- Baby Care & Accessories

- Dog Collars, Leashes & Harnesses Market

Dog Collars, Leashes & Harnesses Market Size, Share, and Growth Forecast 2026 - 2033

Dog Collars, Leashes & Harnesses Market by Product Type (Dog Collars, Dog Leashes, Dog Harnesses), by Material (Nylon, Leather, Polyester, Metal, Rubber/Silicone, Eco-Friendly Materials), by Dog Size (Extra Small, Small, Medium, Large, Extra Large), by Application, by Distribution Channel, and Regional Analysis, 2026 - 2033

Dog Collars, Leashes & Harnesses Market Size and Trend Analysis

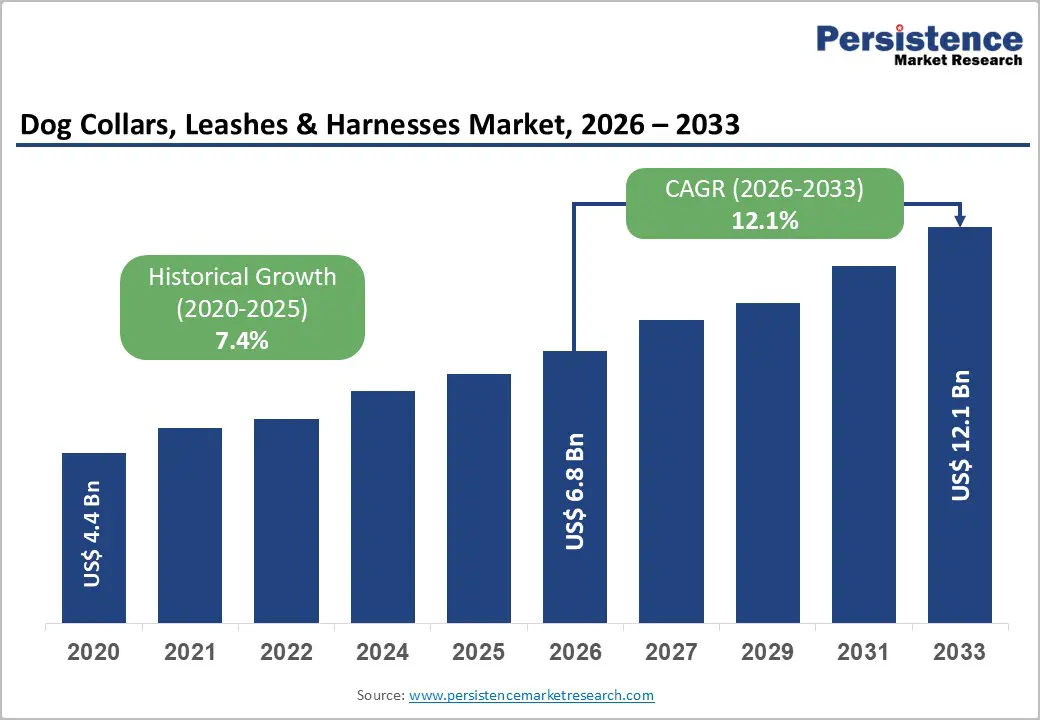

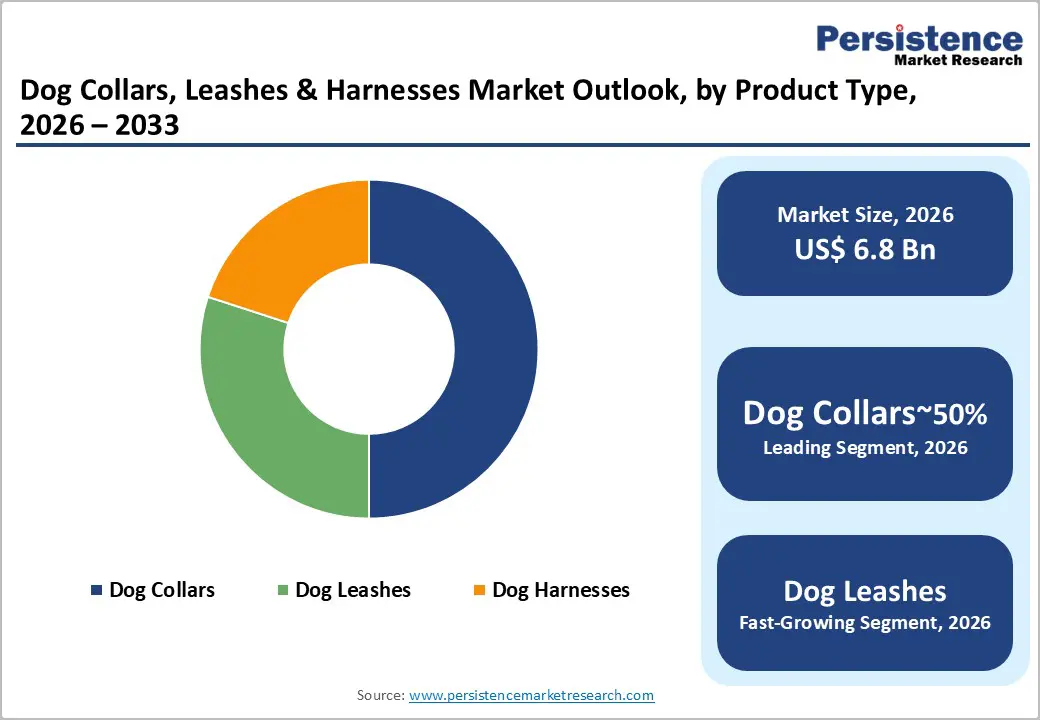

The global Dog Collars, Leashes & Harnesses market is likely to be valued at US$ 6.8 billion in 2026 and is expected to reach US$ 12.1 billion by 2033, growing at a CAGR of 8.6% from 2026 to 2033. The market's robust, accelerating growth is driven by the global surge in pet dog ownership, deepening pet humanization trends, and rising consumer willingness to invest in premium, safe, and technologically enhanced dog accessories.

Key Industry Highlights:

