- Automotive Components & Materials

- Fifth Wheel Coupling Market

Fifth Wheel Coupling Market Size, Share, and Growth Forecast 2026 - 2033

Fifth Wheel Coupling Market by Product (Compensating, Semi-oscillating, Fully-oscillating), by Operation (Hydraulic, Pneumatic, Mechanical), by Material (Cast Steel, Cast Iron, Fabricated Steel, Aluminum, Others), Sales Channel (OEMs, Aftermarket), and Regional Analysis, 2026-2033

Fifth Wheel Coupling Market Size and Trend Analysis

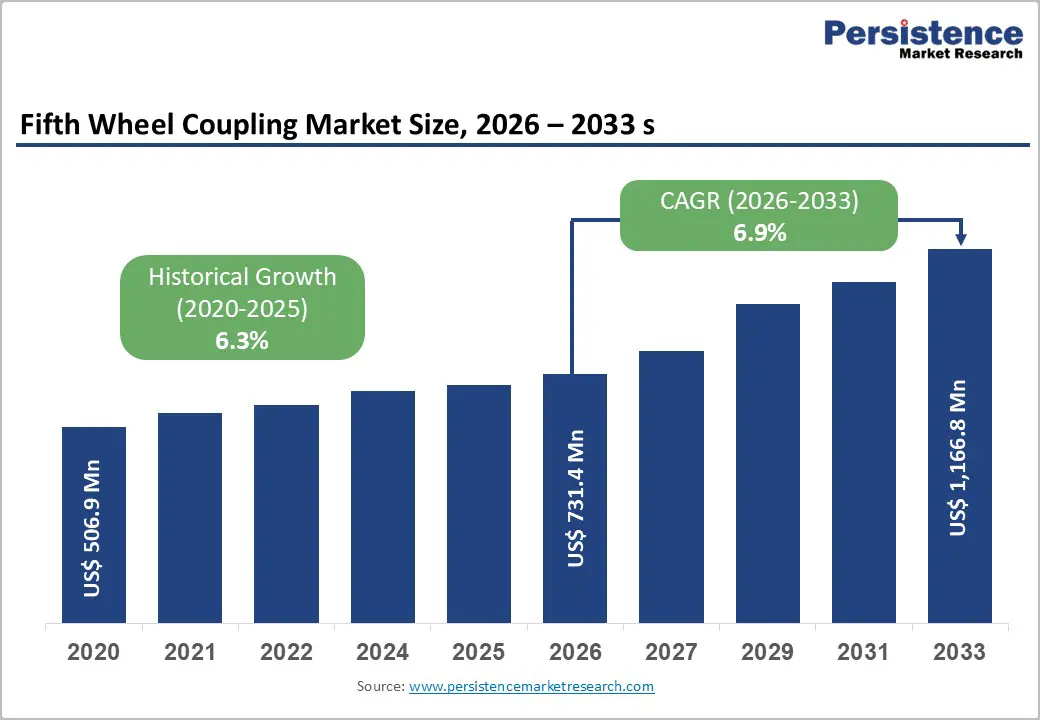

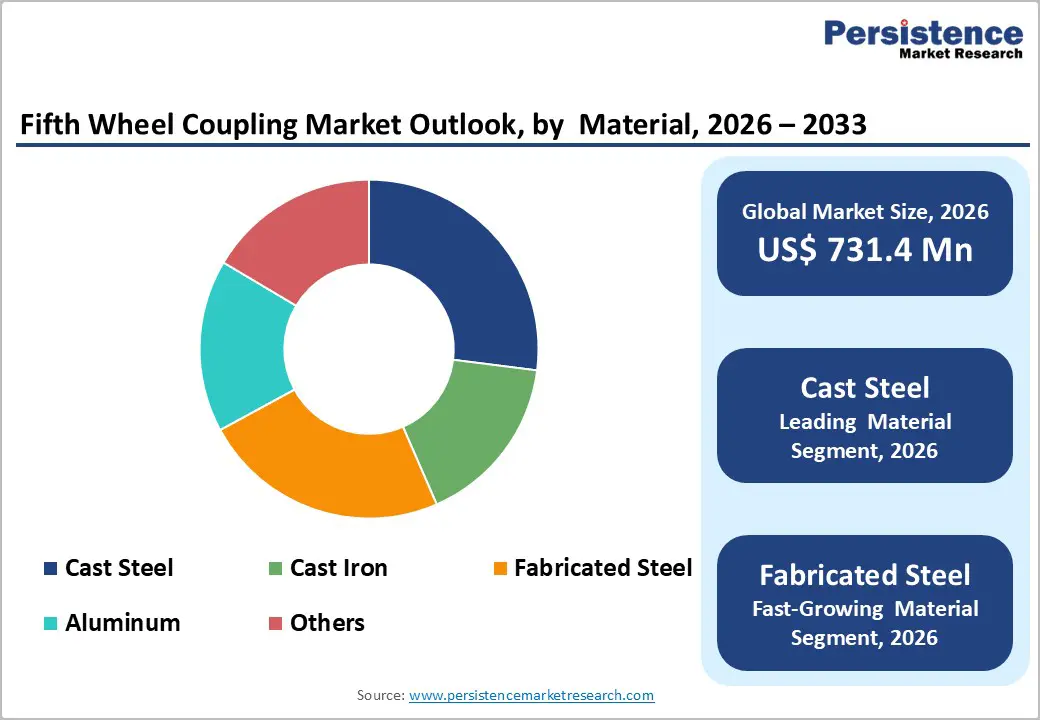

The global fifth wheel coupling market size is expected to be valued at US$ 731.4 million in 2026 and projected to reach US$ 1,166.8 million by 2033, growing at a CAGR of 6.9% between 2026 and 2033.

