- Pharmaceuticals

- Meningococcal Vaccines Market

Meningococcal Vaccines Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Meningococcal Vaccines Market by Product (Meningococcal Polysaccharide Vaccine, Meningococcal Conjugate Vaccine, Serogroup B Meningococcal Vaccine), Age Group, Distribution Channel and Regional Analysis from 2025 to 2032

Meningococcal Vaccines Market Share and Trends Analysis

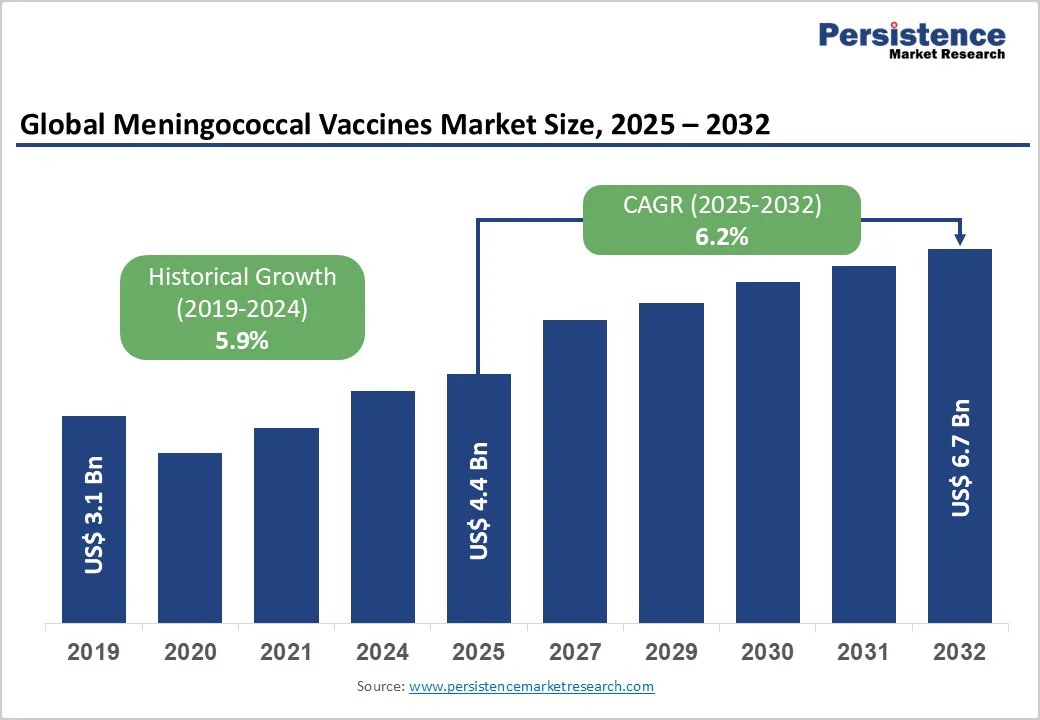

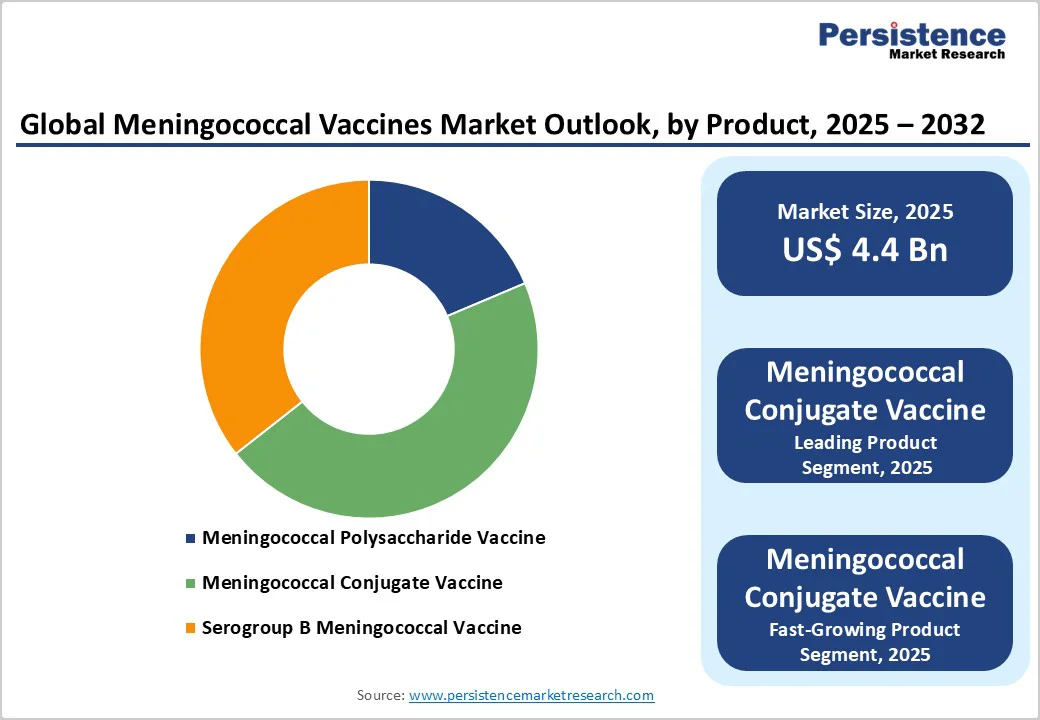

The global meningococcal vaccines market size is likely to value US$ 4.4 billion in 2025 and is projected to reach US$ 6.7 billion by 2032, growing at a CAGR of 6.2% between 2025 and 2032.

Meningococcal vaccinations are administered to prevent infections caused by Neisseria meningitidis, including meningitis, meningococcemia, and septicemia. Highly contagious, meningococcal disease