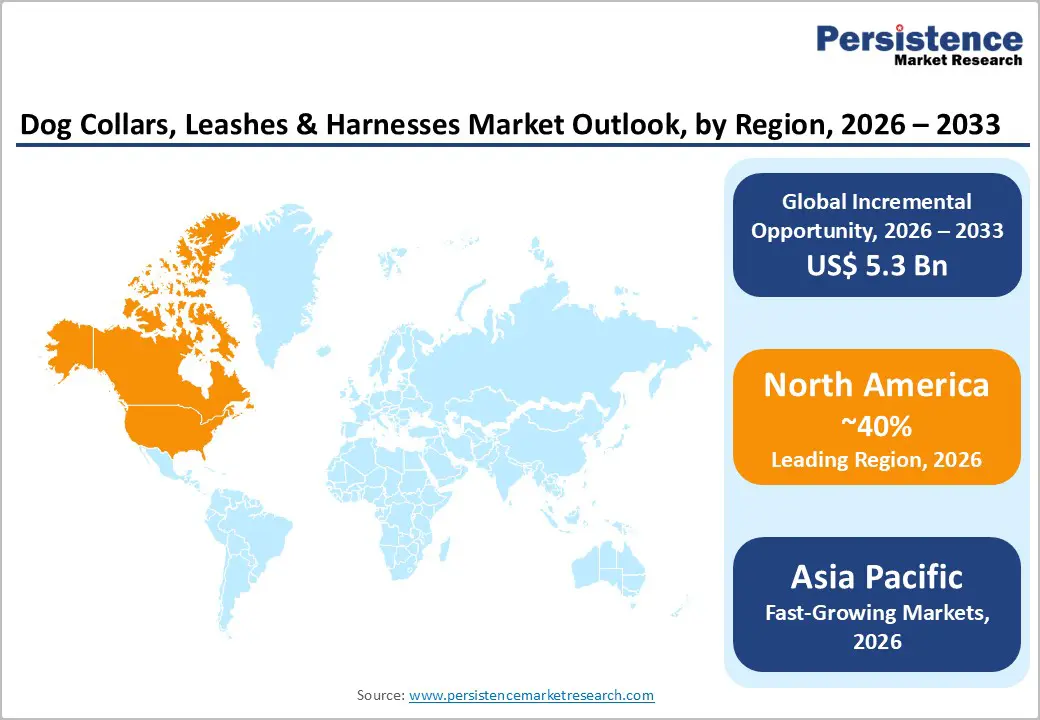

- Leading Region: North America leads the global market, holding 40% share, anchored by total pet industry expenditure, and a strong innovation ecosystem in smart and GPS-integrated dog accessories led by companies including Wagz Inc., FitBark, and Link AKC.

- Fastest Growing Region: Asia Pacific is the fastest growing region with rising CAGR of 9.7%, driven by China's rapidly expanding dog ownership base accelerating e-commerce adoption through platforms, and rising pet humanization trends among urban millennial consumers across China, India, and Southeast Asia.

- Dominant Segment: Dog Collars dominate the product type category with approximately 50% revenue share, driven by their universal purchase necessity, legal identification tag mandates in multiple jurisdictions, and the broadest price spectrum from budget nylon to premium GPS-enabled smart collars.

- Fastest Growing Segment: Eco-Friendly Materials is the fastest growing material segment in dog accessories, propelled by sustainability-conscious millennial and Gen Z pet owners in North America and Europe willing to pay a 25% price premium for certified recycled and organic material products, supported by brands expanding sustainable product lines.

- Key Opportunity: Smart and GPS-integrated dog collars and harnesses represent the highest-value growth opportunity, with connected pet wearable adoption growing at double-digit rates, and the broad infrastructure of smartphone-connected millennial pet owners globally.

| Key Insights | Details |

|---|---|

|

Dog Collars, Leashes & Harnesses Market Size (2026E) |

US$ 6.8 Billion |

|

Market Value Forecast (2033F) |

US$ 12.1 Billion |

|

Projected Growth CAGR (2026–2033) |

8.6% |

|

Historical Market Growth (2020–2025) |

7.4% |

Market Dynamics

Drivers - Rising global dog ownership and pet humanization trends are accelerating demand for premium dog accessories worldwide

The steady and accelerating increase in global dog ownership remains the primary driver of demand for dog collars, leashes, and harnesses. The American Pet Products Association (APPA) reported in its National Pet Owners Survey that 66% of U.S. households, or about 86.9 million homes, own at least one pet, with 65.1 million households specifically owning dogs. Total U.S. pet industry spending reached US$ 147 billion in 2023, highlighting the strong commercial scale of the pet economy. The European Pet Food Industry Federation (FEDIAF) estimates around 104 million pet dogs across the European Union, with the United Kingdom, Germany, France, and Poland leading ownership levels. The ongoing pet humanization trend, where dogs are treated as family members, is encouraging higher spending on premium, stylish, and welfare-focused accessories, thereby increasing average transaction values and driving sustained category growth globally.

Smart GPS-enabled collars and connected pet technologies are driving premiumization and expanding the total addressable market

The rapid integration of technology into pet care products is creating a strong growth opportunity within the dog collars, leashes, and harnesses market. GPS-enabled smart collars offered by brands such as Link AKC, FitBark, and Wagz Inc. allow owners to track real-time location, monitor activity levels, and receive health alerts through mobile applications. According to the Consumer Technology Association (CTA), connected pet devices are among the fastest-growing categories in consumer electronics.

Wagz Inc. has introduced GPS-enabled collars and wireless containment systems designed to replace traditional fences, reflecting a clear shift toward safety-driven innovation. Falling GPS component costs, widespread smartphone adoption, and increasing urban concerns about pet safety are accelerating demand for smart collars, which command higher average selling prices and expand the overall addressable market significantly.

