- Medical Devices

- Hemostasis Testing Systems Market

Hemostasis Testing Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Hemostasis Testing Systems Market by Technology (Optical Coagulation, Mechanical Coagulation, Chromogenic Substrate Assays, Immunoturbidimetric Assays, Electromagnetic Coagulation), Application (Coagulation Monitoring, Diagnosis of Bleeding Disorders, Thrombotic Disease Assessment, Surgical Monitoring, Research & Development), End-User (Hospitals & Clinics, Diagnostic Laboratories, Research Institutions, Ambulatory & Home Healthcare), and Regional Analysis for 2026 - 2033

Hemostasis Testing Systems Market Share and Trends Analysis

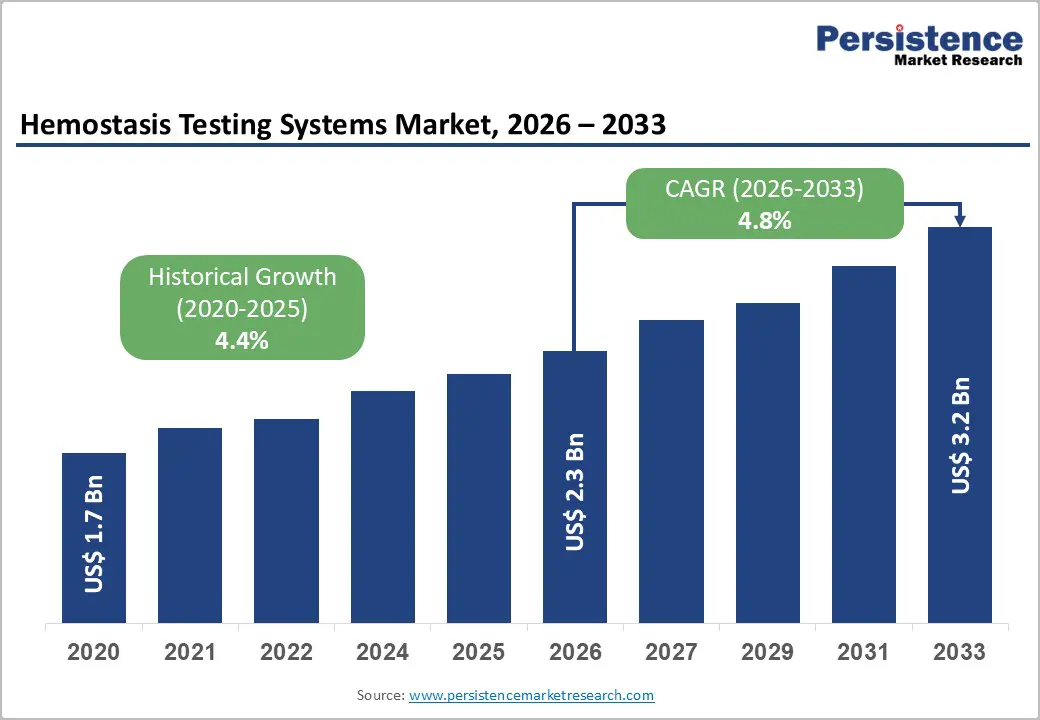

The global hemostasis testing systems market size is likely to be valued at US$ 2.3 billion in 2026, and is projected to reach US$ 3.2 billion by 2033, growing at a CAGR of 4.8% during the forecast period 2026−2033. Market growth is primarily supported by expanding clinical need for coagulation monitoring and increasing incidence of blood-related disorders across aging populations. Healthcare systems continue to strengthen diagnostic infrastructure to enable early identification of bleeding and thrombotic conditions. Hemostasis testing systems support clinicians in evaluating coagulation pathways, monitoring anticoagulant therapy, and managing surgical risk, thereby strengthening demand across hospital laboratories and diagnostic facilities.

Rising awareness of thrombosis, hemophilia, and cardiovascular complications is improving diagnostic adoption within routine clinical pathways. National health agencies such as the U.S. Centers for Disease Control and Prevention (CDC) and the World Health Organization (WHO) emphasize early diagnosis and treatment monitoring for coagulation disorders. Clinical guidelines increasingly incorporate laboratory-based hemostasis testing for treatment planning and patient safety monitoring.