This growth is primarily driven by increasing commercial vehicle production and rising logistics demands worldwide. The expanding freight transportation sector, coupled with stricter safety and regulatory standards, is accelerating the adoption of reliable and durable fifth wheel couplings. Regions such as North America are witnessing steady fleet expansions, while emerging markets are seeing growing demand for heavy-duty transportation solutions, further boosting market prospects.

Key Industry Highlights:

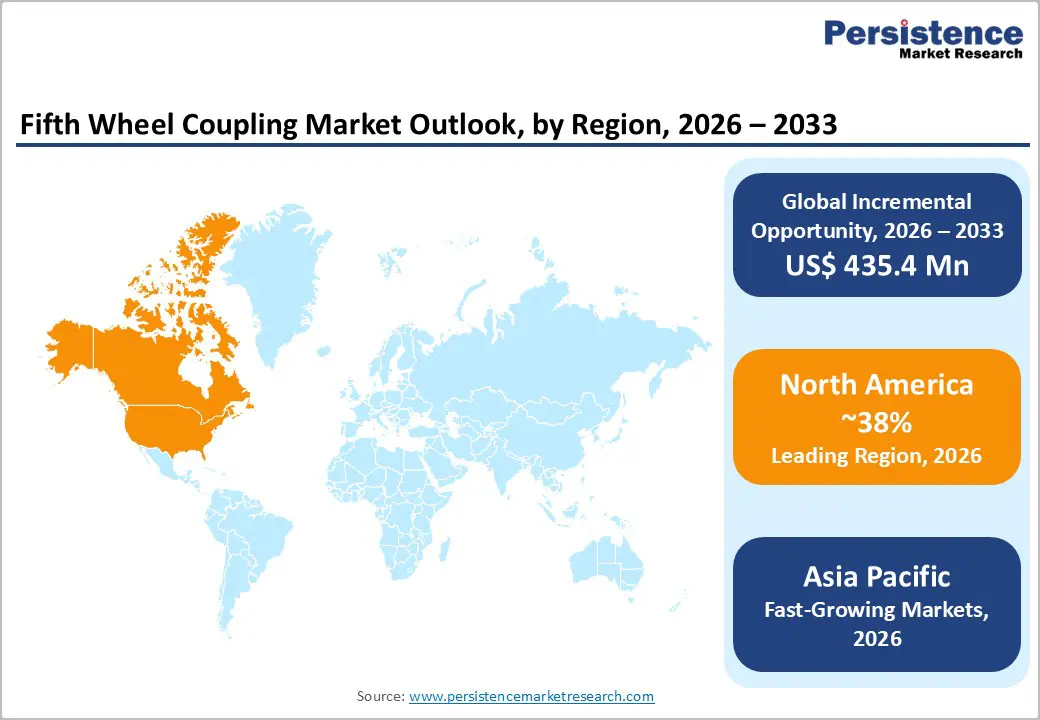

- Leading Region: North America commands a leading position with 38% share in 2025, supported by strong trucking infrastructure, fleet expansions, and stringent safety regulations.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with 36% share in 2025 and a projected CAGR exceeding 6.5%, driven by infrastructure development and expanding e-commerce logistics in China and India.

