- Technology

- Email Application Market

Email Application Market Size, Share, and Growth Forecast, 2026 - 2033

Email Application market by Application Type (Free Email Services, Paid / Subscription-based Email Services, Enterprise Email Solutions), Deployment Mode (Web-based, Desktop-based, Mobile-based) End user (Individual / Consumer, Small & Medium Businesses (SMBs), Large Enterprises) and Regional Analysis for 2026 - 2033

Email Application Market Size and Trends Analysis

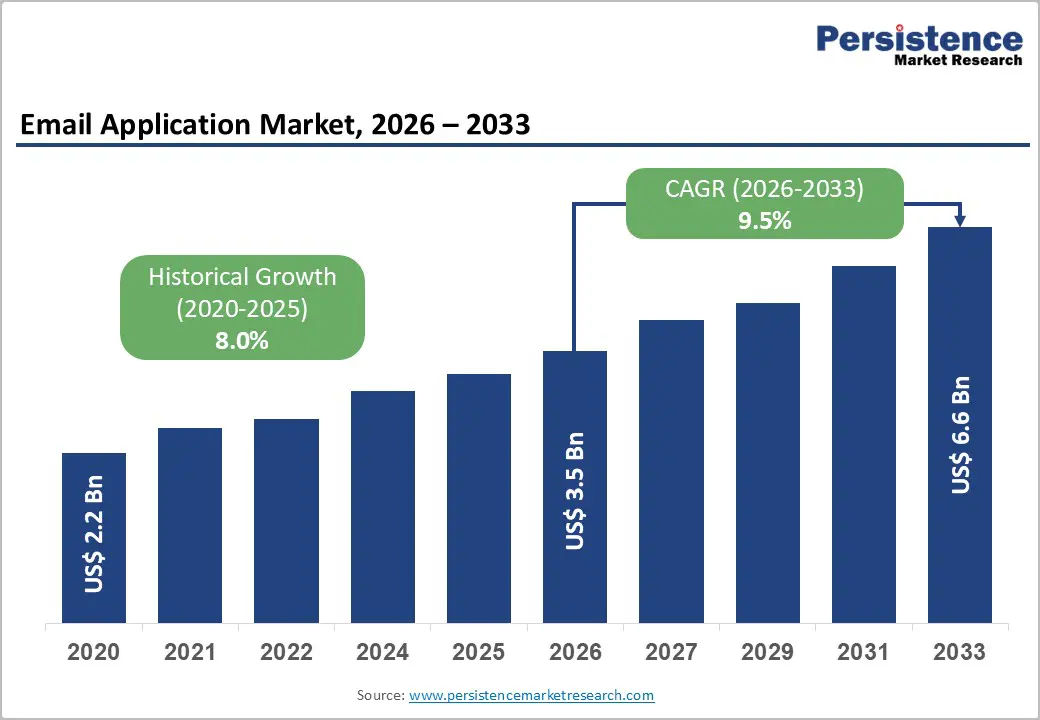

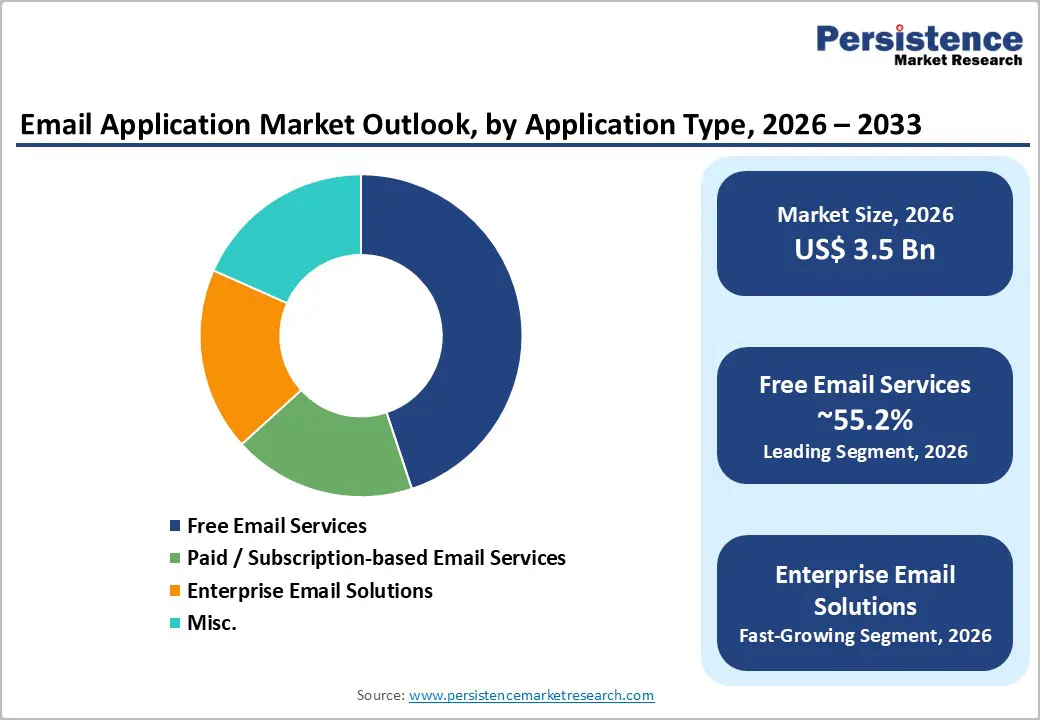

The Global Email Application Market size was valued at US$ 3.5 billion in 2026 and is projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 9.5% between 2026 and 2033. Market expansion reflects fundamental shifts in digital communication infrastructure driven by hybrid work normalization, cloud technology adoption, and intensifying cybersecurity requirements.

The global email user base reached around 4.5 billion in 2024, expanding toward 5 billion by 2027-28, creating substantial addressable markets for feature-rich email solutions across consumer and enterprise segments. Email Application Market growth correlates directly with organizational demand for advanced collaboration capabilities, sophisticated threat protection, and seamless multi-device accessibility supporting distributed workforce requirements.

Key Industry?Highlights:

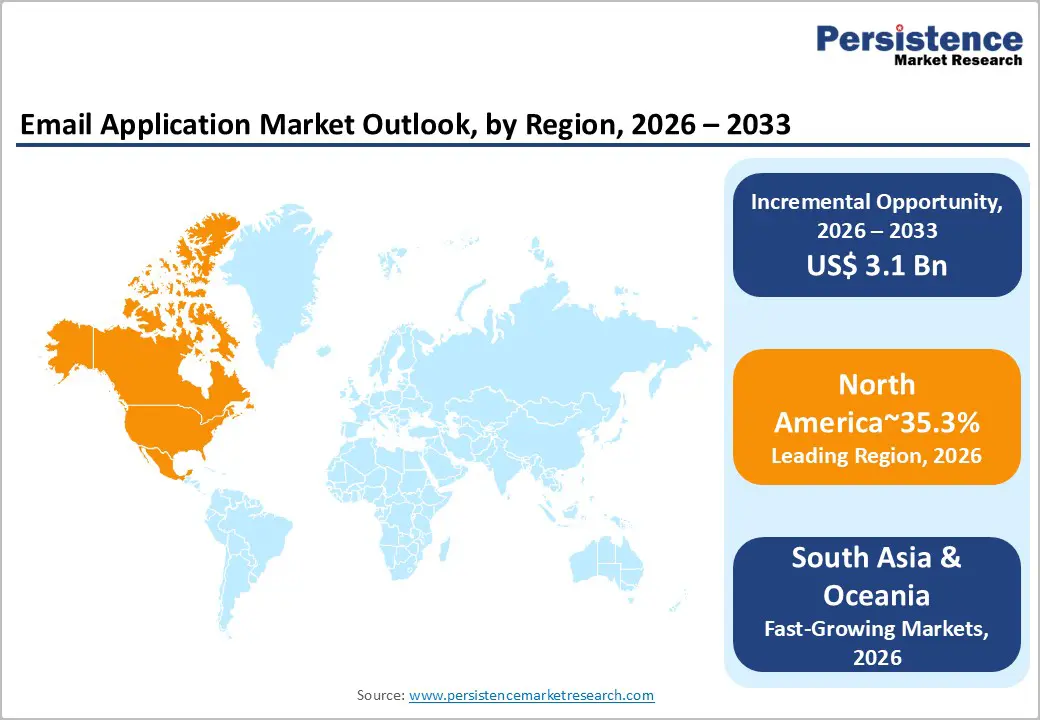

- Leading Region: North America leads the Email Application Market with 35.3% share in 2025, driven by strong enterprise cloud email adoption, AI-enabled security investments, and stringent regulatory compliance requirements.

- Fastest-Growing Region: East Asia captures 20% share and remains the fastest-growing market, supported by mobile-first usage patterns, rapid digital transformation, and expansion of regional email ecosystems in China, Japan, and Korea.

- Dominant Segment: Free Email Services dominate the market with 55.2% share with the highest user penetration, reinforced by Gmail’s massive global reach, strong mobile integration, and ecosystem-driven stickiness.

- Fastest-Growing Segment: Enterprise Email Solutions represent the fastest-growing category as organizations prioritize AI-driven threat detection, compliance, and integrated productivity suites.

- Leading Deployment Mode: Web-based email applications maintain leadership due to universal accessibility, seamless updates, and strong adoption of browser-based enterprise collaboration platforms.

- Fastest-Growing Deployment Mode: Mobile-based email applications grow the fastest, fueled by rising mobile email open rates, Gen Z workforce expansion, and demand for cross-platform real-time synchronization.

| Key Insights | Details |

|---|---|

| Email Application Market Size (2026E) | US$ 3.5 Bn |

| Market Value Forecast (2033F) | US$ 6.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.0% |

Market Dynamics

Growth Drivers

Artificial Intelligence and Machine Learning Integration for Enhanced Security

AI-powered threat detection and automated intelligence systems have transformed the Email Application Market into a sophisticated security-focused industry segment addressing escalating cyber threats and phishing sophistication. Email security vendors have deployed advanced machine learning systems that fundamentally outperform traditional rule-based filtering approaches, with Gmail's spam filtering system blocking over 99.9 percent of malicious messages daily, processing more than 15 billion unwanted messages and protecting 1.8 billion daily users.

Google's RETVec algorithm achieved 35 to 40 percent improvement in spam detection while simultaneously reducing false positives by around 20 percent, a critical advancement enabling organizations to maintain operational efficiency without losing legitimate business communications. TensorFlow integration enables Gmail to block an additional 100 million spam messages daily, demonstrating how machine learning frameworks specifically engineered for image-based spam detection and phishing attack simulation improve Email Application Market value propositions substantially.

The Market increasingly emphasizes AI-driven user experience improvements beyond security, including predictive text capabilities, intelligent sorting, and automated workflow optimization that significantly improve user productivity. Financial services, healthcare, and government organizations particularly prioritize AI-integrated email solutions, justifying premium pricing and driving expansion of enterprise email service revenue, substantially exceeding broader Email Application Market growth rates. As AI algorithms continue maturing and threat landscape complexity increases, organizations across all industries recognize sophisticated email management and security as essential rather than discretionary infrastructure investments.

Cloud Migration and Regulatory Compliance Framework Evolution

Cloud-based email solutions are displacing on-premises infrastructure at accelerating rates driven by cost economics, regulatory compliance requirements, and operational simplification that create substantial Email Application Market expansion opportunities. 70 percent of enterprises globally are transitioning from traditional Secure Email Gateway (SEG) infrastructure toward API-based Integrated Cloud Email Security (ICES) platforms that connect directly to Microsoft 365 and Google Workspace ecosystems without requiring mail-flow rerouting. API-enabled cloud email security solutions substantially exceeding for broader cloud-based email security markets demonstrating powerful competitive advantages compelling rapid architectural migration from legacy gateway-based systems.

