- Home Appliances

- Hangover Cure Market

Hangover Cure Market Size, Share, and Growth Forecast 2026 - 2033

Hangover Cure Market by Product Type (Electrolytes and Vitamins, Herbal Ingredients, NSAIDs, Others), Form (Tablets and Capsules, Liquid, Powder, Patches, Others), by Sales Channel (Online, Offline), and Regional Analysis, 2026 - 2033

Hangover Cure Market Size and Trend Analysis

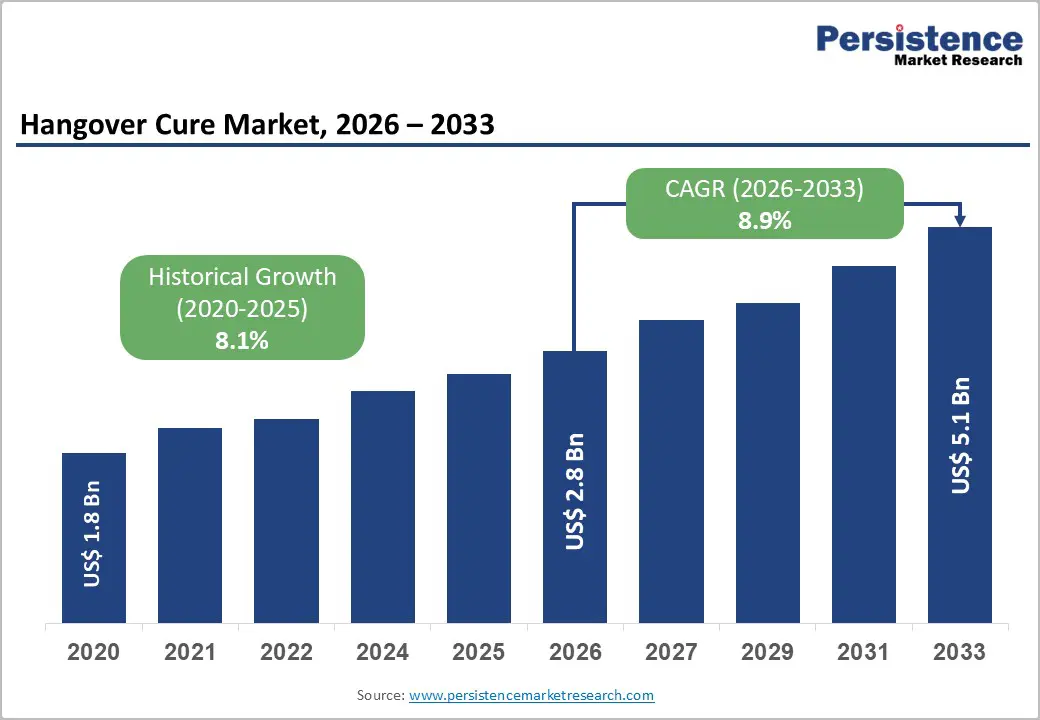

The global Hangover Cure market is likely to be valued at US$ 2.8 billion in 2026 and is expected to reach US$ 5.1 billion by 2033, growing at a CAGR of 8.9% during the forecast period from 2026 to 2033.

This robust double-digit-adjacent growth trajectory is primarily driven by rising global alcohol consumption, shifting millennial and Gen Z consumer attitudes toward proactive wellness recovery, and the rapid proliferation of science-backed nutraceutical and functional supplement products specifically formulated for post-alcohol recovery.

Key Industry Highlights:

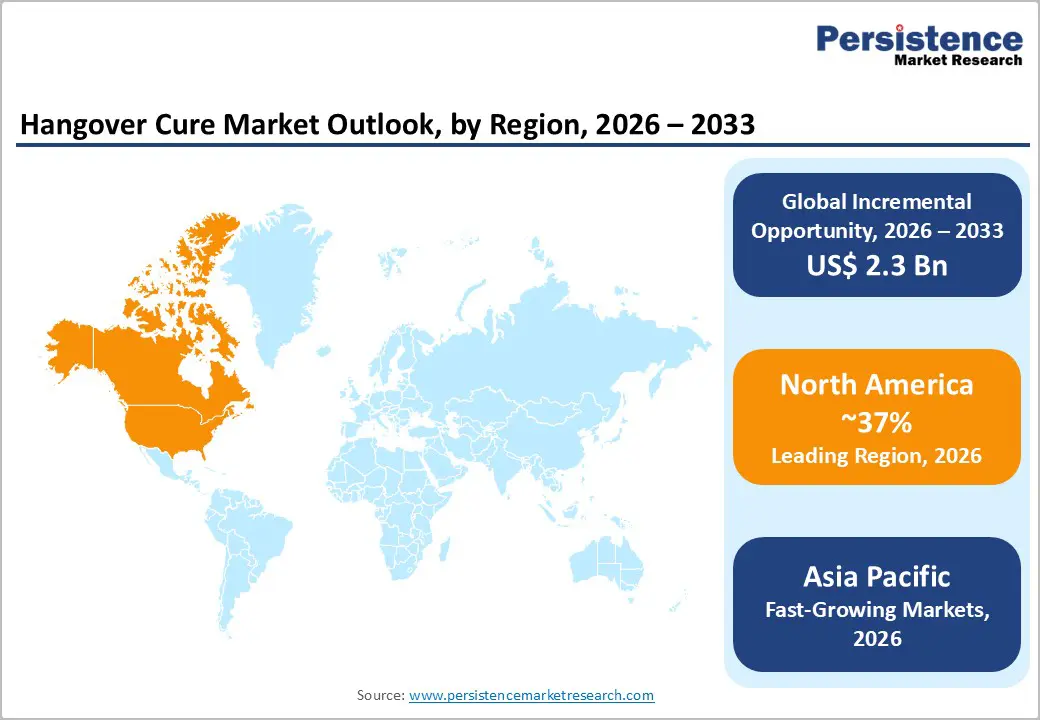

- Leading Region: North America leads the global Hangover Cure market, accounting for 37% share, anchored by the United States' massive alcohol-consuming adult population of approximately 219 million, a permissive dietary supplement regulatory environment under DSHEA, and a highly active DTC innovation ecosystem producing the majority of the world's leading hangover cure brands.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by rising social drinking culture among urban millennials in China, Japan, and India, combined with the Himalaya Wellness Company's established herbal supplement credibility and Japan's decades-old turmeric-based recovery supplement tradition, generating a mature, high-frequency consumer base.

