- Agrochemicals

- Dicamba Market

Dicamba Market Size, Share, and Growth Forecast 2026 - 2033

Dicamba Market by Physical Form (Liquid, Dry), Time (Post-emergence, Pre-emergence), Crop Type (Cereal & grains, Oilseeds & pulses, Pastures & forage crops), and Regional Analysis, 2026 - 2033

Dicamba Market Size and Trend Analysis

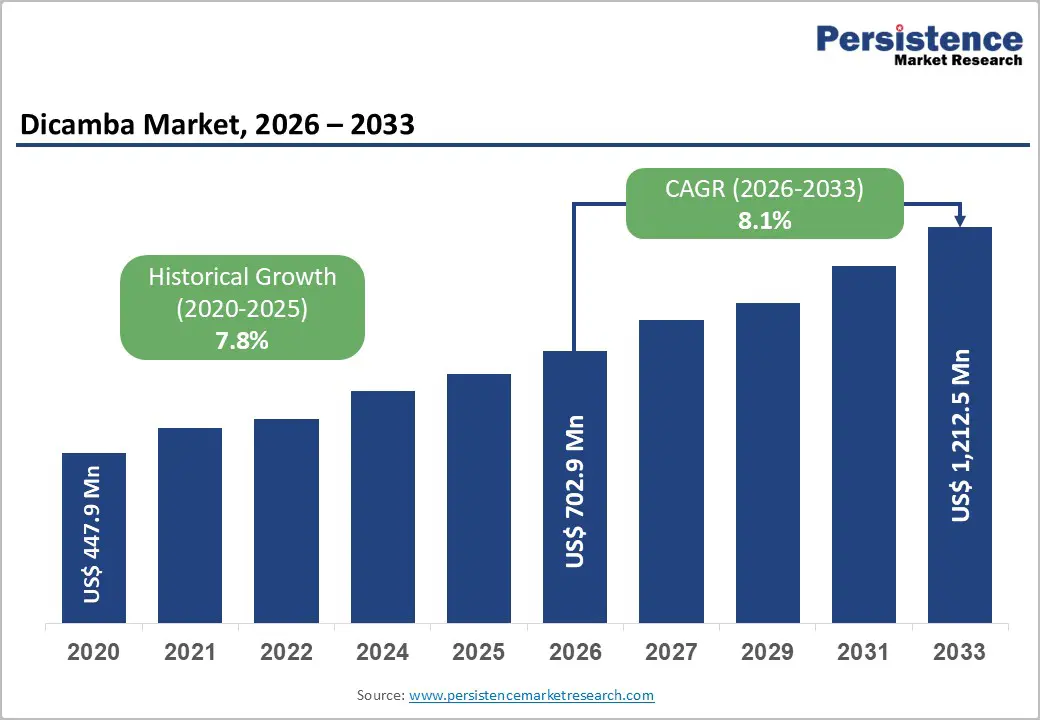

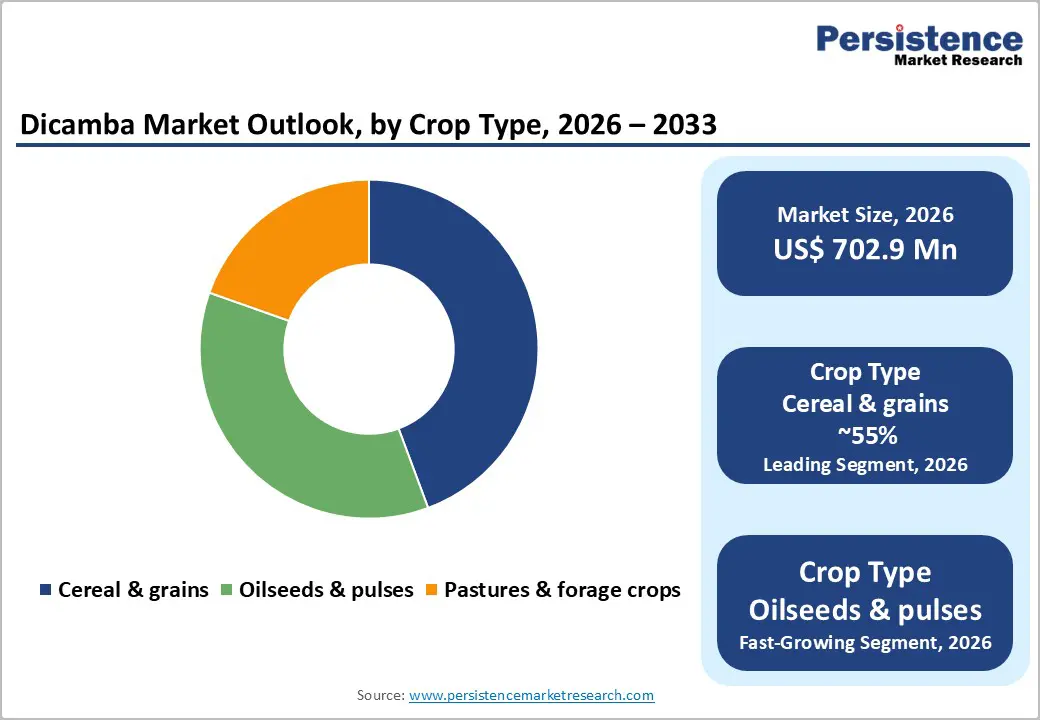

The global dicamba market is projected to reach US$ 702.9 million in 2026 and US$ 1,212.5 million by 2033, expanding at a CAGR of 8.1% over the forecast period.

Growth is primarily driven by the rising incidence of glyphosate-resistant weeds and the broader adoption of dicamba-tolerant crops, particularly soybean and cotton. As farmers shift toward integrated weed