- Biotechnology

- mRNA Synthesis and Manufacturing Market

mRNA Synthesis and Manufacturing Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

mRNA Synthesis and Manufacturing Market by Service Type (mRNA Drug Synthesis, mRNA Vaccine Synthesis), Scale of Operation (Preclinical, Clinical, Commercial), Therapeutic Area (Infectious Diseases, Oncology, Others), Application (Vaccine Production, Therapeutic Development, Drug Discovery, Others), and Regional Analysis from 2026 to 2033

mRNA Synthesis and Manufacturing Market Share and Trends Analysis

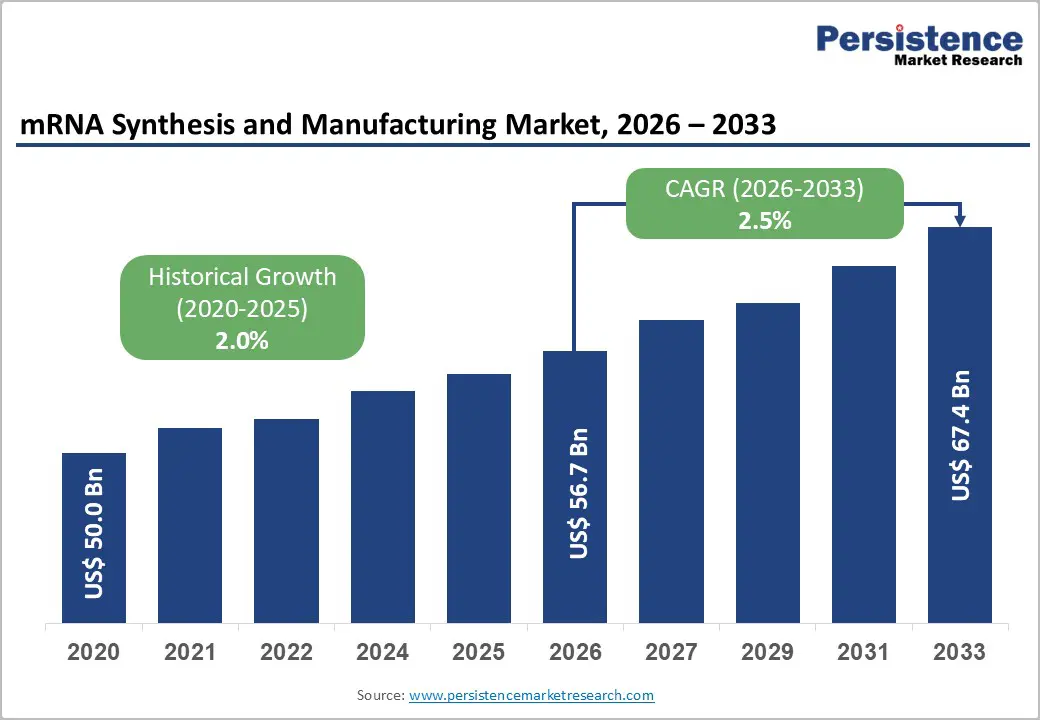

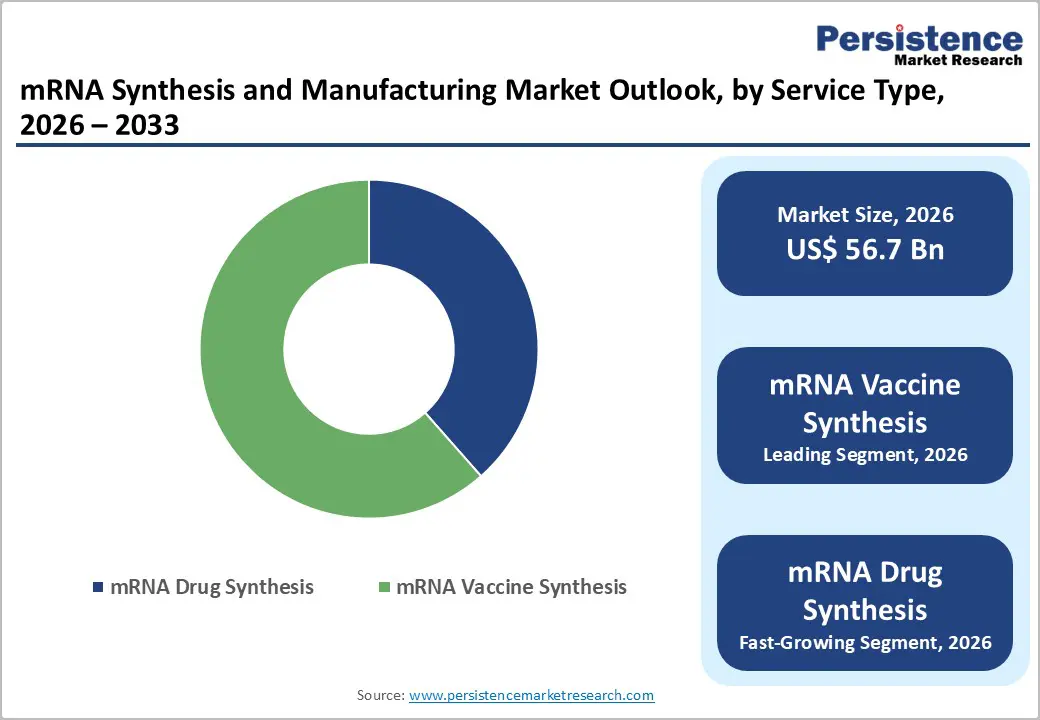

The global mRNA synthesis and manufacturing market size is likely to be valued at US$ 56.7 billion in 2026 to US$ 67.4 billion by 2033 growing at a CAGR of 2.5% during the forecast period from 2026 to 2033.

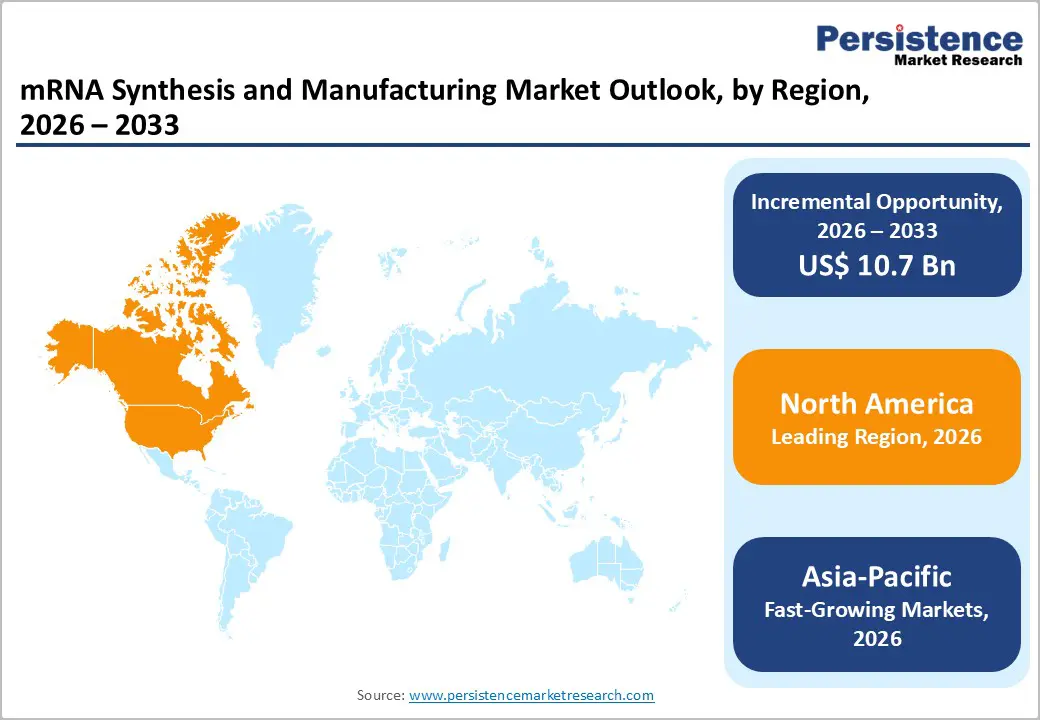

The global market is growing steadily, driven by the rising adoption of advanced therapeutics, automation, and data-driven manufacturing. North America leads owing to robust biopharmaceutical infrastructure and regulatory rigor. Asia-Pacific is the fastest-growing region, supported by expanding manufacturing capacity, government support, a skilled workforce, and increasing investments in scalable RNA production technologies.

Key Industry Highlights:

- Dominant Segment: mRNA vaccine synthesis is primarily based on in vitro transcription (IVT), which underpins commercial vaccine manufacturing. IVT enables rapid, high-yield production of precise mRNA sequences encoding target antigens, supporting fast vaccine design and scale-up. Its flexibility enables rapid adaptation to emerging pathogens, while its compatibility with GMP standards ensures consistent quality and safety, supporting large-scale clinical and commercial deployment.

- Dominant Region: North America leads with approximately a 42.6% share in 2025, supported by advanced biopharmaceutical manufacturing infrastructure, strong regulatory oversight, and high adoption of mRNA vaccines and therapeutics. Asia-Pacific is the fastest-growing region, driven by expanding mRNA manufacturing capacity, government funding, a skilled workforce, and increasing localization of vaccine and therapeutic production.

