- Healthcare Services

- Irradiation Sterilization Services Market

Irradiation Sterilization Services Market Size, Share, and Growth Forecast, 2025 - 2032

Irradiation Sterilization Services Market by Product Type (Gamma Irradiation, X-ray Irradiation, E-beam Irradiation), Application (Medical Instruments, Drug, Food & Laboratory, Others), and Regional Analysis for 2025 - 2032

Irradiation Sterilization Services Market Share and Trends Analysis

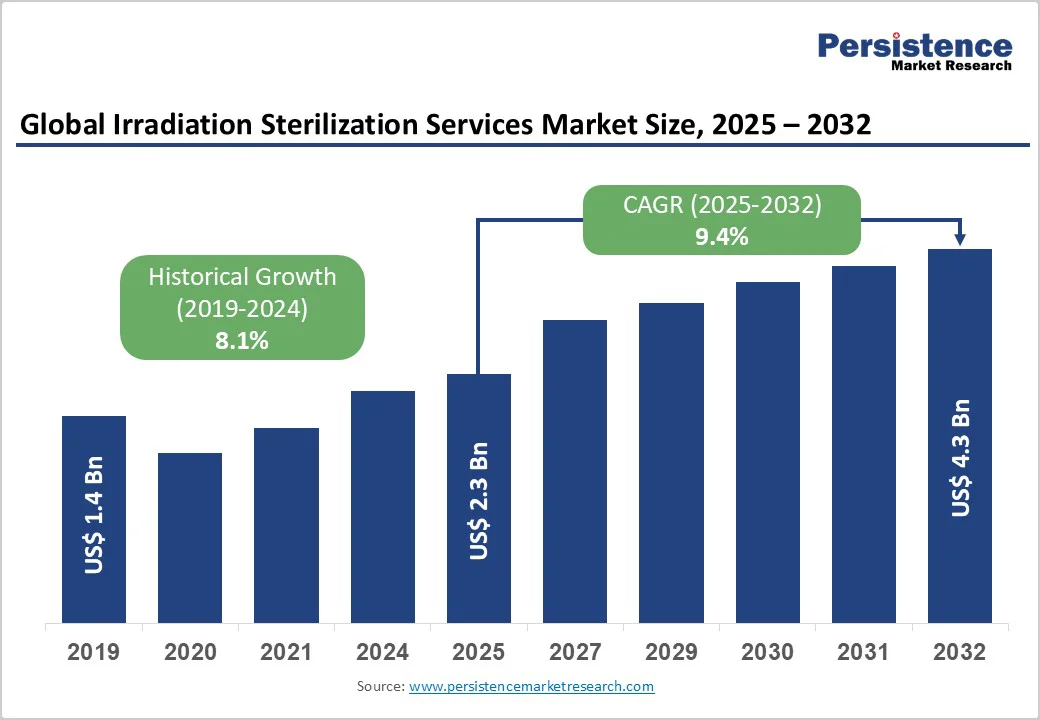

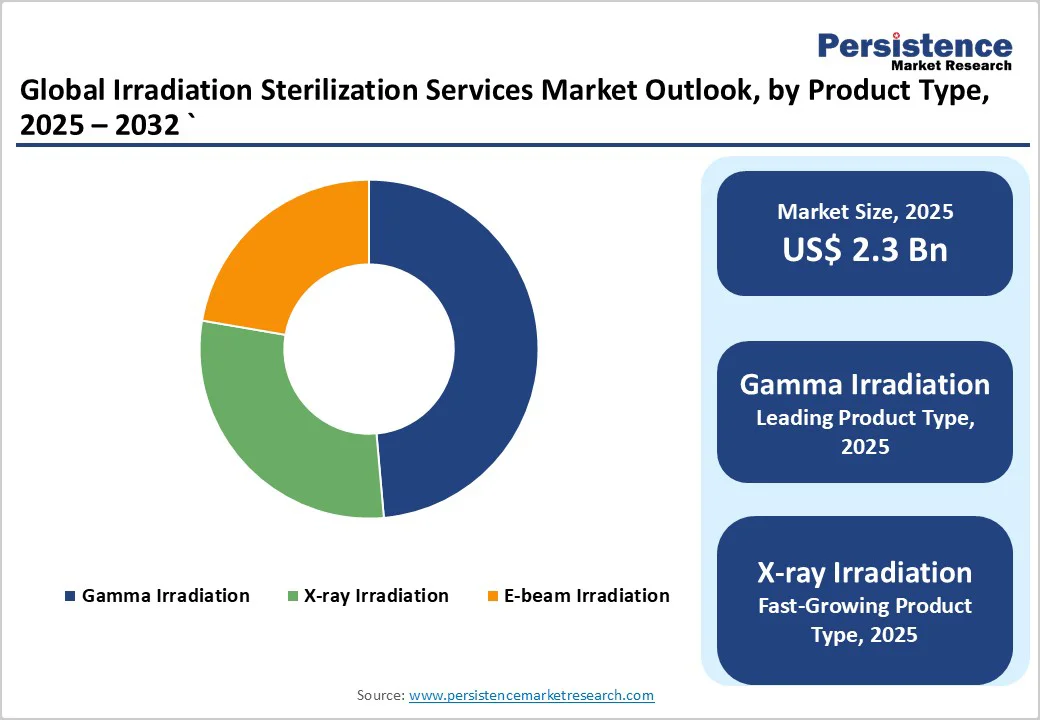

The global irradiation sterilization services market size is likely to be valued at US$2.3 billion in 2025. It is projected to reach US$4.3 billion by 2032, growing at a CAGR of 9.4% during the forecast period 2025-2032.

The market is growing rapidly due to rising demand for safe, effective sterilization of medical devices, pharmaceuticals, and food products. Increasing hospital-acquired infection control measures, advancements in gamma and electron beam technologies, and expanding healthcare infrastructure are driving adoption. Continuous R&D and regulatory support further strengthen market expansion across healthcare and industrial sectors globally.