spreads through respiratory and throat secretions and can progress rapidly, with early symptoms often resembling common infections like the flu.

The most common disease-causing serogroups are A, B, C, W, and Y. Although uncommon, meningococcal disease is serious, with up to 10% of patients dying within 24-48 hours even with timely treatment, and 10-20% of survivors suffering long-term disabilities, such as brain damage, hearing loss, or learning impairments. Vaccination remains the most effective preventive measure. Rising incidence and expanded government vaccination programs are driving increased global adoption of meningococcal vaccines.

Key Industry Highlights:

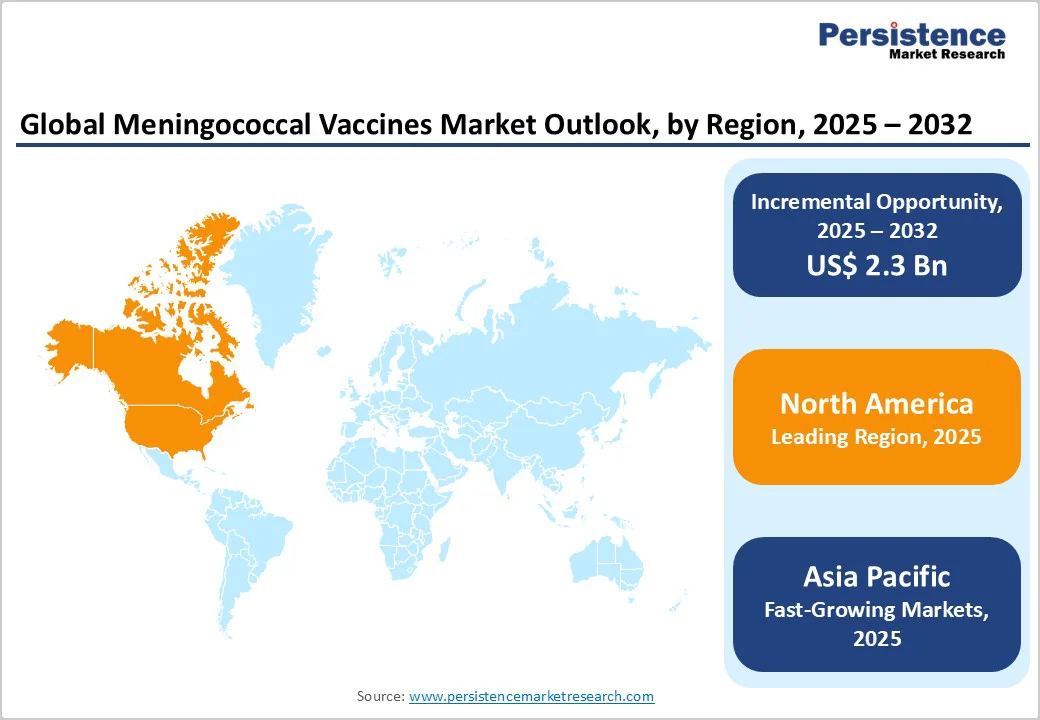

- Leading Region: North America leads due to advanced healthcare infrastructure, high disease awareness, and strong vaccination programs across age groups.