Restraints - High price sensitivity among mass-market consumers limits premium dog accessory adoption and pressures manufacturer margins

Despite the strong appeal of premium and technology-enabled dog accessories, price sensitivity remains a major challenge in the market. The American Pet Products Association 2023–2024 survey indicates that pet owners across income groups are more price-conscious when purchasing accessories compared to essential categories such as food and veterinary care. Accessories show higher demand elasticity, particularly in emerging economies and lower-income households in developed markets. Commodity-grade nylon collars and leashes priced below US$ 10 dominate unit sales in mass retail channels, placing downward pressure on pricing across the industry. This environment makes it difficult for premium manufacturers to expand penetration while maintaining healthy margins. As a result, although innovation and branding create differentiation, a large portion of the global consumer base continues to prioritize affordability over advanced features or premium materials, limiting faster premium segment expansion.

Unregulated online marketplace sellers increase product safety risks and erode consumer trust in accessory quality

The rapid growth of online marketplaces has increased product accessibility but has also introduced quality and safety risks within the category. Platforms such as Amazon and Alibaba Group host numerous third-party sellers, some of whom offer substandard products with weak metal hardware, toxic dye residues, or inaccurate strength specifications.

Regulatory oversight remains inconsistent, as agencies such as the U.S. Consumer Product Safety Commission and the European Union under the General Product Safety Regulation (EU) 2023/988 do not always enforce detailed standards specific to pet accessories. These regulatory gaps allow non-compliant products to enter the market, creating safety risks for pets and liability exposure for sellers. Over time, inconsistent quality levels can erode consumer trust and damage the reputation of established brands competing on the same digital platforms.

Opportunity - IoT-enabled pet wearables present a high-growth premium opportunity driven by data-based pet care adoption

The integration of IoT, GPS tracking, and health monitoring into dog collars and harnesses represents one of the most attractive growth opportunities in the market. As smartphone penetration approaches 90% in developed economies and continues rising across the Asia Pacific, the infrastructure for adopting connected pet wearables is becoming widely accessible. FitBark has expanded partnerships with veterinary clinics and pet insurance providers that use wearable data for preventive care and underwriting decisions, highlighting the commercial potential of health-linked devices.

In 2024, the global pet wearable segment recorded strong double-digit growth, reflecting a structural shift toward data-driven pet management. Companies investing in long-battery GPS collars, lightweight monitoring harness attachments, and integrated mobile applications can capture a disproportionate share of tech-savvy millennial and Gen Z dog owners, who represent the fastest-growing demographic of first-time pet adopters globally.

Growing sustainability awareness is boosting demand for eco-friendly and certified organic dog accessories globally

Sustainability awareness among millennials and Gen Z consumers is creating meaningful opportunities for eco-friendly dog collars, leashes, and harnesses made from recycled, organic, and biodegradable materials. Brands such as Ruff Wear Inc. have introduced products incorporating recycled content, while retailers increasingly request OEKO-TEX Standard 100-certified textiles for pet accessories. Certification bodies such as the Soil Association and the Global Organic Textile Standard (GOTS) are gaining visibility within the sector. In the United States, some premium brands are applying the Sustainable Apparel Coalition Higgs Index framework to assess supply chain impact. Eco-conscious consumers are often willing to pay a 25% premium for sustainable products, making transparency, certified sourcing, and responsible manufacturing strong competitive differentiators across both retail and direct-to-consumer channels.

Category-wise Analysis

By Product Type Insights

Dog collars represent the leading product type segment in the global dog collars, leashes & harnesses market, accounting for approximately 50% of total revenue share. Collars are the most essential and universally required dog accessory, and in many regions they are legally mandatory for identification tag display, including under the Control of Dogs Order 1992 in the United Kingdom and various U.S. state laws. This legal requirement ensures that nearly every dog owner must purchase at least one collar.

