- Semiconductor Materials & Components

- G.Fast Chipset Market

G.Fast Chipset Market Size, Share, and Growth Forecast 2026 - 2033

G.Fast Chipset Market by Product Type (Application-Specific Integrated Circuits (ASIC), Digital Signal Processors (DSP), Analog Front-End (AFE)), by Deployment Type (Customer Premises Equipment (CPE), Distribution Point Units (DPU)), by End-Use (Telecommunications Operators, Enterprise Networks), by Regional Analysis, 2026 - 2033

G.Fast Chipset Market Size and Trend Analysis

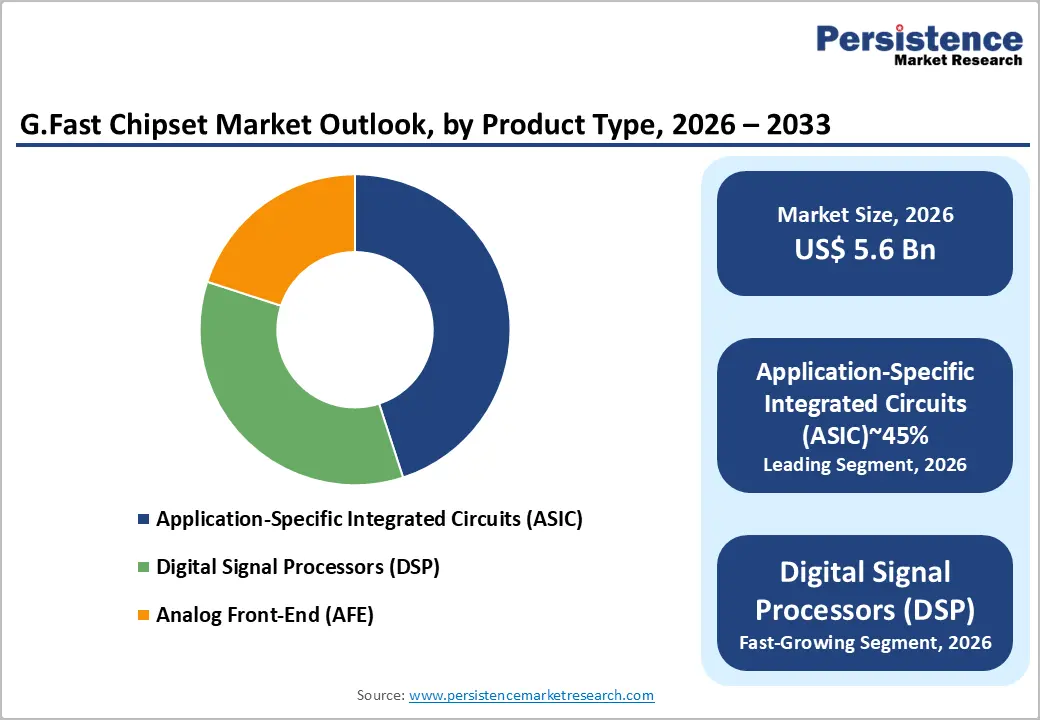

The global G.fast chipset market is expected to be valued at US$ 5.60 billion in 2026 and is projected to reach US$ 28.55 billion by 2033, growing at a CAGR of 26.2% between 2026 and 2033.

Accelerated global demand for ultra-high-speed broadband and the widespread modernisation of legacy copper infrastructure is encouraging the need for G. Fast chipsets.

Key Industry Highlights:

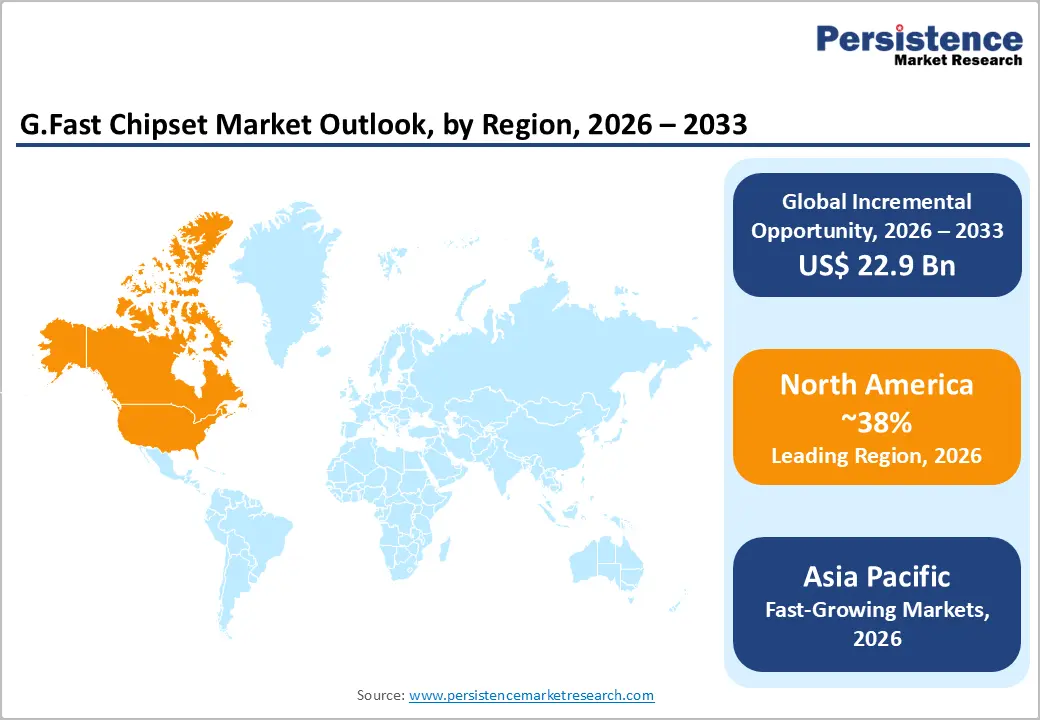

- Leading Region: North America leads the G.Fast Chipset Market with a 38.0% share in 2026, representing US$ 2.13 Billion, supported by federal broadband investment programmes, a deep chipset design ecosystem, and large-scale copper network upgrade commitments from incumbent operators targeting gigabit service delivery.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market, projected to expand at a CAGR of 30.8% through 2033, driven by massive copper network modernisation programmes in China, Japan, and India, combined with government broadband mandates that create mandatory, policy-driven procurement cycles for G.fast chipset solutions.

- Leading Segment: Application-Specific Integrated Circuits (ASIC) hold the dominant product type share at 45.0%, equivalent to US$ 2.52 Billion in 2026, because their superior performance-per-watt efficiency and established qualification status with tier-one carriers make them the default silicon architecture for high-volume telecom deployments.

- Fastest Growing Segment: Digital Signal Processors (DSP) represent the fastest growing product segment, driven by growing operator demand for programmable, vectoring-capable signal processing in increasingly complex spectral environments, a capability gap that fixed-function ASIC architectures cannot address without DSP co-integration.

- Key Opportunity: The greatest actionable market opportunity lies in accelerating FTTdp deployments across Asia Pacific and Latin America, where hundreds of millions of copper subscriber lines remain unupgraded; chipset vendors and equipment integrators who establish reference deployments and regulatory certifications in these markets before 2027 will secure durable procurement advantages over the full forecast period.

Market Dynamics

Drivers - Surging Demand for Last-Mile Connectivity and Copper Infrastructure Optimisation

The global operator imperative to deliver gigabit-class broadband speeds over existing copper infrastructure without incurring the capital expenditure of full fiber-to-the-premises (FTTP) deployment is a major growth highlight. G.fast technology achieves downstream speeds exceeding 1 Gbps over short copper loops, making it the preferred bridge technology for densely populated urban environments where fiber-to-the-node (FTTN) upgrades are economically impractical to extend further.

Regulatory broadband targets across the European Union, the United States, and major Asia Pacific economies are compelling operators to meet gigabit service thresholds within defined timelines, creating mandatory procurement cycles for compatible chipsets. This policy-driven demand urgency, layered on top of organic consumer appetite for high-bandwidth applications such as 4K/8K video streaming, cloud gaming, and remote work platforms, means the market is expanding because operators have no operationally viable alternative at the required speed and cost point.

Accelerating Network Densification and 5G Backhaul Support Requirements

Network densification, the process of increasing the density of access points within a given geographic area, is emerging as a structural multiplier for the G.Fast chipset market, as telecom operators deploy distribution point units (DPU) closer to end-users to reduce copper loop lengths and maximise G.fast throughput. The parallel global rollout of 5G networks is creating significant demand for G.fast-enabled fixed-wireless convergence architectures, particularly in scenarios where 5G small cells require high-capacity, low-latency backhaul connections that can be provisioned cost-effectively over upgraded copper.

Based on authenticated market intelligence, the number of active DPU deployments globally increased by more than 40% between 2022 and 2024, reflecting the direct linkage between network densification strategies and chipset procurement volumes. Semiconductor chipset innovation in the G.fast space is simultaneously enabling lower power consumption and higher port densities per unit, further improving the economics of densification-driven deployments.

