- Medical Devices

- Hadron Therapy Market

Hadron Therapy Market Size, Share, and Growth Forecast 2026 - 2033

Hadron Therapy Market by Therapy Type (Proton Beam Therapy, Carbon Ion Therapy, Others), Application (Prostate Cancer, Pediatric Cancer, Lung Cancer, Head & Neck Cancer, Bone & Soft Tissue Cancer, Others), by End User (Hospitals, Cancer Treatment Centers, Research & Academic Institutes), by Regional Analysis, 2026-2033

Hadron Therapy Market Share and Trends Analysis

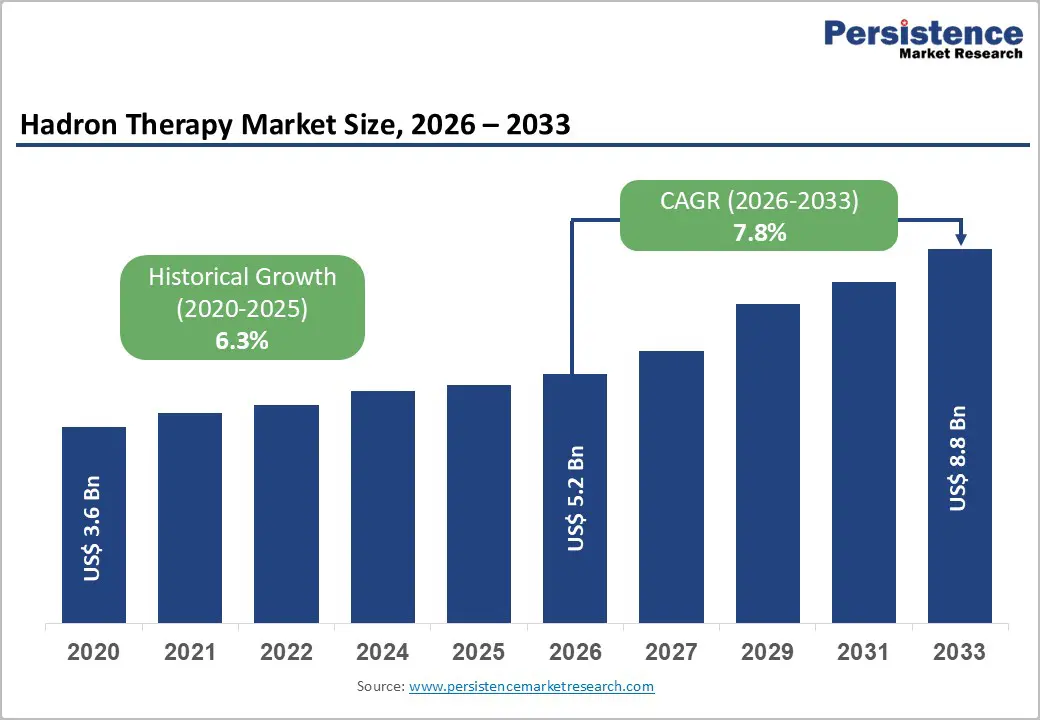

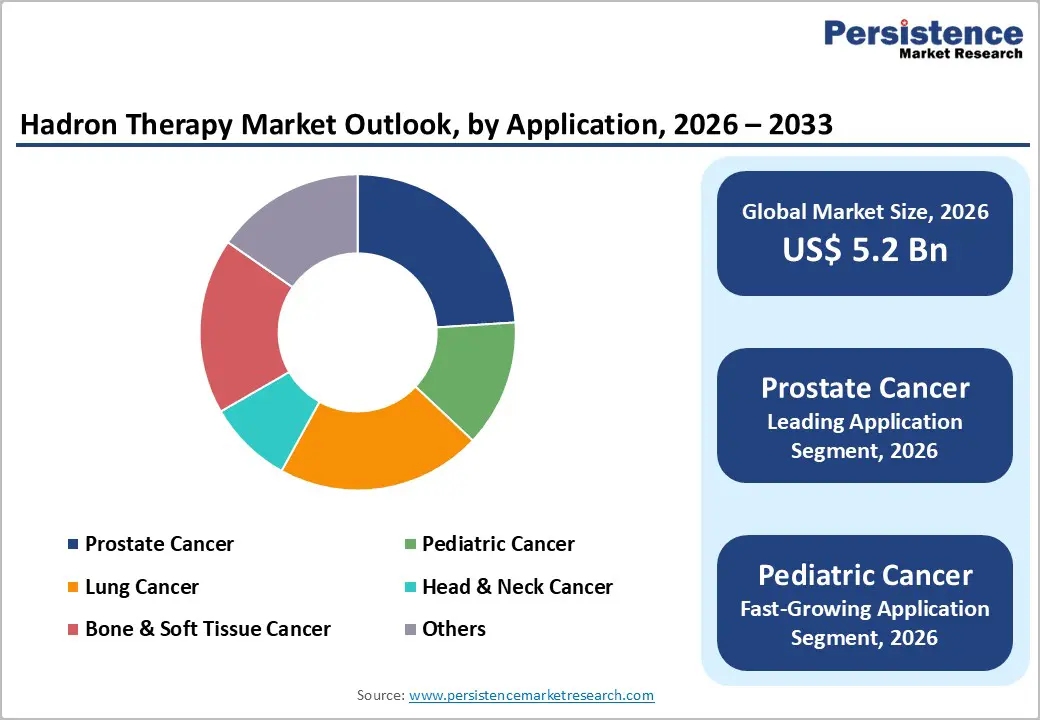

The global hadron therapy market size is expected to be valued at US$ 5.2 billion in 2026 and projected to reach US$ 8.8 billion by 2033, growing at a CAGR of 7.8% between 2026 and 2033. The market is experiencing robust growth driven by escalating global cancer incidence and the superior clinical efficacy of particle-based radiation therapies.

