- Medical Devices

- Hernia Mesh Devices Market

Hernia Mesh Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Hernia Mesh Devices Market by Mesh Type (Biological Mesh, Synthetic Mesh), by Hernia Type (Inguinal Hernia, Incisional Hernia, Femoral Hernia, Others), by End User, and Regional Analysis from 2026 to 2033

Hernia Mesh Devices Market Share and Trends Analysis

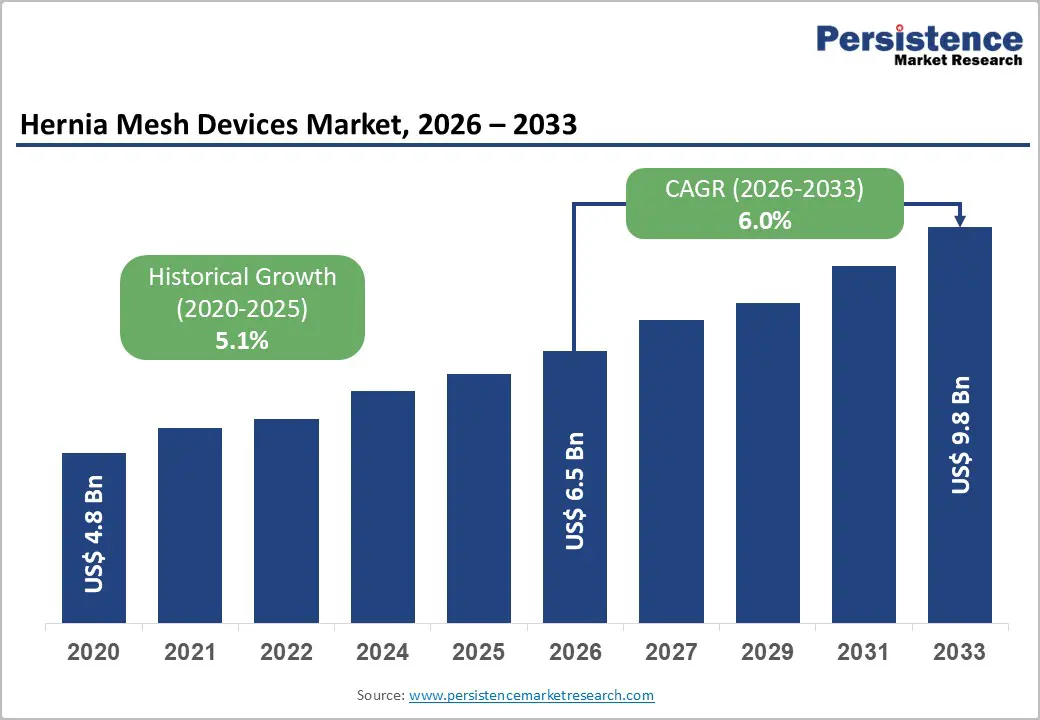

The global hernia mesh devices market is likely to be valued at US$6.5 billion in 2026 to US$9.8 billion by 2033 growing at a CAGR of 6.0% during the forecast period from 2026 to 2033.

The hernia mesh devices market is driven by the rising prevalence of inguinal, ventral, and incisional hernias, the increasing geriatric population, and growing preference for minimally invasive surgical procedures. Hernia mesh products are widely used to reinforce weakened tissue and reduce recurrence rates compared to traditional suturing techniques. Technological advancements such as lightweight, composite, and absorbable meshes are improving patient outcomes and lowering post-operative complications. Additionally, increasing adoption of laparoscopic and robotic-assisted hernia repair, expanding surgical volumes in emerging economies, and favorable reimbursement in developed regions are supporting steady market growth globally.

Key Industry Highlights:

- Surgeons increasingly prefer lightweight and composite meshes due to lower chronic pain, improved flexibility, reduced foreign body reaction, and better long-term patient comfort outcomes.

- Absorbable and biosynthetic meshes are gaining traction in contaminated or high-risk surgeries, as they lower infection risk while providing temporary structural support during tissue regeneration.

- The shift toward outpatient hernia repair in ASCs is boosting demand for easy-to-handle, cost-effective mesh products optimized for shorter surgical durations and rapid patient discharge.