- Leading Product Category: Semi-oscillating couplings dominate with 57% share in 2025, offering versatile pivoting and enhanced stability for long-haul transport operations.

- Fastest-Growing Product Category: Fully oscillating couplings are the fastest-growing segment, favored for off-road, construction, and specialized hauling applications.

- Key Opportunity: Electric vehicle integration presents a major growth avenue, as EV semi-trailer fleets are projected to expand 25% annually, requiring couplings with higher torque tolerance and smart features.

| Key Insights | Details |

|---|---|

| Fifth Wheel Coupling Size (2026E) | US$ 731.4 Million |

| Market Value Forecast (2033F) | US$ 1,166.8 Million |

| Projected Growth CAGR(2026-2033) | 6.9% |

| Historical Market Growth (2020-2025) | 6.3% |

Market Dynamics

Drivers

Strong Growth in Commercial Vehicle Production and Expanding Logistics Demand

The rapid growth of global logistics and e-commerce sectors has significantly increased the demand for fifth wheel couplings. Rising freight volumes, particularly in international road transport, have grown by over 5% annually across major regions. This surge in transportation activity drives higher production of trucks and semi-trailers, creating a direct correlation with coupling installations. Consequently, manufacturers experience sustained market growth and stability.

In addition, rising commercial vehicle sales, which reached record highs in 2025, further boost demand for reliable trailer connections. As fleet operators prioritize efficiency and durability, the market for advanced fifth wheel systems expands steadily, supporting both OEM and aftermarket segments while enhancing overall industry revenue.

Increasing Adoption Due to Stricter Safety and Regulatory Standards

Stringent safety regulations worldwide are driving the adoption of advanced fifth wheel couplings. Standards such as ECE-R55 in Europe and FMVSS in the U.S. mandate robust designs to prevent accidents like jackknifing and ensure secure load handling. Manufacturers are innovating locking mechanisms and durable materials to comply with these mandates, reducing accident risks by up to 20% in monitored fleets.

The emphasis on safety not only improves operator confidence but also encourages faster integration of modern coupling technologies in both new and existing vehicles. Regulatory compliance has become a key factor for fleet operators and OEMs, boosting market penetration while promoting safer, more efficient heavy-duty transport solutions.

Restraints

High Upfront Investment and Ongoing Maintenance Costs Limiting Adoption

Premium fifth wheel coupling systems require substantial initial investment, which can deter smaller fleet operators from upgrading. Advanced models are priced 30–50% higher than basic variants, putting pressure on operational budgets, especially amid fluctuating fuel costs. The significant upfront expense often delays procurement decisions, reducing market penetration in cost-sensitive regions and smaller fleet segments.

Beyond the purchase price, these systems require regular maintenance, including lubrication, inspection, and occasional component replacement. The cumulative ownership costs increase total operational expenses, making fleets cautious about widespread adoption. High maintenance needs also add logistical and labor demands, further constraining growth in emerging and budget-conscious markets.

Production Challenges and Supply Chain Vulnerabilities Affecting Market Growth

Global fifth wheel coupling production is increasingly affected by supply chain disruptions, including geopolitical tensions and raw material shortages. Steel price volatility surged by 15% in 2025, impacting the manufacturing of cast components and delaying production schedules. These challenges contribute to longer lead times, inconsistent availability, and operational planning difficulties for fleet operators.

Extended delivery timelines can cause fleet downtime, reducing operational efficiency and eroding confidence among truck and trailer operators. Inconsistent supply also limits manufacturers’ ability to meet growing demand, slowing overall market expansion. Consequently, these production and logistical hurdles act as key restraints on the fifth wheel coupling industry.

Opportunities

Growing Opportunities from Electric and Autonomous Vehicle Integration

The growing adoption of electric and autonomous trucks presents significant opportunities for the fifth wheel coupling market. EV semi-trailer fleets are projected to expand at approximately 25% annually through 2032, creating demand for couplings designed to handle higher torque and automated hitching. Innovative systems with smart sensors improve operational safety and efficiency, catering to the unique requirements of these advanced vehicles.

