- Metals & Minerals

- Kaolin Market

Kaolin Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Kaolin Market by Product Type (Crude Kaolin, Calcined, Hydrous, Air-floated Kaolin, Delaminated, Levigated), End-user (Fiberglass, Ceramics & Sanitarywares, Paints & Coatings, Plastic & Rubber, Paper & Paperboards, Agriculture, Other), and Regional Analysis for 2025 - 2032

Kaolin Market Size and Trend Analysis

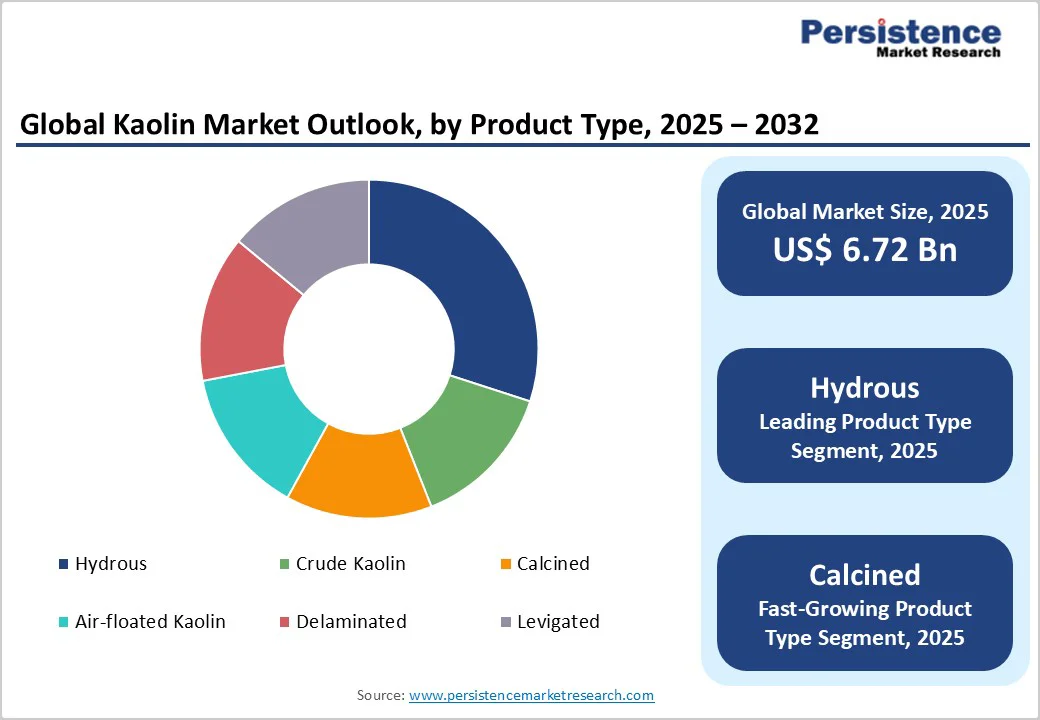

The global Kaolin Market size is valued at US$6.7 billion in 2025 and is projected to reach US$9.4 billion, growing at a CAGR of 4.9% between 2025 and 2032.

The kaolin market's expansion is primarily propelled by surging demand from construction and manufacturing sectors, where its unique properties such as whiteness and plasticity, enhance product quality. This is underpinned by global urbanization rates reaching 2.5% annually as per United Nations data, boosting ceramics and paints applications, while technological improvements in extraction reduce costs and improve yield. Furthermore, sustainability trends favor kaolin over synthetic alternatives, supporting consistent growth across end-uses.