According to the World Health Organization (WHO) and the International Agency for Research on Cancer (IARC), an estimated 20 million new cancer cases were diagnosed globally in 2022, with projections reaching 35 million cases by 2050. This expanding patient population, combined with clinical evidence demonstrating reduced side effects and improved outcomes with hadron therapy compared to conventional photon radiotherapy, is propelling market expansion. Additionally, technological advancements such as intensity-modulated proton therapy (IMPT), pencil beam scanning, and emerging FLASH therapy methodologies are enabling more precise tumor targeting while minimizing exposure to healthy tissues, thereby increasing adoption rates across oncology centers worldwide.

Key Industry Highlights:

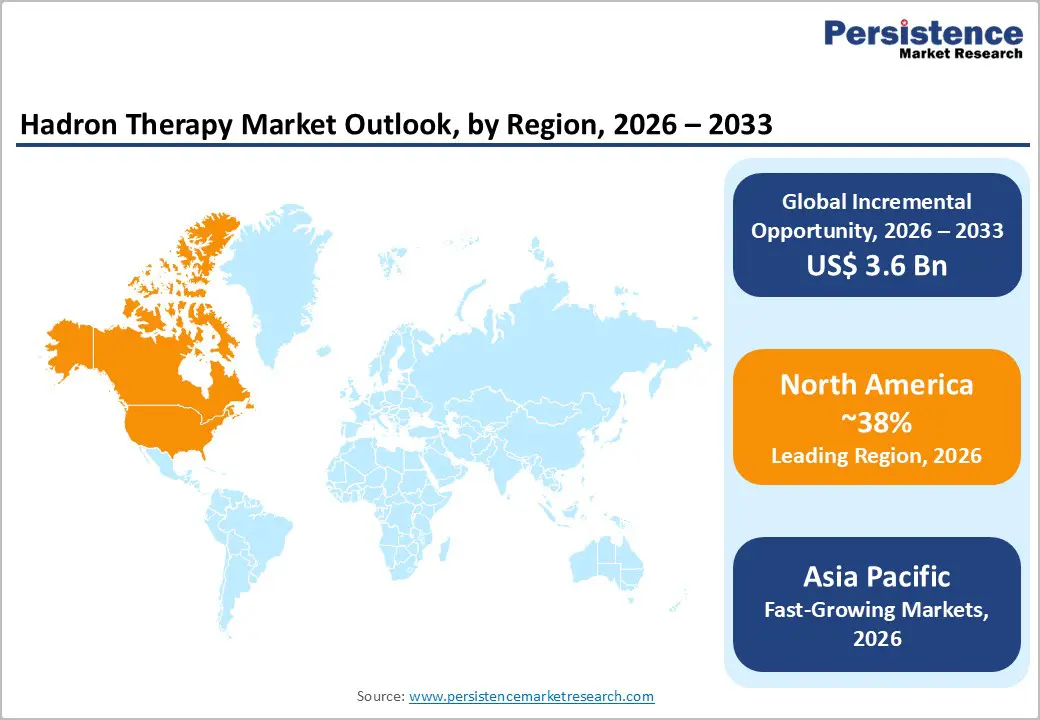

- Leading Region: North America leads the global hadron therapy market with ~38% share in 2025, supported by advanced healthcare infrastructure, favorable reimbursement, and strong research ecosystems.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, with a CAGR >10% (2025–2032), driven by Japan’s carbon ion leadership, China’s infrastructure investments, and rising cancer burden.

