- Hardware & Software IT Services

- Flash-Based Array Market

Flash-Based Array Market Size, Share, and Growth Forecast, 2026 - 2033

Flash-Based Array Market By Product Type (All-flash Array, Hybrid Flash Array), Enterprise Type (Large Enterprise, SMEs), Storage Capacity (Less than 100 TB, 100 TB to 500 TB, 500 TB to 1 PB, More than 1 PB), End-user Vertical, and Region Analysis 2026 to 2033

Market Overview

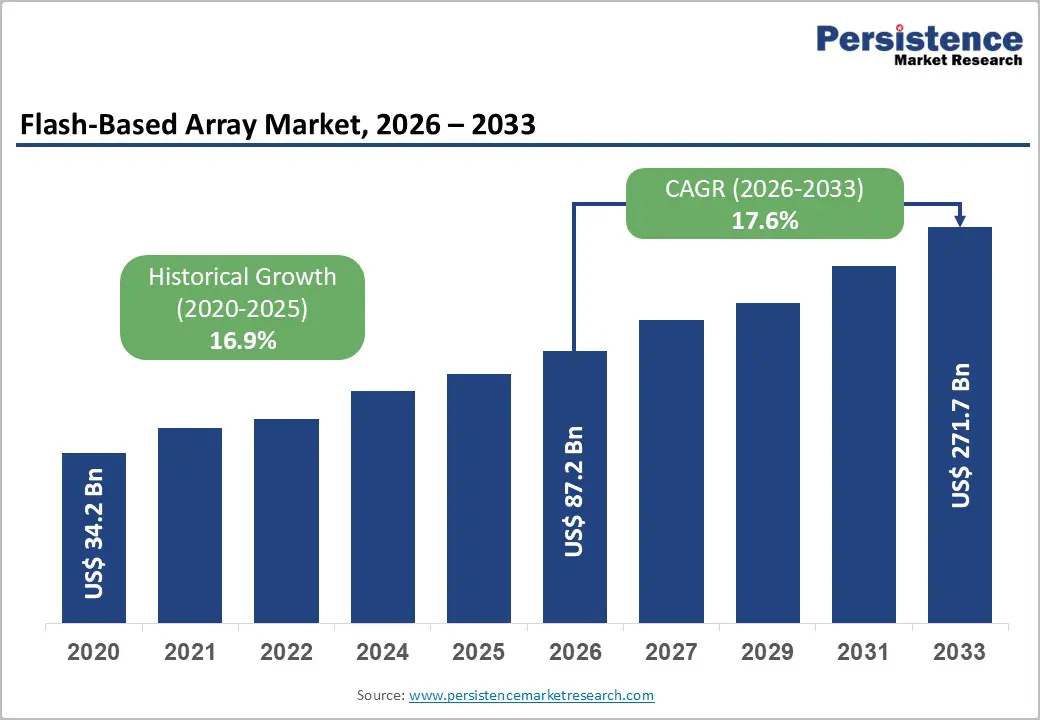

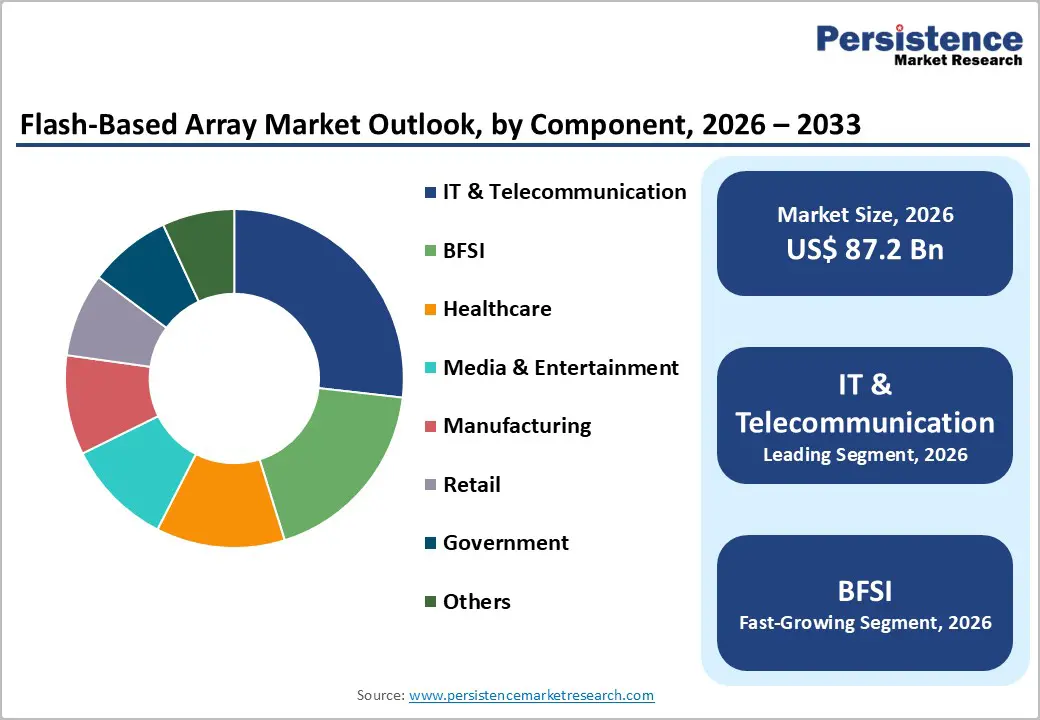

The global Flash-Based Array Market size is projected to be valued at US$87.2 Billion in 2026 and is anticipated to reach US$271.7 Billion by 2033, growing at a CAGR of 17.6% between 2026 and 2033. This expansion is driven by exponential data growth reaching 181 zettabytes globally by 2025, cloud computing adoption exceeding 94% among enterprises, and digital transformation investments surpassing US$2.3 trillion worldwide. Flash storage