- Pharmaceuticals

- Metered Dose Inhalers Market

Metered Dose Inhalers Market Size, Share and Growth Forecast, 2026 - 2033

Metered Dose Inhalers Market by Inhaler Type (Standard Metered Dose Inhalers, Others), Disease Type (Asthma, COPD, Others), Medication Type (Reliever Inhalers, Preventive Inhalers, Combination Therapy Inhalers), and Regional Analysis for 2026 - 2033

Metered Dose Inhalers Market Share and Trends Analysis

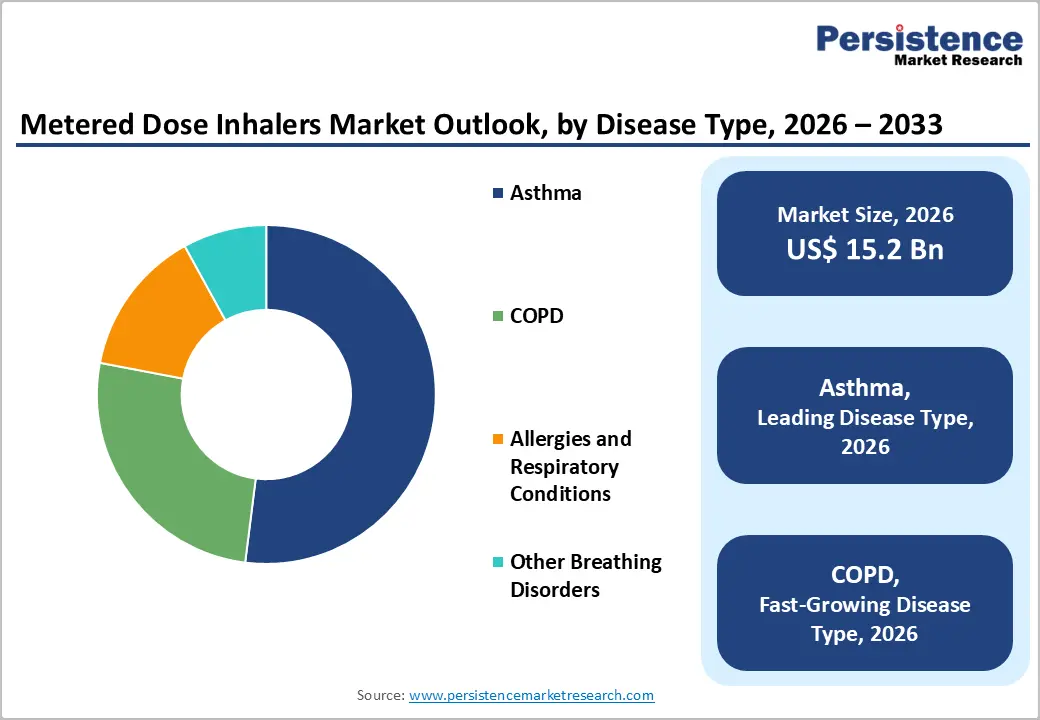

The global metered dose inhalers market size is likely to be valued at US$15.2 billion in 2026 and is projected to reach US$21.4 billion by 2033, growing at a CAGR of 5.0% during the forecast period 2026 - 2033, driven by increasing diagnosis rates of asthma and chronic obstructive pulmonary disease (COPD), expansion of home-based respiratory care, and regulatory support for environmentally sustainable inhaler technologies.

The integration of digital adherence tracking and connected healthcare platforms is also accelerating the adoption of smart inhalers and the broader digital inhaler market. Pharmaceutical manufacturers are investing in low-carbon propellants, combination therapies, and patient-centric inhalation systems to strengthen competitive positioning across developed and emerging healthcare markets.

Key Industry Highlights:

- Dominant Inhaler Types: Standard metered dose inhalers are projected to command around 47% of the revenue share in 2026, while smart inhalers are likely to grow the fastest at 5.4% CAGR through 2033, driven by connected respiratory monitoring and digital healthcare adoption.

