- Electrical Equipment & Services

- Frameless Brushless DC Motors Market

Frameless Brushless DC Motors Market Size, Share, and Growth Forecast 2026 - 2033

Frameless Brushless DC Motors Market by Motor Type (Inner Rotor, Outer Rotor), by Application (Robotics, Medical Equipment, Aerospace & Defense, Industrial Automation, Electric Mobility), by End User (Automotive, Healthcare, Aerospace, Industrial Manufacturing), by Regional Analysis, 2026 - 2033

Frameless Brushless DC Motors Market Size and Trend Analysis

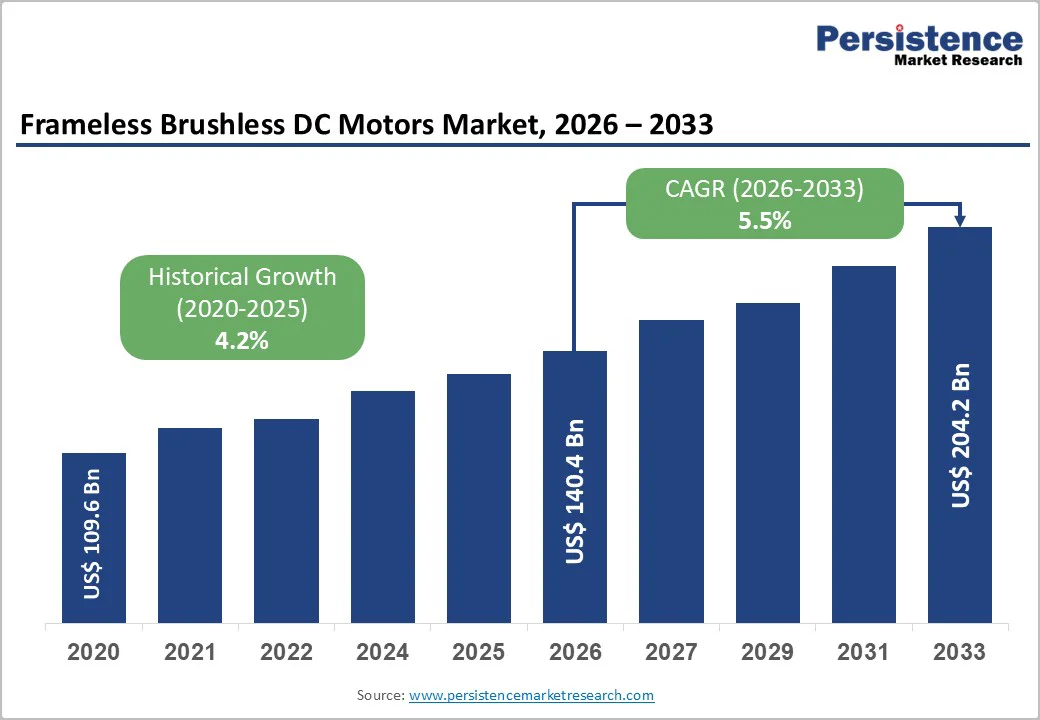

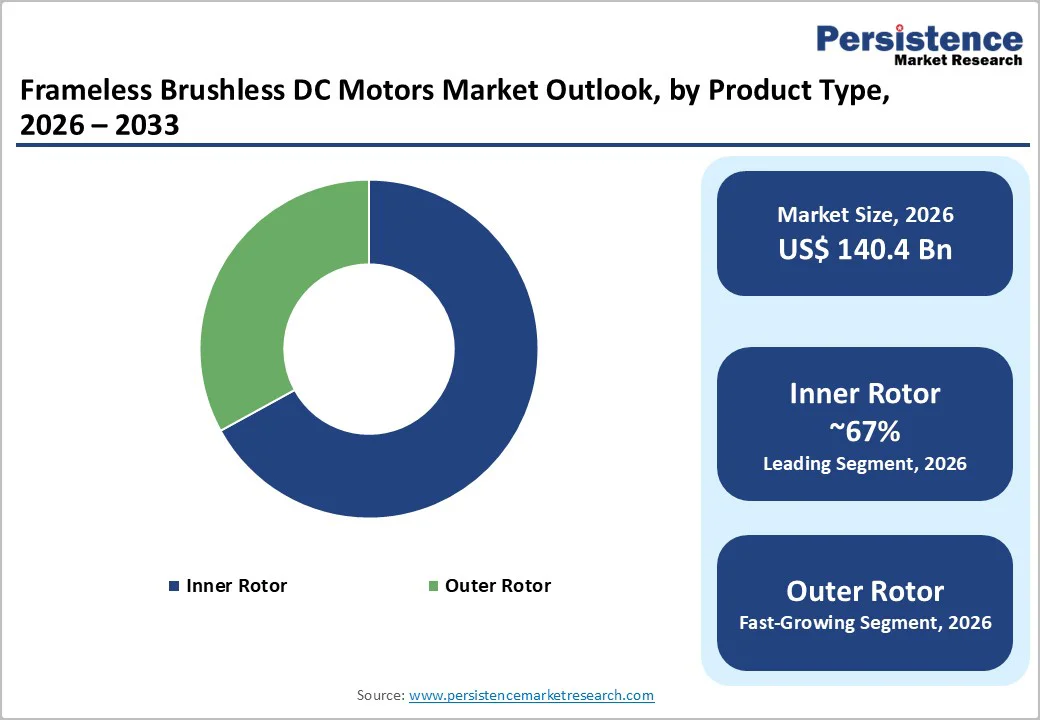