performance advantages delivering 100x faster data access than traditional disk arrays, declining NAND flash prices by 56%, and edge computing requirements processing 75% of enterprise data outside centralized data centers further accelerate market adoption.

Key Market Highlights

- All-flash Arrays lead with 60% share and fastest growth; Hybrid Flash Arrays deliver cost-effective performance at 14.8% CAGR.

- Large Enterprises dominate with 70% share for petabyte-scale workloads; SMEs grow fastest at 20.1% CAGR driven by cloud adoption.

- >1 PB systems lead with 30% share, while 500 TB–1 PB grows 17.4% CAGR for mid-sized deployments.

- IT & Telecom verticals lead at 27% share; BFSI accelerates fastest at 19.6% CAGR for real-time, low-latency workloads.

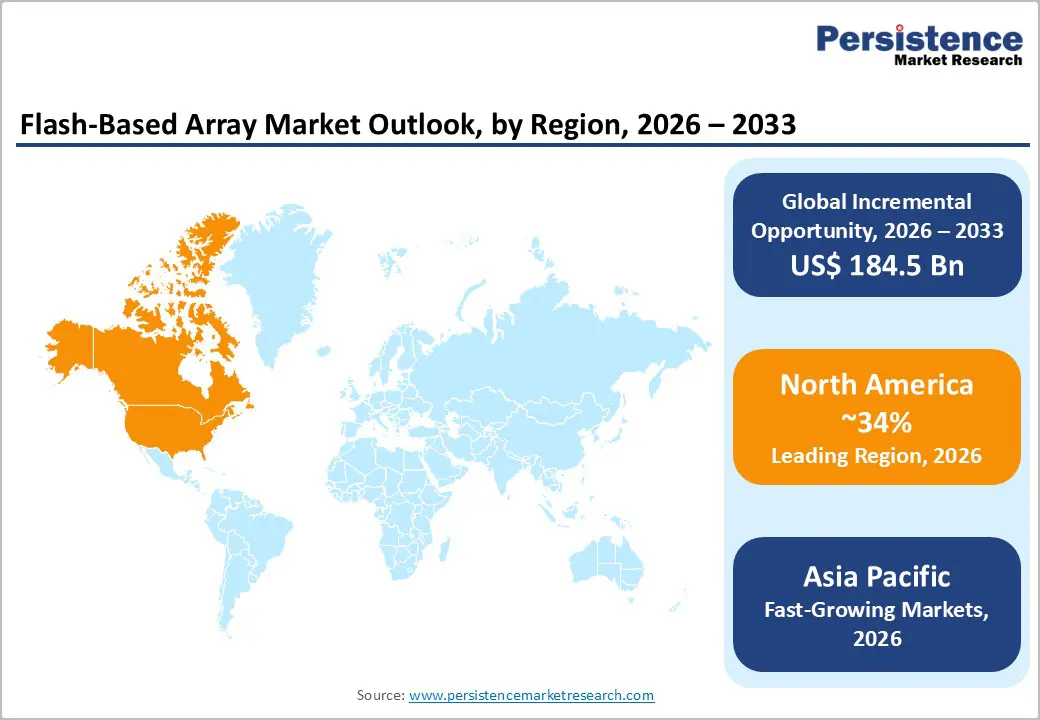

- North America holds 34% share with 340 hyperscale data centers; Asia Pacific grows 18.5% CAGR fueled by China’s investments.