Regulatory frameworks including GDPR, CCPA, HIPAA, and the emerging NIS 2 Directive throughout Europe are institutionalizing data protection and cybersecurity requirements that mandate investment in compliant email infrastructure. Microsoft's May 5, 2025, sender authentication requirements for Outlook, requiring implementation of Sender Policy Framework (SPF), DomainKeys Identified Mail (DKIM), and Domain-based Message Authentication, Reporting, and Conformance (DMARC) protocols, exemplify how regulatory evolution drives standardization and security maturation within Email Application Market ecosystems.

Organizations prioritizing regulatory compliance simultaneously enhance operational security, creating alignment between governance obligations and technical security improvements that justify substantial Email Application Market investment budgets.

Market Restraining Factors

Data Privacy Complexity and Quantum Computing Security Threats

Data privacy regulations spanning the European Union's General Data Protection Regulation (GDPR), California's Consumer Privacy Act (CCPA), and healthcare-specific frameworks including HIPAA create substantial compliance costs and operational constraints limiting Email Application Market adoption among smaller organizations and international companies managing cross-border data flows. GDPR fines for data exfiltration via email have reached extraordinary magnitudes, creating reputational and financial incentives for organizations to implement sophisticated email security controls that exceed mandatory compliance thresholds.

Quantum computing represents an emerging technological threat to encryption foundations underlying contemporary email security, compelling vendors to invest substantially in quantum-resistant cryptography research and development to ensure Email Application Market solutions maintain security effectiveness throughout future technology transitions.

Key Market Opportunities

Enterprise Cloud Email Security Platform Consolidation

Enterprise organizations are systematically consolidating security infrastructure toward unified cloud-native platforms integrating email, collaboration application, endpoint, and identity security under single vendor management, creating substantial market opportunities for Email Application Market participants offering comprehensive integrated solutions.

Security leaders prioritizing operational efficiency and streamlined threat intelligence increasingly favor unified platforms reducing alert fatigue and simplifying incident response workflows compared to specialized point solutions requiring manual integration and cross-platform correlation. Proofpoint's integration of Azure security APIs demonstrates how strategic partnerships between Email Application Market vendors and cloud infrastructure providers accelerate deployment cycles and enhance solution breadth.

Integration of advanced security analytics through unified platforms enables organizations to identify compromised accounts within minutes rather than traditional detection timeframes measured in hours or days, directly reducing breach impact and financial damage. The consolidated security platform market represents a substantial expansion of addressable markets for email security vendors willing to invest R&D capital developing integrated solution capabilities, particularly within North America and Europe where enterprises demonstrate premium pricing willingness for integrated security platforms. Organizations across financial services, healthcare, and government sectors prioritize consolidated security infrastructure addressing regulatory compliance obligations while simultaneously enhancing operational security posture.

Mobile-First Email Application Development and Cross-Platform Optimization

Mobile devices now account for 55 percent of all email opens globally, with demographic data demonstrating that Gen Z and Millennial workforces will represent the majority of organizational workforces by 2030, creating structural demand for Email Application Market solutions optimized specifically for mobile user experiences.

Mobile-optimized email communications achieve first-link click rates 30 percent higher than non-responsive designs, demonstrating quantifiable competitive advantages for organizations prioritizing mobile experience quality. Email Application Market participants developing sophisticated mobile clients providing seamless synchronization across iPhone, Android, and tablet platforms while maintaining enterprise-grade security features directly address the primary user experience preferences of contemporary and emerging workforces.

Regional markets throughout Asia-Pacific demonstrate particularly strong mobile-first preferences, with China and India showing adoption rates and growth rates substantially exceeding North American and European markets.

The Market opportunity in mobile-optimized solutions extends beyond consumer segments into enterprise deployments, where field-based workforces, healthcare providers, and logistics organizations require robust mobile email clients supporting mission-critical communication. Vendors successfully developing mobile-first strategies while maintaining enterprise security and compliance capabilities position themselves to capture substantial market share among emerging economies and youthful workforce demographics increasingly resistant to desktop-centric application design.

