- Agrochemicals

- Crop Growth Regulators Market

Crop Growth Regulators Market Size, Share, and Growth Forecast 2026 - 2033

Crop Growth Regulators Market by Product Type (Auxins, Gibberellins, Cytokinins, Ethylene, Abscisic Acid (ABA), Others), by Function (Promoters, Inhibitors), by Formulation (Liquid Form, Powder, Emulsifiable Concentrates, Others), by Crop Type (Fruits & Vegetables, Cereals & Grains, Oilseeds & Pulses, Turf & Ornamentals, Others), and Regional Analysis, 2026 - 2033

Crop Growth Regulators Market Size and Trend Analysis

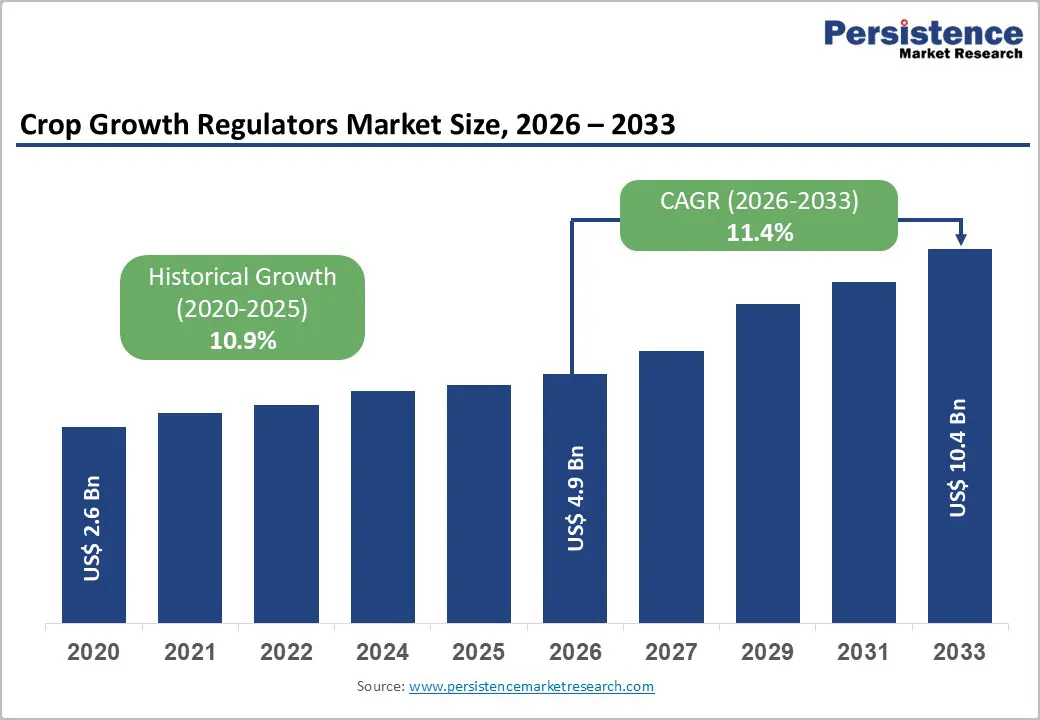

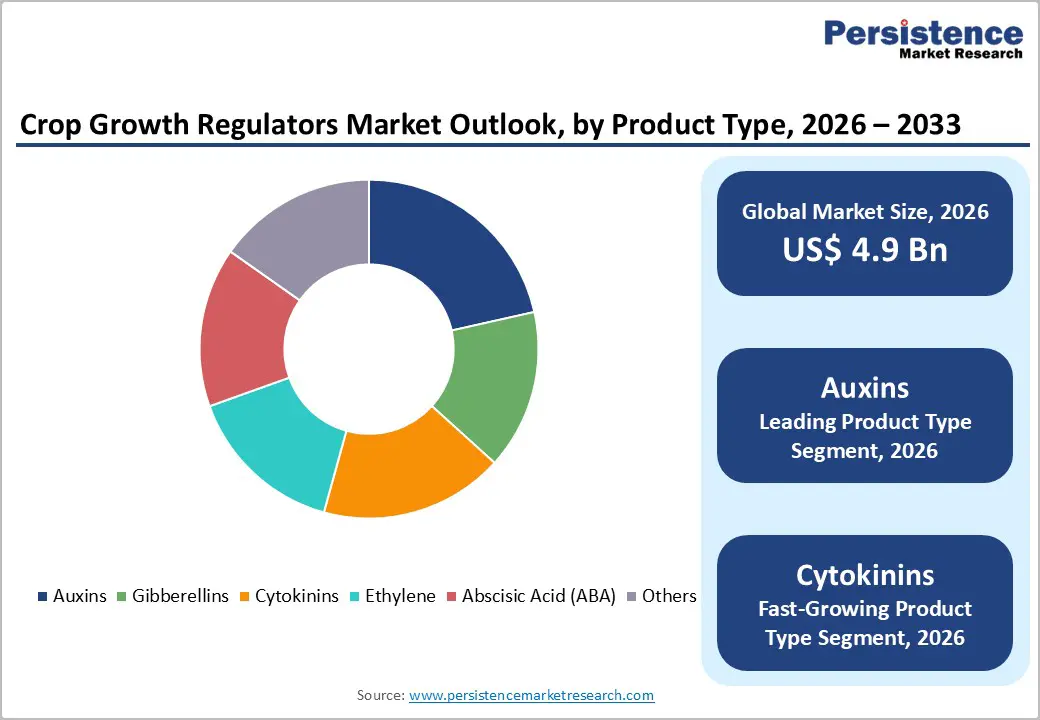

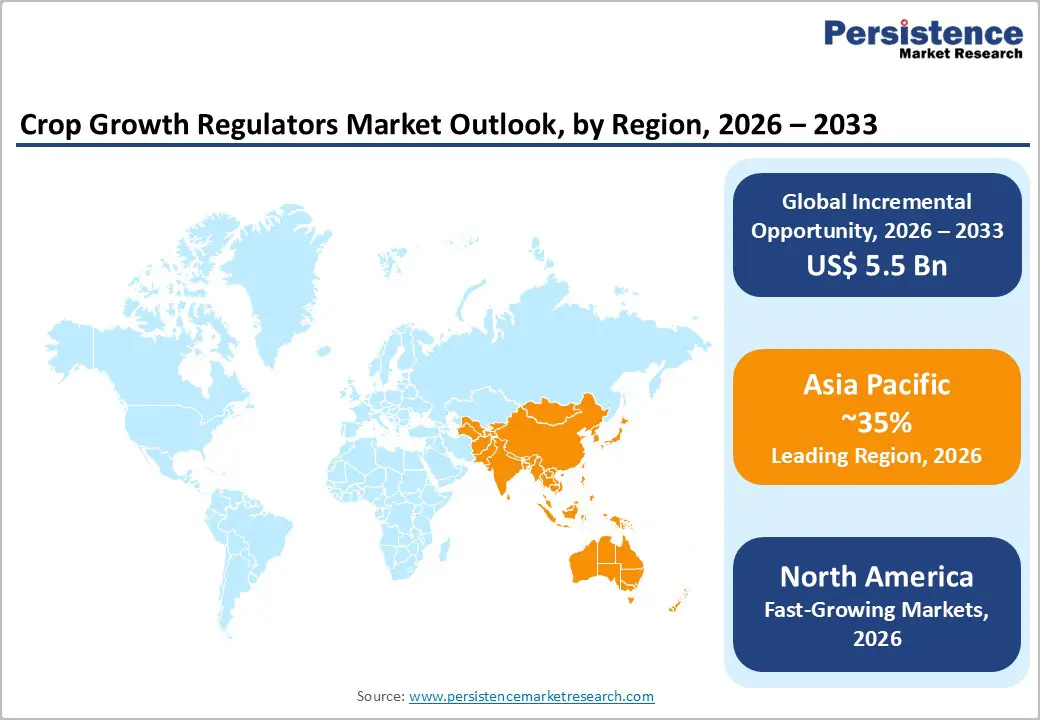

The global crop growth regulators market size is expected to be valued at US$ 4.9 billion in 2026 and projected to reach US$ 10.4 billion by 2033, growing at a CAGR of 11.4% between 2026 and 2033.