- Strategic focus: NVMe boosts performance 70%, software acquisitions enhance data management, and storage-as-a-service targets 35% market growth.

| Key Insights | Details |

|---|---|

| Flash-Based Array Market Size (2026E) | US$ 87.2 billion |

| Market Value Forecast (2033F) | US$ 271.7 billion |

| Projected Growth CAGR (2026-2033) | 17.6% |

| Historical Market Growth (2020-2025) | 16.9% |

Market Dynamics Analysis

Market Drivers

Explosive Data Growth and Real-Time Analytics Requirements

Global data creation has reached unprecedented levels, with the International Data Corporation reporting 120 zettabytes generated in 2023 and projecting 181 zettabytes by 2025, reflecting 51% compound annual growth. The U.S. Department of Commerce notes enterprise data volumes double every 18 months, intensifying storage infrastructure challenges. Flash-based arrays enable real-time processing for artificial intelligence, machine learning, and advanced analytics requiring sub-millisecond latency. Financial institutions execute 2.8 million high-frequency trades per second, demanding instantaneous storage response. Autonomous vehicle systems process nearly four terabytes of sensor data daily, requiring high-performance architectures. The World Economic Forum reports flash adoption delivers 67% application performance improvement and 54% faster data processing. Healthcare providers rely on flash arrays to support medical imaging, genomics, and electronic records.

Digital Transformation and Mission-Critical Application Modernization

Corporate digital transformation initiatives are accelerating flash array adoption, with Accenture reporting US$2.3 trillion in enterprise investments through 2025 to modernize applications and infrastructure. Migrating legacy databases from disk to flash improves transaction processing by 10–25x, enabling real-time customer experiences and operational insights. The European Commission’s Digital Europe Programme allocates €7.5 billion to digital capabilities requiring high-performance storage. SAP HANA in-memory deployments depend on flash arrays supporting real-time analytics across multi-terabyte datasets, with 12,400 enterprise implementations worldwide. E-commerce platforms processing millions of peak-period transactions rely on flash arrays to avoid revenue loss from latency. Telecommunications providers rolling out 5G use flash storage for network virtualization, as GSMA projects US$1.3 trillion in 5G investments through 2030 supporting network slicing and edge.

Market Restraints

High Initial Capital Expenditure and Budget Constraints

Flash-based array implementations demand substantial upfront investment, with enterprise all-flash systems costing US$450,000 to US$2.8 million based on capacity and performance. Budget constraints persist, as 64% of IT departments report insufficient funding for storage modernization. Total cost of ownership, including licensing, services, and support, raises initial costs by 65–85%. SMEs face barriers, citing storage costs as key obstacles to cloud adoption. Replacement cycles of 4–5 years drive recurring capital expenditure, while US$89 billion in legacy infrastructure sunk costs fuels resistance.

NAND Flash Supply Chain Volatility and Price Fluctuations

Flash storage markets face pronounced price volatility driven by NAND manufacturing cycles. The Semiconductor Industry Association reports NAND prices fluctuated 67% between 2020 and 2023, creating procurement uncertainty and margin pressure for vendors. Geographic concentration, with 92% of production capacity in Asia Pacific, heightens supply chain risk during geopolitical tensions and pandemics. New fabrication facilities require US$8–15 billion investments and 18–24 months to build, limiting flexibility. Transitions to 3D NAND increase complexity, with 47% of new lines facing yield issues.

Market Opportunities

Edge Computing and IoT Data Processing Requirements

Edge computing infrastructure represents a US$155.9 billion opportunity by 2030, requiring flash storage for distributed processing, local analytics, and real-time decision making. International Data Corporation projects 75% of enterprise data will be processed outside centralized data centers by 2025, increasing demand for high-performance edge storage. Internet of Things deployments reached 16.7 billion connected devices in 2023 and are projected to exceed 29 billion by 2030, generating data needing localized flash processing. Manufacturing facilities deploy edge analytics for predictive maintenance and quality control, retail stores rely on local transaction processing during network disruptions, and autonomous vehicles require onboard flash storage for sensor data. Expanding 5G networks enable edge applications across augmented reality, autonomous systems, and smart cities, driving flash array deployment.

