- Clothing, Footwear, & Accessories

- Desert Boots Market

Desert Boots Market Size, Share, and Growth Forecast, 2026 – 2033

Desert Boots Market by Material Type (Suede, Leather, Others), Price Point (Mass, Mid-Range, Premium/Luxury), Distribution Channel (Offline/Retail, Online/E-commerce), End-user (Men, Women, Children), and Regional Analysis 2026 – 2033

Desert Boots Market Size and Trends Analysis

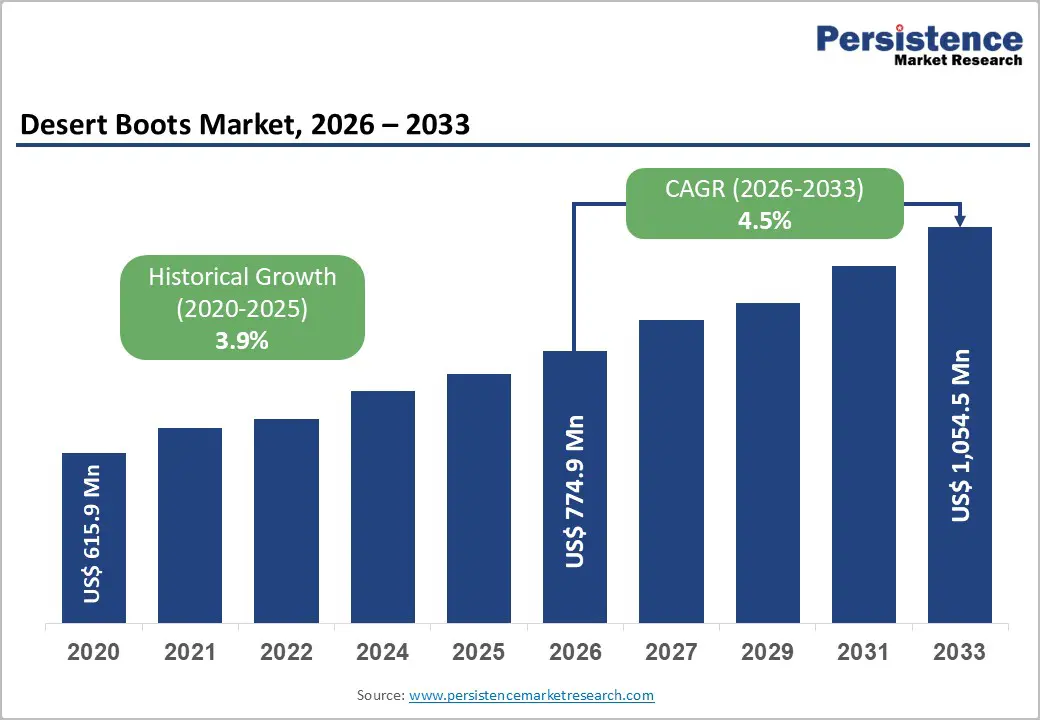

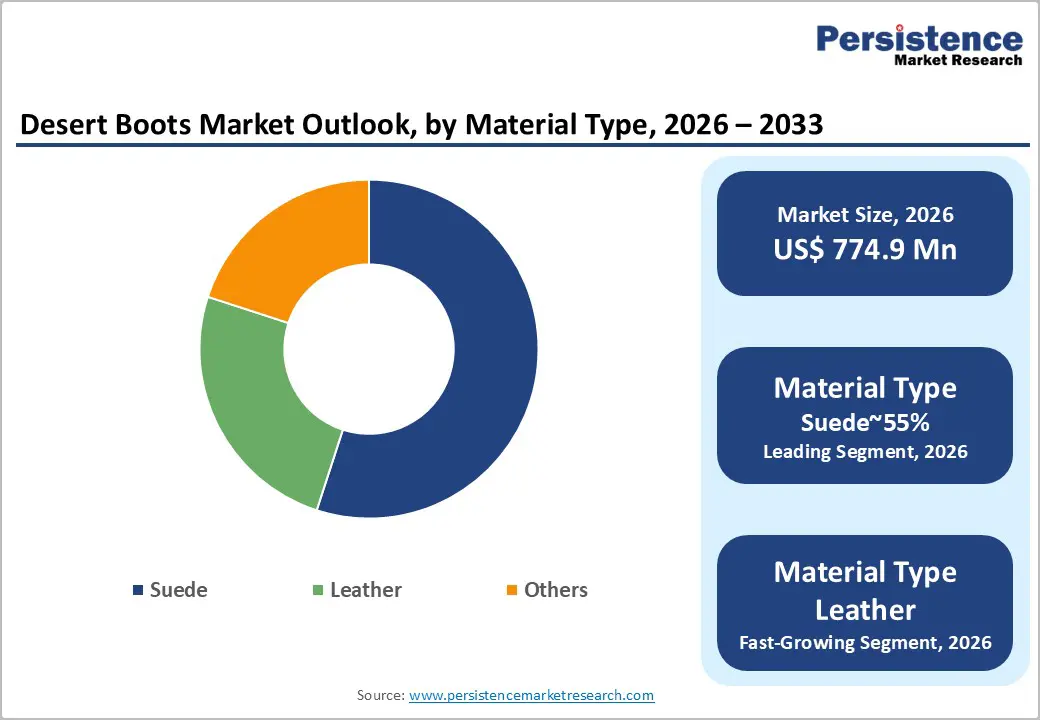

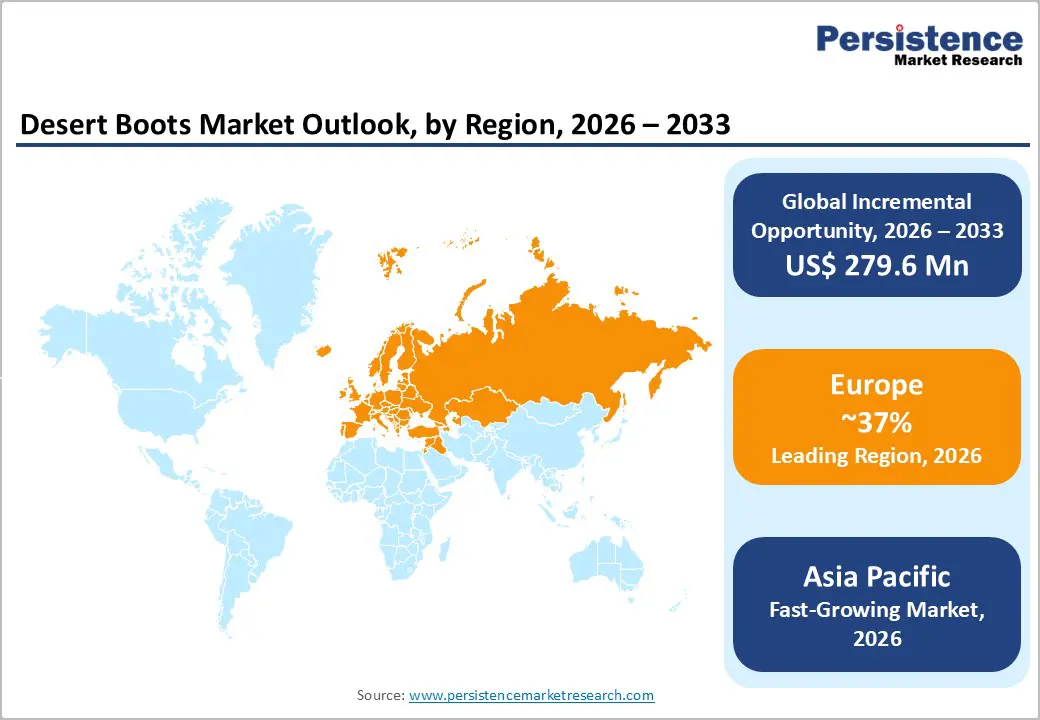

The global desert boots market size is likely to be valued at US$774.9 million in 2026 and is expected to reach US$1,054.5 million by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by the structural shift toward "business casual" attire in corporate environments and a heightened consumer appetite for versatile, cross-seasonal footwear. The integration of sustainable material supply chains and the rapid digital transformation of Direct-to-Consumer (DTC) sales channels are reshaping the competitive landscape.