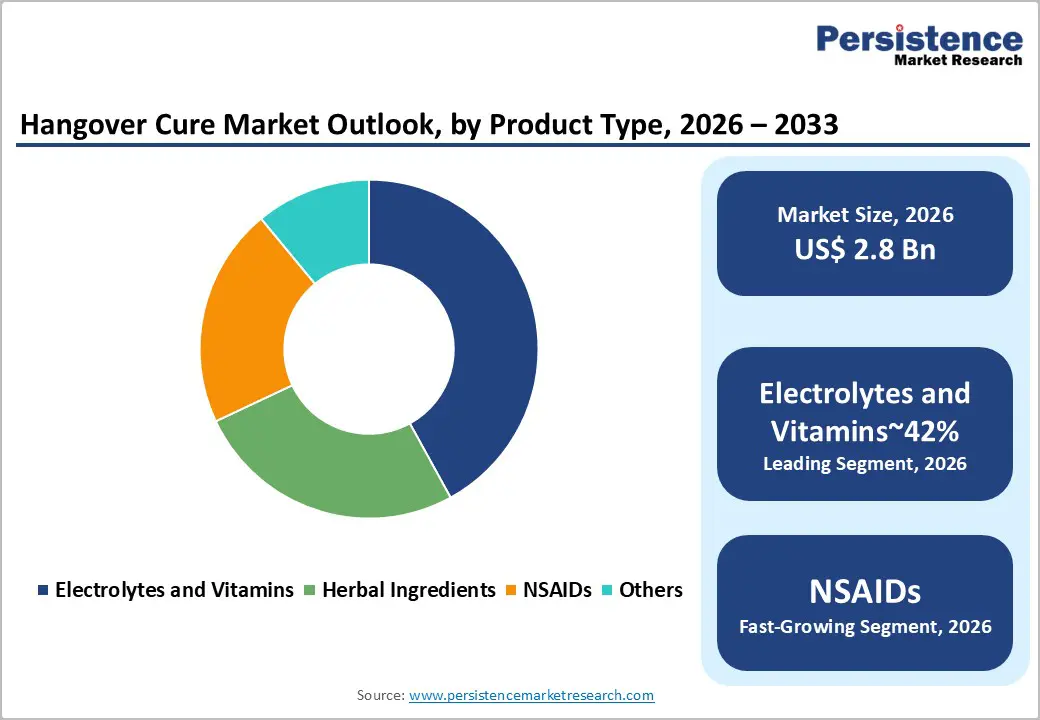

- Leading Segment: The Electrolytes and Vitamins segment dominates the product type category with approximately 42% market share, supported by strong scientific credibility from NIH documentation of alcohol's dehydrating and vitamin-depleting effects, broad consumer familiarity, and the category leadership of brands including Liquid I.V., Inc. and DripDrop Hydration.

- Fastest-Growing Segment: The Online sales channel is the dominant and fastest-growing distribution channel with approximately 58% share, reflecting the digitally native origins of most leading hangover cure brands, growing DTC e-commerce adoption globally, and the critical role of social media platforms, including TikTok and Instagram in consumer discovery and conversion.

- A significant market opportunity lies in premiumization through clinically validated, science-backed formulations featuring ingredients such as DHM and NAC, enabling brands like Cheers Health, Inc. and More Labs to command premium price points of US$ 25–US$ 60 per unit and build differentiated brand equity in an otherwise commoditizing supplement landscape.

| Key Insights | Details |

|---|---|

|

Hangover Cure Market Size (2026E) |

US$ 2.8 Billion |

|

Market Value Forecast (2033F) |

US$ 5.1 Billion |

|

Projected Growth CAGR (2026–2033) |

8.9% |

|

Historical Market Growth (2020–2025) |

8.1% |

Market Dynamics

Drivers - Rising Global Alcohol Consumption and Growing Awareness of Hangover Management Solutions

The primary driver of the global Hangover Cure market is the widespread consumption of alcohol among adults worldwide, combined with a growing willingness to spend on proactive recovery solutions. According to the World Health Organization (WHO), around 2.3 billion people globally consume alcohol, with the highest concentration among adults aged 18–45, an economically active group with strong discretionary spending power.

The National Institute on Alcohol Abuse and Alcoholism (NIAAA) reports that nearly 85% of U.S. adults have consumed alcohol at some point, highlighting the large potential customer base. Social media influence, wellness-focused lifestyles, and targeted digital marketing are transforming hangover recovery from traditional home remedies to branded, science-positioned supplements. Consumers increasingly seek measurable recovery benefits, making hangover management a structured part of modern wellness routines rather than an occasional reactive solution.

Expansion of the Functional Wellness and Nutraceutical Industry Creating Favorable Market Conditions

The Hangover Cure market benefits significantly from its strong alignment with the rapidly expanding functional wellness and nutraceutical industry. Over the past decade, consumer acceptance of dietary supplements has grown substantially. According to the Council for Responsible Nutrition (CRN), 74% of U.S. adults reported using dietary supplements in 2023, marking a record high. Hangover recovery products, often formulated with B-complex vitamins, electrolytes, N-acetyl cysteine (NAC), dihydromyricetin (DHM), and herbal extracts,fit naturally into daily wellness routines. Young consumers increasingly view “morning-after recovery” as part of self-care, rather than a stigma-driven purchase. Expanding availability across pharmacies, health stores, and e-commerce platforms further supports growth. This favorable ecosystem allows hangover brands to scale faster than the broader supplement industry, benefiting from established consumer trust in functional health products and increasing spending on preventive wellness solutions.