- Leading Mesh Type: Synthetic meshes are significantly cheaper than biological meshes, making them the preferred option for routine and large-volume hernia surgeries globally.

- Leading Region: North America leads due to a large number of inguinal and ventral hernia repairs are performed annually, driven by aging demographics, obesity prevalence, and early diagnosis.

| Key Insights | Details |

|---|---|

| Hernia Mesh Devices Market Size (2026E) | US$6.5 Bn |

| Market Value Forecast (2033F) | US$9.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Dynamics

Driver - Rising Obesity-Linked Abdominal Wall Weakness

Rising obesity levels worldwide are emerging as a critical driver of the hernia mesh devices market, as excess body weight directly contributes to abdominal wall weakness and hernia formation. Obesity increases intra-abdominal pressure, placing continuous mechanical stress on the abdominal muscles and connective tissues. Over time, this pressure weakens natural tissue barriers, making individuals more susceptible to inguinal, ventral, and incisional hernias. Additionally, obese patients often have reduced muscle tone and impaired collagen quality, further compromising the body’s ability to maintain abdominal wall integrity.

From a surgical perspective, obesity significantly increases the complexity of hernia repair. Traditional suture-based techniques are less effective in obese patients due to higher recurrence rates caused by persistent pressure on repaired tissues. As a result, surgeons increasingly rely on mesh reinforcement to provide long-term structural support and evenly distribute mechanical forces across the abdominal wall. Durable synthetic meshes, particularly lightweight and large-pore variants, are preferred to withstand continuous strain while minimizing post-operative discomfort.

Moreover, obesity is frequently associated with comorbidities such as diabetes and cardiovascular disease, which impair wound healing and elevate complication risks. Mesh-based repair helps reduce reoperations and long-term treatment costs in this high-risk population. With global obesity prevalence continuing to rise across both developed and emerging economies, the demand for advanced, high-strength hernia mesh solutions is expected to grow steadily, reinforcing obesity as a sustained and structural market growth driver.

Restraints - Risk of Mesh Infection in Contaminated Surgeries

The risk of mesh infection in contaminated or potentially contaminated surgical fields remains a significant restraint in the hernia mesh devices market, particularly for synthetic mesh products. In cases involving bowel perforation, strangulated hernias, prior infections, or emergency surgeries, the presence of bacteria increases the likelihood of mesh colonization. Synthetic meshes, being non-biological foreign materials, can serve as a surface for bacterial biofilm formation, making infections difficult to treat with antibiotics alone. Once infected, mesh removal is often required, leading to additional surgeries, prolonged hospital stays, and increased healthcare costs.

This risk of infection has made operating surgeons cautious about using synthetic meshes in complex or contaminated procedures, especially in high-risk patient populations such as diabetics, immunocompromised individuals, or elderly patients. As a result, clinicians may opt for biological or biosynthetic meshes, which are designed to integrate with native tissue and allow gradual remodeling, thereby reducing infection susceptibility. However, these alternatives are significantly more expensive and may offer lower long-term mechanical strength, limiting their routine use.

The concern over infection not only impacts product selection but also affects clinical decision-making, surgical timing, and patient counseling. Hospitals and surgeons must balance recurrence prevention against infection risk, often resulting in delayed surgeries or staged repair approaches. This ongoing challenge continues to restrict broader synthetic mesh adoption and drives the need for innovation in infection-resistant materials and antimicrobial mesh technologies.

Opportunity - Continuous Advancements in Sophisticated Mesh Technologies

An opportunistic factor propelling the worldwide market for hernia mesh devices is the ongoing development and innovation of sophisticated mesh technologies. Manufacturers are increasing their investments in research and development to produce mesh devices that exhibit improved patient outcomes, decreased complications, and enhanced biocompatibility as technology advances. Biological and absorbable meshes, among other advanced materials, are becoming increasingly prominent in the marketplace. By progressively being absorbed by the body over time, absorbable meshes reduce the risk of long-term complications and eliminate the need for permanent implantation. By virtue of being derived from human or animal tissues, biologic scaffolds intend to render hernia repair a more organic and unified process.