Key Industry Highlights

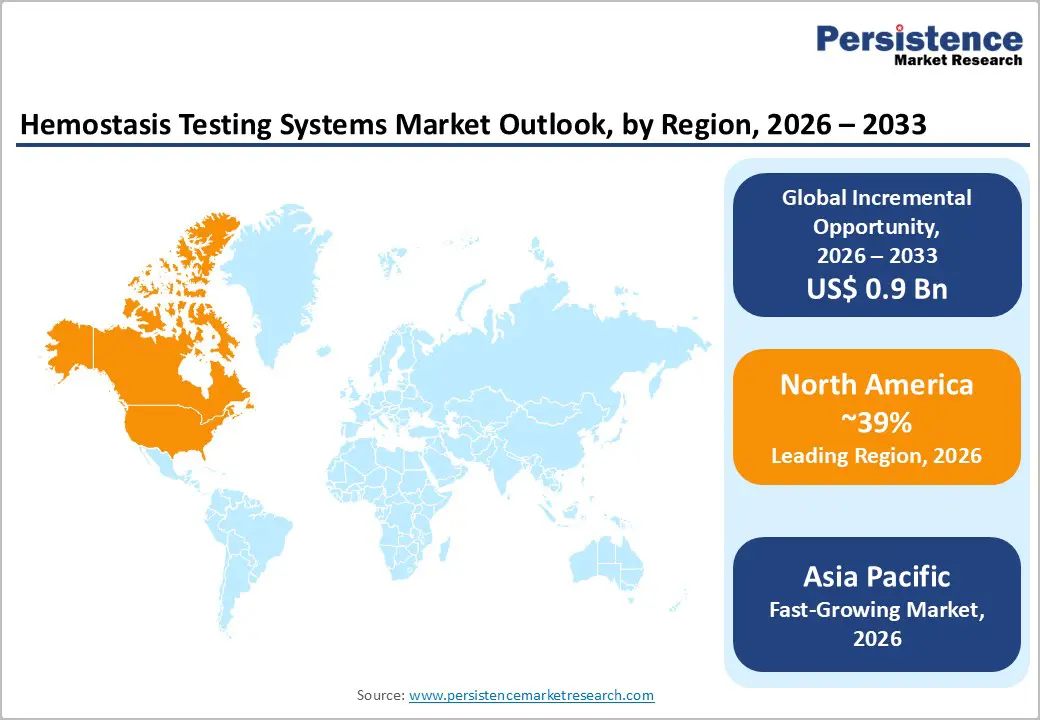

- Dominant Region: North America is projected to hold about 39% share of hemostasis testing systems in 2026, driven by advanced laboratories in the United States and Canada.

- Fastest-growing Regional Market: Asia Pacific is projected to be the fastest-growing market for hemostasis testing systems during 2026–2033, supported by healthcare expansion in China and India.

