in remote disease management. Chronic musculoskeletal conditions increasingly require long-term therapy, making home care a cost-effective alternative. Pharmaceutical companies are responding by developing patient-friendly formulations, such as oral and topical therapies, suitable for self-administration. For example, Home administration of oral analgesics and the use of remote monitoring tools for arthritis patients allow effective pain management and disease tracking, reducing hospital dependency while maintaining quality of care.

Regional Insights

North America Musculoskeletal Medicine Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, due to advanced healthcare infrastructure, high disease prevalence, and strong adoption of innovative therapies. The region’s mature pharmaceutical ecosystem supports widespread use of biologics, biosimilars, and targeted treatments for chronic musculoskeletal disorders such as rheumatoid arthritis, osteoarthritis, and ankylosing spondylitis. Healthcare systems in the U.S. and Canada benefit from extensive reimbursement frameworks that help reduce out-of-pocket costs for patients and support the uptake of high-value therapies. There is also growing integration of digital health solutions and remote patient monitoring, which enhances long-term chronic care management and improves adherence to treatment regimens.

The increasing focus on biologics and biosimilars to enhance treatment affordability and accessibility is a major trend influencing the North American musculoskeletal medicine market. Recent developments, such as Teva Pharmaceuticals’ U.S. launch of SELARSDI, a biosimilar to ustekinumab for psoriatic arthritis and related conditions, highlight the expanding role of biosimilars in delivering cost-effective musculoskeletal therapies. A growing number of regulatory approvals and label expansions are further strengthening competitive differentiation and optimizing treatment outcomes. Ongoing investments by leading companies, including AbbVie, Pfizer, and UCB, continue to advance innovation pipelines, supporting both established therapies and next-generation treatment approaches across the region.

Europe Musculoskeletal Medicine Market Trends

Europe is likely to be a significant market for musculoskeletal medicine in 2026, driven by a growing disease burden and evolving care models tailored to chronic musculoskeletal disorders such as osteoarthritis, rheumatoid arthritis, and lower back pain. According to the WHO, the region has a high prevalence of these conditions, with musculoskeletal disorders affecting over 120 million Europeans, creating substantial clinical and economic demand for effective therapeutic solutions. The aging population, sedentary lifestyles, and rising obesity rates are further increasing disease incidence, reinforcing demand for pain management medicines, disease-modifying therapies, and supportive care interventions.

The European market is witnessing expanded adoption of biologics, biosimilars, and regenerative therapies that provide targeted, long-term disease management rather than mere symptomatic relief. Healthcare providers and payers are increasingly prioritizing value-based outcomes, driving the integration of cost-effective biosimilars and personalized treatment approaches into clinical practice. Continued investments in rehabilitation technologies, minimally invasive interventions, and early-stage treatment strategies are reinforcing a comprehensive continuum of musculoskeletal care. Strong regulatory backing for biosimilar uptake, along with cross-country pricing regulations, is enhancing treatment affordability and accelerating market penetration across Europe.

Asia Pacific Musculoskeletal Medicine Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the musculoskeletal medicine market in 2026, driven by the rising prevalence of musculoskeletal disorders, increasing healthcare access, and growing awareness of long-term disease management. The region is experiencing a demographic shift with a rapidly aging population prone to chronic conditions such as osteoarthritis, rheumatoid arthritis, and osteoporosis, fueling demand for effective treatment solutions. Technological advancements in digital health, telemedicine, and remote patient monitoring are also gaining traction, enabling better management and follow-up care for chronic musculoskeletal conditions, particularly in rural and underserved areas.

The increasing entry and localization strategies of global pharmaceutical companies targeting Asia Pacific. For example, LG Chem’s Chinese partner Yifan Pharmaceutical launched a single-injection osteoarthritis treatment, Synovian, in China, underscoring rising demand for innovative musculoskeletal therapies tailored to local needs. This trend reflects a broader shift toward localized manufacturing, regional clinical trials, and pricing strategies designed to improve affordability and regulatory compliance across Asia Pacific markets.

Competitive Landscape

The global musculoskeletal medicine exhibits a moderately fragmented structure, driven by the presence of numerous multinational pharmaceutical and biotechnology companies competing to develop innovative treatments, expand therapeutic portfolios, and capture a larger share of the growing demand for musculoskeletal disorder therapies. Major players leverage strong research and development capabilities, extensive distribution networks, and strategic collaborations to maintain competitiveness. The entry of biosimilar and next-generation treatments has further intensified competition, prompting firms to prioritize value-based care and real-world evidence to differentiate their offerings and improve patient outcomes.

With key leaders including AbbVie Inc., Pfizer Inc., Johnson & Johnson, Novartis AG, and Amgen Inc., the competitive landscape is marked by aggressive efforts in R&D, strategic partnerships, and expansion into high-growth segments such as biologics and targeted therapies. These players compete through product innovation, lifecycle management of blockbuster drugs, and geographical expansion to strengthen their foothold in major regional markets. Strategic activities such as mergers and acquisitions, licensing agreements, and co-development partnerships enable companies to rapidly scale their portfolios and increase access to cutting-edge treatments.

Key Industry Developments:

- In December 2025, Dr. Reddy’s Laboratories received marketing authorization from the European Commission for AVT03, a biosimilar to Prolia and Xgeva (denosumab), used in the treatment of osteoporosis and cancer-related bone disorders. AVT03 addresses major bone-weakening conditions, including osteoporosis in postmenopausal women and men at high fracture risk, bone loss associated with hormone therapies, and prevention of skeletal complications in advanced cancers.

- In July 2024, Dr. Reddy’s Laboratories launched Muslaxin in Russia, a fixed-dose combination of ibuprofen 400 mg and chlorzoxazone 500 mg, marking the first NSAID–muscle relaxant combination in the Russian market without generic equivalents. The prescription drug is indicated for acute low back pain caused by muscle spasm, offering dual analgesic, anti-inflammatory, and muscle-relaxant action. The launch addressed a significant unmet need, as low back pain affects hundreds of millions globally and is often inadequately managed with NSAID monotherapy alone.

Companies Covered in Musculoskeletal Medicine Market

- Mylan N.V.

- Teva Pharmaceutical Industries Ltd.

- UCB S.A.

- Novartis Pharmaceuticals

- Roche Inc.

- Hospira Inc.

- Valeant Pharmaceuticals International, Inc.

- Dr. Reddy's Laboratories Ltd.

- Sun Pharmaceutical Industries Ltd.

- Sawai Pharmaceutical Co. Ltd.

- Endo International

- Hikma Pharmaceuticals

- Fresenius Kabi LLC

- Boehringer Ingelheim

- Merck

- GSK

- Bayer

- Rafa Laboratories

- Grunenthal

- Pfizer

- Sanofi

Frequently Asked Questions

The global musculoskeletal medicine market is projected to reach US$65.5 billion in 2026.

The rising prevalence of musculoskeletal disorders, aging populations, advancements in biologic and regenerative therapies, and improved access to healthcare.

The musculoskeletal medicine market is expected to grow at a CAGR of 4.5% from 2026 to 2033.

The development of non-opioid and regenerative therapies, the expansion of digital and home-based care solutions, and the growing demand for advanced treatments in emerging economies.

Mylan N.V., Teva Pharmaceutical Industries Ltd., UCB S.A., Novartis Pharmaceuticals, Roche Inc., and Hospira Inc. are the leading players.