- Leading Disease Segment: Asthma is expected to lead with an estimated 52% share in 2026, while COPD is projected to witness the fastest growth at about 5.9% CAGR during 2026 - 2033, supported by aging demographics and rising pollution-linked respiratory disorders.

- Primary Medication Category: Reliever inhalers are anticipated to dominate with approximately 44% share in 2026, whereas combination inhaler therapy is likely to emerge as the fastest-growing segment at 5.3% CAGR through 2033 due to stronger long-term disease management outcomes.

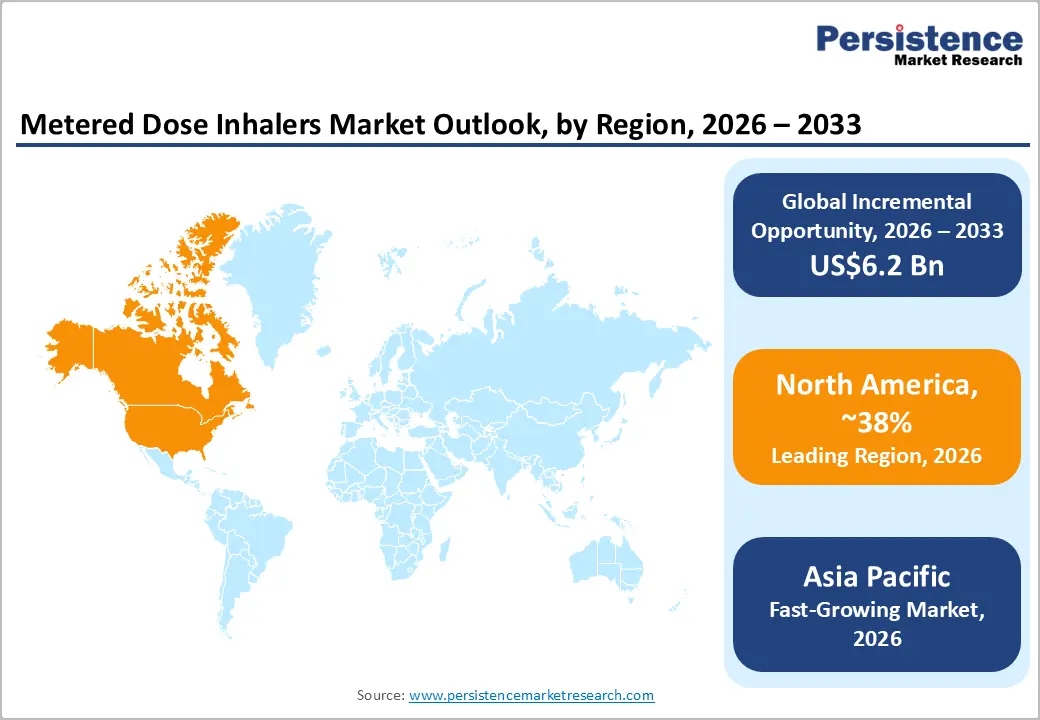

- Regional Leadership: North America is poised to dominate with an estimated 38% share in 2026, while Asia Pacific is projected to register the fastest CAGR of 5.8% through 2033, led by healthcare infrastructure expansion and respiratory drug manufacturing growth.

- Competitive Environment: Competitive strategies are increasingly focused on low-carbon propellant innovation, digitally connected inhalers, and advanced respiratory drug delivery devices, alongside expansion into emerging respiratory care markets.

DRO Analysis

Driver - Rising Global Burden of Asthma and COPD Accelerating Demand for Inhalation Therapies

The rising prevalence of chronic respiratory diseases continues to drive growth in the metered dose inhalers market. According to the World Health Organization (WHO), asthma affects an estimated 363 million people globally, while COPD causes more than 3.5 million deaths annually. . Increasing urban pollution, smoking rates, occupational exposure, and aging populations are contributing to higher respiratory disease incidence across major healthcare markets.