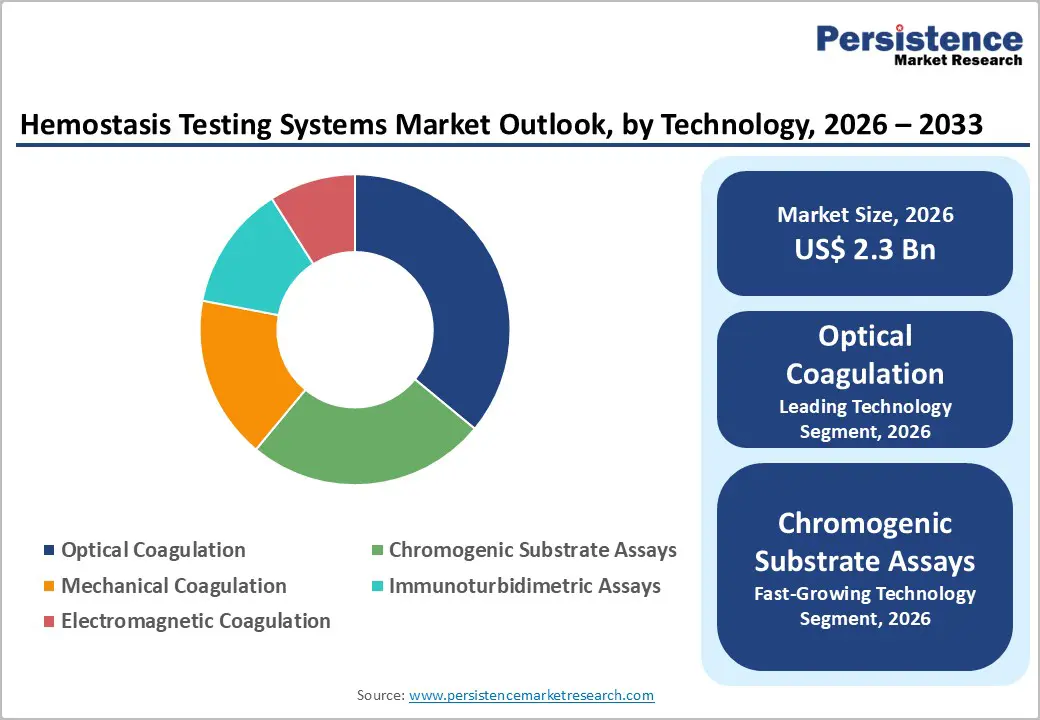

- Leading Technology: Optical coagulation is projected to hold around 36% share in 2026, due to widespread clinical use in laboratories.

- Fastest-growing Technology: Chromogenic substrate assays are projected to be the fastest-growing segment through 2033, supported by an increasing demand for coagulation factor testing.

| Key Insights | Details |

|---|---|

|

Hemostasis Testing Systems Market Size (2026E) |

US$ 2.3 Bn |

|

Market Value Forecast (2033F) |

US$ 3.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Surgical Procedures and Critical Care Diagnostics

Rising surgical volumes across hospitals and ambulatory surgical centers (ASCs) intensify the requirement for accurate coagulation assessment during perioperative care. Major procedures such as cardiovascular interventions, orthopedic reconstruction, trauma management, and organ transplantation involve a high probability of intraoperative or postoperative bleeding complications. Laboratory-based coagulation screening therefore functions as a clinical safeguard that supports preoperative risk evaluation, intraoperative monitoring, and postoperative recovery management. Clinical teams rely on diagnostic coagulation parameters to determine clotting capability, guide transfusion protocols, and evaluate anticoagulant therapy in complex surgical cases. Global health authorities indicate that surgical care represents a large share of healthcare activity, with more than 300 million surgical procedures performed worldwide each year, reflecting extensive reliance on perioperative diagnostic monitoring in modern healthcare systems.

Critical care medicine strengthens demand for coagulation assessment within intensive care units and emergency departments. Severe trauma, sepsis, major burns, and complex cardiovascular conditions often trigger coagulopathy, disseminated intravascular coagulation, or abnormal platelet activity. Continuous laboratory evaluation enables clinicians to detect clotting abnormalities early and implement therapeutic interventions such as anticoagulant adjustment, plasma transfusion, or targeted hemostatic therapy. Intensive care treatment pathways involve frequent monitoring of clotting parameters in mechanically ventilated patients, extracorporeal circulation cases, and post-operative recovery following major surgery. Rising hospital admissions for high-acuity conditions and increasing availability of specialized trauma centers create a clinical environment where rapid coagulation diagnostics support treatment precision and patient stabilization.

Growing Prevalence of Coagulation Disorders and Cardiovascular Diseases

Escalating incidence of coagulation abnormalities and cardiovascular complications is creating sustained clinical demand for diagnostic evaluation of blood clotting mechanisms. Cardiovascular conditions involve thrombotic events such as myocardial infarction, stroke, and venous thromboembolism which require continuous assessment of coagulation pathways during diagnosis, treatment planning, and post-treatment monitoring. Anticoagulant therapies including heparin and oral anticoagulants require routine laboratory monitoring to prevent excessive bleeding or therapeutic failure, increasing reliance on specialized coagulation assays within hospitals and diagnostic laboratories. According to the WHO, cardiovascular diseases caused around 19.8 million deaths worldwide in 2022, representing nearly one-third of global mortality.