Government initiatives, such as the EU Green Deal, further incentivize lightweight, durable coupling designs. Manufacturers that align with these regulations and integrate technology-enabled features can capture new revenue streams. The push for sustainability and automation in freight transportation ensures long-term growth potential for advanced fifth wheel solutions.

Expanding Infrastructure in Emerging Markets Driving Demand

Rapid development of highway and transport infrastructure in Asia Pacific, particularly in China and India, is fueling market expansion. Governments plan investments exceeding US$ 500 billion in road networks by 2030, stimulating semi-trailer adoption for bulk transport. This growth increases the demand for durable fifth wheel couplings, especially in construction and heavy logistics operations.

High-growth segments, including fully oscillating and robust coupling types, are gaining traction in off-road and industrial applications. As emerging markets expand their freight and construction capabilities, manufacturers have strong opportunities to supply tailored coupling solutions that meet durability and safety requirements while supporting expanding commercial transport networks.

Category-wise Analysis

Product Insights

The semi-oscillating type leads with approximately 57% share in 2025, favored for its versatility across varied terrains. It provides controlled pivoting and better handling during turns, minimizing jackknifing risks in long-haul operations. Fleet operators in North America widely adopt it for highway stability and reliability, enhancing operational efficiency. Its durable design supports heavy loads and long-distance freight, making it a preferred choice for logistics companies.

The fully oscillating fifth wheel is the fastest-growing segment, gaining traction in construction and off-road transport applications. Its enhanced articulation allows vehicles to navigate uneven or rugged terrain without compromising trailer stability. Fleet operators increasingly adopt this type for specialized hauling tasks, particularly in infrastructure projects and emerging markets, where versatility and durability are critical.

Operation Analysis

Mechanical operation dominates with around 50% share in 2025, appreciated for its simplicity, robustness, and low maintenance. Unlike pneumatic or hydraulic systems, it does not rely on air or fluid circuits, making it ideal for heavy-duty applications and remote locations with limited service access. ECE-R55 compliance ensures high reliability under extreme loads, driving preference among logistics and fleet operators globally.

The semi-automatic and automatic operations are growing rapidly due to rising demand for time-saving, user-friendly couplings. These systems reduce manual effort and streamline trailer attachment, improving operational efficiency in busy fleet operations. Adoption is especially notable in regions with modernized logistics infrastructure and automated trucking fleets.

Material Insights

Cast steel holds a leading 45% market share in 2025, favored for high tensile strength, impact resistance, and superior weldability compared to cast iron. Its ability to withstand extreme loads, low corrosion rates, and extended service life reduces downtime for fleet operators, making it a standard choice in heavy-duty trucking applications. Durable and reliable, it meets global safety standards and supports long-haul transport operations efficiently.

Composite and alloy-based materials are the fastest-growing segment, driven by lightweight, corrosion-resistant designs. These materials enhance fuel efficiency and reduce vehicle weight while maintaining adequate strength for demanding freight operations. Manufacturers are increasingly experimenting with advanced alloys to meet sustainability and performance requirements.

Sales Channel Insights

OEMs lead the market with roughly 60% share in 2025, as couplings are integrated directly into new vehicle assembly lines. Established manufacturers provide standardized units compliant with international safety regulations, ensuring consistent quality. Long-term contracts with major truck producers, especially in North America and Europe, solidify OEM dominance, supporting high-volume adoption in new commercial vehicles.

Aftermarket sales are the fastest-growing channel, fueled by fleet expansions, trailer retrofits, and replacement needs. Operators increasingly prefer flexible solutions for upgrades and maintenance, creating opportunities for distributors and service providers to supply high-quality coupling systems to existing fleets.

Regional Insights

North America Fifth Wheel Coupling Market Trends

North America dominates the global fifth wheel coupling market, holding approximately 38% share in 2025, driven by extensive trucking networks and high freight volumes. The U.S. alone operates over 3.5 million semi-trucks, creating substantial demand for reliable couplings. Stringent FMVSS 121 safety regulations mandate advanced designs, including no-tilt and smart couplings, ensuring higher adoption across fleets.