This growing disease burden is strengthening demand for asthma inhalers, COPD inhalers, and pressurized metered dose inhalers due to their portability and rapid drug delivery efficiency. Healthcare providers are expanding outpatient respiratory management and preventive treatment programs, increasing inhaler prescription volumes. Pharmaceutical companies are also investing in advanced formulations, combination therapies, and digital adherence technologies to improve long-term respiratory care outcomes.

Restraint - Environmental Regulations and Transition Costs for Propellant Technologies

Environmental concerns surrounding hydrofluoroalkane (HFA)-based propellants remain a major challenge for the pressurized metered dose inhalers market. Regulatory agencies across Europe and North America are tightening decarbonization requirements for respiratory drug delivery systems. Traditional pressurized Metered Dose Inhalers (pMDIs) contribute to inhaler-related greenhouse gas emissions, compelling manufacturers to invest heavily in reformulation and sustainable propellant technologies.

The transition toward low-global-warming-potential propellants requires extensive clinical testing, regulatory approvals, and manufacturing upgrades. These changes increase operational costs and create supply chain complexities, particularly for smaller manufacturers with limited R&D capabilities. Companies must also balance sustainability targets with affordability, therapeutic equivalence, and uninterrupted product availability across cost-sensitive healthcare markets.

Opportunity - Expansion of Connected Respiratory Care and Smart Inhaler Ecosystems

The growing adoption of connected healthcare technologies is creating significant opportunities for smart inhalers and the digital inhaler market. Healthcare providers are increasingly using digital respiratory monitoring tools to improve medication adherence, reduce emergency hospitalizations, and enhance chronic disease management. Bluetooth-enabled inhalers integrated with mobile applications can track dosage frequency and patient compliance in real time.

Connected inhalation platforms are gaining strong traction in asthma and COPD management due to persistent global non-adherence challenges. In October 2025, the U.S. FDA granted 510(k) clearance to Aptar Digital Health’s HeroTracker Sense, a connected add-on device for pressurized metered dose inhalers, supporting wider adoption of digitally enabled respiratory care. Rising smartphone penetration, telemedicine expansion, and investment in AI-enabled monitoring solutions are further accelerating growth opportunities for advanced inhalation therapy devices.

Category-wise Analysis

Inhaler Type Insights

Standard metered dose inhalers are projected to dominate with an estimated 47% share in 2026, supported by affordability, strong prescription volumes, and broad reimbursement coverage across asthma and COPD therapies. Their portability and rapid drug delivery continue to support widespread adoption in hospitals and outpatient care. In May 2025, the U.K. MHRA approved AstraZeneca’s low-carbon Trixeo Aerosphere inhaler for COPD treatment, reinforcing continued innovation in pressurized metered dose inhalers.

Smart inhalers are expected to grow at the fastest CAGR of 5.4% through 2033, driven by rising demand for connected respiratory monitoring and adherence tracking. Healthcare providers are increasingly integrating digital inhaler platforms into chronic disease management programs. In June 2025, Irish healthtech firm Phyxiom launched a digital respiratory monitoring platform for asthma and COPD management, supporting growth across the digital inhaler market.

Disease Type Insights

Asthma is anticipated to remain the leading segment with around 52% share in 2026, supported by increasing diagnosis rates, pollution exposure, and growing respiratory health awareness. Demand for preventive and rescue Asthma Inhalers remains strong across both developed and emerging healthcare markets. In May 2025, AstraZeneca reported positive late-stage trial results for Breztri Aerosphere in uncontrolled asthma treatment.

COPD is projected to witness the fastest growth at a CAGR of 5.9% during 2026 - 2033, driven by aging populations, smoking-related illnesses, and rising industrial pollution exposure. Healthcare systems are expanding pulmonary disease management and home-based respiratory care programs globally. In May 2025, the U.K. MHRA approved the first low-carbon Trixeo Aerosphere inhaler for COPD treatment, highlighting growing investment in advanced COPD Inhalers.

