- Off-Road Equipment & Machinery

- Excavator Attachments Market

Excavator Attachments Market Size, Share, and Growth Forecast, 2026 - 2033

Excavator Attachments Market by Attachment Type (Buckets, Grapples, Rakes, Hammers, Augers, Large Room and Others), Excavator Size (<6 Metric Tons, 6-20 Metric Tons, 20-50 Metric Tons and >50 Metric Tons), End-user (Demolition, Excavation, Forestry, Mining and Others), and Regional Analysis for 2026 - 2033

Excavator Attachments Market Size and Trends Analysis

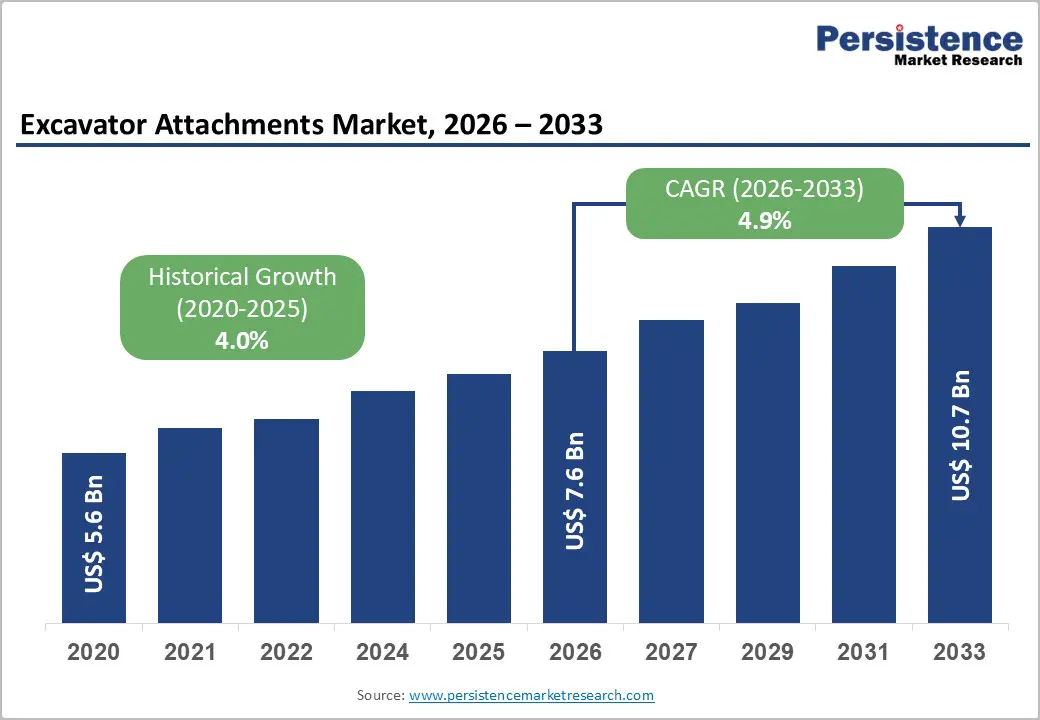

The global excavator attachments market size is likely to be valued at US$ 7.3 billion in 2026 and is projected to reach US$ 10.7 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

The market is driven by the adoption of multi-functional attachments, enabling cost-effective equipment utilization; rising demolition and urban renewal activities requiring specialized attachment solutions; and technological advancements integrating IoT monitoring and automation, enhancing operational efficiency.

Key Industry Highlights:

- Leading Attachment Type: Grapples dominate with 26.4% market share due to demolition and material-handling requirements; Buckets are the fastest-growing at an 8% CAGR, driven by excavation fundamentals and infrastructure development.

- Dominant Excavator Size: 6-20 MT capacity commands 35.3% market share through balanced capacity-to-cost positioning; <6 MT mini equipment is the fastest-growing at a 9% CAGR, driven by the prevalence of urban projects.