The global frameless brushless DC Motors market size is likely to be valued at US$ 140.4 billion in 2026 and is projected to reach US$ 204.2 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033. The market is primarily driven by the accelerating adoption of advanced robotics and automation across industrial and medical sectors. Manufacturers are increasingly prioritizing compact, high-torque-density solutions that eliminate mechanical redundancy, such as housing and bearings, to achieve lighter and more efficient designs.

Key Market Highlights

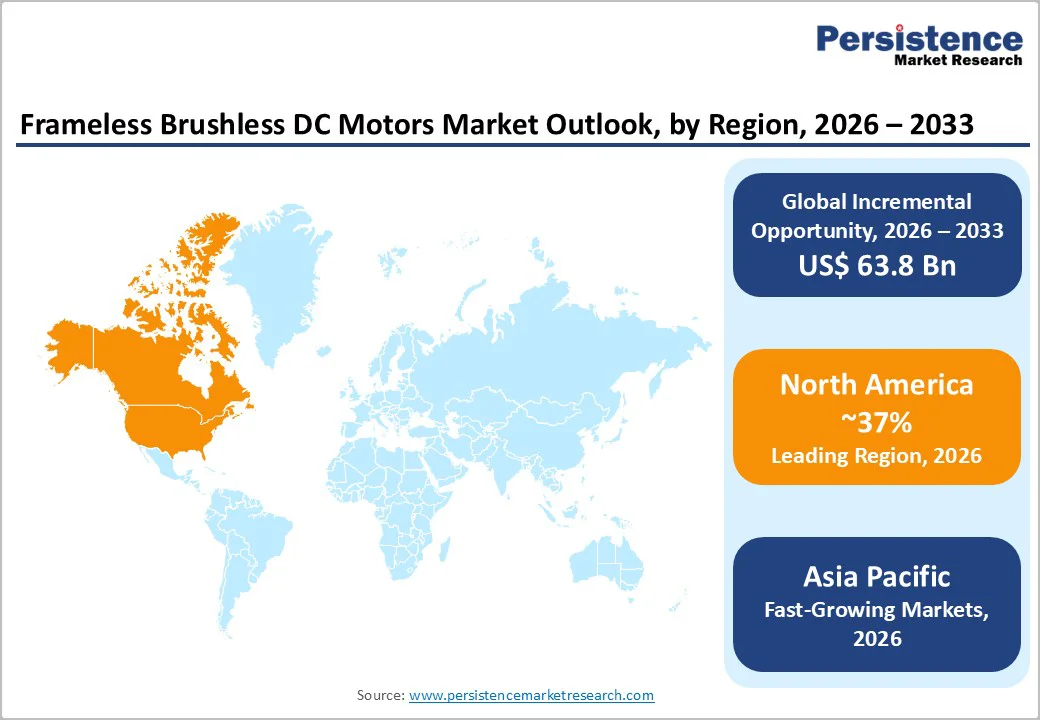

- Leading Region: Asia Pacific dominates global volume with 39% share, due to rapid industrialization and the massive scale of its electronics and automotive manufacturing sectors.