Restraint - Lack of Regulatory Approval and Clinical Evidence Validation Concerns

One of the major restraints in the Hangover Cure market is the lack of formal regulatory approval for therapeutic efficacy claims from authorities such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Most hangover cure products are classified as dietary supplements rather than pharmaceutical treatments, which restricts manufacturers from making direct curative claims under FDA regulations. This regulatory limitation affects marketing communication and can reduce consumer confidence.

In addition, while some ingredients show scientific promise, many available clinical studies remain small in scale and lack rigorous methodology. As a result, brands face challenges in obtaining strong medical endorsements or recognized evidence-based claims. These constraints limit premium positioning opportunities and slow mainstream acceptance within healthcare professional communities, impacting the market’s overall credibility.

Social Stigma and Cultural Barriers Limiting Mainstream Consumer Adoption

Despite strong demand fundamentals, the Hangover Cure market faces social and cultural barriers in several major regions. In many Asian, Middle Eastern, and South Asian countries, alcohol consumption is influenced by cultural and religious norms, which can restrict open discussion and retail promotion of hangover recovery products. According to the World Health Organization Global Status Report on Alcohol and Health, abstinence rates are significantly higher in South Asia and MENA regions compared to Western markets.

This reduces the addressable consumer base in highly populated regions and limits large-scale retail penetration. Brands originally developed in North American and European markets often face challenges adapting their marketing approach to culturally sensitive environments. As a result, global expansion strategies require localized positioning, discreet branding, and carefully structured distribution models to overcome these social constraints.

Opportunity - Premiumization and Science-Backed Product Formulation as a High-Value Growth Opportunity

The growing consumer preference for premium, science-backed supplements presents a major opportunity for the Hangover Cure market. Brands that invest in clinically supported ingredients, improved bioavailability, and transparent labeling can differentiate themselves in a competitive environment. Research published in the Journal of Clinical Medicine highlights the potential role of compounds such as dihydromyricetin (DHM) and N-acetyl cysteine (NAC) in supporting liver detoxification and reducing hangover symptoms. Companies including Cheers Health, Inc. and More Labs are investing in clinical research partnerships to strengthen product credibility. This strategy enables premium pricing between US$ 25 and US$ 60 per unit while building long-term consumer trust. Premiumization not only increases average revenue per customer but also supports higher margins and brand loyalty through 2033.

Growth of On-Trade and Festival Economy Driving Impulse Purchase and Point-of-Sale Distribution Opportunities

The strong recovery of nightlife, hospitality, and live events industries is creating new distribution opportunities for hangover cure brands. According to the International Nightlife Association, the global nightlife economy generates over US$ 1.5 trillion annually, largely driven by social drinking activities. This environment creates ideal conditions for impulse purchases of recovery products. Companies such as DOTSHOT and Rally Labs LLC are placing products directly at bars, hotels, and festival venues to capture consumers before or immediately after alcohol consumption. Music festivals, sporting events, and tourism growth further expand visibility and brand exposure. On-trade distribution complements digital sales channels, creating a diversified revenue model that strengthens long-term market growth potential.

Category-wise Insights

Product Type Insights

The Electrolytes and Vitamins segment leads the global Hangover Cure market by product type, accounting for approximately 42% of the total market share. This leadership is driven by strong consumer awareness of electrolyte replenishment and vitamin supplementation as essential wellness practices. Consumers widely understand that alcohol causes dehydration and depletes key nutrients, especially B vitamins, which directly contribute to hangover severity. The National Institutes of Health (NIH) has documented alcohol’s diuretic effects and its interference with the absorption of thiamine (B1), folate, and B12, providing a credible scientific foundation that brands use in their marketing strategies.

Companies such as Liquid I.V., Inc. and DripDrop Hydration have successfully built strong brand loyalty around hydration-focused recovery solutions. Their products serve both everyday hydration needs and post-alcohol recovery occasions, enabling widespread retail presence across pharmacies, supermarkets, and online platforms, which consistently supports high-volume revenue generation within this leading segment.