Innovation and R&D investment further strengthen the region, with manufacturers like SAF-Holland expanding specialty facilities to develop durable and technologically advanced fifth wheels. Fleet operators prioritize stability, efficiency, and compliance, solidifying North America’s leadership position. Continuous fleet expansions and modernized logistics systems sustain growth in both OEM and aftermarket channels.

Europe Fifth Wheel Coupling Market Trends

Europe’s market is growing steadily, with a CAGR of 7.1%, supported by rising truck electrification and harmonized safety standards under EU ECE-R55. Germany leads with 316,928 new truck registrations in 2024, while the U.K., France, and Spain follow closely, ensuring consistent demand for modern couplings. Policies targeting 65% CO2 reduction by 2035 promote lightweight and durable fifth wheel designs.

Manufacturers focus on innovation, integrating eco-friendly materials and automation-ready systems to meet stringent regulatory requirements. The region’s emphasis on sustainability, safety, and fleet modernization positions Europe as a key market for advanced fifth wheel solutions, particularly in urban and long-haul logistics operations.

Asia Pacific Fifth Wheel Coupling Market Trends

Asia Pacific accounts for roughly 36% share in 2025, with China and India leading due to rapid infrastructure development and highway expansion. Growing e-commerce and logistics operations drive high demand for semi-trailers, boosting adoption of reliable and durable fifth wheel couplings across the region. ASEAN countries contribute via competitive manufacturing and supply chain advantages.

Fleet modernization initiatives and government investments in road networks further accelerate market growth. Operators prioritize efficiency and heavy-duty performance, making Asia Pacific a high-potential region for OEMs and aftermarket suppliers. Projected CAGR exceeds 6.5%, reflecting rising adoption of advanced coupling systems in both domestic and cross-border freight transport.

Competitive Landscape

The fifth wheel coupling market is moderately consolidated, with leading players controlling over half of the global share. Market leaders focus on innovation, investing heavily in R&D to develop lightweight, automated, and technology-enabled coupling systems. Differentiation comes from features such as integrated lubrication, smart safety indicators, and enhanced durability, which cater to modern fleet requirements and regulatory compliance.

Strategic expansion into emerging markets supports long-term growth, while aftermarket offerings emphasize retrofitting and replacement solutions for existing fleets. The combination of OEM integration and flexible aftermarket options strengthens competitive positioning, driving both adoption and revenue across global logistics and transportation sectors.

Key Market Developments

- In April 2024, SAF-Holland inaugurated a new facility in Texas dedicated to specialty fifth wheel production. This expansion aims to enhance high-variation manufacturing capabilities starting 2025, supporting faster delivery times and meeting growing demand for advanced and customized coupling systems.

- In March 2024, Fontaine Fifth Wheel introduced lightweight couplers designed for Class 8 trucks. These new couplers improve fuel efficiency, reduce vehicle weight, and support long-haul operations, enabling fleet operators to optimize performance while complying with evolving environmental and safety standards.

- In September 2024, Fontaine Fifth Wheel unveiled a new safe coupling system with integrated LED safety indicators at Automechanika. The innovation enhances operational safety, provides real-time visual alerts during attachment, and strengthens adoption in commercial and heavy-duty trucking fleets globally.

Companies Covered in Fifth Wheel Coupling Market

- SAF-HOLLAND S.A.

- JOST Werke AG

- Fontaine Fifth Wheel

- Guangdong Fuwa Engineering Group Co., Ltd.

- RSB Group

- Tulga Fifth Wheel Co.

- TITGEMEYER Group

- Sohshin Co., Ltd.

- Zhenjiang Baohua Semi-Trailer Parts Co., Ltd.

- Foshan Yonglitai Axle Co., Ltd.

- Xiamen Wondee Autoparts Co., Ltd.

- Shandong Fuhua Axle Co., Ltd.

- York Transport Equipment

- Rockinger

- Haacon Hebetechnik GmbH

Frequently Asked Questions

The global fifth wheel coupling market is expected to reach US$ 731.4 million in 2026.

Rising commercial vehicle production and freight volumes, supported by high truck registrations in regions like North America and Europe.

North America holds 38% share in 2025, driven by extensive trucking networks, fleet expansions, and stringent safety regulations.

Integration with electric trucks, as EV semi-trailer fleets expand by 25% annually, creating demand for smart and high-torque couplings.

Leading firms include JOST Werke AG, SAF-Holland, Fontaine Fifth Wheel, and Essentra plc.