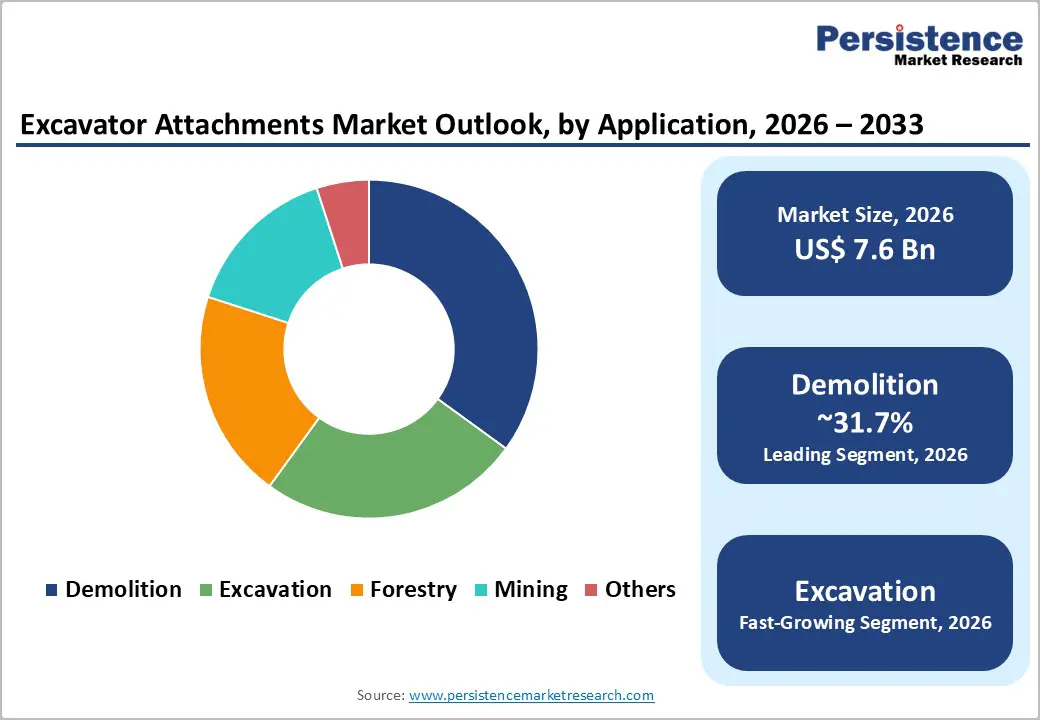

- Leading Application: Demolition maintains 31.7% market share through specialized attachment requirements; Excavation represents fastest growing at 6% CAGR, driven by infrastructure development and urbanization.