Form Insights

The liquid form segment dominates the global market by product form, holding approximately 38% of the total share. Liquid recovery solutions, including ready-to-drink shots, drinkable supplements, and dissolvable powder stick packs, offer faster absorption and improved bioavailability compared to tablets or capsules, which require additional digestion time. This rapid action is especially important for consumers seeking immediate relief after alcohol consumption.

The liquid format also naturally aligns with hydration needs, making it intuitive and easy to consume during recovery. Leading brands such as DOTSHOT, More Labs, and Flyby have strengthened their presence through direct-to-consumer e-commerce strategies, while also expanding into bars, pharmacies, and convenience stores to capture both planned and impulse purchases. Additionally, liquid packaging allows strong shelf visibility and clear communication of functional benefits, further reinforcing its leading position within the product form category.

Sales Channel Insights

The online sales channel leads the global hangover cure market accounting for approximately 58% of the total market share. Most hangover cure brands were launched as digitally native direct-to-consumer businesses targeting millennial and Gen Z consumers through advanced digital marketing strategies. As a result, online retail has become the core revenue driver for the industry. Platforms such as Amazon, brand-owned websites, and specialty health e-commerce portals enable companies to reach consumers across multiple regions without heavy investment in traditional retail infrastructure.

Social media platforms, including Instagram, TikTok, and YouTube play a critical role in brand discovery and conversion, with influencer marketing significantly lowering customer acquisition costs. According to the U.S. Census Bureau, e-commerce sales of health and personal care products continue to grow steadily year over year, reinforcing the online channel’s long-term dominance through 2033.

Regional Insights

North America Hangover Cure Trends

North America is the leading regional market for hangover cure products, with the United States serving as the global hub for product innovation, venture capital investment, and brand development. High per-capita alcohol consumption, a strong supplement culture, and an advanced e-commerce infrastructure create favorable conditions for sustained market growth. According to the National Survey on Drug Use and Health (NSDUH), approximately 219.2 million U.S. adults have consumed alcohol in their lifetime, representing a substantial potential customer base. The regulatory framework established under the Dietary Supplement Health and Education Act (DSHEA) of 1994 enables manufacturers to bring products to market without pre-approval, encouraging innovation and rapid brand expansion. Major brands such as Cheers Health, Inc More Labs, Flyby, No Days Wasted, Rally Labs LLC, and Liquid I.V., Inc. have expanded distribution into mainstream retailers, signaling the category’s transition into a recognized wellness segment.

Europe Hangover Cure Market Trends

Europe represents the second-largest regional market for hangover cure products, supported by high alcohol consumption levels and increasing interest in functional wellness supplements. The World Health Organization consistently reports Europe as the region with the highest per-capita alcohol consumption globally, particularly in countries such as Germany, the United Kingdom, France, and the Czech Republic.

The United Kingdom is the most commercially advanced market in the region, benefiting from a vibrant nightlife culture and strong supplement retail networks, including Holland & Barrett and Boots. AfterDrink Ltd. is a notable domestic brand addressing local demand. Regulatory oversight under the European Food Safety Authority framework limits explicit health claims, requiring brands to adopt compliant marketing language. Growing online retail penetration across Southern Europe is further expanding consumer access and supporting steady market growth.

Asia Pacific Hangover Cure Trends

Asia Pacific is the fastest-growing regional market for hangover cure products, driven by rising social drinking trends among urban populations and growing acceptance of functional health supplements. Japan remains the most established market, with a long-standing tradition of “sober-up” drinks, including turmeric-based recovery products. Kowa American Corporation reflects Japan’s structured approach to recovery beverages. In China, expanding urban nightlife and increasing disposable income among young professionals are driving demand, with e-commerce platforms such as Tmall and JD.com serving as primary distribution channels. Regulatory development by the China National Center for Food Safety Risk Assessment is gradually strengthening product standards and consumer confidence. In India, growing urbanization and rising awareness of wellness supplements are creating new opportunities, with Himalaya Wellness Company well-positioned to capitalize on demand for herbal and Ayurvedic recovery formulations.

