- Automotive Components & Materials

- Forged Automotive Components Market

Forged Automotive Components Market Size, Share, and Growth Forecast 2026 - 2033

Forged Automotive Components Market by Vehicle Type (Heavy Commercial Vehicles, Light Commercial Vehicles, Passenger Vehicles), Forging Process (Impression Die Forging (Hydraulic Presses, Mechanical Presses, Hammers), Cold Forging, Open Die Forging, Seamless Rolled Ring Forging), Material, Automotive Component, Application, Regional Analysis, 2026 - 2033

Forged Automotive Components Market Size and Trend Analysis

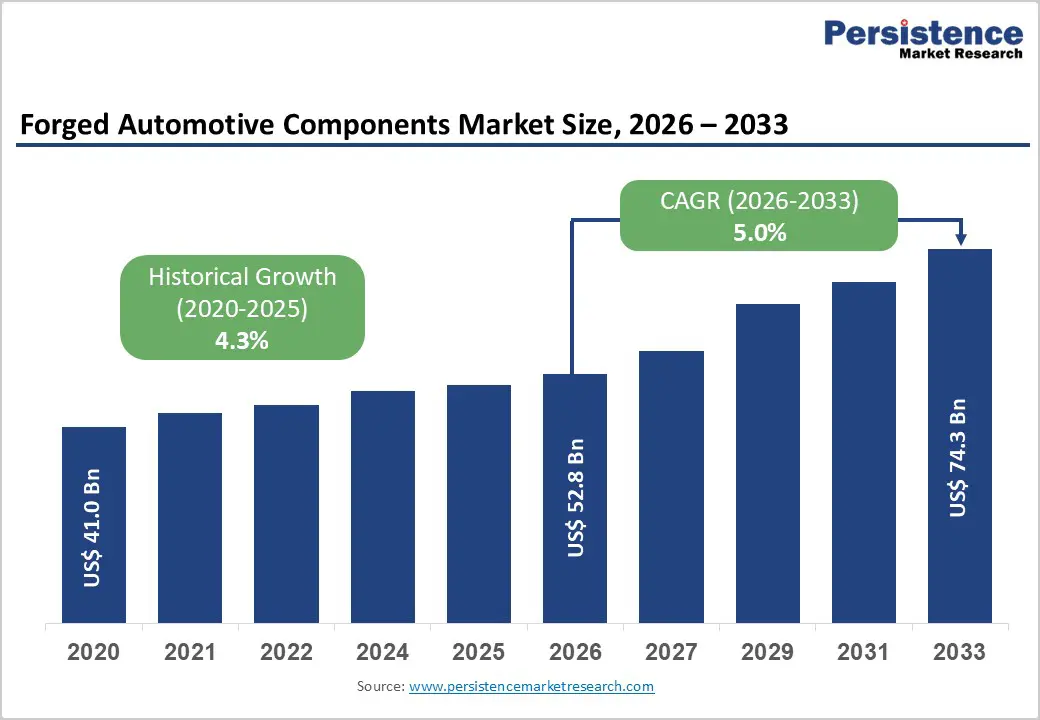

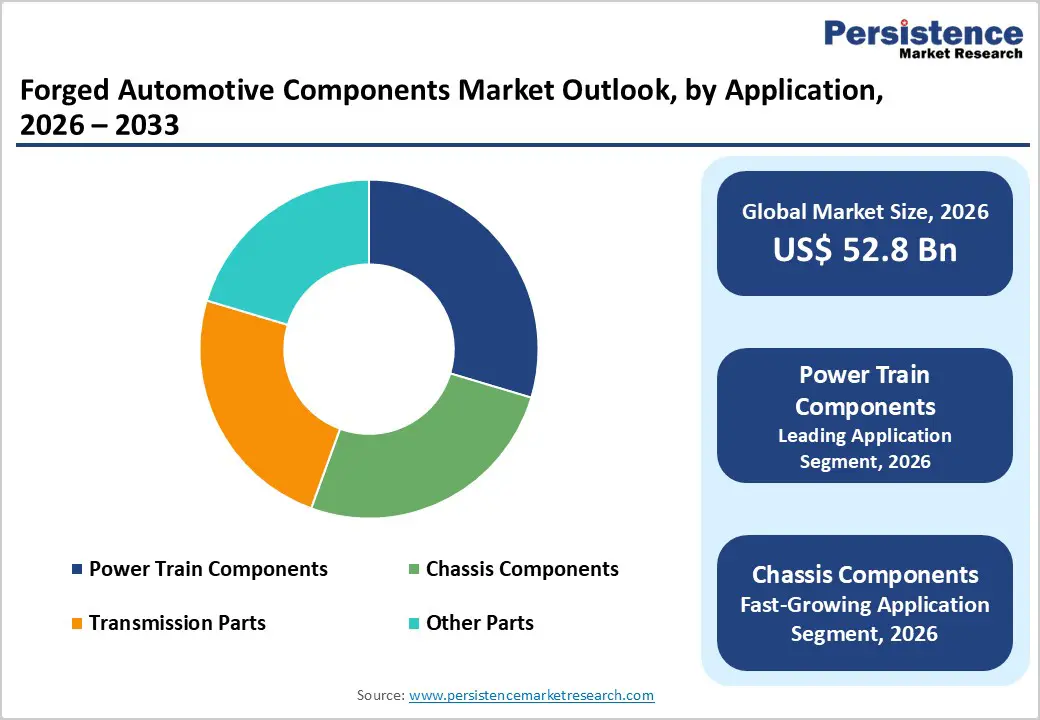

The global forged automotive components market size is expected to be valued at US$ 52.8 billion in 2026 and projected to reach US$ 74.3 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033. Increasing global vehicle production and accelerating electrification trends are key growth catalysts.

