- Medical Devices

- Knee Reconstruction Devices Market

Knee Reconstruction Devices Market Size, Share, and Growth Forecast 2026 - 2033

Knee Reconstruction Devices Market by Product (Cemented Implants, Cementless Implants, Partial Implants, Revision Implants), Indication (Osteoarthritis, Rheumatoid Arthritis, Trauma, Others), End - User (Hospitals, Ambulatory Surgical Centers, Orthopedic Clinics), by Regional Analysis, 2026 - 2033

Knee Reconstruction Devices Market Size and Trend Analysis

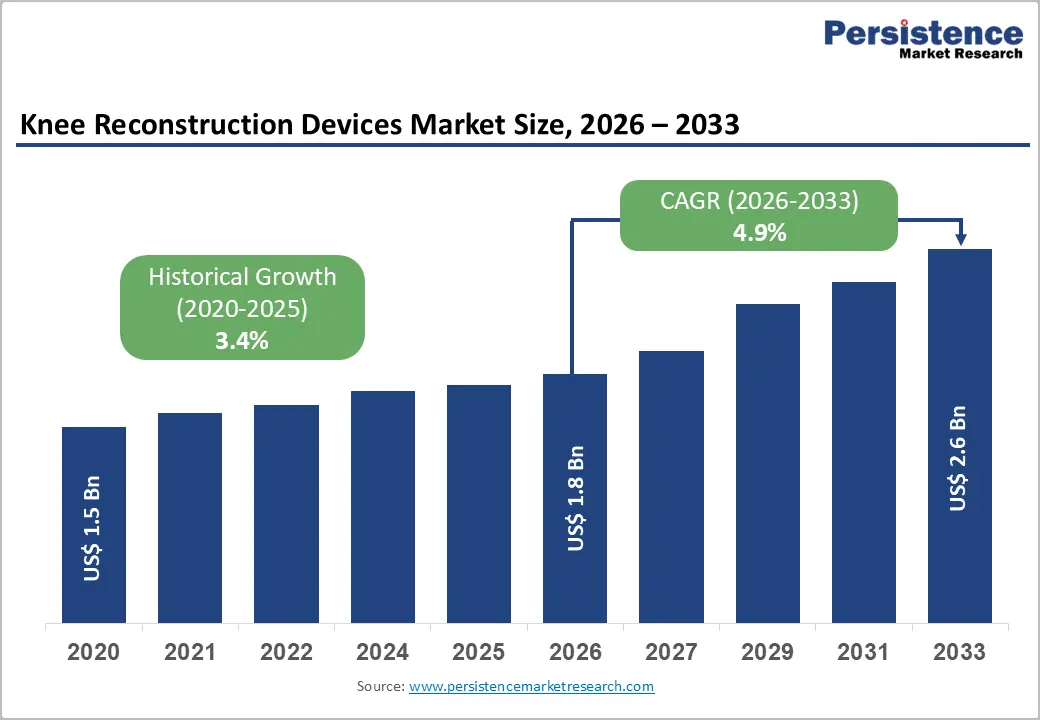

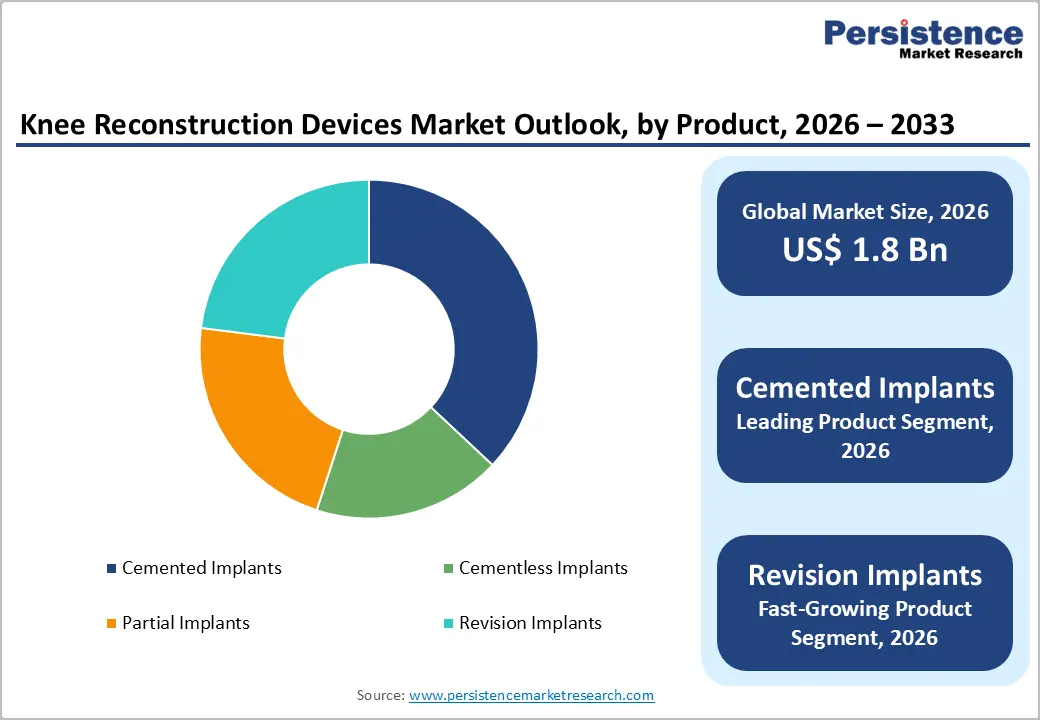

The global knee reconstruction devices market size is expected to be valued at US$ 1.8 billion in 2026 and projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

The market is experiencing steady growth propelled by three converging factors: the rapidly expanding aging global population where approximately 1 in 6 individuals is projected to exceed 60 years old by 2030, substantially increasing osteoarthritis prevalence, with more than 500 million people worldwide currently affected; the demonstrated technological superiority of cementless fixation systems showing comparable or superior long-term survivorship compared to traditional cemented implants while reducing operative time by 7-8 minutes per procedure; and expanding access to ambulatory surgical centers (ASCs) that perform knee replacement procedures at approximately 30-35% lower costs than hospital-based procedures, driving procedure adoption across diverse socioeconomic populations globally.

Key Industry Highlights:

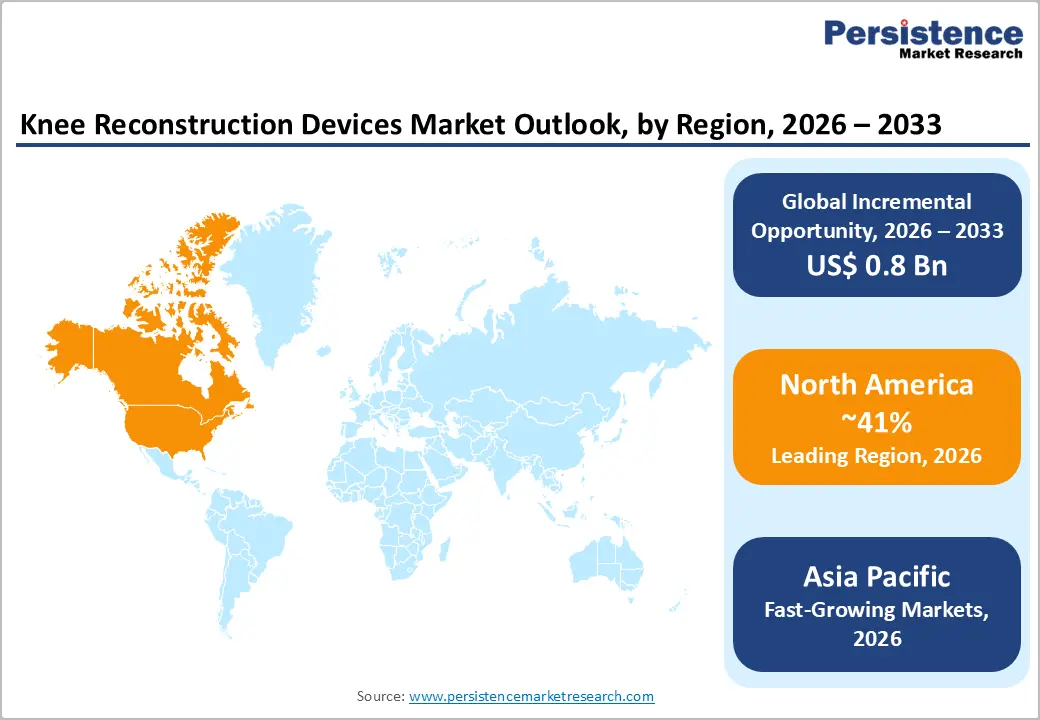

- Leading Region: North America leads with 41% share in 2025, supported by FDA clarity, >600,000 annual knee replacements, advanced infrastructure, 44% robotic-assisted adoption, and Medicare reimbursement boosting ASC volume to 30%.

- Fastest Growing Region: Asia-Pacific grows fastest, driven by China’s 265M aged 60+, India’s 200,000 knee replacements at 60% lower cost, government investments, and rising domestic manufacturing.

- Dominant Segment: Cemented Implants hold 37% of the market, backed by 15-20-year survivorship, 94-98% 10-year survival, surgeon familiarity, and broad product portfolios.

- Fastest Growing Segment: Revision Implants grow fastest, fueled by rising primary knee replacements, longer patient lifespans, and advanced designs for complex anatomies.

| Key Insights | Details |

|---|---|

| Knee Reconstruction Devices Market Size (2026E) | US$ 1.8 billion |

| Market Value Forecast (2033F) | US$ 2.6 billion |

| Projected Growth CAGR (2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 3.4% |

Market Dynamics

Drivers - Rising Prevalence of Osteoarthritis and Demographic Aging Across Global Population

The exponential growth in knee osteoarthritis diagnosis globally represents the primary market driver, with the World Health Organization (WHO) documenting that 344 million individuals currently experience osteoarthritis globally, with approximately 73% of affected patients being older than 55 years. The Arthritis Foundation projects that by 2040, an estimated 78 million adults in the United States will have doctor-diagnosed arthritis, with knee osteoarthritis representing the most prevalent manifestation. This epidemiological shift reflects demographic aging: according to United Nations projections, the 65-plus population will comprise 1.5 billion individuals by 2050, creating unprecedented demand for functional restoration therapies. The American Joint Replacement Registry (AJRR) reported more than 600,000 knee replacement surgeries annually in the United States alone, reflecting robust procedure volume and establishing knee reconstruction as one of the highest-volume surgical procedures globally. These demographic and epidemiological trends directly translate to sustained demand for knee reconstruction devices across developed and developing economies.