NVMe and Storage Class Memory Technology Integration

Non-Volatile Memory Express and storage class memory technologies represent opportunities, delivering sixfold performance gains over traditional storage interfaces. NVMe over Fabrics enables shared flash across distributed environments with sub-100 microsecond latency, supporting high-frequency trading, real-time fraud detection, and AI model training workloads. The Storage Networking Industry Association reports NVMe adoption has grown 240 percent since 2020, with enterprises achieving 67 percent reductions in application response times. Storage class memory technologies, including Intel Optane and persistent memory, provide tenfold performance and thousandfold endurance improvements, enabling new application architectures. This convergence represents a US$48.6 billion opportunity by 2030 as organizations modernize infrastructure for next-generation workloads. Cloud service providers deploy NVMe-based flash arrays to reduce infrastructure costs by 35 percent while enhancing quality.

Segmentation Analysis

Product Type Analysis

All-flash array systems command a leading 60% market share, delivering maximum performance, minimal latency, and high reliability for mission-critical enterprise workloads. These systems eliminate mechanical components, using NAND flash exclusively to ensure consistent sub-millisecond response across workloads. All-flash arrays support databases, virtual desktop infrastructure, online transaction processing, and real-time analytics demanding predictable performance. Advancements such as NVMe interfaces, 5:1 data reduction, and quality-of-service controls improve utilization. Manufacturing efficiencies have reduced costs 56% globally.

Hybrid flash array systems grow at 14.8% CAGR, combining flash for active data with disk for capacity workloads, delivering cost-effective flexibility. Intelligent tiering automatically shifts frequently accessed data to flash while storing cold data on disk, optimizing performance-to-cost ratios for enterprises balancing budget constraints and mixed application requirements efficiently globally.

Enterprise Type Analysis

Large enterprises hold 70% market share, supported by sizable IT budgets, complex application portfolios, and extensive data management needs. Organizations exceeding 1,000 employees manage petabyte-scale data across multiple data centers, requiring enterprise-grade storage with high availability, data protection, and global replication. Fortune 500 firms allocate 18–24% of IT budgets to storage, with flash arrays comprising 67% of new acquisitions, prioritizing reliability, vendor support, and long-term partnerships over cost sensitivity and predictable multi-year investment planning.

Small and medium enterprises represent the fastest-growing segment at 20.1% CAGR through 2033, driven by cloud-based flash services, declining system prices, and rising performance needs. SMEs adopt flash arrays as subscription models remove upfront capital costs, while software-defined storage and hyperconverged infrastructure broaden access for resource-constrained organizations across diverse industries.

Storage Capacity Analysis

More than 1 PB capacity systems command segment leadership with 30% market share, serving hyperscale cloud providers, telecom operators, and large enterprises managing massive data volumes. Petabyte-scale deployments support data lakes, genomic databases, media libraries, and artificial intelligence training workloads requiring flash performance at scale. Advancements in high-density NAND, data reduction, and controller efficiency enable 100+ terabyte arrays, making petabyte configurations economically viable. Major cloud providers including Amazon, Microsoft, and Google account for 45% of large-capacity flash flash purchases, driving sustained growth.

Systems ranging from 500 TB to 1 PB grow at 17.4% CAGR, serving mid-sized cloud providers and enterprises consolidating workloads. This segment supports video surveillance, medical imaging, and scientific research, offering an optimal balance of performance, scalability, and cost efficiency for large but sub-petabyte data environments.

End User Vertical Analysis

IT & Telecommunication leads verticals with 27% market share, encompassing cloud providers, telecom operators, managed service providers, and technology firms requiring high-performance storage. Cloud providers deploy flash arrays for infrastructure-, platform-, and software-as-a-service offerings serving millions globally. Telecom operators utilize flash for 5G networks, content delivery, and customer applications demanding low-latency performance. Managed service providers deliver differentiated enterprise performance while optimizing data center efficiency, and technology companies leverage flash storage for software development, continuous integration pipelines, and product testing, enabling rapid provisioning and high throughput across critical workloads.

BFSI emerges as the fastest-growing vertical at 19.6% CAGR, driven by real-time transaction processing, algorithmic trading, fraud detection, and regulatory compliance. Financial institutions process billions of daily transactions, requiring sub-millisecond latency. High-frequency trading systems demand flash arrays for extreme performance, ensuring competitive advantage and revenue protection.