- Fastest-Growing Region: Asia Pacific is expanding rapidly, driven by rising disease awareness, government initiatives, and introduction of novel meningococcal vaccines.

- Leading Product: Meningococcal conjugate vaccines dominate owing to broad serogroup coverage, proven clinical efficacy, and inclusion in routine immunization schedules.

- Leading Age Group: Adolescents and young adults lead because of higher disease prevalence and recent approvals of combination vaccines for this population.

- Increasing government funding and global initiatives are improving vaccine accessibility and coverage in high-risk populations and epidemic-prone regions.

- Clinical trials focusing on immunogenicity, safety, and combination vaccines are attracting investments and driving product innovation in the market.

- Introduction of pentavalent and multivalent vaccines provides broader protection, simplifying immunization schedules and improving vaccination compliance.

| Key Insights | Details |

|---|---|

| Global Meningococcal Vaccines Market Size (2025E) | US$ 4.4 billion |

| Market Value Forecast (2032F) | US$ 6.7 billion |

| Projected Growth (CAGR 2025 to 2032) | 6.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.9% |

Market Dynamics

Driver - Rising Disease Burden, Global Collaborations, and New Vaccine Launches Accelerate Meningococcal Immunization Efforts

Rising incidence of meningococcal disease, estimated at 1.2 million cases and 135,000 deaths globally per year, especially in developing countries is fueling demand for vaccines. Although the disease is rare, meningococcal meningitis carries a mortality rate of 5-15%, and among survivors, one in five suffers permanent harm such as hearing loss, brain damage, limb loss, or seizures.

In response, governments, companies, and non-profit organizations are collaborating more than ever to expand vaccination programs, heighten public awareness of early symptoms, and improve access in underserved regions. For example, global agencies aid procurement, financing, and vaccine prequalification in parts of Africa, spurring greater availability of meningococcal vaccines.

Policy guidance also plays a critical role. The World Health Organization (WHO) recommends that countries with high or intermediate endemic rates conduct large-scale vaccination programmes; specifically, in the African meningitis belt, preventive MenACV campaigns targeting ages 1-29 years and introduction of a routine dose at 9-18 months, with catch-ups for those missed, are urged.

In 2024, GlaxoSmithKline launched a new quadrivalent meningococcal conjugate vaccine with enhanced immunogenicity and competitive pricing, strengthening market expansion in both developed and emerging economies.

Together, these factors-disease burden, public-private collaboration, policy directives, and new product launches-are the primary drivers of growth in the global meningococcal vaccines market.

Restraints - Limited Supply, Low Awareness, and Pricing Barriers Continue to Restrict Global Meningococcal Vaccine Adoption

Despite ongoing vaccination initiatives, several factors continue to restrain the growth of meningococcal vaccine adoption worldwide. A key challenge is the limited global supply and dependence on a small number of manufacturers, which often results in production bottlenecks and regional shortages. In many low- and middle-income countries (LMICs), vaccine accessibility is further constrained by financing limitations and low public awareness, reducing demand even when vaccines are available.

There also remains a large coverage gap between existing and newly developed vaccines, largely due to public apathy and insufficient educational outreach. In addition, differential pricing policies implemented by developing-country governments often restrict market entry for newer and more advanced vaccines, limiting their affordability and penetration.

Although antibiotic treatments exist, meningococcal disease remains severe-10-15% of patients still die, while many survivors experience lasting disabilities such as hearing loss, brain damage, or limb amputation. The persistence of these outcomes underscores the urgent need for stronger awareness, equitable pricing models, and expanded manufacturing capacity to overcome current meningococcal vaccine market restraints.