Technological Innovation in Implant Design and Robotic-Assisted Surgical Systems

Advanced implant technologies and robot-assisted surgical platforms are revolutionizing knee reconstruction procedures, substantially improving surgical precision and patient outcomes while reducing complications. Robotic-assisted total knee arthroplasty (RA-TKA) has achieved market penetration exceeding 44% of knee replacements in the United States, with projections suggesting 70% of all arthroplasties will incorporate robotic assistance by 2030. Systems including Stryker’s MAKO platform, Zimmer Biomet’s ROSA Knee System, and Smith & Nephew’s CORI system deliver real-time patient-specific surgical guidance, improving component alignment precision to within 0.1 millimeters and 0.1 degrees. Registry data demonstrate that robotically-assisted procedures achieve cumulative percent revision (CPR) rates of 1.9% at 2-4 years compared to 2.2% for conventional TKA, while enabling surgeons to return to normal load-bearing activities within hours rather than days. These technological advances reduce recovery times, complications, and implant revision rates, creating compelling value propositions driving device adoption.

Restraint - High Cost Barriers and Reimbursement Limitations in Emerging Economies

High cost barriers and reimbursement limitations remain a major restraint for the knee reconstruction devices market in emerging economies. Knee replacement and reconstruction procedures involve expensive implants, advanced surgical tools, and skilled orthopedic surgeons, making the overall treatment cost unaffordable for a large portion of the population. In many emerging countries, public healthcare systems provide limited coverage for elective orthopedic surgeries, while private insurance penetration remains low. Reimbursement policies often cover only basic procedures and exclude premium implants, advanced materials, or robotic-assisted techniques, forcing patients to pay significant out-of-pocket expenses. This discourages timely surgical intervention and leads patients to delay or avoid knee reconstruction altogether. Additionally, hospitals in cost-sensitive markets are reluctant to invest in high-priced devices due to uncertain reimbursement and low return on investment. These financial constraints slow the adoption of advanced knee reconstruction technologies and limit overall market growth in emerging economies.