- Fastest Growing Region: Asia Pacific is projected to maintain the highest growth rate with CAGR of 6.3%, driven by China's aggressive automation targets and EV production.

- Dominant Segment: The Inner Rotor motor type has the largest market share at 67%, which is the standard for high-dynamic servo applications, commanding the majority of the market.

- Fastest Growing Segment: Robotics applications are expanding most rapidly with rising CAGR of 6.5%, fueled by the proliferation of cobots and surgical robotic systems.

- Key Market Opportunity: Predictive Maintenance integration via AI-enabled controllers represents a high-value service revenue stream for motor manufacturers.

| Key Insights | Details |

|---|---|

|

Frameless Brushless DC Motors Market Size (2026E) |

US$ 140.4 Billion |

|

Market Value Forecast (2033F) |

US$ 204.2 Billion |

|

Projected Growth CAGR (2026-2033) |

5.5% |

|

Historical Market Growth (2020-2025) |

4.2% |

Market Dynamics

Market Growth Drivers

Growing Adoption of Minimally Invasive Surgical Robots is Driving Strong Demand for Compact, High-Precision Frameless Motors

The rapid growth of surgical robotics and precision-medicine technologies is becoming a major catalyst for the frameless brushless DC motor market. Medical-robot sales increased by 91% in 2024, reaching nearly 16,700 units, according to the International Federation of Robotics (IFR), highlighting strong global momentum. This growth is driven by rising demand for minimally invasive surgeries, greater hospital automation, and continuous advancements in robotic-assisted procedures.

Frameless motors are preferred in these systems because they deliver high torque, smooth motion, and precise control while occupying minimal space, making them ideal for robotic joints requiring compact, sterilizable components. Companies developing surgical platforms increasingly rely on motors with diameters as small as 10–20 mm, supporting the trend toward miniaturization. As health systems worldwide adopt more robotic solutions to improve surgical accuracy and reduce recovery times, suppliers of high-precision frameless motor kits are positioned for strong and sustained demand.

Rising Deployment of Cobots in Modern Factories is Boosting the Need for Lightweight, Joint-Integrated Frameless Motor Solutions

Industrial automation is transforming rapidly, especially with the rising deployment of collaborative robots (cobots) that work safely alongside human operators. These robots require lightweight, joint-embedded motors to ensure smooth, efficient, and safe movement. Frameless brushless DC motors are ideal because they allow direct integration of the rotor and stator into the robot joint, lowering inertia and improving motion responsiveness. This integration enhances overall robot performance while maintaining human-machine safety standards.

The shipments of industrial robots across manufacturing sectors, reflecting strong growth in automation investments. As companies automate tasks such as assembly, packaging, testing, and material handling, suppliers of compact, high-torque frameless motors that meet tight engineering and safety requirements are experiencing increasing demand. The shift toward flexible, smart, and human-assisted automation will continue to make frameless motors a preferred choice in next-generation robotic systems.

Market Restraints

Complex Engineering Requirements and High Integration Expenses Remain Key Barriers to Frameless Motor Adoption

Affecting wider adoption of frameless motors is the high upfront engineering effort required for proper integration. Unlike traditional enclosed motors, frameless motors do not come with housings or mounting systems and must be fitted precisely within the machine’s structure. This means manufacturers must handle critical aspects such as rotor-stator alignment, air-gap optimization, and custom mechanical mounting. Such tasks demand experienced motion-engineering teams, specialized tools, and strict manufacturing tolerances.

For many small and medium-sized companies, these additional engineering needs increase project budgets and delay development timelines. As a result, cost-sensitive industries often continue using standard housed motors even though they offer less flexibility and performance. The need for extensive customization, higher design complexity, and added mechanical integration remains a major restraint for the frameless motor market, especially in applications where budgets and design resources are limited.

Thermal Challenges due to the Lack of Motor Housing limit Frameless Motor Use in High-Power and Harsh-Environment Applications

Thermal management represents another significant limitation for frameless motor adoption. Because the motors lack built-in housings, they depend heavily on the host equipment to dissipate heat. In high-power or continuous-duty applications, inadequate heat dissipation can cause temperature buildup, leading to performance loss, demagnetization of rare-earth magnets, or internal component failure. This makes thermal design a crucial engineering requirement during system integration.