Rising prevalence of inherited and acquired coagulation disorders further intensifies the need for laboratory evaluation of clotting function. Conditions such as hemophilia, thrombophilia, liver dysfunction, and disseminated intravascular coagulation influence the balance between clot formation and bleeding risk, requiring precise measurement of parameters including prothrombin time, activated partial thromboplastin time, and platelet function. Growth in complex surgical procedures, organ transplantation, and oncology therapies introduces additional coagulation risks that require continuous perioperative monitoring. Clinical guidelines emphasize early detection of coagulation abnormalities to reduce complications such as hemorrhage, thrombosis, and post-surgical mortality.

High Capital Investment and Laboratory Infrastructure Requirements

Substantial capital allocation for diagnostic instrumentation, automated analyzers, precision reagents, and integrated digital platforms creates a major financial barrier for healthcare institutions. Clinical laboratories require high-throughput analyzers, temperature-controlled reagent storage units, centrifuges, and laboratory information systems to maintain analytical accuracy and regulatory compliance. Budget pressure within public hospitals and small diagnostic centers limits the ability to procure advanced diagnostic infrastructure, particularly in emerging economies where healthcare spending prioritizes emergency and primary care services. Advanced coagulation analyzers frequently require significant acquisition expenditure, specialized consumables, and long-term maintenance contracts, resulting in elevated total ownership cost across the equipment life cycle.

Infrastructure limitations within clinical laboratories further intensify the restraint. Accurate coagulation diagnostics depend on controlled laboratory environments, uninterrupted power supply, temperature regulation, contamination control systems, and trained hematology specialists capable of interpreting complex clotting assays. Many regional hospitals and diagnostic centers lack these structural requirements, leading to reliance on manual or outdated testing approaches with lower throughput and accuracy. According to the U.S. government public health data from the U.S. CDC, up to 900,000 people experience venous thromboembolism annually in the United States, demonstrating the clinical demand for reliable clotting diagnostics and the pressure placed on laboratory systems to support accurate testing infrastructure.

Limited Skilled Workforce and Laboratory Training Gaps

Operational complexity within coagulation diagnostics requires personnel with advanced clinical laboratory competencies, while workforce pipelines for specialized laboratory science remain constrained. Training pathways for medical laboratory technologists require extensive academic preparation in hematology, coagulation pathways, reagent calibration, and analyzer troubleshooting, creating high entry barriers for new professionals. Limited availability of accredited laboratory training programs and restricted clinical training capacity slow workforce expansion across diagnostic institutions. Information from the U.S. Bureau of Labor Statistics (BLS) highlights persistent workforce shortages within clinical laboratory professions. Shortage of qualified personnel reduces laboratory operational efficiency, leading to longer diagnostic turnaround times, restricted laboratory throughput, and underutilization of advanced coagulation analyzers in several healthcare facilities.

Skill intensity of coagulation diagnostics further intensifies laboratory training gaps. Interpretation of clotting assays, calibration of automated analyzers, quality control procedures, and validation of reagents require experienced laboratory scientists with strong clinical exposure. Many healthcare institutions face workforce attrition linked to retirements, while educational pipelines generate limited graduates with specialization in laboratory hematology. Declining numbers of laboratory training programs and restricted awareness of laboratory science careers limit new workforce entry. Workforce shortages increase workload pressure on existing personnel, creating operational strain and restricting adoption of advanced diagnostic platforms.

Integration of Automation and High-Throughput Laboratory Technologies

Rising diagnostic workload in hospitals and reference laboratories is creating pressure for rapid and standardized coagulation analysis, which positions automated and high-throughput laboratory platforms as a major growth opportunity. Conventional manual workflows involve multiple steps such as sample labeling, centrifugation, loading, and verification, which increase operational delays and human-handling risks. Automated laboratory lines integrate barcode tracking, robotic sample preparation, and digital validation systems, enabling continuous processing of large volumes of plasma samples within standardized workflows. High-throughput analyzers further enable laboratories to perform hundreds of coagulation assays per hour, supporting emergency diagnostics, anticoagulant monitoring, and surgical screening without workflow disruption.