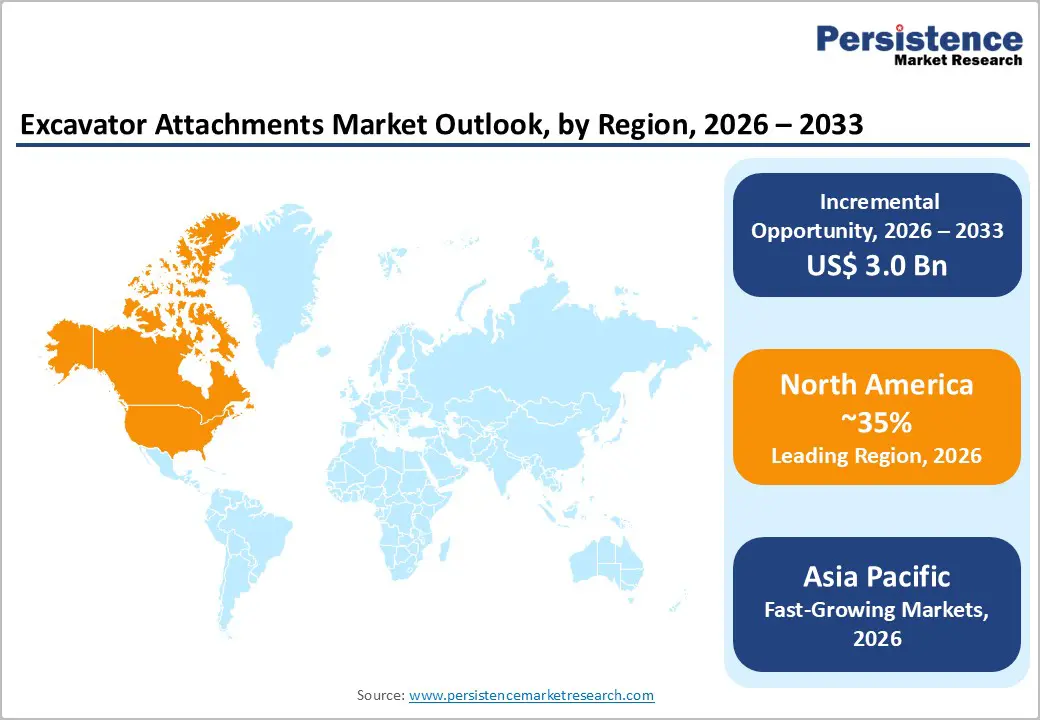

- Regional Market Dominance and Growth: North America maintains 35% global market share, driven by construction activity; Asia Pacific demonstrates the fastest regional growth at a 6% CAGR, expanding from its current 30% share to 42-50% by 2033 through rapid urbanization.

- Technology and Market Innovation Momentum: Top 10 suppliers control 55% market share (Caterpillar, Komatsu, Volvo leading); IoT integration enabling predictive maintenance, reducing downtime 25%; Mini attachment specialization capturing the fastest-growing segment; Waste management specialization establishing new market segments.

| Key Insights | Details |

|---|---|

| Excavator Attachments Market Size (2026E) | US$ 7.6 Bn |

| Market Value Forecast (2033F) | US$ 10.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.0% |

Market Dynamics

Drivers - Global Construction Industry Expansion and Urbanization Trajectory

The global construction market reached approximately US$ 15-17 trillion in 2024-2025, representing 5-7% annual growth and establishing demand for foundational excavator attachments. Urbanization acceleration, with the global urban population projected to reach 68-70% by 2033 and the corresponding construction requirements, drives demand for versatile material-handling equipment. Infrastructure investment expansion, with government spending on infrastructure globally reaching US$4-5 trillion annually through the 2033 forecast period, establishes systematic requirements for construction equipment.

Urban renewal and redevelopment, with major cities investing US$ 200-500 million annually in modernization projects requiring demolition and renovation attachments, drive specialized equipment demand. Residential and commercial construction growth, with middle-class populations in emerging markets driving building demand at 5% annually, establishes proportionate attachment requirements. Modular and prefabricated construction advancement, with construction methods growing 10-15% annually and requiring specialized handling attachments, establish technical differentiation opportunity.

Versatile Multi-Functional Attachment Adoption and Cost Optimization

Equipment consolidation demand, with construction companies increasingly adopting multi-functional attachments that eliminate the need for separate specialized equipment, creates proportionate attachment demand. Cost-effectiveness advantage, with versatile attachments reducing total equipment ownership costs by 20-30% through equipment consolidation, establishes economic justification for adoption. Operational flexibility enhancement, with multi-functional equipment enabling rapid task transitions on dynamic job sites and improving project economics, drives purchasing preference. Material handling requirements, with excavators serving as primary material handling platforms in construction and demolition, requiring grapples, buckets, and specialized handling attachments, establish foundational demand.

The expansion of the equipment rental market, with equipment leasing companies growing 15-20% annually and requiring diverse attachment portfolios to support customer specialization, drives attachment procurement. Workforce productivity optimization, with attachment technology reducing manual labor requirements by 30-40%, aligning with labor cost escalation and skilled labor shortage concerns.

Restraints - High Equipment Investment Barriers and Financing Constraints

Excavator attachment acquisition costs, with advanced specialized attachments commanding prices of US$ 15,000-150,000+ depending on specialization and technology, constrain SME adoption. Equipment financing complexity, with attachment financing requiring 12-24-month approval timelines and stringent credit requirements, impairs purchasing flexibility for smaller operators. Maintenance cost escalation, with advanced technology integration increasing preventive maintenance costs to 5-10% of equipment acquisition cost annually, increase total cost of ownership.

Skilled technician availability, with specialized maintenance requiring trained technicians commanding premium compensation, limit cost-effective support in emerging markets. Replacement cycle pressure, with rapid technology advancement creating equipment obsolescence cycles of 5-8 years, creates financial planning challenges. Used equipment market saturation, with secondary market oversupply constraining new attachment sales and compressing pricing margins, particularly in developed markets.

Regulatory Compliance and Environmental Standard Requirements

Emission regulation stringency, with EU Stage V and equivalent standards requiring 90%+ emission reductions and increasing equipment costs 15-20%, compress manufacturer margins. Safety certification requirements, with increasingly stringent ISO and regional standards requiring comprehensive testing and validation, increase product development costs. Operating restrictions, with noise and vibration regulations limiting deployment in urban areas during certain hours, reduce the addressable market for demolition attachments.