management systems, dicamba plays an increasingly strategic role in maintaining productivity and cost efficiency. Farm consolidation, larger operational scales, and regulatory frameworks that permit conditional dicamba approvals, coupled with stricter safety protocols, are expected to further support steady market expansion during the forecast period.

Key Industry Highlights:

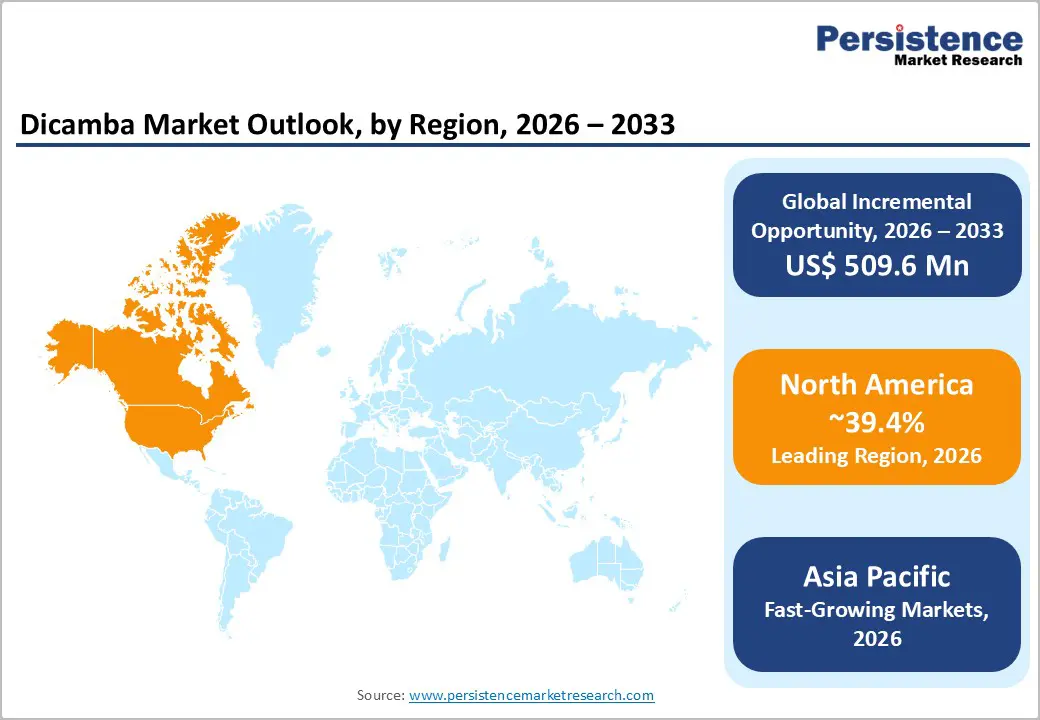

- Leading Region: North America leads the dicamba market with ~39.4% share, supported by dicamba-tolerant crop adoption and mature regulatory stewardship systems.

- Fastest-Growing Region: Asia Pacific, already accounting for ~30% of global demand, is the fastest-growing region, driven by agricultural intensification and regional manufacturing expansion.