The segment’s leadership is further supported by its broad product range, including basic nylon collars, premium leather fashion collars, martingale training collars, and advanced GPS-enabled smart collars. According to the American Pet Products Association Survey, collars are the most frequently purchased and replaced accessory among U.S. dog owners. Leading brands such as Coastal Pet Products Inc., Mendota Pet, and Hunter Pet Store maintain extensive collar portfolios, strengthening the segment’s consistent revenue leadership across global retail channels.

By Material Insights

Nylon is the dominant material segment in the Dog Collars, Leashes & Harnesses market, contributing approximately 38% of total revenue. Its strong market position is driven by high durability, water resistance, easy maintenance, color flexibility, and most importantly, cost efficiency that supports competitive pricing across mass-market and mid-range tiers. Nylon webbing remains the primary construction material for most entry-level and mid-range collars, leashes, and harnesses worldwide.

Industry insights from the INDA highlight nylon’s widespread use in woven and strap-based pet accessories due to its strength-to-cost advantage. Major manufacturers such as Ancol Pet Products continue to rely heavily on nylon to support large-scale production volumes. While nylon leads in revenue, eco-friendly alternatives such as recycled PET and organic cotton are the fastest-growing material categories, particularly in North America and Europe, where sustainability-conscious consumers are increasingly willing to pay premium prices for environmentally responsible products.

By Dog Size Analysis

The Large dog size segment leads the Dog Collars, Leashes & Harnesses market, accounting for approximately 29% of total revenue. This leadership reflects both higher product pricing and the significant global population of large-breed dogs. Products designed for large dogs require more material, stronger stitching, reinforced hardware, and enhanced durability, resulting in higher average selling prices compared to small-dog equivalents.

In the United States, data from the American Pet Products Association shows that popular breeds such as Labrador Retriever and German Shepherd consistently rank among the most owned breeds, supporting sustained demand for large-format accessories. Harnesses for large dogs command particularly strong price premiums due to engineering complexity and safety requirements. Similarly, the FEDIAF confirms that large breeds represent a significant share of Europe’s dog population, reinforcing both volume and revenue dominance across developed and emerging markets.

By Application Insights

Daily walking is the dominant application segment contributing approximately 43% of total revenue share. Daily walking is the most common and consistent activity among dog owners, making collars, leashes, and harnesses essential rather than optional purchases. According to the American Pet Products Association National Pet Owners Survey, routine outdoor exercise ranks among the top activities for U.S. dog owners, ensuring steady and recurring demand for walking accessories.

This segment includes a wide range of products, from basic flat leashes to retractable leads and ergonomic no-pull harness systems. Brands such as Ruff Wear Inc. and Coastal Pet Products Inc. offer dedicated daily-walking product lines.

By Distribution Channel Insights

Online retail is the leading distribution channel in the dog collars, leashes & harnesses market, accounting for approximately 35% of total revenue and representing the fastest-growing channel globally. The transition toward e-commerce has been accelerated by the COVID-19 pandemic and reinforced by the digital purchasing preferences of millennial and Gen Z consumers. Online platforms allow customers to compare prices, read reviews, and access a wider product assortment with home delivery convenience. Alongside Amazon, these platforms account for a substantial share of online pet accessory sales in North America. Additionally, brand-owned websites are expanding rapidly as manufacturers invest in direct-to-consumer models to improve margins, strengthen customer relationships, and gather valuable consumer data insights.

Regional Insights

North America Dog Collars, Leashes & Harnesses Market Trends

The United States leads the North American dog collars, leashes & harnesses market and remains the largest and most mature national market globally. The American Pet Products Association 2023–2024 Survey reported total U.S. pet industry spending of US$ 147 billion in 2023, with dog accessories representing one of the fastest-growing categories. Regulatory requirements and local breed-specific rules in certain municipalities support consistent demand for collars and harnesses. The market is characterized by strong innovation, particularly in smart and GPS-enabled accessories. Companies such as Link AKC, Wagz Inc., and FitBark are advancing connected pet technology solutions. Canada closely follows U.S. trends, supported by high pet ownership rates and organized retail networks including PetSmart and Petco, alongside growing D2C and subscription-based accessory brands.