The advancement of minimally invasive surgical techniques constitutes an additional facet of technological innovation that propels the market for hernia mesh devices. The prevalence of laparoscopic and robotic-assisted hernia repair procedures has increased due to their advantageous characteristics, including reduced pain, shorter recuperation times, smaller incisions, and decreased postoperative complications. The introduction of mesh devices tailored for these minimally invasive procedures is an additional factor driving market expansion. These advancements not only enhance the overall effectiveness of hernia repair but also mitigate issues linked to conventional open surgeries, thereby expanding the treatment options for patients and healthcare practitioners to include personalized and efficient interventions.

Category-wise Analysis

By Mesh Type Insights

Synthetic mesh accounts for the highest share of the hernia mesh devices market primarily because it offers an optimal balance of clinical effectiveness, affordability, and wide applicability across most hernia repair procedures. Synthetic meshes have been used for decades and are supported by extensive clinical evidence demonstrating strong tensile strength, durability, and significantly lower hernia recurrence rates compared to non-mesh repairs. Their predictable performance makes them the standard of care for common hernia types such as inguinal, ventral, and incisional hernias.

Cost is another major factor driving dominance. Synthetic meshes are substantially less expensive than biological meshes, making them more accessible for hospitals, ambulatory surgery centers, and patients, especially in high-volume and cost-sensitive healthcare settings. They are also available in multiple formats, including lightweight, heavyweight, composite, and coated variants, allowing surgeons to select products based on patient condition and surgical technique.

Additionally, synthetic meshes are compatible with open, laparoscopic, and robotic-assisted procedures, further supporting widespread adoption. Favorable reimbursement policies in developed regions and strong manufacturing scalability also contribute to their high market share. In contrast, biological meshes are reserved for specific contaminated or high-risk cases, limiting their overall market penetration despite higher pricing.

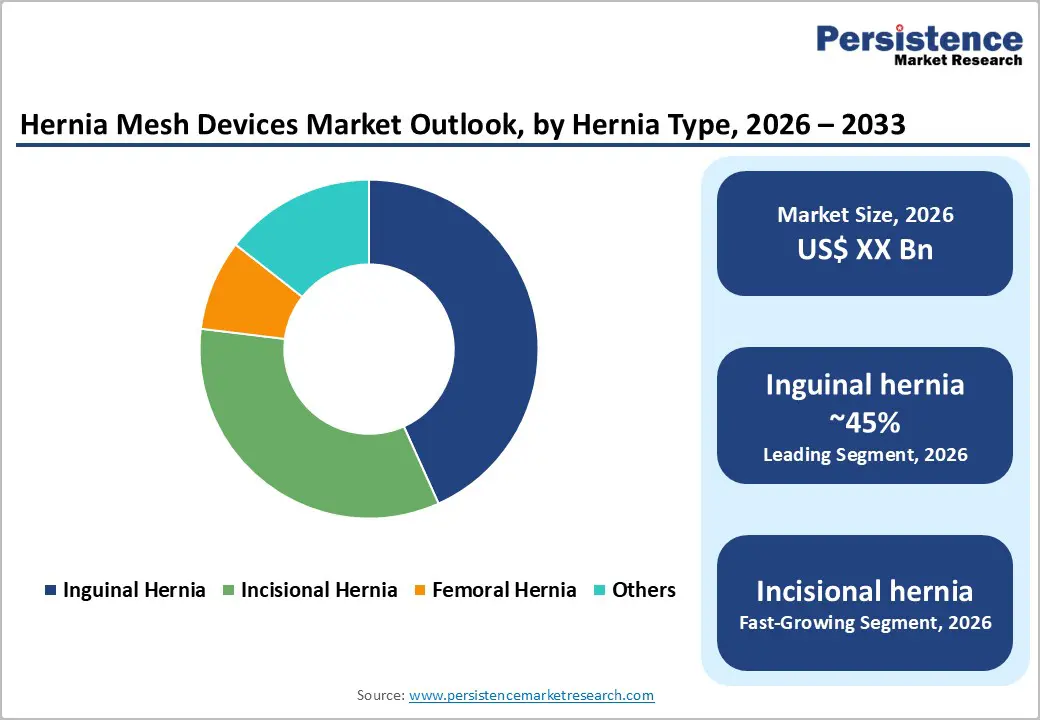

By Hernia Type Insights

Inguinal hernias account for the highest share in the hernia mesh devices market due to their high prevalence and the standardized use of mesh-based repair techniques. Globally, inguinal hernias represent approximately 70-75% of all hernia cases, making them the most frequently encountered type in clinical practice. They occur predominantly in men because of anatomical vulnerabilities in the groin region, though women can also be affected. The high incidence creates substantial demand for surgical interventions, with mesh repair becoming the gold standard.