- Market Drivers: Growth is driven by sustained demand for mRNA vaccines, expanding pipelines of mRNA therapeutics, increased biopharma R&D investments, advancements in enzymes, nucleotides, and capping technologies, and rising outsourcing to specialized mRNA CDMOs.

- Market Opportunity: Key opportunities include self-amplifying mRNA (saRNA), personalized cancer vaccines, rare disease therapies, automated and continuous mRNA manufacturing platforms, AI-enabled process optimization, and rapid expansion of GMP mRNA facilities in emerging biotech regions.

| Key Insight | Details |

|---|---|

| mRNA Synthesis and Manufacturing Market Size (2026E) | US$ 56.7 Bn |

| Market Value Forecast (2033F) | US$ 67.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 2.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.0% |

Market Dynamics

Driver: Continuous Innovation in mRNA Synthesis and Manufacturing Techniques

The rapid advancements in mRNA technology are revolutionizing the biopharmaceutical industry. Innovations in mRNA synthesis and manufacturing, particularly the development of sophisticated lipid nanoparticle delivery systems, are pivotal in driving market growth.

Such advancements enhance the stability, efficacy, and delivery efficiency of mRNA-based therapeutics and vaccines. The ability to precisely engineer mRNA sequences and optimize delivery mechanisms has significantly expanded the therapeutic potential of mRNA technology beyond vaccines to include treatments for various diseases, such as cancer, genetic disorders, and autoimmune conditions. Continuous innovation improves patient outcomes and attracts substantial investment and collaboration across industry sectors, fostering a robust ecosystem for further development and commercialization.

Restraints: Complexity of Manufacturing Steps

The complexity of manufacturing steps poses a significant restraint for mRNA synthesis and manufacturing. The process involves intricate steps, including mRNA synthesis, purification, and formulation into lipid nanoparticles, each requiring precise control and specialized equipment.

Ensuring consistency and scalability across production batches adds further challenges. Moreover, stringent regulatory requirements for quality control and validation increase operational complexities and costs. These factors collectively limit the speed and scale of production, potentially delaying time-to-market for new therapies. Addressing these challenges requires sustained investment in automation, process optimization, and regulatory compliance to streamline manufacturing and effectively meet growing global demand.

Opportunity: Regulatory Support, Accelerated Approvals, and Multiple Funding Initiatives

Regulatory support and accelerated approvals are crucial for advancing the market for mRNA synthesis and manufacturing. Close collaboration between industry pioneers and regulatory bodies is essential to establish robust guidelines and expedite approval processes for mRNA-based therapies.

The proactive engagement not only accelerates the time to market for new treatments but also ensures that stringent safety and efficacy standards are met. Furthermore, funding initiatives undertaken by regulatory bodies play a pivotal role in accelerating the development and production of mRNA technologies. Such an initiative not only supports advances in vaccine and therapeutic development but also reinforces the FDA's commitment to fostering a robust ecosystem for mRNA technologies.

Category-wise Analysis

By Service Type Insights

mRNA vaccine synthesis occupies 61.5% share of the global market in 2025, because vaccines represent the highest-volume application for RNA production, driving sustained demand for large-scale synthesis services. Real-world immunization data show that more than 11 billion COVID-19 vaccine doses of all types were administered globally by early 2022, with mRNA platforms accounting for roughly 43 % of production volume during peak pandemic manufacturing efforts, reflecting unparalleled scale relative to other biologics. This massive deployment established mRNA vaccine workflows, infrastructure, and regulatory pathways, creating a dominant service demand that translates into the largest share of mRNA synthesis activity worldwide.

By Scale of Operation Insights

By scale of operation, commercial production dominates the mRNA synthesis and manufacturing market because industrial-level output far exceeds preclinical and clinical needs, anchored by worldwide demand for licensed mRNA vaccines and therapeutics. Government and industry data indicate that commercial-scale operations account for more than 85% of total mRNA synthesis and manufacturing activity, reflecting the prioritization of large-volume vaccine and therapeutic supply chains over smaller research batches. This predominance arises because commercial production requires rigorous GMP compliance, high-throughput facilities, and consistent quality to meet regulatory approval and global immunization programs, capacities that research or clinical-scale labs cannot match. The volume of commercial mRNA vaccine manufacture, exemplified by billion-dose production capacities at companies such as Pfizer/BioNTech and Moderna, underscores the scale imbalance between commercial and early-stage synthesis.