Key Industry Highlights

- Dominant Product Type: Gamma irradiation, with about 48.6% share in 2025, is dominant due to its deep penetration, reliability, and ISO 11137 compliance.

- Dominant Application: Medical instruments lead, accounting for about 36.3% of the market in 2025, as single-use surgical tools, implants, catheters, and diagnostic kits require precise, validated sterilization.

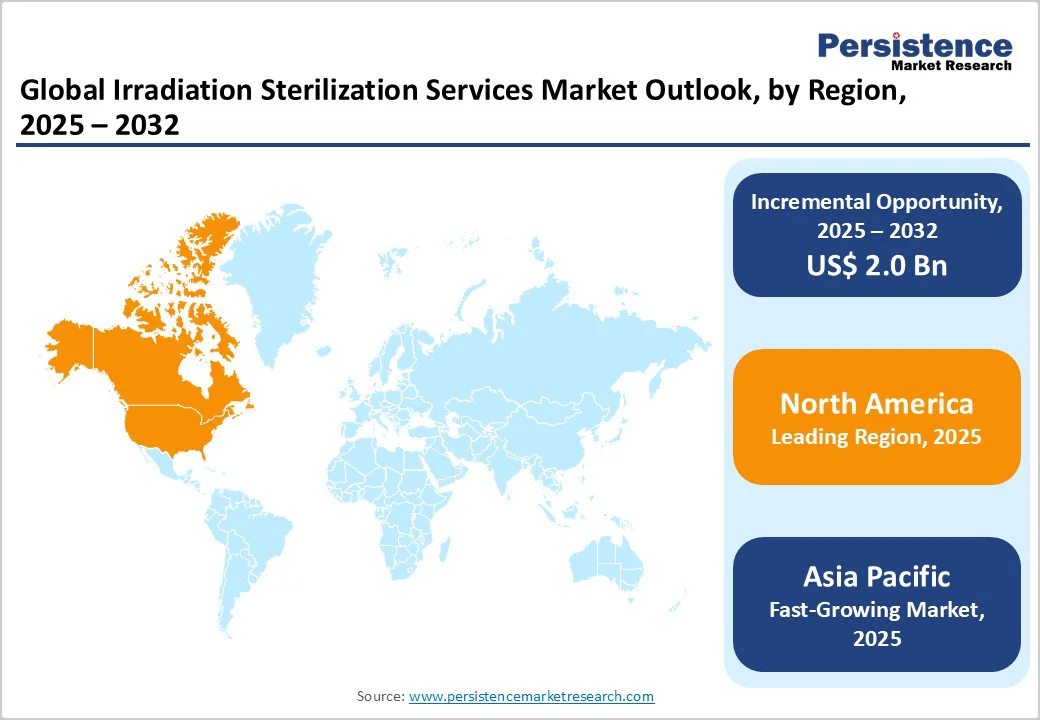

- Dominant Region: North America holds an estimated 41.2% of the market share in 2025, due to the strong presence of major sterilization providers, high medical device manufacturing capacity, and robust regulatory oversight.

- Investment Plans: Asia Pacific is the fastest-growing regional market through 2032, driven by rising contract sterilization partnerships, expanding pharmaceutical and food manufacturing bases, and government investments in healthcare infrastructure.