Key Market Highlights

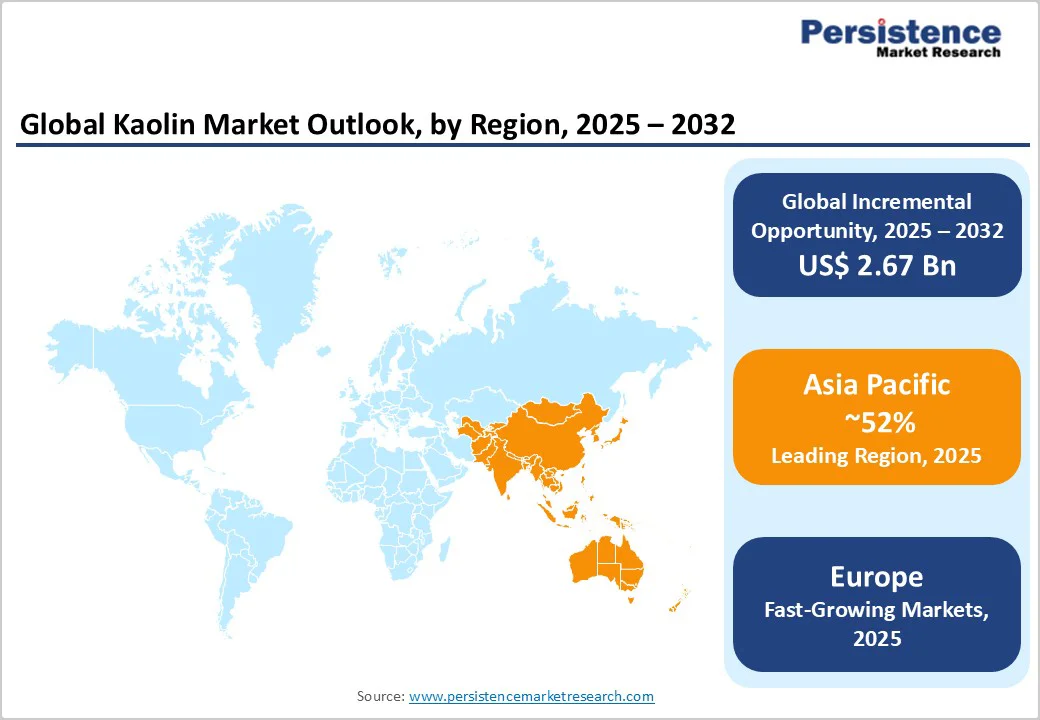

- Regional Leader: Asia Pacific leads the kaolin market with 52% of the market share, driven by manufacturing in China and India, with infrastructure projects boosting ceramics and paints consumption.

- Fastest Growing Region: Europe is the fastest-growing region, achieving 5.3% CAGR from balanced performance in the key countries and growing inter-country trade.

- Leading Segment: Ceramics and Sanitaryware dominate end-use segments with 35% share, propelled by a rise in tile production amid global housing booms.

- Fastest Growing Segment: Paints & Coatings represents the fastest-growing end-use, propelled by 4.3% annual production increases in construction.

- Growth Opportunities: Innovation in fiberglass grades offers key opportunities, improving composites with 18% cost savings for automotive applications.

| Key Insights | Details |

|---|---|

|

Kaolin Market Size (2025E) |

US$6.7 Bn |

|

Market Value Forecast (2032F) |

US$9.4 Bn |

|

Projected Growth CAGR (2025-2032) |

4.9% |

|

Historical Market Growth (2019-2024) |

3.4% |

Market Dynamics

Drivers - Increasing Infrastructure Development Worldwide

The primary driver for the kaolin market is the surging demand from the ceramics and construction industries, particularly in regions undergoing rapid urbanization. Kaolin's high whiteness and plasticity make it essential for producing tiles, sanitaryware, and refractories, with global ceramic production exceeding 1.5 billion square meters annually in key markets like Asia. According to the World Bank, infrastructure investments are set to rise by 5.7% annually in developing regions through 2030, directly correlating with higher kaolin consumption in refractory and glazing applications. This demand is fueled by government initiatives such as India's Smart Cities Mission, which aims to develop 100 smart cities by 2030, directly increasing kaolin consumption for infrastructure projects. This driver enhances market volumes by enabling producers to supply high-purity grades that improve durability and reduce energy use in firing processes, fostering long-term economic contributions in building sectors. Moreover, policies like China's Belt and Road Initiative amplify exports, solidifying kaolin's role in sustainable development.

Surge in Demand for Eco-Friendly Fillers in Paints

The rise in demand for kaolin in the Paints and Coatings Market as a sustainable, non-toxic filler boosts opacity and weather resistance without compromising environmental standards. With global paints production reaching 45 million tons in 2024, kaolin's low oil absorption and fine particle size reduce the need for expensive pigments like titanium dioxide, lowering costs by up to 20% for manufacturers. Industry reports from the International Council of Chemical Associations indicate paint production will grow 4.9% yearly, propelled by residential and commercial renovations amid post-pandemic recovery.

Kaolin's low oil absorption and high brightness allow for formulation efficiencies, cutting costs by 12% compared to titanium dioxide alternatives, which positively impacts profit margins for manufacturers. Eco-friendly coatings, driven by regulations like the EU REACH, are incorporating more kaolin to achieve sustainable performance, thereby convincing stakeholders of its role in market expansion. This trend not only expands market reach but also aligns with global regulations favoring green chemistry.

Restraints - Environmental Compliance Challenges in Mining

Stringent environmental regulations hinder kaolin market growth by complicating mining operations and raising operational expenses through mandatory reclamation and emission controls. In the U.S., the Environmental Protection Agency (EPA) mandates comprehensive land reclamation under the Surface Mining Control and Reclamation Act, adding 10-15% to production expenses through dust control and water management systems. These rules have delayed new mine permits by an average of 2 years, as seen in recent assessments in Georgia's kaolin belt, hindering supply responsiveness to demand spikes.