Cross-border compliance complexity, with equipment requiring certification modifications across jurisdictions, creating an operational burden. Material-recycling mandates, with regulations mandating minimum recycled content requirements for components, increase production complexity. Supply chain regulatory impact, with component sourcing restrictions and manufacturing location requirements affecting cost structure and supply continuity.

Opportunity - Mini Excavator and Compact Equipment Attachment Expansion

Mini excavator market growth, with compact equipment (<6 MT) expanding by 8-12% annually, driven by urban construction and confined-space requirements, creates a specialized attachment opportunity. Specialized mini attachment development, with companies establishing mini-scale versions of standard attachments, drive new product opportunities. Urban project prevalence, with cities increasingly requiring equipment capable of operating in restricted spaces and residential areas, establish proportionate demand. Cost-effective equipment alternative, with mini excavators commanding 40-50% cost advantage versus standard equipment while meeting 70-80% of task requirements, drive rental and small contractor adoption. Technology adaptation, with IoT and automation scaled for compact equipment, create differentiation opportunity.

Recycling and Waste Management Specialized Attachments

Waste management equipment specialization, with recycling operations creating unique attachment requirements, including specialized grapples, sorters, and processing equipment, establishes a niche market opportunity. Circular economy alignment, with global waste processing growing 12-18% annually and creating proportionate equipment demand, establish market foundation. Demand for attachment customization, with waste operators requiring specialized solutions for diverse material handling, drives custom attachment development. Environmental compliance advantage, with specialized equipment improving sorting efficiency and material recovery by 20-30%, align with sustainability regulations. Regulatory incentive alignment, with government sustainability mandates creating demand for advanced recycling equipment and attachments, and establishing purchasing incentives.

Category-wise Analysis

Attachment Type Insights

The grapples segment is expected to dominate the market. Grapples play a vital role in construction and demolition activities, allowing operators to handle and sort various materials, including debris, concrete, and metal. The growth in construction and demolition projects worldwide directly drives the demand for grapples as efficient tools for material handling and waste management.

Nonetheless, the buckets segment of the excavator attachments market is expanding at the quickest rate. The continuous growth in construction and infrastructure development globally fuels the demand for excavator buckets as indispensable attachments for excavation, grading, and trenching tasks.

Excavator Size Insights

The 6-20 MT excavator segment holds 35.3% market share, driven by its balanced capacity-to-cost profile and broad applicability. These machines account for 60-70% of global excavator production, benefiting from manufacturing scale and standardized components. They support diverse applications across construction, demolition, mining, and forestry, while offering a 30-40% cost advantage over larger equipment and meeting 70-80% of task requirements. Widespread use in infrastructure projects and dominance in rental fleets where 65-75% of units fall in this range-reinforce demand and pricing accessibility.

The <6 MT mini excavator segment is the fastest growing, expanding at 6.4% CAGR through 2033. Growth is driven by dense urban construction, limited job-site access, and advances in compact hydraulics. Lower transport and ownership costs, strong rental adoption, expanding attachment options, and rising urban infrastructure investment are accelerating mini excavator deployment.

Application Insights

The demolition sector holds 31.7% market share, driven by specialized attachment requirements and large project scales. Urban renewal activity, with major cities undertaking 5-10 significant demolition projects annually, creates consistent equipment demand. Demolition relies on dedicated attachments such as hydraulic hammers, shears, pulverizers, and grapples, reinforcing specialized procurement. Stricter safety regulations and certification requirements further accelerate adoption of advanced attachments. Growing emphasis on material recovery and recycling increases demand for sorting and handling tools, while the technical complexity of demolition projects supports premium-priced, high-performance equipment.

The excavation segment is the fastest-growing, projected to expand at 7% CAGR through 2033. Growth is driven by global infrastructure expansion, urbanization, and the foundational role of excavation in all construction projects. Bucket attachments dominate, accounting for 60-70% of utilization, ensuring steady demand. Development of specialized buckets and productivity-enhancing technologies, including smart and IoT-enabled designs, further supports segment expansion.