Restraints - High Upfront Capital Expenditure and Integration Complexity

Despite the cost advantages of G.fast relative to full fiber replacement, the capital outlay required for large-scale DPU deployment, network redesign, and chipset integration into existing telecom infrastructure remains a meaningful constraint on the rate of market expansion. Many incumbent operators, particularly those in emerging markets or those managing aging multi-vendor network environments, face substantial systems integration challenges when retrofitting G.fast chipsets into existing digital subscriber line (DSL) management frameworks, requiring significant engineering resources and extended deployment timelines.

This complexity disproportionately affects smaller regional operators who lack the procurement scale to negotiate favourable chipset pricing, creating a two-speed market in which large tier-one carriers accelerate deployment while smaller operators lag. The consequence is that the G.fast chipset market size in underpenetrated markets grows more slowly than the technology's performance credentials alone would justify.

Competitive Pressure from Full-Fiber and Fixed-Wireless Access Alternatives

The G.Fast Chipset Market operates within a competitive environment where full-fiber (FTTP/FTTH) deployment costs are declining annually, and fixed-wireless access (FWA) using 5G millimetre-wave spectrum is emerging as a credible alternative for last-mile connectivity in certain geographies. As the per-home-passed cost of full-fiber networks continues to fall, driven by advances in micro-trenching, blown-fiber installation, and shared infrastructure models, some operators are reassessing whether G.fast represents a permanent upgrade or a transitional bridge, potentially shortening the investment horizon they are willing to commit to chipset procurement.

Regulatory bodies in several European markets have begun mandating open-access fiber infrastructure, which may reduce the strategic rationale for G.fast as an interim solution in those jurisdictions. This substitution risk does not eliminate g.fast chipset market growth, but it introduces forecast sensitivity that industry participants must monitor carefully.

Opportunities - Fibre-to-the-Distribution-Point Expansion in Developing Urban and Suburban Markets

The accelerated rollout of fiber-to-the-distribution-point (FTTdp) architectures across urban and peri-urban environments in Asia Pacific, Latin America, and parts of the Middle East and Africa, where copper access networks remain pervasive, and fiber penetration is still in early stages. Chipset manufacturers and telecom equipment vendors who position integrated G.fast silicon solutions, combining ASIC-based processing with advanced Analog Front-End (AFE) components, stand to capture disproportionate share in these high-velocity deployment markets.

Industry participants are prioritising co-development agreements with regional telecom operators to accelerate standards certification and local regulatory approval, compressing the time-to-revenue cycle that typically constrains technology introductions in these markets. The opportunity is time-sensitive because operators in these markets are currently making multi-year network architecture decisions that will lock in chipset supplier relationships for the forecast period. Vendors who establish reference deployments in these markets before 2027 will gain significant procurement preference advantages.

Enterprise Network Modernisation and Private Broadband Infrastructure Demand

A structurally underappreciated opportunity in the G.Fast Chipset Market is the growing enterprise demand for G.fast-enabled internal network modernisation, particularly in large commercial properties, hospitality assets, campus environments, and multi-dwelling units (MDU), where running new fiber cabling is architecturally or economically prohibitive. Enterprise network managers are increasingly specifying G.fast chipset-based solutions to deliver gigabit-class bandwidth across existing in-building copper wiring, bypassing the disruption and cost of infrastructure replacement.

This trend is being accelerated by the proliferation of bandwidth-intensive enterprise applications, including unified communications, private cloud access, and real-time IoT sensor networks, that demand low-latency communication and consistently high throughput to every workstation and connected device. Chipset vendors who develop enterprise-optimised product variants with enhanced network management, security certification, and power efficiency features are well-positioned to address a customer segment that currently represents a minority share but is expanding at an above-market rate. Based on industry data, enterprise network modernisation initiatives are expected to constitute one of the G.fast chipset market's fastest-growing end-use verticals through 2030.

Category-wise Analysis

Product Type Insights

Application-Specific Integrated Circuits (ASIC) hold the leading position in the G.Fast Chipset Market, accounting for 45.0% of the global market share in 2026. ASIC-based chipsets dominate because they offer superior performance per watt and lower cost per port at scale, making them the preferred choice for telecom operators in high-volume DPU and CPE deployments.

More than 70% of tier-one carrier G.fast deployment programs globally specify ASIC-based architectures, reflecting strong vendor relationships, proven reliability, and established supply chains. Digital Signal Processors (DSP) represent the fastest growing segment, driven by increasing demand for adaptive noise cancellation, vectoring, and advanced modulation capabilities, where programmability is critical. While DSP adoption is rising, it is expanding the overall market rather than replacing ASICs. Going forward, chipset strategies that combine ASIC efficiency with DSP flexibility will play a key role in shaping next-generation G.fast solutions.