Market expansion is driven by rising global food demand due to population growth, as crop growth regulators improve yields, fruit quality, and stress resilience. In 2022, global consumption of plant growth regulators reached 51.69 thousand metric tons, highlighting strong agricultural adoption. Additionally, advancements in precision agriculture and sustainable farming practices are accelerating market growth by optimizing resource efficiency and crop performance.

Key Industry Highlights:

- Leading Region: Asia Pacific dominates the Crop Growth Regulators market with 35% share in 2025, driven by population growth and extensive arable land.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with a 12% CAGR between 2025–2032, fueled by modernization in China and India.

- Leading Product Type: Auxins lead the product type segment with 31% share in 2025, essential for root growth, fruit development, and integrated crop management.

- Leading Function: Promoters dominate the function segment with 65% share in 2025, enhancing yield, stress tolerance, and crop productivity across major crops.

- Key Opportunity Segment: Bio-based and eco-friendly regulators are emerging as a high-potential opportunity, especially in sustainable, high-value crops.

| Key Insights | Details |

|---|---|

|

Crop Growth Regulators Size (2026E) |

US$ 4.9 billion |

|

Market Value Forecast (2033F) |

US$ 10.4 billion |

|

Projected Growth CAGR(2026-2033) |

11.4% |

|

Historical Market Growth (2020-2025) |

10.9% |

Market Dynamics

Drivers - Rising Global Food Demand and Need for Yield Enhancement

The increasing world population, coupled with shrinking arable land, is creating immense pressure on agriculture to produce more with less. Crop growth regulators play a critical role in this context, enabling higher crop productivity without the need to expand farmland. Regulators like auxins and gibberellins enhance fruit set, size, and overall yield, contributing to efficient resource utilization.

Orchard trials demonstrate yield improvements of 18–22% in fruits with regulator use, supporting sustainable intensification. By boosting output on existing farmland, these products reduce food security risks, align with FAO recommendations for efficient agriculture, and help farmers meet the rising global demand for high-quality crops while maintaining environmental sustainability.

Increasing Adoption of Precision Agriculture Technologies for Optimized Regulator Use

Precision agriculture is transforming modern farming by integrating crop growth regulators with advanced technologies such as drones, IoT sensors, and GPS-guided sprayers. This approach ensures targeted application, maximizing efficacy while minimizing chemical waste and environmental impact.

USDA data shows significant adoption of these technologies, enhancing nutrient uptake and stress tolerance. Industry trials indicate that ultra-low-volume sprayers reduce regulator application rates by 29%, cutting costs and improving sustainability. The convergence of technology and regulators strengthens stakeholder confidence in data-driven, efficient, and environmentally responsible agricultural practices.

Restraints - Stringent Regulatory Approvals and High Compliance Costs Limiting Market Entry

Crop growth regulators face rigorous scrutiny from regulatory agencies such as the EPA and EU authorities, which require extensive testing and documentation before approvals. Compliance with standards like FIFRA, which classifies many regulators as pesticides, often delays product launches and adds substantial costs, affecting time-to-market.

Recent regulatory actions against unregistered products highlight the risks for manufacturers, especially smaller players. These hurdles restrict market entry, slow innovation, and limit product availability. As a result, companies must invest heavily in regulatory compliance to maintain competitiveness, impacting profitability and strategic planning, particularly in regions with complex approval processes.

Challenges from Crop Resistance Development and Raw Material Volatility

Over time, crops can develop resistance to certain growth regulators, necessitating continuous research and development to formulate more effective products. This ongoing R&D investment significantly increases operational costs for manufacturers.

Additionally, raw materials for regulators, often linked to petrochemical derivatives, experience price fluctuations that affect production costs and profitability. These combined factors can deter adoption in cost-sensitive regions, reduce margins, and create uncertainty for growers and suppliers, slowing overall market growth despite the rising demand for efficient crop management solutions.