Key Industry Highlights:

- Leading Region: Europe is projected to lead due to entrenched heritage manufacturing clusters, regulatory harmonization under EU chemical compliance frameworks, and vertically integrated leather ecosystems, accounting for approximately 37% share in 2026, supported by sustainability-led technology adoption and advanced tanning infrastructure advantages.

- Fastest-Growing Region: Asia Pacific is anticipated to grow the fastest due to rapid urban industrial expansion, trade integration under regional agreements, rising disposable income, and accelerated digital commerce adoption across manufacturing and consumer sectors.

- Leading Material Type: Suede is expected to lead accounting with approximately 55% share through entrenched industrial adoption in 2026, mature tanning throughput, consistent nap quality standards, and sustained relevance in high-value smart-casual applications.

- Leading Distribution Channel: Offline/Retail is projected to dominate for tactile verification simplicity, structured cost economics, established consumer adoption, and functional fit assurance across key urban sectors, holding approximately 57% share in 2026.

| Report Attribute | Details |

|---|---|

|

Desert Boots Market Size (2026E) |

US$774.9 Mn |

|

Market Value Forecast (2033F) |

US$1,054.5 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Structural Realignment of Professional Dress Codes Toward Hybrid Footwear Demand

The normalization of hybrid work frameworks is restructuring global footwear consumption patterns. Flexible employment models are institutionalizing relaxed yet professionally credible dress expectations. Desert boots are positioned between athletic sneakers and formal leather footwear categories. This intermediate positioning captures demand from professionals navigating multi-context daily routines. Workplace wardrobe codes increasingly prioritize ergonomic comfort alongside understated visual authority. Minimalist silhouettes and durable uppers align with evolving corporate aesthetic standards. Retail assortments are recalibrating toward lifestyle versatile non-athletic footwear classifications. This shift expands addressable demand across office, travel, and social environments.

Design priorities emphasize lightweight construction and material resilience. Manufacturers are optimizing the latest engineering to balance support with extended wear comfort. Sourcing strategies increasingly favor suede treatments and crepe sole innovations. These material decisions influence cost structures and gross margin stabilization dynamics. Omnichannel retail analytics reinforce inventory allocation toward adaptable professional styles. Brand portfolios are repositioned to reflect contemporary business casual identity shifts. Regulatory workplace safety norms indirectly support closed-toe structured footwear adoption. Hybrid employment permanence anchors sustained structural demand for desert boots.

Advancement of Bio-Based Material Engineering and Regulatory Alignment

Shifting consumer expectations are accelerating material innovation within footwear manufacturing ecosystems. Younger demographics increasingly demand transparent sourcing and reduced environmental externalities. Bio-based leathers and recycled suede alternatives are gaining structural market acceptance. These materials address lifecycle emissions concerns embedded within global supply chains. Regulatory frameworks emphasize chemical compliance and traceability across tanning processes. Vegetable tanning methods eliminate chromium exposure and associated environmental liabilities. Sustainability certifications increasingly influence wholesale procurement and retail listing decisions. This transition embeds environmental compliance within core product development cycles.

Bio material adoption reshapes sourcing dependencies. Conventional raw hide markets expose manufacturers to volatility and supply disruption. Bio-based inputs offer comparatively stable procurement economics and traceable origins. Process innovation reduces waste treatment burdens and downstream compliance expenditures. Manufacturers reconfigure supplier partnerships toward regenerative agricultural feedstocks. Margin structures benefit from predictable input pricing and lower remediation liabilities. Retail positioning integrates sustainability credentials into core brand architecture. Collectively, material science evolution strengthens resilience across desert boot production networks.

Barrier Analysis – Competitive Encroachment from Performance-Oriented Sneaker Technologies

The ongoing sneakerization trend is reshaping global non-athletic footwear hierarchies.