Infection Complications and Post-Operative Revision Risks Associated with Implant Failure

Infection complications and post-operative revision risks associated with implant failure act as significant restraints on the knee reconstruction devices market. Surgical site infections, though relatively infrequent, can lead to prolonged hospital stays, additional treatments, and in severe cases, implant removal. Factors such as patient comorbidities, poor wound healing, and hospital-acquired infections increase the risk, particularly in high-volume or resource-limited settings. Implant failure due to loosening, wear, or misalignment further raises the likelihood of revision surgeries, which are complex, costly, and clinically challenging. These risks create hesitation among patients and surgeons when considering knee reconstruction, especially for younger or high-risk individuals. Concerns over long-term implant durability and post-operative complications also increase regulatory scrutiny and liability risks for manufacturers, thereby slowing adoption and limiting overall market expansion.

Opportunity - Expansion of Cementless Implant Technology and Advanced Surface Coatings for Enhanced Osseointegration

The expansion of cementless implant technology and the development of advanced surface coatings present a significant growth opportunity for the knee reconstruction devices market. Cementless implants, designed to promote natural bone growth into the implant, reduce reliance on bone cement and offer longer-term stability, particularly for younger and more active patients. Innovations in surface coatings, such as porous metals, hydroxyapatite, and bioactive composites, enhance osseointegration, improve implant fixation, and minimize the risk of loosening or failure. These technological advancements not only increase the longevity and performance of knee implants but also appeal to patients seeking durable, minimally invasive solutions. As orthopedic surgeons gain confidence in these innovations and awareness among patients rises, the adoption of cementless and coated implants is expected to accelerate, driving market expansion globally, including in both mature and emerging economies.

Category-wise Analysis

Product Insights

Cemented Implants represent the dominant knee reconstruction device product category with approximately 37% market share in 2025. This leadership position reflects the historical standard-of-care status of cemented fixation in total knee arthroplasty, with decades of established clinical performance and surgeon familiarity. Cemented systems provide exceptional initial stability through polymethylmethacrylate (PMMA) cement interdigitation with bone, enabling immediate load-bearing and proven long-term survivorship exceeding 15-20 years in established registries.

The Australian Orthopaedic Association National Joint Replacement Registry (AOANJRR) and United Kingdom National Joint Registry (UKNJR) document 10-year cumulative survival rates of 94-98% for cemented primary total knee replacements. Zimmer Biomet, Stryker, DePuy Synthes, and Smith & Nephew dominate the cemented implant market through comprehensive product portfolios offering diverse sizing, bearing surface options, and revision specifications.

However, cemented systems face competitive pressure from advancing cementless technology, as surgeons recognize operational efficiency gains and enhanced outcomes with modern cementless designs, particularly in younger, more active patient populations.

End-user Insights

Hospitals constitute the dominant end-user segment, performing approximately 70% of knee replacement procedures and maintaining this position through advanced surgical infrastructure, specialized orthopedic teams, capability for complex revision cases, and established insurance reimbursement frameworks. Hospital-based programs integrate pre-operative assessment, intraoperative surgical support, and post-operative rehabilitation protocols within comprehensive orthopedic departments.

However, ambulatory surgical centers (ASCs) represent the fastest-growing end-user category, expanding through favorable Medicare reimbursement authorization, cost-effectiveness relative to hospital procedures, and patient preference for outpatient recovery.

Orthopedic specialty clinics, particularly in Asia-Pacific regions, represent a distinct and growing end-user segment driven by medical tourism expansion, rising middle-class populations seeking orthopedic care, and government healthcare infrastructure investments. In India, specialized orthopedic clinics perform over 200,000 knee replacements annually, establishing the region as a dominant center for high-volume, cost-efficient procedures. This end-user diversification reflects broader healthcare delivery transformation toward decentralized, efficient surgical models, reducing patient burden while optimizing cost-effectiveness.