- Dominant Therapy Type: Proton Beam Therapy dominates with ~82–83% market share, reflecting clinical maturity, strong evidence, and broad adoption across major regions.

- Fastest-Growing Application: Pediatric cancer is the fastest-growing application, with CAGR of ~12–15%, driven by lower toxicity and increasing adoption in pediatric oncology.

- Key Opportunity: Carbon ion therapy expansion in radioresistant and complex tumors offers strong

| Key Insights | Details |

|---|---|

| Hadron Therapy Market Size (2026E) | US$ 5.2 billion |

| Market Value Forecast (2033F): | US$ 8.8 billion |

| Projected Growth CAGR (2026-2033) | 7.8% |

| Historical Market Growth (2020-2025) | 6.3% |

Market Dynamics

Drivers- Rise in Cancer Burden and Precision Oncology Demand

The global cancer epidemic represents the primary catalyst for hadron therapy market expansion. The American Cancer Society's Global Cancer Statistics 2024 report documents that lung cancer remains the most frequently diagnosed malignancy with 2.5 million cases globally, followed by female breast cancer with 2.3 million cases, and colorectal cancer with 1.9 million cases in 2022. The WHO projects that cancer mortality will increase by approximately 77% by 2050, particularly in low to medium human development index countries experiencing 99-142% proportional increases. Hadron therapy's superior dose conformality delivering approximately 60% lower integral dose compared to conventional photon therapy makes it increasingly attractive for complex tumor cases. Major cancer treatment centers across North America, Europe, and Asia Pacific are investing substantially in hadron therapy infrastructure. As of 2023, 125 particle therapy facilities operate globally, including 110 proton therapy centers and 15 carbon ion facilities, representing a significant expansion from the 40 facilities operational in 2010.

Technological Innovation and Clinical Evidence in Pediatric Oncology

Pediatric cancer represents a high-growth clinical segment driving market momentum. The clinical superiority of hadron therapy for children with cancer is supported by extensive peer-reviewed evidence published in medical journals and institutional outcome data. Proton therapy significantly reduces acute and late radiation-related sequelae in pediatric patients by minimizing exposure to developing organs and reducing secondary malignancy risks. Clinical registries indicate that over 50% of pediatric patients diagnosed with conditions such as medulloblastoma, rhabdomyosarcoma, and ependymoma in leading centers now receive proton therapy. Research institutions across the United States, Japan, and Germany have documented superior long-term quality of life outcomes in proton-treated pediatric cohorts. Additionally, modern technologies including intensity-modulated proton therapy (IMPT) with pencil beam scanning capabilities enable superior dose optimization, facilitating treatment personalization.

Restraints - High Capital Investment Requirements and Infrastructure Challenges

Capital intensity represents a significant barrier to hadron therapy facility development, particularly in resource-constrained healthcare systems. Comprehensive hadron therapy centers require substantial upfront investment, with synchrotron-based facilities demanding €100 million to €150 million in construction costs. Infrastructure requirements include specialized vault construction, radiation shielding systems, treatment planning software, and quality assurance equipment. Operating expenses include maintenance of sophisticated accelerator systems and specialized workforce development. Reimbursement models in numerous countries have not fully aligned with the higher treatment delivery costs, creating financial sustainability challenges for some centers.