Operational transformation across modern diagnostic laboratories is strengthening the opportunity created by automation-enabled high-throughput testing. Robotic processing platforms streamline pre-analytical, analytical, and post-analytical stages through integrated laboratory information systems, minimizing sample misidentification, data entry mistakes, and result variability. Automated laboratories support continuous testing cycles and enable simultaneous processing of thousands of specimens each day, which improves laboratory productivity and supports clinical decision timelines in emergency and critical care settings. A 2025 hospital automation initiative reported that a fully automated pathology laboratory platform processed over 4,000 diagnostic tests per hour, demonstrating the capacity expansion achieved through integrated automation technologies.

Expansion of Diagnostic Infrastructure in Emerging Healthcare Markets

Diagnostic capacity expansion across emerging healthcare systems creates a structural opportunity for advanced laboratory technologies and coagulation assessment solutions. Many developing regions continue to experience limited laboratory penetration, uneven distribution of clinical testing facilities, and delayed disease diagnosis in secondary and rural hospitals. Government health authorities and public health agencies are directing investments toward laboratory modernization, community diagnostic centers, and integrated hospital laboratories to address these gaps. Expanded infrastructure introduces automated analyzers, standardized laboratory workflows, and quality-controlled clinical testing networks, which increases demand for specialized blood analysis platforms used in surgery preparation, trauma care, and chronic disease management.

Improved diagnostic reach across tier-2, tier-3, and rural healthcare systems generates higher testing volumes and broader clinical adoption of laboratory-based screening protocols. Healthcare providers increasingly integrate laboratory testing into preventive medicine, surgical planning, and disease surveillance programs, which increases utilization of coagulation analysis during cardiovascular treatment, oncology therapy monitoring, and emergency care procedures. Infrastructure development further supports integration of digital laboratory information systems, automated sample processing, and centralized diagnostic hubs that connect primary health facilities with tertiary laboratories. These operational networks improve turnaround time and clinical accuracy, encouraging physicians to rely more frequently on laboratory evidence during treatment decisions.

Category-wise Analysis

Technology Insights

Optical coagulation is anticipated to secure around 36% of the hemostasis testing systems market revenue share in 2026, reflecting widespread clinical adoption and established reliability in coagulation diagnostics. Optical coagulation analyzers detect clot formation by measuring changes in light transmission through plasma samples during coagulation reactions. Clinical laboratories widely utilize this technology due to high sensitivity, compatibility with multiple assays, and integration with automated analyzers. Hospitals and diagnostic laboratories prioritize optical coagulation platforms for routine testing of prothrombin time, activated partial thromboplastin time, and fibrinogen levels. The technology supports high-throughput laboratory environments where rapid processing of patient samples is required.

Chromogenic substrate assays are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by increasing demand for specialized coagulation diagnostics and advanced factor analysis. Chromogenic assays measure enzyme activity through colorimetric reactions produced during substrate cleavage. This approach allows accurate evaluation of coagulation factors such as Factor VIII and Factor IX, which are essential for diagnosis and monitoring of hemophilia and other coagulation disorders. Clinical laboratories adopt chromogenic assays to improve diagnostic specificity and treatment monitoring accuracy. These assays support detection of subtle changes in coagulation factor activity that may not be identified through conventional clot-based testing methods.

Application Insights

Coagulation monitoring extracts are poised to dominate with a forecasted market share of over 38% in 2026, powered by extensive clinical use in anticoagulant therapy management and chronic disease treatment pathways. Patients undergoing treatment with anticoagulants require continuous monitoring of coagulation parameters to maintain therapeutic balance and prevent complications. Hemostasis testing systems provide essential diagnostic insights that guide dosage adjustment and treatment planning. Healthcare providers incorporate routine coagulation monitoring into patient management programs for cardiovascular disease, atrial fibrillation, and thrombosis prevention. Laboratory-based testing supports evaluation of clotting time and coagulation factor activity.