In industries such as aerospace, heavy machinery, or large-scale automation, implementing active cooling systems or redesigning structural components to act as heat sinks can be challenging and costly. When the host structure cannot effectively manage heat, the overall system reliability is compromised, limiting frameless motor usage in demanding environments. These complex thermal considerations often discourage adoption, especially in applications where cooling space is restricted or where the additional engineering needed to manage heat is not feasible.

Market Opportunities

Smart Frameless Motors with AI-Enabled Predictive Monitoring Present a Major Growth Opportunity for Manufacturers

Growing interest in “smart” motor systems presents a strong opportunity for frameless motor manufacturers. By integrating sensors, IoT connectivity, and AI-based analytics into the motor setup or its drive electronics, companies can offer predictive maintenance features that detect early signs of wear, overheating, or vibration imbalance. This is especially valuable in industries where unexpected downtime leads to major financial losses, such as semiconductor fabrication, automated logistics, and high-precision manufacturing.

Smart frameless motor kits that continuously monitor thermal and motion data can help customers improve efficiency, schedule maintenance proactively, and avoid system failures. As industries increasingly move toward smart automation and digital monitoring, suppliers that combine high-performance frameless motors with advanced diagnostic capabilities will gain a competitive edge, securing stronger demand in sectors requiring reliability, uptime, and constant operational monitoring.

Rising Shift toward Electric Construction and Agricultural Machinery is Creating Strong Demand for High-Torque Frameless Motors

The global shift toward electrification is expanding beyond passenger cars into construction, agricultural, and off-highway machinery. These vehicles increasingly require efficient electric actuators for steering, braking, lifting, and implement control, functions traditionally powered by hydraulics. Frameless brushless DC motors are well-suited for this transition because they deliver high torque density and can fit into the limited mechanical spaces available in heavy vehicles. Their lightweight design also helps extend battery life by improving system efficiency.

Government initiatives in Europe, China, and other regions promoting sustainable and electric agricultural technology further accelerate adoption. As manufacturers redesign machinery to reduce emissions and operating costs, demand for rugged frameless motors capable of working in harsh environments, exposed to dust, vibration, and continuous load-is growing. This segment presents substantial opportunity for companies developing large-diameter, durable frameless motor solutions.

Category-wise Insights

Inner Rotor Analysis

The Inner Rotor segment holds the largest market share at approximately 67%, driven by its superior performance in applications demanding high torque and efficiency. This architecture positions the rotor inside the stator, which significantly enhances heat dissipation and enables high-speed operation, making it ideal for robotics, industrial automation, and electric vehicle systems. Manufacturers favor inner rotor designs for their compact footprint and ability to deliver rapid acceleration with low inertia. The segment's dominance is further reinforced by its extensive adoption in automotive power steering and drivetrain applications, where performance and reliability are critical. Continuous advancements in materials and motor design are expanding the applicability of inner rotor brushless DC motors across diverse industries worldwide.

Robotics Analysis

Robotics stands as the dominant application segment, supported by the International Federation of Robotics reporting 542,000 industrial robot installations globally in 2024, with the operational stock reaching 4.66 million units, marking a 9% increase year-over-year. The integration of frameless motors directly into robotic joints eliminates couplings and reduces backlash, enabling smoother and more precise motion critical for modern automation. Asia leads with 74% of new robot deployments, while installations are forecasted to grow 6% to 575,000 units and exceed 700,000 units. This sustained expansion solidifies robotics as the primary revenue driver for frameless motor manufacturers globally.

Automotive Analysis

The Automotive segment is emerging as a leading end-user category, particularly with the accelerating transition to electric vehicles. Frameless motors are increasingly deployed in electric power steering, active suspension, and electronic braking systems where weight reduction directly extends vehicle range. The automotive sector's demand is identifying it as the leading end-user segment for brushless DC motors. Major tier-1 suppliers are actively partnering with motor manufacturers to develop custom frameless solutions that integrate seamlessly into chassis designs. These partnerships focus on reducing overall vehicle weight while maintaining performance, creating substantial opportunities as global EV production continues its upward trajectory across markets.