Europe Dog Collars, Leashes & Harnesses Market Trends

Europe represents a large and premium-focused market for dog collars, leashes, and harnesses, with strong demand across Germany, the United Kingdom, France, and Spain. According to FEDIAF, the EU had approximately 104 million pet dogs in 2023, providing a substantial customer base for accessories. In the United Kingdom, the Control of Dogs Order 1992 requires dogs in public spaces to wear identification collars, ensuring steady demand.

Germany, Europe’s largest pet market, demonstrates a strong preference for premium leather and organic-material products, supporting higher average selling prices. Regulatory harmonization under the General Product Safety Regulation (EU) 2023/988 is raising safety and quality standards across member states, benefiting established brands. Companies such as Ancol Pet Products and Hunter Pet Store compete through craftsmanship and material quality, while sustainability trends remain particularly strong in Northern and Western Europe.

Asia Pacific Dog Collars, Leashes & Harnesses Market Trends

Asia Pacific is the fastest-growing regional market for dog collars, leashes, and harnesses, supported by rising pet ownership, rapid urbanization, and growing awareness of pet care standards. China has witnessed remarkable expansion in pet ownership, with the China Pet Industry White Paper reporting over 130 million pet dogs in 2024. Urban millennials are driving premiumization trends and increasing spending on quality accessories.

E-commerce platforms such as JD.com and Tmall play a crucial role in expanding product access and accelerating online sales. Japan maintains a mature and design-oriented market, favoring compact and functional products suited for urban living. India is emerging as a high-growth market with expanding middle-class pet ownership, supported by brands such as Pets Empire. Australia remains a mature and premium-focused market, while Southeast Asian countries, including Thailand, Malaysia, and Vietnam, are steadily building organized pet retail ecosystems.

Competitive Landscape

The global dog collars, leashes & harnesses market is highly fragmented, with competition spanning multinational corporations, regional specialty brands, and numerous small-to-medium manufacturers, particularly in Asia. Established companies such as Ruff Wear Inc. and Coastal Pet Products Inc. compete primarily on material quality, ergonomic design, brand credibility, and strong distribution networks. Technology-driven brands, including FitBark and Link AKC are shaping the premium smart accessories segment through GPS tracking and health monitoring features. Strategic priorities across the industry include expanding direct-to-consumer sales channels, investing in sustainable product lines, integrating smart technologies, and entering high-growth Asia Pacific markets. Additionally, private-label offerings from major retailers such as PetSmart and Chewy, Inc. increase competitive pricing pressure, particularly within the mid-market segment.

Key Developments:

- March 2024: Ruff Wear Inc. introduced its updated Web Master Pro Harness, featuring recycled shell materials and a reinforced aluminum V-ring. This upgrade targets outdoor and adventure dog walkers prioritizing sustainability and premium performance.

Companies Covered in Dog Collars, Leashes & Harnesses Market

- Co-Leash

- Mendota Pet

- Coastal Pet Products Inc.

- Ruff Wear Inc.

- Bingin Dog

- Pets Empire

- PetsUp

- Hunter Pet Store

- Link AKC

- Wagz Inc.

- Scholar

- FitBark

- Ancol Pet Products

- PetSafe

- Kurgo

Frequently Asked Questions

The market is projected to reach US$ 12.1 Billion by 2033, growing at a CAGR of 8.6% from 2026.

Growth is driven by rising global dog ownership, pet humanization, legal collar mandates such as the Control of Dogs Order 1992, and increasing adoption of smart GPS collars from brands like FitBark and Wagz Inc.

Dog Collars dominate the market, accounting for approximately 50% of total revenue due to mandatory usage and high repurchase rates.

North America, led by the United States and supported by data from the American Pet Products Association, holds the largest market share globally.

Key players include Coastal Pet Products Inc., Ruff Wear Inc., FitBark, Wagz Inc., Ancol Pet Products, and Hunter Pet Store, among others.