According to the International Organization of Motor Vehicle Manufacturers (OICA), 93 million vehicles were produced in 2023, reflecting steady automotive output recovery. The International Energy Agency reports EVs accounted for 18% of global vehicle sales, intensifying demand for high-strength, lightweight forged components in powertrain, chassis, and transmission applications to meet emission and performance standards.

Key Industry Highlights:

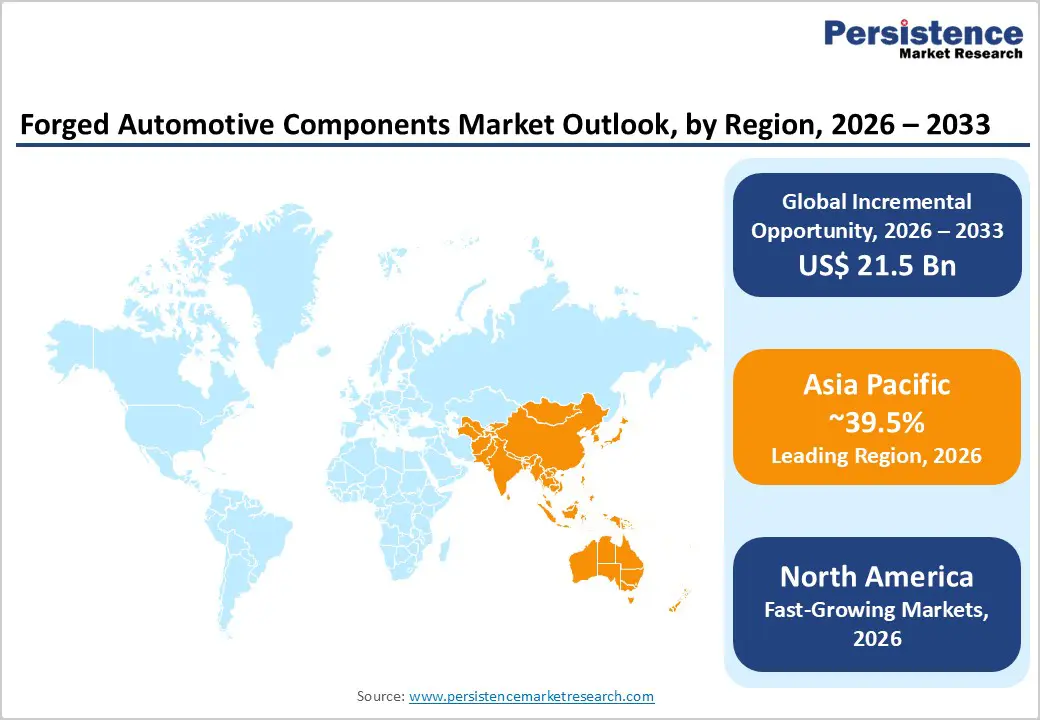

- Leading Region: Asia Pacific leads the forged automotive components market with a 39.5% share in 2025, supported by strong vehicle production across China, Japan, and India.

- Fastest-Growing Region: Europe is projected to expand at a CAGR of 4.8% during the forecast period, supported by electrification and emissions

- regulations.