- Market Drivers: Increasing production of single-use medical devices, stricter infection control norms, and a global shift from chemical to radiation-based sterilization methods are propelling market growth.

- Market Opportunity: Growth opportunities lie in eco-friendly, accelerator-based irradiation systems, automation in dose monitoring and traceability, and regional capacity expansion across emerging economies.

| Key Insights | Details |

|---|---|

|

Irradiation Sterilization Services Market Size (2026E) |

US$2.3 Bn |

|

Market Value Forecast (2033F) |

US$4.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand for Sterilization in Healthcare

The growing need for sterile healthcare environments is a primary driver for the irradiation sterilization services market. Globally, surgical volumes are increasing. The World Health Organization (WHO) reported that over 312 million major operations were performed in 2012, marking a 33% rise compared to previous years. Hospital-acquired infections (HAIs) remain a significant concern, affecting a considerable number of patients in high-income countries and an even larger number of patients in low- and middle-income regions during hospitalization.

This rising surgical workload, combined with stringent infection control requirements, has amplified the demand for reliable sterilization of medical devices, implants, syringes, and diagnostic kits. Irradiation sterilization using gamma, X-ray, and E-beam methods, provides validated, high-capacity sterilization with deep material penetration. Its ability to maintain sterility while preserving device integrity makes it critical for hospitals and contract sterilization facilities, ensuring patient safety and regulatory compliance worldwide.

Regulatory Compliance and Industry Dominance

Regulatory compliance is both a driver and a restraint for the irradiation sterilization services market growth. In the U.S., the Food and Drug Administration (FDA) reports that approximately 50% of all sterile medical devices are sterilized with ethylene oxide (EtO), and has been actively working to promote alternatives to EtO, such as gamma, X-ray, or E-beam. Compliance with standards such as ISO-11137 and AAMI guidance mandates detailed documentation, dose mapping, and sterility assurance validation. Between 2018 and 2022, the U.S. recorded 189 Class?I device recalls, the most severe type, with many linked to sterilization or manufacturing lapses.

These stringent regulatory requirements increase operational costs and create high barriers to entry, limiting smaller providers’ ability to compete. Moreover, industry dominance by established contract sterilization providers reduces flexibility for new entrants, restraining market expansion despite rising demand for irradiation-based sterilization in medical, pharmaceutical, and diagnostic sectors.

Automation and Digital Traceability

Automation and digital traceability present a compelling opportunity for the irradiation sterilization services market. The FDA requires manufacturers of implants or life-sustaining devices to establish traceability systems enabling each batch of finished devices to be traced throughout the distribution chain. This regulatory expectation creates demand for sterilization service providers to integrate automated dose-monitoring systems, digital logs, bar-code tracking, and software validation compliant with the FDA’s Quality System Regulation (21-CFR?820).

Automated systems reduce manual error, enhance audit readiness and speed up recall actions, which is critical in a sector where the sterilization provider must deliver validated, documented sterility assurance. Contract irradiation facilities adopting end-to-end digital traceability stand to differentiate themselves by offering faster, more transparent service and meeting strict regulatory oversight, thus capturing growing demand from device makers pursuing high throughput and compliance.

Category-wise Analysis

Product Type Insights

The gamma irradiation segment held around 48.6% of the market revenue share in 2025, owing to its deep-penetration capability and long-standing industry acceptance. Radiation modalities in total account for roughly 45% of sterilization methods for devices, and gamma still dominates radiation-based approaches. Gamma irradiation enables sterilization of final-packaged products without heat or moisture exposure, reducing the risk of damage to devices, and is compatible with a wide array of materials and densities. As a result of its broad applicability, proven validation frameworks, such as ISO-11137, and product versatility, gamma has emerged as the default product-type-choice in irradiation sterilization services.

Application Insights

The dominance of medical instruments in the irradiation sterilization services market revenue share is driven by the sheer volume of devices requiring validated terminal-sterilization. According to a presentation published by the Food and Drug Administration (FDA), around 40 billion medical devices are sterilized per year globally, with radiation methods, including gamma, covering around 40-% of that total. Furthermore, the WHO estimates that in acute-care hospitals, about 7% of patients in high-income countries and up to 15% in low? and middle-income countries acquire a healthcare-associated infection (HAI), underscoring the critical need for instrument sterilization. Surgical tools, endoscopic devices, implants and catheters, often heat and moisture-sensitive, require irradiation, a validated method that preserves device integrity and meets regulatory sterility assurance. This results in the medical instruments category dominating the application share in irradiation sterilization services.