Medication Type Insights

Reliever inhalers are projected to account for nearly 44% of market revenue in 2026, owing to their widespread use in emergency asthma attacks and acute COPD symptom relief. Short-acting bronchodilators continue to generate strong prescription demand across hospitals and retail pharmacies. In June 2025, U.S. lawmakers investigated pricing and accessibility concerns related to pediatric asthma inhalers, highlighting continued dependence on reliever therapies.

Combination inhaler therapy is expected to grow at the fastest CAGR of 5.3% through 2033, supported by increasing physician preference for integrated maintenance therapies combining corticosteroids and bronchodilators. These inhalers improve adherence and reduce exacerbation risks in long-term respiratory care. In October 2025, Chiesi announced U.S. FDA acceptance of its triple-combination inhaler application for asthma maintenance treatment, strengthening commercial momentum in combination respiratory therapies.

Regional Analysis

North America Metered Dose Inhalers Market Trends

North America is projected to account for approximately 38% of global market revenue in 2026, supported by advanced respiratory care infrastructure, high asthma prevalence, and rapid adoption of connected healthcare technologies. The region continues to lead demand for smart inhalers and digital respiratory monitoring systems. In February 2026, the U.S. Department of Health and Human Services expanded funding support for chronic respiratory disease management programs, strengthening long-term inhalation therapy adoption.

U.S. Metered Dose Inhalers Market Trends

The U.S. is expected to contribute nearly 32% of the North American market in 2026, driven by strong respiratory drug spending and inhaler innovation. Pharmaceutical companies are expanding investments in AI-enabled adherence monitoring and sustainable inhaler technologies. In January 2026, Teva Pharmaceuticals expanded respiratory manufacturing operations in Pennsylvania to strengthen asthma and COPD inhaler supply capacity.

Canada Metered Dose Inhalers Market Trends

Canada is projected to account for around 11% of the regional market in 2026, supported by rising telehealth adoption and preventive respiratory care initiatives. Home-based pulmonary monitoring and connected respiratory care platforms are gaining traction across the country. Government-led healthcare digitization programs are also supporting demand for advanced inhalation therapy devices.

Europe Metered Dose Inhalers Market Trends

Europe is estimated to hold nearly 29% of global market revenue in 2026, supported by strong healthcare reimbursement systems and increasing adoption of sustainable inhaler technologies. The region is accelerating the transition toward low-emission respiratory devices under stricter carbon reduction policies. Demand for preventive pulmonary therapies and connected inhaler platforms continues to expand across major European healthcare markets.

Germany Metered Dose Inhalers Market Trends

Germany is projected to contribute approximately 24% of the European market in 2026, supported by advanced pharmaceutical manufacturing and respiratory treatment infrastructure. The country remains a major hub for inhaler engineering and pulmonary drug development. In March 2025, Boehringer Ingelheim expanded investment in respiratory biologics and inhalation therapy R&D operations in Germany.

U.K. Metered Dose Inhalers Market Trends

The U.K. is anticipated to account for nearly 21% of the regional market in 2026, driven by increasing adoption of low-carbon inhalers and digital respiratory care solutions. In September 2025, the U.K. National Health Service expanded green inhaler prescribing initiatives to reduce healthcare-related carbon emissions. Growing investment in connected respiratory monitoring programs is also supporting market growth.

Asia Pacific Metered Dose Inhalers Market Trends

Asia Pacific is projected to account for approximately 24% of global market revenue in 2026 and register the fastest regional growth, driven by rising respiratory disease burden and expanding inhaler manufacturing investments. Increasing pollution exposure, smoking prevalence, and asthma diagnosis rates are strengthening demand for affordable Asthma Inhalers and COPD Inhalers. Regional manufacturers are also investing in low-cost and digitally integrated respiratory therapies.