- Leading Vehicle Type: Passenger vehicles dominate with a 55% share in 2025, driven by high global production volumes and demand for safety-critical forged components.

- Leading Forging Process: Impression die forging holds a 60% share in 2025, owing to its suitability for high-volume, precision automotive parts manufacturing.

- Key Opportunity: Lightweight aluminium forging adoption is accelerating, supported by EV-driven structural optimization and next-generation vehicle platform development.

| Key Insights | Details |

|---|---|

|

Forged Automotive Components Market Size (2026E) |

US$ 52.8 billion |

|

Market Value Forecast (2033F) |

US$ 74.3 billion |

|

Projected Growth CAGR(2026-2033) |

5.0% |

|

Historical Market Growth (2020-2025) |

4.3% |

Market Dynamics

Drivers - Accelerating Electric Vehicle Production Driving High-Performance Forged Component Demand

The rapid expansion of electric vehicle manufacturing is significantly increasing demand for forged automotive components engineered for superior fatigue resistance and torque handling. EV powertrains generate instant torque, requiring robust parts such as axles, gears, and transmission shafts to ensure durability and structural integrity. Forged components also enable up to 15% weight optimization, improving overall vehicle efficiency and battery performance.

According to the International Energy Agency, global EV stock is projected to reach 250 million units by 2030, with strong year-on-year sales growth. Automakers are integrating advanced forging technologies into production lines to enhance scalability and precision, reinforcing long-term demand across passenger and commercial EV segments.

Stringent Emission and Vehicle Safety Regulations Accelerating Adoption of Durable Lightweight Forgings

Tightening global emission and safety regulations are accelerating the adoption of forged components across automotive platforms. Standards such as EPA Phase 3 and Euro 7 emphasize lightweight construction and enhanced structural integrity, positioning forgings as preferred alternatives to cast components. High-strength steel forgings can achieve tensile strengths up to 1,500 MPa, supporting fuel efficiency and crash performance improvements.

Data from the National Highway Traffic Safety Administration (NHTSA) indicates improved vehicle structures contributed to a 5% decline in roadway fatalities in 2023. Additionally, global production trends reported by the International Organization of Motor Vehicle Manufacturers reinforce sustained OEM demand for advanced forged solutions.

Restraints - Volatility in Steel and Aluminium Prices Creating Cost Pressures Across Forging Operations

Fluctuations in steel and aluminium prices are creating margin pressures for forged automotive component manufacturers worldwide. Raw material costs represent a significant portion of total production expenses, and price swings of nearly 25% in 2024, as highlighted by the World Steel Association, have raised overall manufacturing costs by an estimated 15–20%. This volatility directly affects profitability and long-term pricing contracts with OEMs.

Smaller and mid-sized forging companies are particularly vulnerable due to their dependence on imported raw materials and limited hedging capabilities. Unstable input costs complicate procurement planning, restrict capital allocation for technology upgrades, and intensify competitive pressures within the global automotive supply chain.

High Capital Investment Requirements for Advanced Forging Equipment Limiting SME Expansion

The adoption of modern forging technologies requires substantial capital investment, creating barriers for small and medium-sized enterprises. Advanced hydraulic and mechanical presses can cost over US$ 10 million per unit, according to the International Forging Association, significantly raising entry thresholds for new participants and expansion plans for existing firms.

Additionally, companies typically allocate around 5% of annual revenue toward research and development to maintain competitiveness in precision forging and automation. During economic slowdowns or automotive demand fluctuations, such high fixed investment and R&D commitments strain cash flows and limit operational flexibility.

Opportunity - Expanding Demand for Lightweight Aluminium Forgings Supporting Electric Vehicle Efficiency Goals

The shift toward electric mobility is unlocking strong opportunities for lightweight aluminium forgings, particularly in EV chassis and structural systems. Aluminium forged components can deliver up to 30% weight reduction compared to traditional steel parts, directly improving battery efficiency and driving range. Government incentives, including clean mobility programs under the U.S. Inflation Reduction Act, are accelerating domestic EV manufacturing and component sourcing.

China’s long-term electrification targets further strengthen demand momentum, with ambitious industry expansion plans toward 2031. Strategic collaborations such as the Bharat Forge–Cummins partnership reflect growing investment in advanced lightweight solutions, supporting double-digit growth potential in specialized EV forgings.