Regulatory Complexity and Clinical Evidence Generation

Regulatory frameworks governing hadron therapy devices remain fragmented across regions, creating commercialization challenges. The FDA and European Medicines Agency (EMA) employ distinct approval pathways and evidence standards, requiring manufacturers to conduct separate clinical validation studies for market entry in different jurisdictions. Traditional randomized controlled trials comparing hadron therapy with photon radiotherapy present methodological challenges and extended timelines. Patient recruitment for comparative effectiveness studies is hindered by established clinical enthusiasm for proton therapy and ethical considerations regarding randomization when clinical equipoise diminishes. Limited head-to-head clinical trial data comparing proton therapy and carbon ion therapy across specific tumor types has constrained insurance coverage policies in some regions, reducing institutional incentives for system deployment. Ongoing multi-institutional registries, while valuable, do not satisfy some payer organizations' evidentiary requirements for coverage expansion. Variations in regulatory requirements across the European Union, United States, China, and Japan necessitate significant resource investment by manufacturers for market-specific compliance, increasing commercialization costs.

Opportunity - Precision Medicine Integration and AI-Enabled Treatment Planning

Artificial intelligence integration into treatment planning and adaptive radiotherapy represents a high-impact growth opportunity. Varian, a Siemens Healthineers Company, has developed advanced image reconstruction algorithms including HyperSight, enabling improved visualization of target volumes and organs at risk in proton therapy planning. Integration of AI-powered adaptive radiotherapy systems with hadron therapy delivery enables treatment plan modifications based on daily imaging data, improving dose conformality while reducing normal tissue exposure. Mevion Medical Systems has received FDA clearance for the innovative MEVION S250-FIT™ proton therapy system, featuring upright patient positioning and integrated CT imaging, fundamentally reducing facility footprint and installation complexity. This technological advancement enables treatment room integration into existing linear accelerator vaults, substantially lowering infrastructure barriers for hospital adoption.

Category-wise Insights

Application Analysis

Prostate cancer represents the leading clinical application for hadron therapy primarily due to its high global prevalence and favorable disease characteristics that align well with particle-based radiation. Prostate tumors are typically localized and slow growing, allowing clinicians to fully leverage the precision of hadron therapy, particularly proton beam therapy, to deliver high radiation doses directly to the tumor while minimizing exposure to surrounding healthy tissues such as the bladder and rectum.

This precision significantly reduces treatment-related side effects, improving patient quality of life and treatment compliance. In addition, prostate cancer patients often have long life expectancy, making long-term toxicity reduction a critical clinical priority where hadron therapy offers clear advantages over conventional photon radiation. Strong clinical evidence, established treatment protocols, and increasing physician familiarity have further supported widespread adoption. Moreover, prostate cancer is one of the most reimbursed indications for advanced radiation therapies in developed markets, encouraging healthcare providers to invest in hadron therapy systems and expand treatment capacity, reinforcing its leadership position among clinical applications.

End User Insights

Hospitals represent the leading end-user segment, commanding approximately 56% of market share in 2025. Major teaching hospitals and comprehensive cancer centers across North America, Europe, and Asia Pacific have prioritized hadron therapy infrastructure as a strategic differentiation and clinical quality initiative. Hospital-based proton and carbon ion facilities enable integrated multidisciplinary cancer care, supporting patient convenience and institutional revenue generation. Academic medical centers, including Mayo Clinic, Massachusetts General Hospital, MD Anderson Cancer Center, Heidelberg University Hospital, and University of Tokyo Hospital, maintain sophisticated hadron therapy programs supporting clinical care and research missions.

Hospital investment in hadron therapy has expanded substantially as reimbursement policies have matured and clinical indications have broadened. Specialty cancer treatment centers represent a secondary but rapidly growing segment, with emerging dedicated proton and carbon ion therapy facilities expanding geographic access. Freestanding cancer centers emphasizing advanced treatment technologies have positioned hadron therapy as a core clinical offering. Research and academic institutes maintain specialized hadron therapy capabilities supporting clinical investigation, treatment method validation, and emerging technology development. Government-supported research institutions in Japan (including QST Hospital), Germany (including GSI), and China continue developing advanced hadron therapy platforms and conducting prospective trials. These institutions advance the evidence base supporting clinical applications and train next-generation radiation oncologists and medical physicists in hadron therapy methodologies.