Regional market insights

North America Excavator Attachments Market Insights

North America commands approximately 35% of global Excavator Attachments market share, valued at approximately US$ 2.4 billion in 2026 with projections approaching US$ 3.6 billion by 2033. The United States represents dominant regional market contributor, accounting for 78% of North American market value, driven by construction activity and demolition project volume.

Infrastructure investment prioritization, with US federal government allocating US$ 150-200 billion annually for infrastructure modernization, establishes systematic equipment demand. Demolition and urban renewal prevalence, with major US cities conducting 10-15 significant demolition projects annually, drive specialized attachment demand. Construction sector expansion, with residential and commercial construction growing 4-6% annually, drive material handling equipment procurement. Technology adoption leadership, with North American contractors investing in advanced equipment and IoT monitoring, establish innovation hub positioning.

Europe Excavator Market Analysis

Europe represents approximately 22% of global Excavator Attachments market share, valued at approximately US$ 1.6 billion in 2026. Germany, Italy, France, and Spain collectively represent 70% of European market value, reflecting established construction manufacturing and demolition activity.

Environmental regulatory leadership, with EU emission standards and circular economy directives, is driving equipment modernization and sustainable attachment development. Construction activity concentration, with the European construction market valued at US$ 2.0-2.3 trillion and growing 3-5% annually, establishes proportionate equipment demand. Waste management specialization, with European waste processing and recycling growing 8-10% annually, drives specialized attachment requirements.

Asia Pacific Excavator Market Share and Insights

The Asia Pacific demonstrates robust growth dynamics, commanding approximately 30% market share with projections increasing to 42-50% by 2033. The region valued at approximately US$ 2.3 billion in 2026 is anticipated to reach US$ 4.3 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 7% in the forecast period.

Infrastructure investment expansion, with China, India, and Southeast Asia investing US$ 400-600 billion annually in infrastructure, establishes substantial equipment demand. Construction sector acceleration, with urbanization creating 20-30% annual growth in construction activity across emerging markets, drive material handling equipment procurement. Mini-excavator proliferation, with demand for compact equipment growing 12-18% annually in emerging Asian markets, establishes specialized attachment requirements. Manufacturing localization, with equipment manufacturers establishing regional production, achieving 25-35% cost advantages, enables market penetration at accessible price points.

Competitive Landscape

Prominent organizations, including Caterpillar Inc. and Komatsu Ltd., are at the vanguard of this sector; Caterpillar offers a wide range of excavator attachments to cater to the diverse needs of its customers across various industries, including construction, mining, forestry, and waste management. This diversified product portfolio allows Caterpillar to capture a larger market share and maintain a competitive edge. Caterpillar is committed to innovation and technology, continuously developing new and improved excavator attachments that enhance performance, efficiency, and safety.

The company invests heavily in research and development to stay ahead of the competition and meet the evolving needs of its customers. Caterpillar has a strong global distribution network, ensuring its excavator attachments are readily available to customers worldwide. The company's network of dealers, distributors, and service centers provides customers with convenient access to products, technical support, and aftermarket services.

Key Industry Developments

- In October 2025, Caterpillar Inc. entered into an agreement to acquire RPMGlobal Holdings Limited, an Australian-based software provider, in a strategic move to integrate advanced mining software with its existing equipment expertise and further enhance its digital solutions for global mining operations.

- In June 2025, Komatsu Ltd. finalized a major agreement with Barrick Gold Corporation for the delivery of primary mining equipment to the substantial Reko Diq copper-gold project in Pakistan, reflecting the company’s expanding relationships and global footprint in strategic partnerships for mining equipment supply.

Companies Covered in Excavator Attachments Market

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- Volvo Construction Equipment

- Doosan Infracore Co., Ltd.

- Liebherr Group

- JCB

- Sandvik Group

- CNH Industrial N.V.

- Atlas Copco Group

- Others Key Players

Frequently Asked Questions

The excavator attachments market is estimated to be valued at US$ 7.6 Bn in 2026.

The key demand driver for the Excavator Attachments market is the rising demand for versatile, productivity-enhancing equipment in construction, mining, demolition, and infrastructure projects, driven by global construction and urbanization growth.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Excavator Attachments market.

Among the applications, Demolition holds the highest preference, capturing beyond 31.7% of the market revenue share in 2026, surpassing other applications.

The key players in Excavator Attachments are Caterpillar Inc., Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Volvo Construction Equipment, and Doosan Infracore Co., Ltd.