China Metered Dose Inhalers Market Trends

China is expected to contribute around 36% of the Asia Pacific market in 2026, supported by strong pharmaceutical manufacturing capabilities and expanding respiratory healthcare access. The country continues to strengthen local inhaler production and chronic respiratory disease management programs. In April 2025, China’s National Medical Products Administration approved new respiratory therapy formulations to improve asthma and COPD treatment access.

India Metered Dose Inhalers Market Trends

India is projected to account for nearly 19% of the regional market in 2026, driven by cost-effective inhaler manufacturing and rising pulmonary healthcare demand. The country is emerging as a major production hub for affordable respiratory drug delivery systems. In August 2025, Cipla expanded respiratory therapy production capacity at its Goa facility to support growing inhalation therapy demand across Asia and Africa.

Competitive Landscape

The global metered dose inhalers market structure is moderately consolidated, with leading players including GlaxoSmithKline, AstraZeneca, Teva Pharmaceutical Industries, and Boehringer Ingelheim collectively accounting for a significant share of global revenue. These companies benefit from strong respiratory therapy portfolios, established healthcare distribution networks, and long-standing relationships with hospitals and healthcare providers. Major players continue investing heavily in low-carbon inhaler technologies, connected respiratory monitoring platforms, and advanced respiratory drug delivery devices to strengthen competitive positioning.

Regional and specialized companies such as Cipla, Chiesi Farmaceutici, and Vectura Group are expanding through cost-effective inhaler production, sustainable inhalation systems, and digital respiratory care solutions. Regulatory approvals, propellant transition requirements, and complex inhaler-device integration continue to create barriers for new entrants. However, rising adoption of smart inhalers and connected healthcare platforms is enabling digital health firms and respiratory technology providers to enter the market through software integration and adherence-monitoring partnerships.

Key Industry Developments:

- In October 2025, GSK announced positive phase III data for its next-generation low-carbon Ventolin metered dose inhaler using HFA-152a propellant technology. The company stated that the inhaler could reduce greenhouse gas emissions by approximately 92% per device while maintaining therapeutic equivalence.

- In May 2025, Lupin Limited partnered with Honeywell to integrate Solstice Air propellant technology into next-generation inhalers, supporting lower-emission respiratory treatment systems.

- In May 2026, Chiesi USA, Inc., a global biopharmaceutical company, announced that the U.S. FDA has approved TRIMBOW® (beclomethasone dipropionate/formoterol fumarate/glycopyrrolate) for the maintenance treatment of asthma in adults, available in specified dosage strengths.

- In May 2026, at ATS 2026, GSK presented respiratory research highlighting MDI innovations using low-carbon HFA-152a propellant, showing comparable safety and efficacy to existing inhalers while reducing environmental impact.

- In May 2025, AstraZeneca’s Trixeo Aerosphere received UK approval with a next-generation near-zero GWP propellant. It became the first pMDI medicine using a propellant with 99.9% lower global warming potential than conventional inhaler propellants, supporting COPD treatment with reduced environmental impact.

Companies Covered in Metered Dose Inhalers Market

- GlaxoSmithKline

- AstraZeneca

- Teva Pharmaceutical Industries

- Boehringer Ingelheim

- Cipla

- Novartis

- Chiesi Farmaceutici

- 3M

- Vectura Group

- Lupin Limited

- Glenmark Pharmaceuticals

- AptarGroup

- Propeller Health

- Adherium

Frequently Asked Questions

The global metered dose inhalers market is projected to reach US$15.2 billion in 2026.

Rising asthma and COPD prevalence, growing adoption of smart inhalers, and increasing demand for connected respiratory care drive the market.

The metered dose inhalers market is expected to grow at a CAGR of 5.0% from 2026 to 2033.

Growth opportunities lie in digital respiratory monitoring, low-carbon inhaler technologies, and the expansion of home-based pulmonary care.

GlaxoSmithKline, AstraZeneca, Teva Pharmaceutical Industries, and Boehringer Ingelheim are key players in the metered dose inhalers market.