Consumers increasingly prioritize advanced cushioning and biomechanical support systems. Hybrid sneaker boot constructions blur categorical boundaries within retail assortments. This convergence intensifies substitution risk across heritage desert boot portfolios. Athletic conglomerates leverage substantial research capabilities and proprietary midsole platforms. Comfort engineering now competes directly with traditional craftsmanship narratives. Retail floor space reallocations increasingly favor performance-infused lifestyle models. Category fragmentation heightens pricing pressure across conventional suede boot offerings.

Ergonomic integration alters component sourcing priorities. Manufacturers must incorporate shock-absorbing midsoles and anatomical footbed technologies. Failure to adopt orthopedic innovations elevates substitution elasticity within core demographics. Production complexity increases as lightweight composites replace conventional crepe constructions. Research investments shift toward gait analysis and material rebound optimization. Margin compression emerges when craftsmanship premiums lack functional differentiation. Distribution channels prioritize technology-validated claims over heritage storytelling. The performance convergence structurally challenges traditional desert boot positioning.

Volatility in Premium Suede Sourcing and Trade Cost Pressures

The desert boots market faces sustained volatility in premium suede procurement. High-grade leather inputs remain exposed to cyclical livestock and commodity shifts. Trade tariff escalations between manufacturing and consumption hubs elevate landed costs. These cumulative duties structurally inflate import expenses across footwear categories. Manufacturers confront constrained flexibility within tightly calibrated margin frameworks. Cost absorption strategies directly compress profitability across mid-tier portfolios. Price pass-through mechanisms risk demand contraction within mass-positioned segments. Input instability therefore transmits financial stress across the entire value chain.

Suede production requires specialized tanning capabilities and technical process control. The limited supplier base concentrates sourcing risk within select geographic clusters. Seasonal demand spikes intensify procurement competition among branded manufacturers. Supply bottlenecks disrupt production scheduling and inventory replenishment cycles. Working capital requirements increase as firms secure forward material contracts. Compliance with environmental treatment standards further narrows qualified suppliers. These constraints reinforce dependency on vertically integrated or long-term partners. This sourcing concentration embeds structural fragility within desert boot manufacturing networks.

Opportunity Analysis – Strategic Demand Expansion through Women's Lifestyle Diversification

The desert boots market remains structurally concentrated within male consumer cohorts. However, women represent the most accelerated adoption segment across lifestyle footwear. Contemporary fashion narratives increasingly legitimize androgynous and boyfriend-inspired silhouettes. Desert boots integrate seamlessly with dresses, tailoring, and casual denim assortments. This cross-styling adaptability enhances year-round wardrobe utility perceptions. Retail platforms identify underrepresented female consumers within heritage boot categories. Product repositioning, therefore, targets aesthetic refinement without diluting core design language. Such recalibration structurally widens the addressable consumer base.

Feminine-specific engineering requires modified last geometries. Narrower fits and differentiated heel elevations alter tooling and sampling workflows. Marketing investments shift toward segmented storytelling within digital commerce channels. Inventory planning integrates broader size curves and seasonal capsule introductions. Revenue projections indicate incremental contribution from women-focused portfolio expansion. Margin realization depends on aligning fashion responsiveness with disciplined cost control. Distribution partners increasingly allocate shelf space toward gender diversified collections.

Acceleration of Sustainable Eco Leather Integration

The desert boots market is undergoing material substitution toward eco-leather platforms. Environmental accountability expectations increasingly influence footwear purchasing behavior globally. Eco leather alternatives reduce reliance on conventional chromium-intensive tanning systems. This transition aligns with tightening chemical compliance frameworks across export markets. Lifecycle transparency requirements reshape procurement standards within manufacturing ecosystems. Sustainable inputs strengthen brand positioning within environmentally conscious retail channels. Material traceability initiatives integrate digital tracking across upstream supply networks. Eco leather adoption becomes embedded within long term product roadmaps.

Sustainable materials alter sourcing and processing economics. Eco leather suppliers require certified feedstocks and controlled conversion technologies. Production lines adapt to accommodate alternative finishing and bonding characteristics. Waste management costs decline through reduced hazardous effluent treatment obligations. Compliance expenditures shift toward certification audits and environmental documentation systems. Margin structures benefit from reputational premiums and regulatory risk mitigation. Retail buyers increasingly prioritize collections demonstrating verified sustainability credentials. Eco leather expansion enhances structural resilience within desert boot manufacturing.