- Dominant Physical Form: Liquid dicamba formulations hold ~70% market share, due to easier application, equipment compatibility, and alignment with drift-reduction technologies.

- Fastest-Growing Time Application: Pre-emergence application (vs. post-emergence at ~65% today) is expanding fastest as regulators and growers prioritize reduced volatility and early-season control.

- Key Opportunity: Precision agriculture integration (RTK GPS, VRT, AI systems) positions dicamba as a premium, higher-margin solution while improving drift control and farm profitability.

| Key Insights | Details |

|---|---|

| Dicamba Market Size (2026E) | US$ 702.9 Million |

| Market Value Forecast (2033F) | US$ 1,212.5 Million |

| Projected Growth CAGR (2026 - 2033) | 8.1% |

| Historical Market Growth (2020 - 2025) | 7.8% |

Market Dynamics

Drivers - Proliferation of Herbicide-Resistant Weed Species and Integrated Weed Management Requirements

The rapid spread of glyphosate-resistant weed species across key soybean, cotton, and cereal belts has transformed on-farm weed control strategies. With dicamba-tolerant crop adoption expanding, including substantial penetration across U.S. soybean acreage, growers increasingly rely on dicamba to manage persistent broadleaf weeds while protecting crop productivity and input investments.

At the same time, dicamba’s efficacy in both pre-emergence and early post-emergence programs supports integrated weed management systems. By diversifying their modes of action, farmers can slow the development of resistance, align with extension service recommendations, and safeguard long-term yield stability. This strategic fit reinforces sustained usage and strengthens overall market demand.

Advancement in Low-Volatility Dicamba Formulations and Regulatory Compliance Drivers

Continuous innovation in formulation chemistry has significantly reduced historical concerns regarding volatilization and drift associated with dicamba. Newer technologies, including diglycolamine (DGA) salts and volatility-reduction agents, have shown strong performance improvements, helping protect neighboring crops while improving stewardship credibility and grower confidence.

Regulatory authorities are increasingly emphasizing drift-mitigation standards and enhanced application practices, accelerating the shift toward premium, compliant formulations. Requirements for adjuvants and buffering systems not only elevate performance expectations but also create value-added opportunities for manufacturers. This regulatory alignment, combined with safer and more advanced formulations, is expected to reinforce market adoption and long-term product differentiation.

Restraint - Litigation, Compliance Costs, and Regulatory Uncertainty Impacting Market Access

Ongoing litigation related to off-target dicamba drift has materially increased business risk for manufacturers, distributors, and growers. Large settlement payouts and high-profile lawsuits have intensified regulatory scrutiny, while periodic court rulings have created uncertainty about product availability and legal liability. These developments have raised insurance exposure, reduced grower confidence, and slowed investment in new dicamba technologies and distribution partnerships.

At the same time, expanding regulatory obligations, including restricted-use certifications, mandatory training, application window controls, and detailed record-keeping, increases operational costs across the value chain. Smaller retailers and regional formulators are disproportionately impacted, often lacking resources to absorb compliance overheads. This combination of legal pressure and administrative burden accelerates consolidation, limits new market entrants, and constrains overall market accessibility.

Environmental Restrictions and Volatility Concerns Limiting Geographic Expansion

Environmental concerns surrounding dicamba volatilization and non-target plant damage continue to drive restrictive regulatory responses across multiple regions. Tightened label requirements, temperature-based cutoffs, and enforced buffer zones limit practical application windows and reduce growers’ willingness to rely on the product. In some geographies, proposed or enacted prohibitions significantly narrow commercial opportunities and discourage long-term investment commitments.

Beyond regulatory limits, evolving consumer preferences and the expansion of organic and non-GMO farming systems further restrict dicamba’s demand potential. These production models explicitly exclude synthetic herbicides, encouraging alternatives such as mechanical weed control or biological inputs. Together, heightened environmental scrutiny, constrained field-use conditions, and shifting production trends limit geographic expansion, compress the addressable market, and compel manufacturers to allocate substantial resources to stewardship, compliance, and risk-mitigation programs.

Opportunity - Expansion of Precision Agriculture, Sensor Technology, and AI-Driven Application Systems

The integration of precision agriculture technologies, including RTK GPS, variable rate technology (VRT), and artificial intelligence, offers significant growth potential for the dicamba market. High-accuracy systems enable targeted herbicide application, reducing chemical use while improving efficacy, supporting premium pricing, and enhancing product margins. Automated guidance and section control minimize overlap and off-target movement, thereby creating measurable environmental and economic benefits.