Opportunity - Rising Adoption of Bio-Based and Eco-Friendly Regulators in Sustainable Agriculture

The growing shift toward sustainable and organic farming has created significant opportunities for bio-based crop growth regulators. Natural auxins, cytokinins, and other eco-friendly formulations align with the global expansion of organic agriculture, as highlighted by FAO reports.

Trials show bio-regulators enhance crop resilience under heat and environmental stress, improving both yield and quality. Companies such as BASF have launched innovative cytokinin products in 2024, supporting this trend. With favorable government policies promoting low-risk substances, this segment demonstrates a higher CAGR than traditional synthetic regulators, making it a key growth driver in the sustainable farming landscape.

Precision Application of Regulators in High-Value Crops Driving Market Expansion

High-value fruits, vegetables, and specialty crops present significant growth potential for crop growth regulators, as they improve fruit quality, uniformity, and shelf-life. Market data shows orchard demand for apples and citrus increased 23% YoY in 2025, highlighting strong adoption.

In countries like India, crops such as sugarcane and cotton demonstrate robust uptake, supported by government initiatives aimed at doubling farmer incomes through resilient and efficient practices. Targeting these high-value crop segments allows manufacturers to capitalize on rapid adoption, premium pricing, and technology-driven precision application, making this a strategic opportunity for market expansion.

Category-wise Analysis

Product Type Insights

Auxins lead the market with 31% share in 2025, valued at USD 681 million in 2024. Their versatile applications in root growth, fruit development, and weed control make them dominant across cereals like rice and horticultural crops. Auxins enhance pollination, reduce fruit drop, and improve overall crop performance, making them a staple in integrated crop management programs.

Emerging bio-based cytokinins and gibberellins are gaining traction due to increasing demand for sustainable agriculture solutions. These categories are being adopted for stress resilience, improved flowering, and fruit size enhancement. Farmers are increasingly exploring these alternatives in high-value and export-oriented crops, reflecting a shift toward innovative, environmentally friendly growth regulators.

Function Insights

Promoters dominate with 65% market share in 2025, driven by their ability to enhance yield, stress tolerance, and crop productivity. Auxins, gibberellins, and cytokinins act as cell division and flowering promoters, supporting high-yield cereals, fruits, and vegetables. Their widespread adoption, present in over 65% of applications, demonstrates their critical role in maximizing crop efficiency and performance across major farming systems.

Stress mitigation and ripening regulators are the fastest-growing function categories. These are increasingly used to protect crops from drought, heat, and salinity, and to achieve uniform fruit ripening. High-value fruits and vegetables are driving experimentation with these regulators to improve marketable quality, shelf-life, and resilience, particularly under changing climatic conditions.

Formulation Insights

Liquid formulations hold the leading share in 2025, preferred for ease of foliar application and rapid absorption. Patented liquid concentrates of gibberellins and auxins reduce phytotoxicity while improving stability, making them ideal for modern, high-efficiency farms. Their compatibility with precision agriculture systems further enhances their appeal among commercial growers.

Emerging encapsulated and controlled-release formulations are the fastest-growing segment. These offer targeted delivery, reduced chemical wastage, and sustained effects, making them increasingly popular in high-value crops and stress-prone environments. Precision dosing and long-lasting activity make these formulations attractive for sustainable and resource-efficient farming practices.

Crop Type Insights

Fruits & Vegetables dominate the market in 2025, driven by demand for uniform ripening, improved quality, and enhanced shelf-life. High-value crops like mangoes, grapes, and tomatoes benefit from regulator use, boosting fruit size, color, and storage potential, aligning with export standards and consumer expectations.

Cereals and plantation crops are the fastest-growing category, with regulators used to enhance grain filling, stress tolerance, and flowering uniformity. Adoption is rising in rice, wheat, sugarcane, and coffee plantations, particularly in regions adopting precision agriculture techniques, reflecting a focus on increasing productivity and resilience in staple and commercial crops.

Regional Insights

North America Crop Growth Regulators Market Trends and Insights

North America holds a 32% market share in 2025, led by the U.S., where advanced agricultural technology, efficient infrastructure, and EPA regulations under FIFRA promote safe and effective regulator use. Auxins dominate at 41% share, particularly in soy and corn, enhancing yields and stress tolerance amid drought-prone areas.