Category–wise Analysis

Material Type Insights

Suede is projected to lead the market, accounting for approximately 55% share in 2026, supported by entrenched heritage positioning and material familiarity across global retail channels. Its distinctive nap texture and immediate pliability align with smart casual workplace transitions, reinforcing relevance within hybrid professional wardrobes. Brands such as Clarks Originals, Astorflex, Drake’s, and Common Projects sustain dominance through premium suede sourcing and differentiated finishing technologies. Integration of nano-coated performance suede and waterproof treatments addresses historical durability concerns without compromising breathability. Leather Working Group-compliant traceability protocols further stabilize enterprise procurement standards. Hybrid sole innovations pairing suede uppers with Vibram or EVA platforms modernize comfort architecture while preserving aesthetic continuity. This convergence of heritage equity, supply chain maturity, and adaptive product engineering sustains suede’s structural leadership.

Leather is projected to be the fastest-growing segment, propelled by systemic shifts in material governance and ethical consumption frameworks. Adoption accelerates as brands integrate mycelium composites, pineapple fibers, and DryTan processing to reduce chemical intensity and water dependency. Companies including Allbirds, Veja, Vivobarefoot, and Will’s Vegan Store are embedding plant-based and bio-derived platforms into core desert boot portfolios. NFC-enabled digital product passports enhance transparency by communicating environmental footprint metrics directly to consumers. Retail green listing policies increasingly prioritize certified low-impact materials within merchandising strategies. Improved tensile strength and water resistance characteristics now meet the structural requirements unique to desert boot construction. These technological and commercial inflection points position eco leather as the category’s velocity driver.

Distribution Channel Insights

Offline/Retail is expected to lead, accounting for approximately 57% share in 2026, supported by the category’s high-touch purchase dynamics and fit sensitivity. Consumers prioritize tactile verification of suede texture, crepe sole flexibility, and break-in comfort before purchase. Heritage brands such as Clarks and Woodland leverage flagship environments to reinforce craftsmanship narratives and material authenticity. Retailers, including Nordstrom and Selfridges, are advancing phygital showroom models integrating localized fulfillment nodes. In-store gait analysis and foot scanning technologies enhance conversion rates while reducing post-purchase returns. Physical outlets also function as experiential hubs through curated boutiques and resole clinics that deepen lifecycle engagement. This integration of sensory assurance, brand storytelling, and supply chain efficiency sustains offline channel dominance.

Online/E-commerce - Direct to Consumer (D2C) is estimated to be the fastest-growing segment, driven by digital fit intelligence and margin accretive disintermediation strategies. Brands such as Thursday Boot Co., Koio, Nisolo, and Clarks Digital are deploying AI-powered fit stylists and LiDAR-enabled virtual try-on systems. These tools materially reduce sizing uncertainty while narrowing historical return rate disadvantages. Direct ownership of first-party consumer data enables hyper-personalized assortment planning and targeted lifecycle marketing. Urban micro fulfillment centers compress delivery windows, neutralizing the instant gratification advantages of physical retail. Social commerce integrations and tiered digital loyalty programs accelerate conversion velocity. This convergence of technology, data monetization, and global size aggregation positions DTC as the channel’s structural growth engine.

Regional Insights

Europe Desert Boots Market Trends

Europe leads the global market with a 37% share and is expected to retain structural dominance due to its entrenched heritage positioning in 2026, regulatory rigor, and vertically integrated leather ecosystem. The region functions as the historical and qualitative benchmark for the category, with production clusters concentrated across the U.K., Italy, Germany, France, and Spain. Regulatory harmonization under frameworks such as the European Union REACH regulation and the European Green Deal is expected to continue reshaping material sourcing, chemical compliance, and traceability standards, reinforcing Europe’s premium manufacturing profile. Sustainability mandates, including durability scoring and circular economy directives, are anticipated to favor established manufacturers that already operate within high environmental thresholds. Heritage demand remains structurally resilient, as desert boots are positioned as enduring wardrobe staples rather than cyclical fashion items. Fragmentation persists at the regional level, yet established brands maintain disproportionate influence over design language, craftsmanship standards, and retail merchandising norms.