Opportunity - Global Policy Reforms and Advancing Clinical Trials Create New Opportunities in Meningococcal Vaccine Development

Growing research collaborations, evolving immunization policies, and technological innovation are creating strong opportunities in the meningococcal vaccines landscape. Recognizing the global burden of meningitis, the WHO’s “Defeating Meningitis by 2030” roadmap calls for coordinated global action, improved surveillance, and expanded vaccine access paving the way for long-term market expansion.

In March 2025, the Public Health Agency of Canada (PHAC) updated its National Advisory Committee on Immunization (NACI) guidance, recommending the broader use of quadrivalent conjugate vaccines such as MenQuadfi™ for both primary and booster immunization. Such policy updates across developed markets are expected to strengthen vaccine uptake and encourage innovation.

Simultaneously, several vaccine developers are advancing novel candidates in Asia, signaling new regional growth opportunities. In March 2025, CanSinoBIO initiated a Phase III clinical trial of its Group ACYW135 conjugate vaccine Menhycia® in Indonesia, expanding its target population.

Similarly, in October 2025, Korea’s EYEGENE launched Phase II trials for EG-MCV4, the country’s first homegrown quadrivalent vaccine, developed in collaboration with EuBiologics and BMI Korea. Together, these global policy reforms and R&D milestones are set to open new frontiers for affordable, region-specific meningococcal vaccines.

Category-wise Analysis

By Product: Meningococcal Conjugate Vaccine Leads Due to Broad Serogroup Coverage and Proven Effectiveness

Meningococcal conjugate vaccines are expected to maintain the leading market share of 42.8% in 2025. Their dominance is driven by long-standing clinical experience, high immunogenicity, and the ability to protect against multiple meningococcal serogroups (A, C, W, and Y).

These vaccines are widely recommended across age groups, from infants to adults, due to proven safety and efficacy profiles. Additionally, their inclusion in national immunization programs and ease of integration into routine vaccination schedules further strengthen their adoption, making conjugate vaccines the preferred choice for preventing invasive meningococcal disease globally.

By Age Group: Adolescents and Young Adults Leading Due to High Risk and Expanded Vaccine Approvals

Adolescents and young adults are projected to remain the leading segment in 2025, holding a 32.1% share of the market. This trend is driven by higher meningococcal disease prevalence in this age group and extensive clinical evidence supporting vaccination benefits.

In December 2023, the FDA approved Pfizer’s Penbraya, the first pentavalent vaccine for individuals aged 10-25, offering protection against five major meningococcal serogroups. Broader coverage, simplified immunization schedules, and the potential to prevent severe, life-threatening infections contribute to increased adoption in adolescents and young adults, reinforcing their position as a priority vaccination cohort.

Regional Insights

North America Meningococcal Vaccines Market Trends

The North American landscape is witnessing robust expansion and is projected to capture around 40.7% of the global market share by 2025.

The rise is largely attributed to increasing meningococcal disease incidence in the United States, where 503 confirmed and probable cases were reported in 2024, the highest since 2013, according to the U.S. Centers for Disease Control and Prevention (CDC). This resurgence, exceeding pre-pandemic levels, has reinforced the urgency for broader immunization coverage and next-generation vaccine deployment.

A series of major regulatory and product milestones is further shaping regional growth. In October 2023, the U.S. FDA approved Pfizer’s PENBRAYA™, the first and only pentavalent vaccine covering all five key serogroups (A, B, C, W, and Y), simplifying the adolescent vaccination schedule. The same month, the CDC’s Advisory Committee on Immunization Practices (ACIP) endorsed its inclusion as an alternative to multiple separate shots.

In April 2025, GSK’s 5-in-1 vaccine Penmenvy received a positive ACIP recommendation for individuals aged over 10, streamlining protection and improving compliance rates. Additionally, in May 2025, Sanofi’s MenQuadfi gained FDA approval for infant immunization following trials in over 6,000 participants, broadening protection from early life stages.

With multiple approved conjugate and serogroup B vaccines-Menveo, MenQuadfi, Bexsero, and Trumeau-the U.S. continues to lead in meningococcal vaccine innovation, regulatory advancement, and immunization policy alignment.

Europe Meningococcal Vaccines Market Trends

Europe represents a significant region in the global meningococcal vaccines landscape, projected to hold around 28.3% of the total market share by 2025. Although invasive meningococcal disease (IMD) is rare, it can progress rapidly, with the UK Health Security Agency reporting that nearly 90% of pediatric and adolescent deaths occur within 24 hours of diagnosis.