Category-wise Analysis

Component Type Insights

Free email service applications maintain dominant market positioning with 55.2 % market share in 2026, reflecting the fundamental role that consumer email plays in personal communication, account recovery processes, and digital service access across global populations. Gmail, with 1.8 billion daily users and approximately 25 percent of email client market share, exemplifies the market dominance of free offerings at scale, capturing India and Indonesia as primary growth markets with penetration rates exceeding 82 percent. Free email services generate substantial platform value through data aggregation, targeted advertising, and integration with complementary Google, Microsoft, and Apple ecosystem services, creating business models enabling continuous feature investment and security enhancements without direct user fees.

The free email service segment benefits from network effects and switching cost dynamics that entrench market leaders while creating substantial barriers to competitive entry. Organizations attempting to displace Gmail, Outlook.com, or Yahoo Mail through alternative free offerings face structural disadvantages including established user bases, brand recognition, and integration with personal data ecosystems that discourage migration.

Enterprise email solutions represent the fastest-growing segment within the Application Type category, driven by organizational demand for advanced security controls, regulatory compliance capabilities, team collaboration features, and integration with enterprise systems that consumer-oriented offerings cannot adequately address.

Deployment Mode Insights

Web-based email deployment modes maintain market leadership position with 50.7% market share in 2026, reflecting the accessibility, cross-platform compatibility, and elimination of local client installation complexity that characterize browser-based email access. Gmail, Outlook.com, Yahoo Mail, and enterprise offerings including Google Workspace and Microsoft 365 online interfaces dominate the web-based segment, providing immediate accessibility across devices without software installation or configuration burden. Web-based applications simplify technology management for organizations and users, enabling automatic security updates, seamless feature deployment, and elimination of local infrastructure requirements that historically created IT support burden and security vulnerabilities through outdated client versions.

The web-based segment benefits from substantial ecosystem maturity, with decades of development optimizing user experience, performance optimization techniques including progressive web application frameworks enabling offline functionality, and comprehensive feature parity between web and native client implementations.

Cloud infrastructure investment from technology leaders including Google, Microsoft, and Amazon ensures web-based applications maintain performance standards and reliability characteristics competitive with native applications while providing superior flexibility across operating systems and devices. Web-based email deployment will likely retain market leadership through 2033 based on demonstrated advantages in accessibility and elimination of installation complexity, though market share may gradually decline as mobile-based deployment expansion captures use cases where web-based access provides suboptimal experiences.

Regional Insights and Trends

North America Market Trend

North America maintains the largest Email Application Market share at 35.3%, reflecting mature digital infrastructure, high enterprise technology investment concentration, and early adoption of cloud-based email solutions and advanced security platforms. The region encompasses substantially higher per-user email application spending compared to international markets, driven by enterprise concentration in financial services, healthcare, technology, and professional services sectors that prioritize email security, regulatory compliance, and team collaboration capabilities justifying premium pricing.

North American email client market share demonstrates Apple's dominance with Gmail's secondary position, reflecting the regional technology ecosystem concentration around Apple devices and Google's aggressive enterprise market expansion through Google Workspace.

Microsoft Outlook maintains third position of the North American email client market share despite significant enterprise market presence, reflecting the complex relationship between consumer email applications, enterprise-specific solutions, and device manufacturer ecosystem integration. Organizations throughout North America have systematically migrated from on-premises email infrastructure toward cloud-based solutions, with 70 percent of enterprises evaluating or implementing API-based Integrated Cloud Email Security platforms designed to provide native integration with Microsoft 365 and Google Workspace ecosystems.

East Asia Market Trend

East Asia represents a strategically significant Email Application Market geography capturing 20% of global market share while demonstrating the fastest regional growth rates driven by rapid mobile device proliferation, digital transformation initiatives, and emerging market expansion. China and India collectively represent the largest addressable markets within the region, with distinct competitive dynamics and growth characteristics.