Germany anchors Europe’s forward momentum and is projected to remain the region’s most structurally stable growth engine, supported by a craftsmanship-driven consumer base and strict environmental compliance culture. German buyers prioritize durability, certified material sourcing, and repairability, aligning directly with European sustainability mandates. National enforcement of chemical safety frameworks tied to EU REACH is expected to accelerate the adoption of metal-free tanning, vegan suede alternatives, and traceable supply chains. Domestic retailers increasingly emphasize transparent sourcing disclosures, reinforcing consumer trust and brand equity. Investment into eco-efficient production facilities across Central Europe is anticipated to deepen regional supply chain consolidation, reducing reliance on extra-European inputs. As sustainability regulation tightens and consumer scrutiny intensifies, Germany is expected to reinforce Europe’s leadership position by institutionalizing high-quality, low-impact desert boot manufacturing standards that shape export competitiveness and long-term category resilience.

Asia Pacific Desert Boots Market Trends

Asia Pacific is projected to emerge as the fastest-growing region, which operates under a dual-engine structure, functioning simultaneously as the world’s primary footwear manufacturing base and an accelerating consumption hub. China, India, Japan, and key ASEAN economies collectively drive this expansion through rapid urbanization, rising disposable income, and digital retail penetration. The expansion of cross-border trade frameworks such as the Regional Comprehensive Economic Partnership is expected to streamline intra-regional sourcing and reduce tariff friction, strengthening supply chain integration. Asia Pacific’s cost-efficient production ecosystem, supported by intelligent manufacturing upgrades and material optimization technologies, is anticipated to maintain pricing competitiveness across both leather and synthetic desert boot categories. Increasing adoption of affordable synthetic alternatives and lightweight sole technologies is projected to further align product design with regional climate conditions and price sensitivity, reinforcing structural growth momentum.

China anchors the region’s forward trajectory and is expected to remain the dominant manufacturing and consumption nucleus within Asia Pacific. National enforcement under the Standardization Administration of China framework is anticipated to streamline product compliance while facilitating controlled import expansion. Consolidation of environmentally compliant tanneries and investment in automated cutting and assembly facilities are projected to enhance efficiency and material utilization. Domestic brands are expected to intensify competition with international players by leveraging vertically integrated production and rapid product refresh cycles. Simultaneously, multinational manufacturers continue to invest in adjacent production corridors across India and Southeast Asia to diversify geopolitical risk while maintaining proximity to end markets. As digital commerce ecosystems deepen across Tier 1 and Tier 2 cities, China is anticipated to reinforce Asia Pacific’s position as the primary growth accelerator for the global desert boots category.

North America Desert Boots Market Trends

North America represents a stable and institutionally mature region, and the stability is supported by high discretionary footwear spending, an advanced direct-to-consumer ecosystem, and strong brand consolidation across mid-premium and heritage tiers. Consumer demand centers on durability, versatility, and work-to-weekend adaptability, positioning desert boots as practical lifestyle footwear rather than purely fashion-driven products. Regulatory oversight from the U.S. Consumer Product Safety Commission reinforces material safety and labeling compliance, strengthening consumer confidence in premium price points. The market is characterized by established multinational players and digitally native brands that prioritize margin expansion through owned e-commerce platforms. Sustainability-focused product lines and chrome-free tanning adoption are expected to accelerate as environmental disclosure requirements and state-level chemical regulations intensify. While growth remains moderate compared to Asia Pacific, North America is projected to maintain predictable replacement-driven demand supported by high brand loyalty and structured retail distribution.