Vaccination programs have been central to reducing IMD burden across the region. In Germany, since January 2024, the Standing Committee on Vaccination (STIKO) recommended meningococcal serogroup B vaccination for all infants and children under five, with doses at 2, 4, and 12 months, and catch-up vaccinations for older children.

Similarly, in the UK, the routine MenB infant immunization programme was introduced in September 2015 and updated from 1 July 2025 to schedule doses at 8 and 12 weeks, with a booster at the first birthday. Alongside MenB, the introduction of teenage MenACWY vaccination has significantly reduced IMD cases caused by groups C, W, and Y.

Following the withdrawal of COVID-19 population control measures, IMD re-emerged, with MenB accounting for 89% of all cases between September 2021 and August 2024. Disease incidence is highest in infants under two years, peaking at 1-3 months, with a smaller peak around 18 years. Although MenB vaccination provides strong individual protection, it does not prevent bacterial carriage, limiting herd immunity. These trends highlight the continued need for targeted immunization strategies across European populations.

Asia Pacific Meningococcal Vaccines Market Trends

The Asia Pacific market is experiencing rapid growth, with a CAGR of 7.8% projected over the forecast period. Significant developments in vaccination are driving market expansion. In July 2023, the Serum Institute of India Pvt Ltd (SIIPL) achieved WHO prequalification for MenFive®, the first conjugate vaccine protecting against five major meningococcal serogroups (A, C, W, Y, and X).

Developed through a 13-year collaboration with PATH and UK government funding, MenFive® demonstrated high safety and immunogenicity in clinical trials across the Gambia, India, and Mali, and can now be procured by UN agencies and Gavi.

In Vietnam, the VNVC Vaccination Center System introduced MenACYW (Sanofi) on July 4, 2025, marking the first time adults aged 56 and above became eligible for meningococcal vaccination.

This launch responds to growing disease threats, including several cases and two fatalities reported in the first half of 2025, as well as warnings from the Pasteur Institute of Ho Chi Minh City regarding potential outbreaks. Crowded environments, delayed treatment, and asymptomatic carriage among 5-25% of the population complicate disease control, emphasizing the urgent need for widespread vaccination.

Competitive Landscape

The global meningococcal vaccines market is highly consolidated, with key manufacturers emphasizing technological innovation to develop next-generation vaccines. Companies are prioritizing research, clinical advancements, and combination formulations to enhance efficacy, broaden serogroup coverage, and improve immunization schedules, supporting stronger disease prevention and expanding market reach globally.

Key Industry Developments:

- In October 2025, Pfizer presented 46 abstracts at IDWeek 2025 in Atlanta, highlighting advancements across its infectious disease portfolio, including COVID-19, RSV, pneumococcal, Lyme, meningococcal, and other serious bacterial and viral infections.

- In February 2025, the U.S. FDA approved GSK’s Penmenvy, a combination vaccine for individuals aged 10-25, merging components of Bexsero and Menveo to protect against the five most common meningococcal strains.

- In April 2024, Nigeria became the first country to introduce Men5CV, a 5-in-1 meningitis vaccine protecting against A, C, W, Y, and X strains, targeting over one million individuals aged 1-29, recommended by WHO and funded by Gavi, the Vaccine Alliance.

Companies Covered in Meningococcal Vaccines Market

- Pfizer Inc.

- GSK

- Serum Institute of India Pvt. Ltd

- Sanofi Pasteur Inc.

- CansinoBl0

- BIO-MED

Frequently Asked Questions

The global meningococcal vaccines market is projected to be valued at US$ 4.4 billion in 2025.

Rise in meningococcal disease incidence, government vaccination programs, public-private collaborations, and the development of next-generation vaccines drive the global market.

The global meningococcal vaccines market is poised to witness a CAGR of 6.2% between 2025 and 2032.

Expanding immunization policies, novel combination vaccines, clinical trials in emerging markets, and increasing awareness in under-vaccinated populations offer lucrative opportunities.

Major players in the global meningococcal vaccines market are Pfizer Inc., GSK, Serum Institute of India Pvt. Ltd, Sanofi Pasteur Inc., and others.