Rising Commercial Vehicle Aftermarket Replacement Cycles Creating Localized Forging Opportunities

The aging global commercial vehicle fleet is generating consistent aftermarket demand for forged components, particularly axles, crankshafts, and transmission parts. According to the International Organization of Motor Vehicle Manufacturers, replacement cycles in commercial fleets contribute to steady component demand, with parts renewals rising annually as vehicles remain operational longer. This creates predictable revenue streams beyond OEM production volumes.

In emerging economies such as India, government-led infrastructure and logistics development schemes are stimulating heavy truck usage, further increasing forging requirements. Localized manufacturing expansion enables suppliers to reduce import dependency while capitalizing on sustained aftermarket growth.

Category-wise Analysis

Vehicle Type Insights

Passenger vehicles dominate the forged automotive components market, accounting for approximately 55% share in 2025, supported by strong global production volumes. According to the International Organization of Motor Vehicle Manufacturers, annual passenger vehicle output reached nearly 78 million units, reinforcing large-scale demand for safety-critical forged parts such as steering knuckles, crankshafts, and connecting rods. Premium automakers, including BMW, extensively utilize high-strength steel forgings to enhance crash performance and structural durability in sedans and SUVs. Light commercial vehicles are expected to be the fastest-growing segment, driven by e-commerce expansion, growth in last-mile delivery, and urban logistics demand. Increasing fleet modernization and the adoption of electrified LCV platforms are further accelerating the integration of forged components across chassis and drivetrain systems.

Forging Process Insights

Impression die forging leads the market with an estimated 60% share in 2025, owing to its suitability for producing high-volume, precision automotive components such as gears, shafts, and transmission parts. Mechanical presses enable consistent dimensional accuracy and high throughput, making the process ideal for OEM-scale manufacturing. Quality benchmarks such as the Japanese Industrial Standards ensure process reliability, particularly in Toyota-produced hybrid vehicles.

Cold forging is projected to grow the fastest, supported by its superior surface finish, minimal material waste, and cost efficiency for smaller, high-strength components. Growing demand for precision drivetrains and EV transmission parts further strengthens adoption.

Material Insights

Steel remains the dominant material segment, holding nearly 70% share in 2025 due to its excellent forgeability, tensile strength, and cost efficiency. With global steel production reaching approximately 1.9 billion tons annually, as reported by the World Steel Association, supply stability supports large-scale automotive applications. Steel forgings are widely used in crankshafts and axles, including high-performance models such as the Ford F-150, where durability and load-bearing capacity are critical.

Aluminium is expected to be the fastest-growing material category, driven by lightweighting initiatives and electrification trends. Its corrosion resistance and weight-saving potential make it increasingly attractive for EV chassis and suspension systems.

Automotive Component Insights

Crankshafts account for an estimated 25% share in 2025, reflecting their essential role in internal combustion engines and hybrid powertrains. Forged crankshafts deliver nearly twice the durability of crankshafts manufactured by alternative methods, as highlighted in technical studies by SAE International. High-performance engine platforms such as the Cummins ISX rely on forged crankshafts to withstand high rotational speeds and torque loads.

Gears are anticipated to be the fastest-growing component category, supported by transmission advancements and EV drivetrain requirements. Increasing torque outputs and precision performance standards are accelerating the need for high-strength forged gear systems.

Application Insights

Power train components lead the market with approximately 45% share in 2025, driven by strong demand for forged gears, connecting rods, and crankshafts that ensure torque transmission and mechanical efficiency. Forged components in powertrain systems can reduce energy losses in EVs by up to 15%, while handling torque levels exceeding 1,000 Nm in modern vehicle platforms. This dominance reflects the critical role of high-strength materials in the reliability of engines and transmissions.

Chassis components are projected to grow the fastest, driven by vehicle lightweighting, safety enhancements, and the integration of structural forged aluminium parts in next-generation electric and hybrid vehicles.

Regional Insights

North America Forged Automotive Components Market Trends and Insights

North America holds an estimated 28% share of the global forged automotive components market in 2025, led by the United States. Regulatory frameworks from the Environmental Protection Agency (EPA) emphasize emission reduction and lightweight vehicle structures, boosting demand for high-strength forged components. Automakers such as General Motors have announced multi-billion-dollar investments in EV development, reinforcing the need for long-term forging across powertrain and chassis applications.

Ongoing R&D support from the U.S. Department of Energy enhances cold forging and material innovation, while crash safety standards from the National Highway Traffic Safety Administration further favor structurally robust forged components.