The U.S. anchors regional performance and is expected to remain the principal revenue generator within North America. A sophisticated innovation ecosystem, strong hybrid-work culture, and elevated casualization trends continue to reinforce steady demand for smart-casual footwear silhouettes. Enforcement under the INFORM Consumers Act is anticipated to reduce counterfeit penetration across online marketplaces, redirecting traffic toward official brand channels. Strategic capital allocation into domestic automation and nearshoring partnerships in Mexico is projected to improve supply chain resilience while mitigating tariff exposure. Direct-to-consumer investment, digital marketing optimization, and sustainable material transitions are expected to define competitive differentiation over the forecast period. As consumer preference converges around value-per-wear, durability, and ethical sourcing transparency, the U.S. is anticipated to sustain North America’s stable yet structurally profitable desert boots market position.

Competitive Landscape

The global desert boots market is moderately fragmented, with leadership concentrated among global footwear suppliers such as Clarks, Dr. Martens, Wolverine Worldwide, and digitally native entrants including Thursday Boot Company. While no single participant exercises structural control over pricing, leading brands exert disproportionate influence over design standards, sourcing practices, and retail merchandising norms. Their scale, established supplier relationships, and multi-channel distribution capabilities shape procurement preferences across department stores, specialty retailers, and online platforms. Brand-led storytelling and sustainability disclosures increasingly define competitive credibility, reinforcing the authority of established players within premium and mid-tier segments.

Competitive positioning reflects clear horizontal and vertical differentiation across the value chain. Legacy brands emphasize heritage craftsmanship, vertically integrated sourcing, and wholesale-retail balance; while emerging direct-to-consumer operators prioritize margin optimization, digital fit technology, and first-party data ownership. Industry behavior indicates gradual ecosystem consolidation through targeted acquisitions, portfolio rationalization, and platform integration strategies that combine product, digital commerce, and after-sales services.

Key Industry Developments:

- In January 2026, Clarks Originals announced plans to introduce its first dedicated apparel collection for the Spring/Summer 2026 season. The initiative leverages the brand’s iconic Desert Boot and Wallabee silhouettes to expand into a broader lifestyle offering, enabling the company to deliver a more cohesive brand aesthetic to its global customer base.

- In September 2025, 3G Capital completed the US$11.4 billion take-private acquisition of Skechers. The transition to private ownership is expected to provide the company with greater strategic flexibility, enabling long-term operational restructuring and investment initiatives without the short-term pressures associated with public market reporting.

- In April 2025, Red Wing Shoe Company joined the United States Footwear Manufacturers Association (USFMA) to support the advancement of domestic footwear manufacturing and innovation. The move strengthens the company’s alignment with emerging U.S. research initiatives and advanced production facilities, reinforcing its “Made in USA” manufacturing proposition.

Companies Covered in Desert Boots Market

- C & J Clarks International

- Red Wing Shoes

- Dr. Martens

- Thursday Boot Co.

- Timberland LLC

- Wolverine World Wide

- ASTORFLEX SRL

- Jim Green Footwear

- Rancourt & Co

- Taylor Stitch

- JADD Shoes

- Bearpaw

- John Lofgren

- PUMA SE

- Skechers

Frequently Asked Questions

The global desert boots market is projected to be valued at US$774.9 million in 2026 and is expected to reach US$1,054.5 million by 2033, supported by sustained demand for business-casual footwear and the expansion of direct-to-consumer retail models.

The normalization of hybrid work environments is reshaping professional dress codes, increasing demand for versatile footwear positioned between formal leather shoes and athletic sneakers. Desert boots meet this requirement through minimalist design, cross-season adaptability, and ergonomic comfort, making them suitable for office, travel, and social settings while maintaining professional credibility.

The desert boots market is forecast to grow at a CAGR of 4.5% from 2026 to 2033, reflecting steady structural demand supported by material innovation and omnichannel retail expansion.

Europe is the leading regional market, accounting for approximately 37% share, driven by strong heritage positioning, vertically integrated leather supply chains, and regulatory frameworks that reinforce sustainable manufacturing and premium craftsmanship standards.

The desert boots market is moderately fragmented, with key players including C. & J. Clark International, Dr. Martens, Wolverine World Wide, Red Wing Shoe Company, and VF Corporation. These companies compete through heritage branding, vertically integrated sourcing, expanding DTC platforms, and differentiated material innovation strategies.