Dicamba manufacturers are increasingly partnering with agritech firms to develop sensor-guided, weather-adaptive application systems that optimize weed control and reduce drift risk. By embedding dicamba into these next-generation integrated crop management ecosystems, the herbicide is positioned as a premium solution, particularly in technologically advanced agricultural markets where farmers are willing to invest in high-value, efficiency-driven equipment.

Emerging Market Expansion in Asia Pacific, India, and Latin America Driven by Agricultural Intensification

Rapid agricultural intensification in the Asia Pacific, India, and Latin America presents a compelling opportunity for dicamba adoption. Expanding cultivation of oilseed, pulse, and soybean crops, coupled with the increasing incidence of herbicide-resistant weeds, drives demand for selective herbicides. In India, oilseed production increased by 15.3% between 2021 and 2023, while Brazil accounts for 40% of regional soybean acreage, consistent with dicamba’s role in glyphosate-resistance management.

Global agrochemical companies are scaling dicamba production locally, reducing supply-chain constraints and supporting aggressive market penetration. Rising farmer incomes, increased per-hectare pesticide expenditures, and regulatory frameworks that permit dicamba use further strengthen the growth outlook, positioning these regions to outpace global market expansion rates over the forecast period.

Category-wise Analysis

Physical Form Insights

Liquid formulations dominate the global dicamba market, accounting for around 70% of total usage. Their widespread adoption reflects clear operational advantages: foliar spraying enables rapid post-emergence absorption, supporting effective integrated weed management. Compatibility with standard farm spraying equipment, including tractors, hoses, and precision nozzles, combined with the ability to integrate drift-reduction agents, pH buffers, and volatility-reduction technologies, helps ensure continued preference for liquid products.

Dry formulations, while representing a smaller segment, remain relevant in niche geographic markets and specific cropping systems. These formulations are gradually being replaced in mainstream markets by liquid chemistries compatible with precision agriculture innovations, variable-rate applications, and advanced spray delivery systems, reinforcing the liquid segment’s dominant position while maintaining a specialized role for dry products.

Time Insights

Post-emergence dicamba applications account for the largest share of global usage, representing approximately 65% of the market. Applied after crops and weeds emerge, they allow farmers to respond adaptively to observed weed pressure, optimizing tactical management decisions. Post-emergence use aligns with grower preferences for operational flexibility and has driven adoption since the commercialization of dicamba-tolerant crops, offering immediate weed control in high-value cropping systems.

Pre-emergence applications, however, are the fastest-growing segment due to reduced risk of volatilization and favorable regulatory emphasis. Applied to bare soil before weed emergence, pre-emergence dicamba reduces early-season drift potential, minimizes environmental impact, and delays post-emergence treatments. Increasing regulatory focus on pre-emergence pathways is expected to expand this segment’s share in the coming years.

Crop Type Insights

Cereal and grain crops account for the largest share of dicamba applications, contributing approximately 55% of global usage. Wheat, barley, corn, and rice cultivation have historically relied on dicamba for controlling broadleaf weeds such as lambsquarters, ragweed, and mustard species. Established agronomic practices, regulatory familiarity, and consistent yield protection in these crops create a stable and recurring revenue base for manufacturers worldwide.

Oilseeds and pulses, however, represent the fastest-growing crop segment. Dicamba adoption in soybean and emerging pulse crops addresses resistant weed populations, transforming weed management strategies. Growth in these crops is driven by technological adoption, resistance management needs, and increasing crop acreage, thereby supporting expanding demand and diversifying dicamba applications beyond traditional cereal and grain systems.

Regional Insights

North America Dicamba Market Trends

North America remains the leading dicamba market, accounting for about 39.4% of global revenue. Widespread adoption of dicamba-tolerant soybean and cotton systems has reshaped weed control practices, supported by deep grower familiarity and advanced mechanization. Strong stewardship programs and premium, low-volatility formulations have reinforced confidence, while coordinated U.S.-Canada regulatory oversight continues to shape responsible usage standards and market structure.

Regulatory frameworks emphasizing buffer zones, application timing, and training requirements have encouraged technology upgrades rather than dicamba substitution. Litigation outcomes and rising compliance costs have also prompted manufacturers to adopt premium, value-added solutions. Together, these factors sustain North America as the region with the highest premium product penetration and margin potential over the forecast period.