Innovation hubs across the region focus on developing resilient and precision-targeted products. The combination of strong R&D infrastructure, technology adoption, and regulatory compliance supports optimized crop performance. North American farmers increasingly integrate regulators with precision agriculture systems, reflecting a strategic focus on yield maximization, sustainability, and efficiency in modern farming practices.

Europe Crop Growth Regulators Market Trends and Insights

Europe demonstrates a growing focus on sustainable crop production, with the EU harmonizing regulations under Regulation (EU) 2024/3115, easing approvals for low-risk regulators. Germany, the U.K., France, and Spain emphasize sustainable use, especially in fruit and horticulture crops.

Organic and bio-regulator trends are increasingly adopted, while precision application techniques enhance productivity. The European market is expected to grow at a CAGR of 6.2%, driven by regulatory support, innovation in bio-based products, and rising demand for high-quality fruits and vegetables aligned with export and consumer standards.

Asia Pacific Crop Growth Regulators Market Trends and Insights

Asia Pacific leads the global market with a 35% share in 2025, driven by extensive arable land, rising population pressures, and high demand in countries like China and India. Government programs in India, including income-doubling initiatives for farmers, are supporting sugarcane and other high-value crops. Modernized farming practices and large-scale production in China further strengthen adoption.

The region is also the fastest-growing globally, with a projected CAGR of 12% between 2025 and 2032. Rapid uptake of precision agriculture, cost-effective production, and a focus on improving yield and crop quality are accelerating the adoption of crop growth regulators across cereals, fruits, and plantation crops throughout Asia Pacific.

Competitive Landscape

The crop growth regulators market is highly consolidated, dominated by a few major players leveraging strong research and development capabilities, strategic partnerships, and global distribution networks. Companies focus on product innovation, sustainable solutions, and enhancing efficacy to maintain a competitive advantage. Market leaders invest heavily in developing advanced formulations that cater to diverse crops and farming practices.

Emerging competitors are adopting precision delivery models and bio-based innovations to differentiate themselves. These strategies include controlled-release formulations, targeted foliar applications, and environmentally friendly solutions. Overall, competition is driven by technological advancement, sustainability, and the ability to meet growing demand for high-quality, efficient crop management solutions.

Key Developments:

- In July 2024, BASF introduced an advanced cytokinin-based crop growth regulator designed to improve plant resilience under heat stress conditions. The product enhances flowering, fruit set, and overall crop performance, supporting sustainable agriculture amid rising temperature challenges globally.

- In Early 2025, Corteva Agriscience formed strategic partnerships in Asia to develop specialized hormone blends for rice and wheat. These tailored regulators aim to boost yield, improve stress tolerance, and enhance grain quality, addressing regional food security and supporting precision farming practices.

- In 2024, the U.S. EPA approved glufosinate-P, enabling its integration with crop growth regulators. This facilitates combined applications with herbicides, improving efficiency and yield outcomes while ensuring compliance with environmental and safety regulations in major agricultural operations.

Companies Covered in Crop Growth Regulators Market

- BASF SE

- Syngenta AG

- Bayer CropScience

- Corteva Agriscience

- FMC Corporation

- UPL Limited

- Nufarm Limited

- Sumitomo Chemical Co., Ltd.

- Valent BioSciences Corporation

- Adama Agricultural Solutions Ltd.

- Arysta LifeScience

- Tata Chemicals Ltd.

- Nippon Soda Co., Ltd.

- Sichuan Guoguang Agrochemical Co., Ltd.

- Sipcam OXON Spa

Frequently Asked Questions

The global Crop Growth Regulators market is expected to reach US$ 4.9 billion in 2026.

Rising global food demand from a projected population of 9.7 billion by 2050 drives adoption of yield-enhancing regulators.

Asia Pacific leads with 35% share in 2025, driven by population pressures and extensive arable land.

Bio-based and eco-friendly regulators are high-potential, especially in sustainable, high-value crops.

Leading players include BASF SE, Syngenta, Valent BioSciences, and Corteva Agriscience.