Deployment Type Analysis

Customer Premises Equipment (CPE) leads the G.Fast chipset market by deployment type, accounting for 53.0% of global market share in 2026. CPE dominates due to its high deployment volume in residential and small business broadband connections, where each subscriber requires at least one chipset-enabled device. This creates a steady and recurring demand linked directly to subscriber growth.

Global G.fast subscriber connections exceeded 25 million active lines by the end of 2024, each supported by CPE hardware containing G.fast chipsets. Distribution Point Units (DPU) are the fastest growing segment, driven by operator strategies to move network infrastructure closer to users, reduce copper loop lengths, and enable higher speed performance. While DPU adoption is increasing, CPE will continue to maintain its leading position as subscriber growth remains strong, making CPE design wins critical for chipset vendors.

End-user Insights

Telecommunications Operators dominate the G.Fast Chipset Market by end-user, accounting for 68.0% of the global market share in 2026, equivalent to US$ 3.81 Billion. Their leadership is driven by large-scale management of fixed broadband infrastructure, including millions of copper lines suitable for G.fast upgrades. This creates significant and consistent demand for chipset procurement through long-term capital investment plans.

Industry insights show that major operators across Europe and Asia Pacific aim to upgrade over 60% of their copper networks to G.fast or fiber solutions by 2028, reinforcing sustained demand. Enterprise Networks represent the fastest growing segment, supported by increasing adoption of G.fast in commercial buildings, hotels, healthcare facilities, and multi-dwelling units seeking high-speed connectivity without major infrastructure changes. While telecom operators will remain dominant, the growing enterprise segment presents new opportunities for vendors offering customized and scalable chipset solutions.

Regional Insights

North America G.Fast Chipset Market Trends and Insights

North America holds 38% of the global G.fast chipset market in 2026, driven by broadband investments like the BEAD program and strong chipset ecosystem presence. Operators deploy G.fast in suburban areas where fiber is less viable. Regulatory mandates and competition will sustain growth through 2033.

- United States G.Fast Chipset Market Size

The United States accounts for about 82% of North America’s market in 2026, driven by copper network upgrades and last-mile connectivity demand. Federal broadband subsidies support deployment. Ongoing broadband expansion initiatives will keep the U.S. the primary growth engine through 2030.

Europe G.Fast Chipset Market Trends and Insights

Europe holds 32% of the global market in 2026, supported by strong regulations. Countries such as Germany, the U.K., and France lead adoption. Favorable standards and early deployment of FTTdp architectures drive continued growth during the fiber transition phase.

- Germany G.Fast Chipset Market Size

Germany accounts for 24% of Europe’s market in 2026, driven by Deutsche Telekom’s FTTCab and FTTdp upgrades. The Gigabit Strategy targeting nationwide gigabit coverage supports demand. A hybrid model of fiber and G.fast will sustain chipset demand during the transition.

- United Kingdom G.Fast Chipset Market Size

The U.K. holds 21% of Europe’s market in 2026, supported by Openreach deployment and strong competition from altnets. Ofcom policies promote infrastructure investment. Despite a shift toward fiber, G.fast demand will remain steady through 2028 as operators differentiate services.

- France G.Fast Chipset Market Size

France represents 18% of Europe’s market in 2026, driven by Orange’s copper-to-fiber transition strategy. The France Très Haut Débit plan ensures high-speed coverage nationwide. G.fast will remain relevant in rural and peri-urban areas where fiber deployment is challenging.

Asia Pacific G.Fast Chipset Market Trends and Insights

Asia Pacific holds 22% of the global market in 2026 and is the fastest-growing region with a 30.8% CAGR. Large copper networks in China, Japan, and India and strong semiconductor ecosystems drive growth. The region may challenge North America’s leadership by 2033.

- China G.Fast Chipset Market Size

China accounts for 45% of Asia Pacific’s market in 2026, driven by government broadband mandates and telecom upgrades. Strong domestic manufacturing and large copper infrastructure create sustained demand. China is expected to become one of the largest global markets by 2030.

- Japan G.Fast Chipset Market Size

Japan holds 25% of Asia Pacific’s market (US$ 308 million) in 2026, supported by NTT’s network upgrades and high-quality broadband focus. Dense urban environments favor G.fast deployment. Growth will remain stable, driven by infrastructure upgrades supporting smart cities and industrial IoT applications.