Diagnosis of bleeding disorders is estimated to be the fastest-growing segment from 2026 to 2033, fueled by expanding awareness of hereditary and acquired coagulation disorders. Medical organizations including the World Federation of Hemophilia promote early diagnosis and treatment monitoring for patients with bleeding disorders. Diagnostic evaluation through specialized coagulation testing supports identification of factor deficiencies and platelet function abnormalities. Advancement in diagnostic technologies allows laboratories to detect complex coagulation disorders with greater precision. Physicians increasingly utilize laboratory diagnostics to evaluate unexplained bleeding symptoms and inherited coagulation deficiencies. Preventive healthcare initiatives encourage early screening for hematological conditions.

Regional Insights

North America Hemostasis Testing Systems Market Trends

North America is expected to lead with an estimated 39% of the hemostasis testing systems market share in 2026, supported by a dense network of advanced clinical laboratories, high surgical procedure volumes, and strong integration of automated diagnostic technologies across hospital systems in the United States and Canada. Tertiary care hospitals, trauma centers, and cardiovascular institutes across these countries rely heavily on coagulation analysis during pre-operative screening, intraoperative monitoring, and post-surgical management. A major structural driver involves the high number of cardiovascular and orthopedic procedures performed annually, which require accurate clotting assessment to guide treatment protocols and reduce bleeding complications. Widespread anticoagulant therapy among aging populations undergoing treatment for atrial fibrillation, deep vein thrombosis, and pulmonary embolism further increases routine testing volumes.

Another defining factor involves a strong regulatory and clinical governance environment that emphasizes diagnostic accuracy and standardized laboratory operations across healthcare systems in the United States and Canada. Healthcare regulatory authorities and professional pathology organizations promote strict laboratory quality frameworks, encouraging adoption of automated analyzers and advanced reagent systems capable of delivering reproducible diagnostic results. High healthcare expenditure supports continuous investment in laboratory modernization, digital workflow integration, and automation technologies that improve efficiency in diagnostic laboratories. Integration of laboratory information systems with electronic medical records enables rapid reporting and improved clinical decision support across hospital networks. Major diagnostic manufacturers operate research laboratories, manufacturing facilities, and distribution networks across the United States and Canada, enabling rapid commercialization of innovative coagulation assays and analyzer technologies.

Europe Hemostasis Testing Systems Market Trends

Europe represents a well-established healthcare diagnostics market driven by regulatory harmonization and laboratory modernization initiatives. Structured healthcare systems across Germany and France emphasize standardized clinical diagnostics and evidence-based treatment protocols, which encourage routine coagulation assessment during surgical preparation, anticoagulant therapy monitoring, and chronic disease management. Public healthcare funding models support widespread access to hospital-based laboratory services, enabling consistent utilization of diagnostic technologies within tertiary care hospitals and specialized clinical laboratories. Rising prevalence of cardiovascular disease and an aging population profile increase the clinical requirement for regular clotting analysis in patient management programs.

Another defining characteristic involves a strong ecosystem of biomedical research and clinical innovation across the United Kingdom and Italy. Academic medical centers, hematology institutes, and biotechnology laboratories conduct extensive research on thrombosis, hemophilia, and rare bleeding disorders, encouraging development of advanced diagnostic assays and specialized laboratory technologies. Government-supported healthcare investment programs promote modernization of hospital laboratories through digital laboratory information systems, automated sample processing technologies, and centralized diagnostic platforms that improve workflow efficiency. Pharmaceutical research activity in cardiovascular and anticoagulant therapies further stimulates demand for laboratory monitoring during drug development and clinical trials.