Regional Market Insights

North America

North America commands a 34% market share, valued near US$29.65 billion in 2026, driven by hyperscale cloud concentration, early adoption, and enterprise IT spending exceeding US$1.8 trillion annually. The United States leads flash array deployment, with major cloud providers operating 340 hyperscale data centers requiring petabyte-scale flash infrastructure. Financial institutions on Wall Street deploy flash arrays for algorithmic trading and risk analytics, while healthcare organizations support electronic health records and medical imaging serving 330 million patients. Silicon Valley firms rely on flash storage for artificial intelligence development, software testing, and continuous integration. Federal agencies adopt flash arrays for defense, intelligence, and citizen services demanding security and performance. Competitive dynamics remain intense among established vendors and software-defined entrants across the region.

Europe

Europe demonstrates steady growth at a 27.6% CAGR, shaped by data sovereignty requirements, GDPR compliance, and digital transformation across manufacturing and financial services. Germany leads adoption through automotive and industrial deployments using flash storage for Industry 4.0 applications such as robotics control, quality management, and supply chain optimization. The United Kingdom maintains strong presence in financial services, with London institutions deploying flash arrays for transaction processing and regulatory compliance. France advances healthcare and public sector implementations, while Spain records growth in telecommunications and media workloads. European Union data residency regulations drive localized data center investments and flash deployments. Horizon Europe allocates €95 billion for digital infrastructure through 2027. Sustainability priorities influence procurement, as energy-efficient flash reduces power consumption by 65% versus disk arrays. Privacy mandates accelerate encrypted flash adoption regionally.

Asia Pacific

Asia Pacific demonstrates strong growth at 18.5% CAGR, driven by cloud infrastructure expansion, manufacturing digitalization, and government digital economy initiatives. China leads development as Alibaba, Tencent, and Huawei deploy flash infrastructure supporting 1.05 billion internet users and an e-commerce sector generating US$2.8 trillion annually. Data localization policies accelerate domestic data center construction, with US$89 billion invested through 2027. Japan contributes through automotive, electronics, and financial services deployments, while India is the fastest-growing market, with cloud adoption rising 47% annually under Digital India programs. ASEAN nations benefit from multinational data center investments, as Singapore, Malaysia, and Indonesia attract US$34 billion by 2026. Regional dominance in NAND manufacturing provides cost advantages and supply proximity. Government semiconductor policies further stimulate flash innovation regionally.

Competitive Landscape

Strategic Developments

- In March 2022, NetApp and Cisco launched FlexPod XCS, an upgraded platform integrating storage, networking, and server technologies to streamline deployment and management of applications and data across hybrid cloud environments.

Business Strategies

Market leaders pursue software-defined storage strategies emphasizing data services, automation, and consumption-based pricing models generating recurring revenue. Innovation focus centers on NVMe optimization, AI-powered storage management, and multi-cloud integration delivering operational simplicity and performance improvements. Strategic partnerships with hyperscale cloud providers enable hybrid cloud offerings combining on-premises flash arrays with cloud storage services. Vertical market specialization addresses industry-specific requirements in financial services, healthcare, and telecommunications with pre-configured solutions and compliance frameworks. As-a-service business models lower customer acquisition barriers while improving predictable revenue streams.

Companies Covered in Flash-Based Array Market

- Dell Technologies Inc.

- Pure Storage, Inc.

- NetApp, Inc.

- Hewlett Packard Enterprise

- Hitachi Vantara Corporation

- IBM Corporation

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- Lenovo Group Limited

- Oracle Corporation

- Infinidat Ltd.

- DDN Storage

- Kioxia Corporation

- Western Digital Corporation

- Samsung Electronics Co., Ltd.

Frequently Asked Questions

The Flash-Based Array Market is projected at US$87.20 Billion in 2026, expanding to US$271.73 Billion by 2033.

Primary drivers include explosive global data growth doubling rapidly, widespread cloud adoption, massive investments in digital transformation modernizing mission-critical applications, and significantly faster performance over traditional disk storage, enabling real-time analytics and advanced AI workloads.

The market is projected to grow at a CAGR of 17.6% between 2026 and 2033.

Major opportunities include rapid expansion of edge computing enabling local processing of the majority of enterprise data, substantial emerging market infrastructure investments with significant allocation to data centers, and adoption of NVMe and storage class memory technologies delivering dramatically higher performance and faster application response times.

Leading players include Dell Technologies, Pure Storage, NetApp, Hewlett Packard Enterprise, Hitachi Vantara, IBM Corporation, Huawei Technologies, Cisco Systems, Lenovo Group, Oracle Corporation, Infinidat, DDN Storage, Kioxia Corporation, Western Digital, and Samsung Electronics.