In India, kaolin operations remain exposed to regulatory restrictions over mining approvals, with suspended operations at facilities like the Kochuveli plant in Kerala due to a shortage of raw materials resulting from pending mining approvals for reserves. Land acquisition challenges, environmental laws, and community resistance constrain expansion opportunities for both local players and foreign investors. These barriers limit new capacity additions, straining supply amid rising demand and potentially inflating prices for end-users.

Quality Inconsistency and Infrastructure Limitations in Key Markets

The kaolin market encounters substantial obstacles related to quality inconsistency in crude kaolin and inadequate infrastructure for processing and transportation. China's kaolin resources, while abundant, consist mainly of sandy kaolin with low grade suitable only for ceramics, bricks, and tiles, with paper-making grade refined kaolin accounting for merely 6% of total reserves, and coating-grade ultra-fine high whiteness calcination kaolin representing only 5% of reserves. This quality disparity necessitates significant capital investment in beneficiation and calcination infrastructure to meet international quality standards.

Logistics and infrastructure limitations, including poor road connectivity to mines and elevated transportation expenses, adversely affect seamless supply chain functioning across major producing regions. The need for chemical agents and specialized processing to reduce viscosity and enhance particle size distribution adds complexity and cost to production, while price competition from imported refined kaolin grades in premium application segments challenges domestic producers seeking to establish a market position in value-added product categories.

Opportunity - Advancements in Sustainable Processing Technologies

A significant opportunity lies in adopting sustainable processing technologies for producing advanced kaolin grades for the Fiberglass Market, where refined particles enhance composite strength and lightweighting in automotive and aerospace sectors. With the International Fibre Association projecting fiberglass demand to grow 6.2% annually through 2032, driven by electric vehicle mandates, kaolin's reinforcing abilities offer cost reductions of 18% over glass fibers alone.

Recent advancements in surface modification technologies, as highlighted in European Ceramic Society journals, improve dispersion and thermal stability, positioning companies to tap into high-value niches. Government incentives for composites in renewable energy further amplify this potential, promising diversified revenue streams. Eco-friendly kaolin grades for sustainable packaging and paper coatings are gaining traction, as demonstrated by Imerys' launch of such products in September 2025 across the U.K. and France markets.

Category-wise Analysis

Product Type Insights

Hydrous Kaolin commands a leading 30% market share in the product type category, attributed to its natural processing advantages and widespread suitability for fillers in ceramics and paper, avoiding the energy-intensive calcination step. In large-scale ceramic tile manufacturing operations, particularly concentrated in India's Morbi district in Gujarat and surrounding areas, hydrous kaolin is extensively used to achieve proper body strength, firing characteristics, and surface whiteness throughout tile and sanitary ware production.

USGS Mineral Commodity Summaries report that hydrous forms constitute the bulk of production due to their high yield from abundant deposits, with global reserves exceeding 5 billion tons, ensuring cost stability and supply reliability. Its water-washed variants deliver superior brightness and rheology, justifying dominance in volume-driven applications where purity meets industry standards without premium pricing. The Rubber Granules Market utilizes hydrous kaolin as a reinforcing filler that enhances strength, durability, and processability, with kaolin's fine particles improving tear resistance, flexibility, and rolling resistance in tire compounds, contributing to better fuel efficiency in vehicles.

End-user Insights

Ceramics & Sanitarywares dominate the end-use category with around 35% market share, driven by kaolin's critical role in achieving high-fired whiteness and structural integrity in tiles and fixtures. This leadership is substantiated by International Ceramic Federation statistics showing kaolin comprising 20-30% of body formulations, enabling 1.2 billion square meters of annual tile output globally.

In sanitaryware, its low thermal expansion prevents cracking during glazing, as evidenced by production data from clusters in India and China, where output rose 12% in 2024. Innovations such as micronized grades have enabled applications in the Feminine Hygiene Product Market, where natural absorbents are preferred, supported by a 10% annual rise in organic product sales per Euromonitor International data. The segment's growth is further supported by urbanization trends, with kaolin enhancing durability in high-volume manufacturing, per USGS Mineral Commodity Summaries.

Regional Insights

North America Kaolin Market Trends

North America, spearheaded by the U.S., exhibits significant growth in the kaolin market through vast reserves in the Southeast, producing over 8 million tons yearly, according to USGS reports, supporting domestic ceramics and paints industries. The regulatory framework under the Clean Water Act ensures sustainable extraction, minimizing environmental impact while fostering an innovation ecosystem with investments in automated processing plants. Recent developments, such as DOE-funded R&D for nano-kaolin, enhance applications in composites, driving efficiency in manufacturing hubs.

Companies investing in environmentally friendly processing technologies and adhering to strict standards gain competitive advantages through certifications related to eco-labeling and sustainability, such as FSC (Forest Stewardship Council) and SFI (Sustainable Forestry Initiative), which influence market positioning and consumer trust. The region's trends emphasize value addition, with companies focusing on air-floated grades for fiberglass, aligning with automotive lightweighting goals and securing supply chains against imports.