Europe Dicamba Market Trends

Europe represents a structurally constrained dicamba market, characterized by restrictive environmental regulations and precautionary approval standards. National differences in product registrations, combined with limits on over-the-top applications and dicamba-tolerant systems, significantly reduce usage intensity compared with North America. As a result, demand is concentrated mainly in traditional cereal and grain programs.

With policy direction focused on sustainability, organic farming, and biodiversity objectives, dicamba growth remains subdued. Europe is projected to grow at a modest low-single-digit CAGR of 2-3%, reflecting tighter application windows, monitoring requirements, and limited label expansion. Participation is dominated by large multinationals that operate efficiently within regulatory constraints, keeping market growth below global averages.

Asia Pacific Dicamba Market Trends

Asia-Pacific is emerging as the fastest-growing regional market, accounting for approximately 30% of global dicamba demand and gaining market share rapidly. Rising herbicide resistance, expanding soybean and pulse cultivation, and growing investment in crop protection infrastructure are key demand drivers across China, India, and Southeast Asia. Localized production capacity and cost advantages further enhance competitiveness.

Supportive government programs that boost agricultural productivity, combined with the gradual adoption of advanced weed-management systems, are accelerating market penetration. More flexible regulatory environments and rising farmer purchasing power enable faster product adoption than in developed regions. These dynamics position the Asia Pacific as the most attractive expansion frontier for manufacturers, with sustained long-term growth prospects.

Competitive Landscape

The dicamba market is moderately consolidated, with a small group of global agrochemical leaders accounting for most sales and shaping pricing, technology standards, and regulatory engagement. High investment requirements for product stewardship, volatility-mitigation research, and registration maintenance reinforce incumbent dominance and create structural barriers for new entrants.

Competition increasingly centers on formulation innovation, regulatory reliability, and integrated agronomic support. Cost-focused producers, particularly in emerging economies, target price-sensitive segments through contract manufacturing and flexible supply chains, while premium suppliers emphasize low-volatility chemistries and precision-application compatibility. Ongoing regulatory reviews may open selective opportunities for repositioning among players able to deliver next-generation stewardship solutions.

Key Developments:

- In July 2025, the United States Environmental Protection Agency announced proposals to unconditionally register XtendiMax, Engenia, and Tavium for over-the-top applications on dicamba-tolerant soybeans and cotton, incorporating enhanced mitigation measures, including volatility-reduction agents, drift-reduction buffers, and temperature-based application restrictions, intended to minimize off-target movement and environmental impact.

- In May 2024, Bayer AG and BASF SE agreed to provide approximately US$400 million in settlement payments to farmers affected by dicamba drift damage between 2015 and 2024, concluding multiyear litigation and establishing precedent for manufacturer accountability in herbicide off-target movement incidents.

- In December 2023, Yashashvi Rasayan Private Limited commissioned a 4,000 metric tons per annum dicamba manufacturing facility in India, enabling regional supply of herbicide products and supporting accelerated dicamba adoption in emerging agricultural markets throughout South Asia and Southeast Asia.

Companies Covered in Dicamba Market

- Bayer AG

- BASF SE

- Syngenta Group

- Corteva Agriscience

- Nufarm Limited

- UPL Ltd.

- FMC Corporation

- Albaugh LLC

- ADAMA Ltd.

- Sumitomo Chemical Co., Ltd.

- Gharda Chemicals Ltd.

- Sinochem Group

- Jiangsu Yangnong Chemical Group Co., Ltd.

- Shandong Weifang Rainbow Chemical Co., Ltd.

- Zhejiang Xinan Chemical Industrial Group Co., Ltd.

Frequently Asked Questions

The global dicamba market is expected to grow from US$ 702.9 Million in 2026 to US$ 1,212.5 Million by 2033, at a CAGR of 8.1%, driven by resistant weeds, dicamba-tolerant crops, and improved formulations.

Growth is fueled by glyphosate-resistant weeds, expanding dicamba-tolerant crop acreage, and newer low-volatility chemistries that support regulatory approvals.

Liquid dicamba leads with about 70% market share, thanks to easier spraying, rapid absorption, and strong compatibility with precision agriculture tools.

North America dominates with ~39.4% market share, supported by dicamba-tolerant soybean/cotton systems and advanced regulatory and stewardship frameworks.

Precision agriculture integrating RTK GPS, variable-rate systems, and AI guidance offers the largest opportunity by enabling premium pricing, drift control, and higher farm profitability.

The dicamba market is dominated by multinational agrochemical leaders Bayer AG, BASF SE, Syngenta AG, Corteva Agriscience, and FMC Corporation.