Asia Pacific Hemostasis Testing Systems Market Trends

Asia Pacific is forecasted to be the fastest-growing market for hemostasis testing systems between 2026 and 2033, stimulated by rapid healthcare infrastructure expansion, increasing surgical volumes, and rising clinical dependence on laboratory-based coagulation diagnostics across developing healthcare systems. Large population bases and increasing prevalence of cardiovascular and thrombotic disorders are expanding the requirement for routine coagulation monitoring within hospitals and specialized diagnostic laboratories. Healthcare modernization programs are strengthening diagnostic capacity through construction of tertiary hospitals, regional medical centers, and integrated laboratory networks that support higher patient testing volumes. China and India are experiencing significant expansion of hospital infrastructure, diagnostic chains, and government-supported healthcare coverage programs that improve access to laboratory services in both urban and semi-urban areas.

Another key growth catalyst involves strong technology adoption and laboratory automation initiatives within advanced healthcare economies. Japan and South Korea maintain highly developed hospital networks and strong medical technology ecosystems that promote early integration of automated laboratory analyzers and digital diagnostic workflows. Hospitals and academic medical centers across these countries emphasize precision diagnostics and standardized laboratory testing protocols, encouraging consistent utilization of coagulation assessment technologies. Growth in medical tourism across several Asia Pacific healthcare hubs is also increasing demand for sophisticated diagnostic infrastructure capable of supporting cardiovascular surgery, oncology treatment monitoring, and transplant procedures.

Competitive Landscape

The global hemostasis testing systems market structure demonstrates moderate consolidation, with several multinational diagnostic manufacturers controlling a substantial share of technology development, analyzer manufacturing, and reagent supply chains. Major participants such as Siemens Healthcare, F. Hoffmann-La Roche, Sysmex Corporation, and Abbott Laboratories maintain strong competitive positions through vertically integrated diagnostic platforms that combine automated analyzers, proprietary reagents, and digital laboratory software. These companies focus on developing high-throughput coagulation analyzers designed for hospital laboratories and centralized diagnostic centers processing large sample volumes.

Competitive dynamics also involve strategic investment in research and development aimed at improving diagnostic accuracy, workflow efficiency, and test standardization. Major manufacturers increasingly focus on automation technologies that reduce manual intervention and enable laboratories to process higher testing volumes with improved turnaround time. Integration of digital laboratory platforms with electronic medical record systems enhances clinical decision support and strengthens adoption of advanced coagulation testing solutions. Regional diagnostic equipment providers also participate in localized markets by offering cost-competitive analyzers and reagent kits tailored to smaller hospital laboratories and community diagnostic centers.

Key Industry Developments

- In January 2026, Sysmex Corporation introduced the CN-9000 Automated Hemostasis Solution, a high-throughput laboratory system designed to optimize coagulation testing workflows and process up to 1,000 samples per hour in high-volume clinical laboratories.

- In December 2025, Sysmex Corporation announced the launch of the CN-700 Automated Blood Coagulation Analyzer, a compact hemostasis testing system designed to deliver high-precision coagulation analysis and improved workflow efficiency for small and medium-sized medical facilities.

- In March 2025, Werfen announced the commercialization of the ACL TOP Family 70 Series hemostasis testing systems in North America following regulatory clearance, introducing next-generation analyzers designed to improve laboratory workflow efficiency, automation, and connectivity across hospital diagnostic network.

Companies Covered in Hemostasis Testing Systems Market

- Siemens Healthcare Limited

- F. Hoffmann-La Roche Ltd

- Sysmex

- Abbott.

- Danaher Corporation.

- HORIBA Group

- Bio-Rad Laboratories, Inc.

- SEKISUI MEDICAL CO., LTD.

- Helena Laboratories (UK) Limited

Frequently Asked Questions

The global hemostasis testing systems market is projected to reach US$ 2.3 billion in 2026.

Rising prevalence of cardiovascular disorders, increasing surgical procedures, and growing clinical dependence on coagulation diagnostics for anticoagulant therapy monitoring are fueling the demand for hemostasis testing systems.

The market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Expansion of diagnostic laboratory infrastructure, increasing adoption of automated coagulation analyzers, and rising healthcare investment in emerging economies are creating key market opportunities.

Some of the key market players include Siemens Healthcare Limited, F. Hoffmann-La Roche Ltd, Sysmex Corporation, Abbott Laboratories, and Danaher Corporation.