Europe Kaolin Market Trends

Europe's kaolin market is characterized by balanced performance across Germany, the U.K., France, and Spain, where harmonized regulations via the EU Industrial Emissions Directive streamline compliance and promote cross-border trade. In Germany, the ceramics sector consumes 500,000 tons annually, with kaolin vital for porcelain exports valued at €2 billion in 2024. Reports from Eurostat highlight a 3.8% rise in construction materials in 2024, underscoring regulatory alignment that boosts efficiency.

Sibelco announced a planned USD 500 million greenfield expansion from 2024 to 2027, aimed at increasing production capacity, including clays to meet anticipated future market growth. Harmonization extends to sustainability, with France and Spain investing in low-emission mining, as seen in recent EEA reports on green extraction, enhancing market resilience and export competitiveness in coatings.

Asia Pacific Kaolin Market Trends

Asia Pacific leads the kaolin market, with 52% of the market share, through dynamic growth in China, Japan, India, and ASEAN, capitalizing on manufacturing prowess and vast deposits for ceramics exports. China's production hit 9.7 million tons in 2024, fueling the world's largest tile market at 8 billion square meters. The country's kaolin reserves reach 49.76 million tons in regions like Longyan and Fujian Province, providing high-quality raw materials for medium and high-grade ceramics with low content of harmful impurities such as iron and titanium. China's infrastructure under 14th Five-Year Plan drives 10% consumption growth, while Japan innovates in electronics fillers.

The India Kaolin Market, with the value of 640.5 Mn, is surging due to Make in India initiatives, with ceramic output rising 7% in 2024 per government data, fueling demand for hydrous grades in tiles. ASEAN's advantages in low-cost processing support automotive rubber applications as ASEAN Secretariat reports indicate, leveraging proximity to end-users for just-in-time supply.

Competitive Landscape

The global kaolin market is moderately fragmented, with top firms holding a small portion of the market share via vertical integration from mining to distribution, enabling cost controls and quality assurance. Expansion strategies include mergers and greenfield projects in Asia, while R&D trends target modified kaolins for pharma, with leaders differentiating through certified sustainability and custom formulations. Companies pursue expansion via strategic acquisitions and joint ventures, such as capacity upgrades in Asia to tap ceramics growth, alongside R&D investments exceeding US$ 200 million annually in particle engineering. Emerging models emphasize B2B partnerships for circular supply chains, mitigating raw material volatility and enhancing adaptability

Key Market Developments:

- October 2025: Ashapura Group launched a new processing plant in India to boost calcined kaolin output for exports, investing $30 million in response to ceramics demand surge.

- July 2024: Imerys S.A. acquired a stake in a U.K.-based kaolin supplier to strengthen European paints supply, focusing on sustainable sourcing amid regulatory changes.

- April 2024: EICL Limited introduced eco-friendly hydrous kaolin for rubber applications, securing contracts in the ASEAN region through enhanced purity standards.

Top Companies in the Kaolin Market

Imerys S.A. (Paris, France) tops the market with extensive global operations and revenue leadership in specialty kaolins, excelling in R&D for high-brightness grades used in paper and coatings; its mature portfolio ensures influence across end-uses.

Thiele Kaolin Company (U.S.A.) commands a strong North American presence through high-volume production and innovation in air-floated products, driving growth in ceramics via reliable supply and technical expertise.

SCR-Sibelco N.V. (Belgium) leverages decades of experience for diversified offerings in refractories and fillers, with portfolio strength in Asia, enabling market expansion and competitive pricing.

Companies Covered in Kaolin Market

- Imerys S.A.

- Ashapura Group

- EICL Limited

- SCR-Sibelco N.V.

- KaMin LLC

- Thiele Kaolin Company

- LASSELSBERGER Group

- Quarzwerke GmbH

- Sedlecký kaolin A.S.

- I-Minerals Inc.

- 20 Microns Limited

- Minotaur Exploration Limited

- W. R. Grace & Co.

- Sibelco Group

- BASF SE

Frequently Asked Questions

The global Kaolin Market will value US$ 6.7 Bn in 2025, reaching US$ 9.4 Bn by 2032 at 4.9% CAGR, supported by infrastructure and manufacturing demands.

Infrastructure development and paint applications are key drivers, with 5.7% annual investments boosting ceramics use and kaolin as an eco-filler.

Hydrous Kaolin leads with 30% share, favored for its cost-effective processing and suitability in high-volume fillers like paper.

Asia Pacific dominates, with growth in China and India driven by manufacturing and 10% consumption increase from infrastructure.

High-performance grades for fiberglass provide opportunities, enhancing composites with 6.2% demand growth in EVs.