Synthetic and composite meshes are widely used in inguinal hernia repair because they provide durable reinforcement of the weakened abdominal wall, reduce recurrence rates, and improve long-term patient outcomes compared to traditional suturing techniques. Additionally, inguinal hernia repairs are commonly performed using minimally invasive approaches, such as laparoscopic or robotic-assisted surgery, where mesh placement is critical for effectiveness.

In contrast, other hernia types such as incisional, femoral, umbilical, or epigastric hernias occur less frequently and often have more complex or individualized repair requirements. Incisional hernias arise from prior surgical sites, femoral hernias are rare and mostly seen in women, and “other” hernias contribute minimally to overall procedural volume. The combination of high prevalence, established treatment protocols, procedural volume, and surgeon familiarity ensures that inguinal hernias dominate the hernia mesh devices markett.

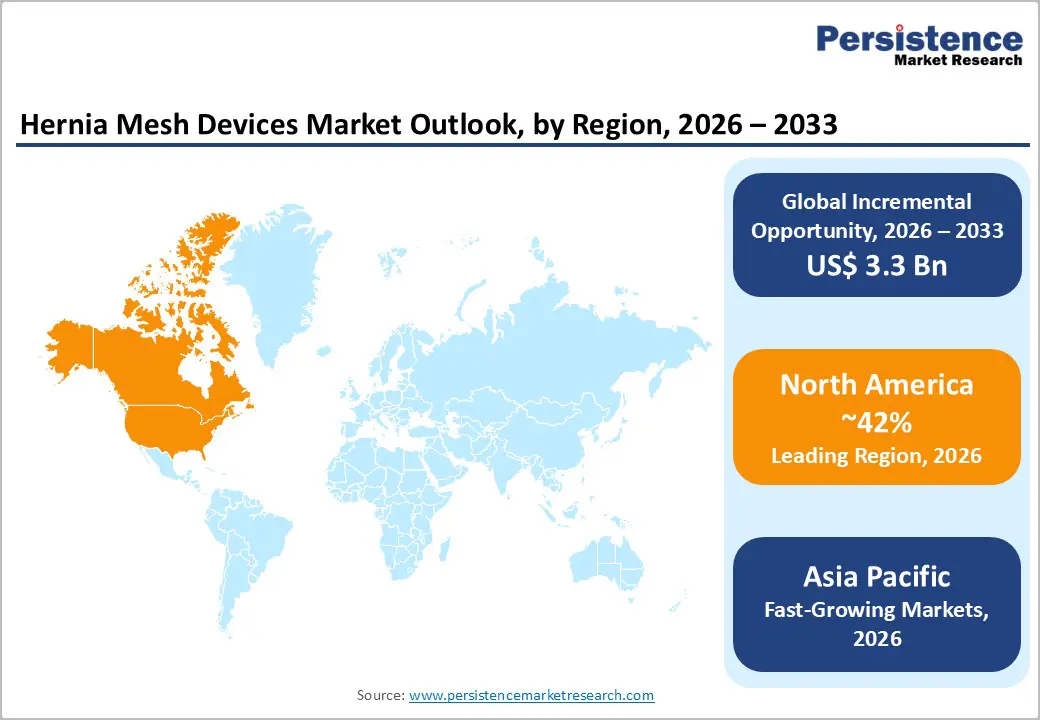

Regional Insights

North America Hernia Mesh Devices Market Trends

North America, led by the United States, remains the dominant region in the hernia mesh devices market due to advanced healthcare infrastructure, high surgical volumes, and strong adoption of innovative mesh technologies. The region benefits from a large aging population, rising obesity rates, and increasing prevalence of inguinal and ventral hernias, all of which drive procedural demand. In the U.S., hernia repair surgeries are among the most common elective procedures, with millions performed annually, providing a steady market for both synthetic and biologic meshes.