Competitive Landscape

Key players such as Cheers Health, Inc., More Labs, and Liquid I.V., Inc. differentiate themselves through ingredient transparency, clinical backing, and influencer-led digital campaigns. Larger companies, including Bayer AG and Himalaya Wellness Company, leverage established distribution networks and brand trust to compete in adjacent recovery segments. Subscription models, bundled wellness kits, and hospitality partnerships are emerging as innovative strategies reshaping competition and strengthening long-term customer engagement.

Key Developments:

- In February 2025: Liquid I.V., Inc., owned by Unilever, expanded its functional hydration portfolio by introducing recovery-focused formulations targeting post-alcohol dehydration. The launch strengthens its positioning across mainstream hydration and wellness recovery categories, leveraging retail scale and brand credibility to capture broader consumer demand.

- In August 2024: Cheers Health, Inc. entered a strategic partnership with a major U.S. national pharmacy chain to expand in-store distribution of its science-backed hangover recovery supplements. This move enhances offline visibility, diversifies revenue beyond its strong DTC base, and increases nationwide consumer accessibility.

- In November 2023: No Days Wasted secured a significant Series A funding round to accelerate U.S. and international expansion. The capital supports clinical validation of its DHM-based formulation, strengthens e-commerce infrastructure, and scales influencer-led marketing to penetrate new consumer demographics.

Companies Covered in Hangover Cure Market

- Bayer AG

- Cheers Health, Inc.

- DOTSHOT

- Flyby

- Himalaya Wellness Company

- Purple Tree Labs

- More Labs

- LES Labs

- Morning Fresh

- Rally Labs LLC

- Liquid I.V., Inc. (Unilever)

- No Days Wasted

- DripDrop Hydration

- Drinkwel, LLC

- AfterDrink Ltd.

- Kowa American Corporation

- Toast! Supplements

- Bytox Hangover Patch

- H-PROOF

- Blowfish for Hangovers

Frequently Asked Questions

The global Hangover Cure market is valued at US$ 2.8 billion in 2026 and is projected to reach US$ 5.1 billion by 2033, growing at a CAGR of 8.9% during the forecast period. Historical growth between 2020 and 2025 was recorded at a strong CAGR of 8.1%, underpinned by rising functional supplement adoption, growing health-conscious social drinking behaviors, and the rapid proliferation of digitally native DTC hangover recovery brands globally.

The primary growth drivers are the large and growing global alcohol-consuming adult population, estimated by the WHO at approximately 2.3 billion people, combined with rapidly rising consumer willingness to invest in science-backed nutraceutical recovery products. The Council for Responsible Nutrition (CRN) reports that 74% of U.S. adults use dietary supplements underscores the favorable behavioral foundation for hangover cure adoption, further accelerated by social media marketing, DTC e-commerce expansion, and increasing retail channel accessibility across major consumer markets.

The Electrolytes and Vitamins segment leads with approximately 42% product type market share. Its dominance is driven by the NIH-documented physiological rationale for electrolyte replenishment and B-vitamin restoration following alcohol consumption, broad consumer familiarity with hydration and vitamin supplementation as wellness behaviors, and the commercial success of leading brands including Liquid I.V., Inc. and DripDrop Hydration that have built mainstream consumer franchises around electrolyte-forward recovery formulations.

North America, led by the United States, is the dominant regional market. With approximately 219 million American adults reporting lifetime alcohol use and the U.S. FDA's DSHEA framework enabling rapid dietary supplement market entry without pre-market approval, the region has fostered the world's densest ecosystem of hangover cure brands. Companies including Cheers Health, Inc., More Labs, Flyby, Liquid I.V., Inc., and No Days Wasted are headquartered in the United States, reinforcing its global commercial leadership in this category.

The most significant opportunity lies in premiumization through clinically validated formulations featuring active ingredients such as dihydromyricetin (DHM) and N-acetyl cysteine (NAC), enabling brands to position hangover cure products as evidence-backed wellness solutions at premium price points of US$ 25–US$ 60 per unit. Investment in clinical research partnerships and ingredient transparency, as demonstrated by Cheers Health, Inc. and More Labs, builds differentiated brand equity that supports superior pricing power and long-term consumer loyalty in an increasingly competitive category.