Regional Insights

North America Hadron Therapy Market Trends and Insights

North America commands approximately 38% of the global hadron therapy market in 2025, driven by advanced healthcare infrastructure, comprehensive insurance coverage, and robust research ecosystems. The United States leads North American market development, with over 30 operational proton therapy centers treating approximately 30,000-35,000 patients annually. Major academic medical centers, including the University of Pennsylvania, MD Anderson Cancer Center (Houston), Mayo Clinic Rochester, and Massachusetts General Hospital, maintain sophisticated proton therapy programs. FDA regulatory clarity and established reimbursement pathways have supported sustained capital investment in proton therapy infrastructure. Current Procedural Terminology (CPT) codes and Centers for Medicare & Medicaid Services (CMS) reimbursement policies provide financial support for proton therapy across multiple clinical indications. Intensity-modulated proton therapy (IMPT) adoption is accelerating across U.S. cancer centers, with pencil beam scanning systems deployed at leading institutions. Emerging technologies, including FLASH proton therapy prototype development and AI-enabled adaptive planning systems, are advancing through clinical validation at research centers.

Asia Pacific Hadron Therapy Market Trends and Insights

Asia Pacific represents the fastest-growing hadron therapy market region, projected to expand at a CAGR exceeding 10% by 2032. Japan maintains the most advanced Asian hadron therapy infrastructure, with over 20 operational hadron therapy facilities include 12 carbon ion centers and 9 proton therapy centers. QST Hospital in Chiba operates the world's most experienced carbon ion therapy program, having treated over 16,813 patients cumulatively through 2024. National carbon ion therapy volumes exceed 5,600 patients annually, with 11 malignancy types covered under Japanese national health insurance. Gunma University Heavy Ion Medical Center represents Japan's first university hospital-based carbon ion facility, expanding access beyond specialized institutes. Japan's leadership in carbon ion technology development and comprehensive clinical evidence generation has established the nation as a global hadron therapy innovation hub. China is rapidly expanding its hadron therapy infrastructure aligned with national healthcare modernization initiatives, with 5 operational proton therapy facilities and multiple carbon ion centers under construction or planning stages.

Competitive Landscape

The hadron therapy market’s competitive landscape is shaped by technological innovation, strategic partnerships, and expanding clinical adoption. Providers compete on system precision, facility footprint, cost efficiency, and integrated treatment planning tools to meet diverse healthcare needs. Competition also centers on developing compact, cost-effective solutions that lower barriers for hospitals and cancer centers to adopt particle therapy. Service offerings are differentiated through maintenance, training, and software support, strengthening customer retention.

Key Developments:

- In September 2025, Loma Linda University Health (LLUH), the institution that created the world’s first hospital-based Proton Therapy Treatment Center in 1990, and Mevion Medical Systems, a leading provider of compact proton therapy solutions, announced a historic partnership to install the MEVION S250-FIT Proton Therapy System™. This milestone represented both a significant clinical advancement and a symbolic return to the forefront of innovation for LLUH, marking the launch of the next chapter in its longstanding legacy.

Companies Covered in Hadron Therapy Market

- Ion Beam Applications (IBA)

- Varian Medical Systems (Siemens Healthineers)

- Hitachi, Ltd.

- Mevion Medical Systems

- Mitsubishi Electric Corporation

- Sumitomo Heavy Industries

- ProNova Solutions

- Advanced Oncotherapy

- ProTom International

- Optivus Proton Therapy

- Elekta AB

- Philips Healthcare

Frequently Asked Questions

The global hadron therapy market is projected to be valued at US$ 5.2 billion in 2026, representing significant growth from the historical US$ 3.6 billion market size in 2020, reflecting expanding patient populations and institutional adoption of proton and carbon ion therapies across North America, Europe, and Asia Pacific regions.

The hadron therapy market is primarily driven by escalating global cancer incidence, with 20 million new cases diagnosed annually according to WHO/IARC statistics, combined with clinical evidence demonstrating superior dose conformality and reduced toxicity compared to conventional photon radiotherapy.

North America represents the leading hadron therapy market region, commanding approximately 38% of global market share in 2025, supported by advanced healthcare infrastructure, comprehensive insurance reimbursement policies, research ecosystem strength, and institutional investments in proton and carbon ion therapy infrastructure across academic medical centers and community cancer centers.

Carbon ion therapy expansion represents a significant market growth opportunity, driven by superior biological effectiveness in treating radioresistant malignancies, including pancreatic cancer, sarcomas, and recurrent tumors.

Leading market participants include Varian (Siemens Healthineers), Ion Beam Applications (IBA), Mevion Medical Systems, Hitachi, Ltd., Mitsubishi Electric Corporation, Sumitomo Heavy Industries, Advanced Oncotherapy, ProTom International, Optivus Proton Therapy, Elekta AB, and Philips Healthcare.