Technological advancements, such as lightweight, composite, coated, and absorbable meshes, are rapidly adopted in North American hospitals and ambulatory surgery centers, supported by well-established reimbursement frameworks. Laparoscopic and robotic-assisted hernia repairs are increasingly preferred due to faster recovery times, reduced hospital stays, and improved patient outcomes, further boosting mesh usage. The U.S. also leads in clinical research and innovation, with ongoing trials to develop infection-resistant, anti-adhesion, and anatomically contoured meshes.

Moreover, strong presence of major manufacturers, robust distribution networks, and high surgeon awareness contribute to market growth. Regulatory support and insurance coverage for mesh-based procedures reinforce adoption. Overall, North America’s combination of high procedure volume, advanced technology adoption, and favorable healthcare policies ensures its leading position in the global hernia mesh market.

Asia Pacific Hernia Mesh Devices Market Trends

The Asia Pacific region is emerging as a high-growth market for hernia mesh devices due to increasing healthcare access, rising surgical volumes, and growing awareness of advanced hernia repair techniques. Rapid urbanization, improving hospital infrastructure, and the expansion of specialized surgical centers are driving demand, particularly in countries like China, India, and Japan. The rising prevalence of inguinal, ventral, and incisional hernias, combined with an aging population and increasing obesity rates, is further fueling procedural growth.

Minimally invasive techniques, including laparoscopic and robotic-assisted repairs, are gaining traction, leading to higher adoption of synthetic and composite meshes. Surgeons are increasingly trained in advanced mesh technologies, supported by ongoing clinical education and workshops by leading manufacturers. Although cost sensitivity remains a challenge, expanding medical insurance coverage and government healthcare initiatives are facilitating wider access to hernia repair procedures.

Overall, Asia Pacific’s combination of rising disease prevalence, expanding healthcare infrastructure, and growing adoption of innovative surgical solutions positions it as a key emerging market in the global hernia mesh devices industry.

Competitive Landscape

The hernia mesh devices market is highly competitive, characterized by the presence of global and regional players offering a diverse portfolio of synthetic, composite, and biological meshes. Companies compete through continuous product innovation, introduction of advanced coated and lightweight meshes, and development of minimally invasive surgery-compatible solutions. Strategic initiatives such as mergers, acquisitions, partnerships, and regional expansions are common to strengthen market presence and distribution networks. Strong emphasis on clinical evidence, surgeon training, and post-market support further differentiates competitors.

Key Industry Developments:

- In April 2025, BD received FDA 510(k) clearance for its Phasix ST umbilical hernia patch. The company subsequently initiated the launch of Phasix ST, marking it as the first and only fully absorbable hernia patch specifically designed for umbilical hernias, according to a company news release.

- In October 2025, TI Medical, one of India’s fastest-growing innovators in surgical device solutions, unveiled its next-generation hernia repair mesh, HIPOM, a cutting-edge product designed to enhance surgical precision and patient comfort. The product was launched at an exclusive event at JW Marriott, Kolkata, attended by leading laparoscopic GI surgeons from the region.

Companies Covered in Hernia Mesh Devices Market

- Medtronic plc

- Ethicon

- W. L. Gore and Associates, Inc

- Atrium Medical Technologies

- B. Braun Melsungen AG.

- LifeCell Corporation

- PRIMEQUAL SA

- Becton, Dickinson, and Company

- Deep Blue Medical Inc

- Dipromed Srl

- BioCer Entwicklungs-GmbH

- Others

Frequently Asked Questions

The global hernia mesh devices market is projected to be valued at US$6.5 Bn in 2026.

The increasing incidence of inguinal, ventral, incisional, and femoral hernias worldwide, especially among the aging and obese populations, is fueling surgical demand.

The global hernia mesh devices market is poised to witness a CAGR of 6.0% between 2026 and 2033.

Growing preference for laparoscopic and robotic-assisted hernia repairs increases demand for compatible, easy-to-use mesh devices.

Medtronic plc, Ethicon, B. Braun Melsungen AG., Becton, Dickinson, and Company, and others.