Europe Forged Automotive Components Market Trends and Insights

Europe represents a technologically advanced forging market, driven by strong automotive manufacturing hubs in Germany, France, and Italy. The region is projected to grow at a CAGR of approximately 4.8% during the forecast period, supported by regulatory pressure and premium vehicle production. Safety assessments conducted by Euro NCAP have encouraged automakers to enhance structural integrity, increasing the adoption of forged steering knuckles and chassis components.

The European Green Deal aims to achieve zero-emission mobility by 2035, accelerating investments in electrification. Major automotive groups such as Stellantis are expanding EV production capacity, strengthening demand for lightweight aluminium and advanced steel forgings across regional supply chains.

Asia Pacific Forged Automotive Components Market Trends and Insights

Asia Pacific dominates the forged automotive components market, accounting for approximately 39.5% share in 2025, supported by large-scale vehicle production across China, Japan, and India. Policy backing from China’s Ministry of Industry and Information Technology (MIIT) continues to strengthen domestic automotive output, with production capacity exceeding 30 million vehicles annually. Strong OEM clusters, cost-competitive manufacturing, and integrated steel supply chains further consolidate the region’s leadership position.

The region is also the fastest-growing market, driven by EV expansion, infrastructure development, and commercial vehicle demand. India’s Automotive Mission Plan 2026 (AMP 2026) promotes domestic manufacturing and exports, accelerating investment in advanced forging technologies and localized component production.

Competitive Landscape

The forged automotive components market is moderately consolidated, with leading manufacturers maintaining a strong global presence through integrated production capabilities and long-term OEM partnerships. Companies are expanding manufacturing footprints across Asia Pacific to leverage cost advantages, proximity to vehicle production hubs, and growing EV demand. Strategic capacity additions and supply chain localization remain key competitive priorities.

Firms typically allocate 4–6% of annual revenue toward research and development, focusing on sustainable forging processes, lightweight materials, and energy-efficient operations. Adoption of digital twins, simulation-based design, and advanced automation technologies is increasingly differentiating players in terms of precision, cost optimization, and faster product development cycles.

Key Developments:

- In June 2025, Bharat Forge commissioned a new aluminum-focused electric vehicle forging facility in India, increasing its production capacity by approximately 30% to address rising demand for lightweight EV chassis and structural components across domestic and export markets.

- In March 2024, Thyssenkrupp announced a €200 million investment in green forging technologies, focusing on low-carbon steel processing, energy-efficient furnaces, and sustainable manufacturing practices aligned with Europe’s decarbonization objectives.

- In October 2024, American Axle & Manufacturing expanded its seamless rolled ring forging operations in Mexico, increasing capacity by nearly 20% to support growing regional demand for drivetrain and commercial vehicle components.

Segmentation of Forged Automotive Components Industry Research

By Vehicle Type

- Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Vehicles

By Forging Process

- Impression Die Forging

- Hydraulic Presses

- Mechanical Presses

- Hammers

- Cold Forging

- Open Die Forging

- Seamless Rolled Ring Forging

By Material

- Steel

- Aluminium

- Other

By Automotive Component

- Connecting rods

- Injectors

- Gears

- Crankshafts

- Axles

- Bearings

- Pistons

- Steering Knuckles

- CV Joints

- Others

By Application

- Power Train Components

- Chassis Components

- Transmission Parts

- Other Parts

By Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Companies Covered in Forged Automotive Components Market

- ThyssenKrupp AG

- CIE Automotive

- NTN Corporation

- American Axle and Manufacturing Inc.

- Bharat Forge Limited

- Ramkrishna Forgings

- Dana Limited

- Meritor Inc.

- ZF Friedrichshafen AG

- Kalyani Group

- Om Forge

- Super Auto Forge Private Limited

- GAZ Group

- TBK Co., Ltd.

- EL FORGE LIMITED

Frequently Asked Questions

The forged automotive components market is projected to reach US$ 52.8 billion in 2026, driven by steady vehicle production and electrification trends.

Rising electric vehicle adoption, projected to reach 250 million units globally by 2030 according to the International Energy Agency, is a major demand driver for high-strength forged components.

Asia Pacific leads the market with a 39.5% share in 2025, supported by strong automotive manufacturing hubs across China, Japan, and India.

Lightweight aluminium forgings for EV applications present a strong opportunity, enabling up to 30% weight reduction in structural and chassis components.

Key participants include ThyssenKrupp AG, CIE Automotive, NTN Corporation, American Axle and Manufacturing Inc., and Bharat Forge Limited.