Regional Insights

North America Frameless Brushless DC Motors Market Trends

North America remains a leading market for frameless brushless DC motors due to strong innovation and high-value industry demand. Sectors such as aerospace, defense, medical devices, and industrial automation continue to invest heavily in advanced motor technologies. The United States, in particular, supports growth through dedicated funding for UAVs, robotics, and next-generation automation systems. States like California and Massachusetts host many medical-device companies that require compact, sterilizable frameless motors for surgical and therapeutic equipment.

In addition, reshoring initiatives aimed at reducing supply-chain dependence have encouraged manufacturers to bring production back to the U.S., further boosting demand for precision motor components. As industries adopt more robotics and smart automation, the region is expected to maintain steady growth in frameless motor adoption, especially for applications that require high reliability and engineering customization.

Europe Frameless Brushless DC Motors Market Trends

Europe represents a technologically mature yet continuously evolving market for frameless brushless DC motors. Germany leads the region with strong expertise in industrial automation, mechanical engineering, and energy-efficient manufacturing systems. European regulations such as the EU Ecodesign Directive encourage the use of high-efficiency brushless technologies, accelerating adoption across industries. The region is also recognized as a global hub for collaborative robotics, with companies such as Universal Robots contributing to the expansion of integrated torque motors and precision motion systems.

As European factories modernize under Industry 4.0 and embrace digitalization, manufacturers increasingly require motors that support advanced automation, precise control, and sustainability objectives. This focus on smart manufacturing, environmental compliance, and engineering excellence positions Europe as a stable and influential market for frameless motors across robotics, packaging, medical devices, and specialized machinery.

Asia Pacific Frameless Brushless DC Motors Market Trends

Asia Pacific stands out as the fastest-growing market for frameless brushless DC motors, driven by large-scale manufacturing bases in China, Japan, and South Korea. China’s national initiatives under “Made in China 2025” actively support growth in robotics, automation, and electric vehicle production, creating strong demand for high-performance motion components. Japan remains a global leader in robotics manufacturing, with companies like Yaskawa and Fanuc setting high reliability and precision standards.

The region benefits from cost-efficient production capabilities, strong electronics supply chains, and rapid industrial expansion. As automation, consumer electronics, EVs, and semiconductor production continue to grow, demand for compact, efficient frameless motors is rising quickly. Asia Pacific’s combination of high manufacturing scale, government support, and technological adoption positions it as a strategic production and consumption hub for frameless motor suppliers worldwide.

Competitive Landscape

The global market is moderately fragmented but features a consolidated tier of top players who dominate high-end applications. Companies like Maxon, Kollmorgen, and Faulhaber maintain strong market positions through extensive patent portfolios and established relationships with key aerospace and medical OEMs. The market is witnessing a trend towards vertical integration, where motor manufacturers are acquiring drive and controller companies to offer complete motion control sub-systems. Differentiation is achieved primarily through customization capabilities; market leaders often provide "modified standard" products to fit unique customer requirements, creating high switching costs and fostering long-term loyalty.

Key Market Developments

- In May 2025: Allient Inc. introduced its new “ElectroFlux” torque motor line and the enhanced “SA Series” axial-flux motors, aimed at delivering high-torque, high-efficiency performance for next-generation robotics and automation systems.

- In November 2024: Maxon rolled out the ECX PRIME 16 L, a compact, brushless motor with ironless windings, engineered for handheld medical tools and sterilization-ready industrial equipment, providing exceptional speed, precision, and dynamic response.

- In December 2023: Kollmorgen released its TBM2G frameless servo motor series, created specifically for collaborative robots, offering lower weight, improved thermal efficiency, and optimized torque density for seamless integration into robotic joints.

Companies Covered in Frameless Brushless DC Motors Market

- Maxon

- Faulhaber

- Kollmorgen

- Portescap

- Allied Motion

- Nidec

- Shinano Kenshi

- T-Motor

- Moog

- Parker Hannifin

- Tecnotion

- Aerotech

- Lin Engineering

- Anaheim Automation

- Oriental Motor

Frequently Asked Questions

The frameless brushless DC motors market is projected to reach a value of US$ 204.2 Billion by 2033.

Key drivers include the rising adoption of surgical and industrial robotics, the push for miniaturization in medical devices, and the electrification of aerospace and defense systems.

The Inner Rotor segment currently holds the largest market share due to its suitability for high-speed and high-dynamic applications in automation.

Asia Pacific is expected to be the fastest-growing region, largely due to aggressive.