China's digital ecosystem operates under distinctive regulatory frameworks and competitive dynamics, with QQ Mail, NetEase, and Alibaba Mail dominating market share compared to Western email providers, creating opportunities for region-specific Email Application Market innovations addressing Chinese consumer preferences and government compliance requirements.

The region's cost advantage in professional services and software development creates opportunities for Email Application Market solution providers and service delivery organizations to develop region-specific solutions addressing unique geographic, regulatory, and linguistic requirements.

Europe Market Trend

Europe represents 25% of the global Email Application Market, characterized by stringent data protection regulations, advanced digital infrastructure, and regulatory-driven security investment disproportionate to market size. The European Union's General Data Protection Regulation (GDPR) established unprecedented data privacy standards and enforcement mechanisms including substantial financial penalties, compelling European organizations to implement email solutions offering granular compliance controls, audit capabilities, and data residency options unavailable in simpler solutions.

The emerging NIS 2 Directive extending cybersecurity requirements beyond large enterprises to smaller organizations and critical infrastructure operators will further elevate email security investment requirements throughout the European region.

Organizations throughout Germany, France, and the United Kingdom prioritize quantum-resistant encryption and ESG-validated data center compliance, creating competitive advantages for Email Application Market vendors offering sophisticated security controls and transparent data governance practices. European regulatory frameworks including GDPR fines for data exfiltration via email have reached extraordinary magnitudes, with published GDPR penalty decisions creating reputational incentives for email security investment extending beyond mandatory compliance thresholds.

Competitive Landscape

The Global Email Application Market is largely oligopolistic, dominated by major players while still accommodating niche providers. Microsoft Outlook and Gmail (Google) lead with massive enterprise and consumer adoption, seamless integration with productivity suites, and AI-powered features. Apple Mail drives loyalty within the Apple ecosystem, while Yahoo Mail retains a strong free-tier user base. Zoho Mail and FastMail cater to SMBs and privacy-focused professionals, and ProtonMail emphasizes end-to-end encryption for secure communications. Competition is fueled by innovations in AI, mobile optimization, cross-platform synchronization, and security, making the market consolidated at the top but fragmented at the periphery.

Key Industry Developments

- On January 8, 2026, Google introduced the Gmail Gemini era, bringing AI-powered features such as AI Overviews, Help Me Write, Suggested Replies, and Proofread, transforming Gmail into a proactive inbox assistant that summarizes conversations, drafts emails, and provides context-aware responses to improve user productivity for its 3 billion users.

- On September 21, 2023, Microsoft launched the new Outlook for Windows for personal accounts, offering a unified email and calendar experience with a modern interface, AI-powered suggestions, seamless integration with OneDrive and Office web apps, and pre-installation on new Windows 11 devices, enhancing accessibility and productivity for millions of users.

Companies Covered in Email Application Market

- Microsoft Corporation

- IBM Corporation

- Google Inc.

- Micro Focus International Plc

- NEC Corporation

- Amazon.Com

- Hitachi

- J2 Global Inc.

- Fujitsu

- Others.

Frequently Asked Questions

The global Email Application market is projected to be valued at US$ 3.5 Bn in 2026.

The Free Email Services segment is expected to account for approximately 55.2% of the global Email Application market by Application type in 2026.

The market is expected to witness a CAGR of 9.5% from 2026 to 2033.

AI- and ML-driven email security advancements, combined with accelerating cloud migration and tightening global regulatory compliance requirements (GDPR, CCPA, HIPAA, NIS2), are the primary growth drivers of the Email Application Market.

Major market opportunities center on unified cloud-native email security platform consolidation and mobile-first, cross-platform email application development, driven by enterprise demand for integrated security and rising mobile-centric workforce adoption.

Key players in the Email Application market include Google (Gmail), Microsoft (Outlook), Apple (Apple Mail), Yahoo Mail, Zoho Mail, Proton Mail, and regional/enterprise providers.