Regional Insights

North America Knee Reconstruction Devices Market Trends

North America remains the leading region in the knee reconstruction devices market, driven by a combination of advanced healthcare infrastructure, rising prevalence of osteoarthritis, and a growing geriatric population. The U.S. and Canada benefit from widespread access to skilled orthopedic surgeons, state-of-the-art surgical facilities, and high adoption of innovative technologies such as robotic-assisted surgery and computer-navigated knee replacements. Favorable reimbursement policies and strong insurance coverage further support the uptake of knee reconstruction procedures, including total, partial, and revision surgeries.

Additionally, increasing patient awareness about the benefits of early surgical intervention and minimally invasive techniques is contributing to market growth. Continuous product innovation, such as cementless implants and advanced surface coatings, reinforces North America’s dominance, making it a hub for clinical trials, technology adoption, and overall market leadership in the global knee reconstruction devices landscape.

Asia Pacific Knee Reconstruction Devices Market Trends

The Asia Pacific knee reconstruction devices market is emerging rapidly, fueled by increasing healthcare awareness, improving medical infrastructure, and a growing elderly population prone to osteoarthritis and knee injuries. Countries like China, Japan, India, and South Korea are witnessing higher adoption of knee replacement surgeries due to rising disposable incomes and expanding access to private healthcare facilities. Although the region faces challenges such as high device costs and limited insurance coverage, technological advancements, including minimally invasive procedures, robotic-assisted surgeries, and cementless implants, are gradually gaining acceptance.

Government initiatives to improve orthopedic care, coupled with the entry of global and local device manufacturers, are driving market penetration. As patient awareness and affordability improve, the Asia Pacific region is expected to experience significant growth, making it a key focus for future market expansion in knee reconstruction devices.

Competitive Landscape

The knee reconstruction devices market is witnessing steady growth globally, driven by the rising prevalence of knee osteoarthritis, sports injuries, and an aging population. Advancements in implant design, including cementless and partial knee implants, along with minimally invasive and robotic-assisted surgical techniques, are enhancing patient outcomes and procedure efficiency. Growing awareness about early intervention and improved post-operative rehabilitation is further supporting market expansion.

Key Market Developments

- In April 2025, OSSTEC, a London-based start-up that was transforming joint replacement implants with a novel 3D printing technology, raised £2.5 million in funding. The round was led by specialist DeepTech VC Empirical Ventures, which, due to heightened interest, remained open for additional investment.

Companies Covered in Knee Reconstruction Devices Market

- Zimmer, Inc.

- Stryker Corporation

- DePuy Synthes

- Smith & Nephew

- Corin

- United Orthopedic Corporation

- Arthrex Inc.

- Exactech Inc.

- DJO Global

- Japan Medical Dynamic Marketing

- Tornier Inc.

- B. Braun Melsungen AG,

- Medacta International SA

- LimaCorporate SpA

Frequently Asked Questions

The global knee reconstruction devices market is expected to reach US$ 1.8 billion in 2026, with continued growth toward US$ 2.6 billion by 2033 at a compound annual growth rate of 4.9%, driven by rising osteoarthritis prevalence and demographic aging globally.

The market is driven by two fundamental factors: the exponential rise in knee osteoarthritis affecting more than 500 million people worldwide with 78 million projected cases in the United States by 2040; and technological advances including cementless fixation systems reducing operative time by 7-8 minutes and demonstrating comparable or superior survivorship, plus robotic-assisted procedures achieving 44% adoption rates in United States knee replacements.

North America maintains the dominant regional position with 41% market share in 2025, supported by >600,000 annual knee replacement surgeries, advanced healthcare infrastructure, FDA regulatory clarity, robotic-assisted adoption exceeding 44%, and Medicare reimbursement supporting ambulatory surgical center expansion.

Cementless implant technology expansion and robotic-assisted surgical integration represent exceptional market opportunities, with cementless adoption projected to exceed 50% by 2026-2027 through 3D-printed porous surfaces enabling superior osseointegration, while robotic-assisted procedures projected to comprise 70% of arthroplasties by 2030, creating substantial demand for specialized device optimization.

Key market leaders include Zimmer, Inc., Stryker Corporation, DePuy Synthes, and Smith & Nephew.