Regional Insights

North America mRNA Synthesis and Manufacturing Market Trends

North America dominates the mRNA synthesis and manufacturing market with 42.6% share in 2025, because its biopharmaceutical and vaccine production infrastructure is significantly more developed than in other regions, supported by concentrated industry hubs, public funding, and regulatory systems that enable rapid development and scale-up. U.S. government investment and pandemic response programs have historically mobilized tens of billions of dollars to develop, manufacture, and purchase mRNA vaccines, with about 92 % of fully vaccinated Americans receiving an mRNA-based COVID-19 vaccine, indicating the scale of domestic mRNA deployment. Additionally, the United States contributes the majority of North American vaccine production capacity, with around 80 % of North America’s vaccine contract manufacturing centered in U.S. hubs like Massachusetts, California, and North Carolina, reflecting robust domestic synthesis and manufacturing capabilities.

Europe mRNA Synthesis and Manufacturing Market Trends

Europe is an important region in the mRNA synthesis and manufacturing market because it combines strong biotechnology infrastructure, coordinated regulatory frameworks, and significant public and private investment in RNA technologies. The European Medicines Agency (EMA) has played a central role in authorizing multiple mRNA vaccines, demonstrating the region’s capacity to evaluate complex RNA products efficiently. European countries such as Germany and Belgium house major mRNA production facilities, including those used for pandemic vaccine manufacture, and have established networks of biotech clusters and CDMOs that support both early-stage synthesis and large-scale manufacturing. Additionally, European Union initiatives on health security and pandemic preparedness have prioritized domestic RNA production capabilities, reinforcing the region’s strategic importance in global mRNA manufacturing.

Asia Pacific mRNA Synthesis and Manufacturing Market Trends

Asia Pacific is the fastest-growing region in the mRNA synthesis and manufacturing market because governments and manufacturers are rapidly expanding local capabilities to meet both domestic and global demand. Major biopharma firms such as BioNTech have established first-of-their-kind GMP mRNA manufacturing facilities in Singapore, expected to produce up to several hundred million doses annually and create over 100 jobs, illustrating expanded regional capacity. Surveys of regional vaccine manufacturers show that 87 % view mRNA technology as a key future modality, with more than 60 % planning new or expanded mRNA facilities over the next few years, reflecting strong industry commitment to growth. Moreover, countries such as China are increasing clinical activity with dozens of approved mRNA-related trials, reinforcing sustained expansion of synthesis and manufacturing infrastructure.

Competitive Landscape

Leading mRNA synthesis and manufacturing companies prioritize scalable IVT production, advanced formulation, and GMP compliance. Investments in process optimization, AI-driven design, and high-throughput screening enhance yield, stability, and reproducibility. Collaborations with biotech, academia, and regulators accelerate mRNA and siRNA development, while integrated quality control and supply chains support vaccines, therapeutics, and precision medicine globally.

Key Industry Developments:

- In May 2025, Azenta Life Sciences announced it had formed a strategic partnership with Form Bio to advance adeno-associated virus (AAV) gene therapy development. The collaboration combined GENEWIZ’s next-generation sequencing and transgene cassette synthesis services with Form Bio’s AI- and machine learning-driven analysis pipelines, aiming to improve insights into AAV capsid content, vector integrity, and safety.

- In May 2025, TriLink BioTechnologies® launched its first mRNA synthesis kit featuring CleanCap® capping technology to simplify and enhance mRNA production. The company celebrated the debut by donating kits to leading academic institutions, supporting research and education in RNA biology.

Companies Covered in mRNA Synthesis and Manufacturing Market

- DH Life Sciences, LLC (Danaher)

- Azenta Life Sciences (Genewiz)

- Merck KGaA

- TriLink BioTechnologies

- GenScript

- Creative Biolabs

- Thermo Fisher Scientific Inc.

- BOC Sciences

- Takara Bio Inc.

- Kaneka Eurogentec S.A

- WuXi Biologics

- Aurigene Pharmaceutical Services Ltd.

- Creative Biogene

- Lonza

- System Biosciences, LLC

- Vernal Biosciences

- RiboPro

- Syngene International Limited

- BioNTech i

- Samsung Biologics

- Recipharm AB

- Catalent, Inc

- AGC Biologics

- Others

Frequently Asked Questions

The global mRNA synthesis and manufacturing market is projected to be valued at US$ 56.7 Bn in 2026.

Rising demand for mRNA vaccines, gene therapies, advanced production technologies, and global biopharmaceutical investments drive growth.

The global mRNA synthesis and manufacturing market is poised to witness a CAGR of 2.5% between 2026 and 2033.

Next-generation mRNA, saRNA, siRNA therapeutics, personalized vaccines, scalable platforms, AI optimization, and emerging biotech expansion.

DH Life Sciences, LLC (Danaher), Azenta Life Sciences (Genewiz), Merck KGaA, TriLink BioTechnologies, GenScript, Creative Biolabs.