Regional Insights

North America Irradiation Sterilization Services Market Trends

North America dominates with approximately 41.2% of the irradiation sterilization services market revenue share in 2025, backed by its advanced healthcare infrastructure, high medical device manufacturing capacity, and strict regulatory oversight. The FDA reports that over USD 20 billion worth of medical devices sold annually require sterilization, with approximately 45% using radiation methods such as gamma and E-beam. The region also accounts for roughly 40% of global sterile-device service revenue, reflecting widespread adoption of contract sterilization facilities.

Regulatory requirements under the FDA Quality System Regulation (21 CFR 820) and ISO 11137 require manufacturers to use validated, high-capacity irradiation methods. The concentration of device producers, coupled with stringent sterility standards and high surgical volumes, ensures North America remains the leading market for irradiation sterilization services globally.

Europe Irradiation Sterilization Services Market Trends

Europe is a significant regional market for irradiation sterilization services, driven by its large and mature medical device industry and stringent regulatory environment. The region’s medical device market accounts for over a quarter of the total global revenues, with high volumes of surgical instruments, implants, and diagnostic tools requiring reliable sterilization. Regulations mandate that both single-use and reusable devices undergo validated sterilization processes before use, ensuring patient safety and product integrity. This has created a strong demand for specialized irradiation services, including gamma, X-ray, and E-beam methods. Compliance with international standards for sterility assurance further reinforces the need for professional contract sterilization providers. The combination of high device volumes, regulatory obligations, and established healthcare infrastructure makes Europe an important and stable market for irradiation sterilization services.

Asia Pacific Irradiation Sterilization Services Market Trends

Asia-Pacific is the fastest-growing regional market for irradiation sterilization services due to a gradual increase in investments in healthcare, expanding device manufacturing, and widening use of medical consumables. For example, governments in India and China have significantly increased medical-equipment spending, and Asia now contains over half of the world’s chronic disease burden. Healthcare infrastructure build-out in India, including tens of thousands of new primary health centers, fuels the demand for sterilized devices.

Furthermore, major device-makers are relocating production and packaging into Asia Pacific, increasing volumes of materials needing terminal irradiation. As these markets transition from import-heavy to domestic manufacturing, the demand for contract irradiation services is likely to grow in the coming years. This combination of manufacturing growth, healthcare expansion and rising device sterilization needs makes Asia Pacific the region with the highest growth potential in irradiation sterilization services.

Competitive Landscape

The global irradiation sterilization services market landscape is highly competitive, dominated by key global players offering gamma, X-ray, and E-beam solutions. Leading contract service providers focus on regulatory compliance, high-capacity processing, and advanced traceability systems. Companies differentiate through technological capabilities, geographic reach, and service quality, while smaller regional providers compete on niche applications and cost-effectiveness. Strategic partnerships, facility expansions, and the adoption of eco-friendly irradiation methods further intensify competition across the market.

Key Industry Developments

- In September 2025, STERIS announced that it had completed its facility in Suzhou, China, which now includes X-ray irradiation processing capabilities. The expansion allows the company to offer advanced sterilization services to medical device and pharmaceutical clients in the region, enhancing capacity and compliance with international sterility standards.

- In August 2025, BGS US launched a state-of-the-art E-Beam sterilization facility, expanding its capacity to provide rapid and validated sterilization services for medical devices and pharmaceutical products. The new facility incorporated advanced technology to ensure consistent sterility assurance, compliance with international standards, and high-throughput processing, strengthening BGS US’s position in the North American irradiation sterilization market.

- In May 2025, Sterigenics announced that it had introduced new X-ray sterilization capabilities at its facilities in the Southeast United States. The upgrade enabled the company to provide advanced, high-throughput sterilization services for medical devices and pharmaceutical products, meeting stringent regulatory standards.

Companies Covered in Irradiation Sterilization Services Market

- STERIS

- Röchling Group

- Sterigenics

- Scapa Healthcare

- Swann-Morton

- SteriTek

- Beta-Gamma-Service

- Taisei Kako

- China Biotech Corporation

- Ionisos

Frequently Asked Questions

The global irradiation sterilization services market is projected to reach US$ 2.3 billion in 2025.

Rising medical device demand, strict infection control, regulatory compliance, outsourcing trends, and advancements in gamma, X-ray, and E-beam technologies drive growth.

The market is poised to witness a CAGR of 9.4% between 2025 and 2032.

Expansion of sterilization services in emerging economies, eco-friendly irradiation solutions, automation, digital traceability, and sterilization of biologics and advanced therapies offer key opportunities.

Steris PLC, Röchling Group, Sterigenics, Scapa Healthcare, Swann-Morton, and SteriTek are the key players in the market.