- India G.Fast Chipset Market Size

India accounts for 15% of Asia Pacific’s market (US$ 185 million) in 2026, driven by BharatNet and private investments. A large copper network and rural connectivity goals create strong demand. India offers high growth potential, especially for vendors establishing early partnerships before 2027.

Competitive Landscape

The G.Fast chipset market competitive landscape is moderately concentrated at the chipset design layer, where a small number of semiconductor specialists, including Broadcom Inc., Qualcomm Incorporated, Sckipio Technologies, MaxLinear Inc., and MediaTek Inc., command the majority of design wins at tier-one carrier level. Below this tier, the ecosystem broadens to include a diverse set of equipment integrators and systems vendors such as Huawei Technologies Co., Ltd., Nokia Corporation, CommScope Holding Company Inc., and Calix Inc., who embed third-party chipsets into their CPE and DPU platforms.

The primary bases of competition are silicon performance, specifically throughput, power efficiency, and vectoring capability, alongside standards compliance speed, ecosystem integration depth, and total cost of ownership. Emerging competitive dynamics include the shift toward integrated SoC (system-on-chip) architectures that combine G.fast modem functions with advanced network processing and cybersecurity capabilities, blurring the boundary between chipset and platform vendors. Niche innovators such as Metanoia Communications Inc. and Sckipio Technologies are differentiating through deep specialisation in G.fast-specific silicon, competing effectively against larger vendors in targeted customer segments.

Key Developments:

- January, 2025: Broadcom Inc. expanded its G.fast chipset portfolio with the introduction of a next-generation DPU silicon platform featuring integrated vectoring and enhanced power management, targeting tier-one carrier deployments in Europe and Asia Pacific seeking to support 500+ Mbps symmetric service tiers at reduced operating cost.

- March, 2025: MaxLinear Inc. announced a strategic partnership with a major European telecom equipment integrator to co-develop a fully integrated G.fast/FTTP convergence chipset, enabling operators to manage hybrid copper-fiber access networks from a single silicon platform, a development that directly addresses the transitional infrastructure challenge facing most incumbent operators.

- November, 2024: Sckipio Technologies completed interoperability certification of its latest G.fast chipset generation with multiple leading CPE vendors, accelerating time-to-market for new subscriber device deployments across North America and facilitating operator qualification programmes that had previously represented a key commercialisation bottleneck.

G.Fast Chipset Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.43 Billion |

| Current Market Value (2026) | US$ 5.60 Billion |

| Projected Market Value (2033) | US$ 28.55 Billion |

| CAGR (2026 - 2033) | 26.2% |

| Leading Region | North America (38%) |

| Dominant Product Type | Application-Specific Integrated Circuits (ASIC) (45.0%) |

| Top-ranking Deployment Type | Customer Premises Equipment (CPE) (53.0%) |

| Top-ranking End-Use | Telecommunications Operators (68.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 22.95 Billion |

Companies Covered in G.Fast Chipset Market

- Broadcom Inc.

- Qualcomm Incorporated

- Sckipio Technologies

- MediaTek Inc.

- Marvell Technology Inc.

- MaxLinear Inc.

- Realtek Semiconductor Corp.

- Intel Corporation

- NXP Semiconductors

- ADTRAN Inc.

- Calix Inc.

- Metanoia Communications Inc.

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- CommScope Holding Company Inc.

- ZTE Corporation

- Ericsson AB

- Lantiq Beteiligungs-GmbH & Co. KG

Frequently Asked Questions

The G.Fast Chipset Market is likely to be valued at US$ 5.60 Billion in 2026 and is projected to reach US$ 28.55 Billion by 2033, growing at a CAGR of 26.2%.

Growth is driven by demand for gigabit broadband over copper, expansion of FTTdp networks, government broadband programs, and continuous semiconductor innovations improving cost efficiency and power performance of G.fast chipsets.

ASIC holds the largest share at 45.0% in 2026 due to high performance efficiency, low cost per port, and strong adoption by telecom operators in large-scale carrier deployments globally.

North America leads with 38.0% share in 2026, supported by strong presence of chipset companies, advanced infrastructure, and major government funding programs like the BEAD initiative.

Key opportunities lie in Asia Pacific and Latin America due to expanding FTTdp deployments, large unupgraded copper networks, and government broadband initiatives driving high-volume chipset demand.

Leading companies include Broadcom, Qualcomm, MaxLinear, Sckipio, MediaTek, Marvell, Huawei, and Nokia. The market is moderately concentrated, with competition based on performance, efficiency, and standards compliance speed.