- Oil & Gas

- Christmas Tree Valves Market

Christmas Tree Valves Market Size, Share, and Growth Forecast, 2026 – 2033

Christmas Tree Valves Market by Product Type (Ball Valve, Gate Valve, Globe Valve, Butterfly Valve, Check Valve), Application (Residential Use, Commercial Use, Industrial Use, Agricultural Use, Government and Municipal Use), and Regional Analysis for 2026 – 2033

Christmas Tree Valves Market Size and Trends Analysis

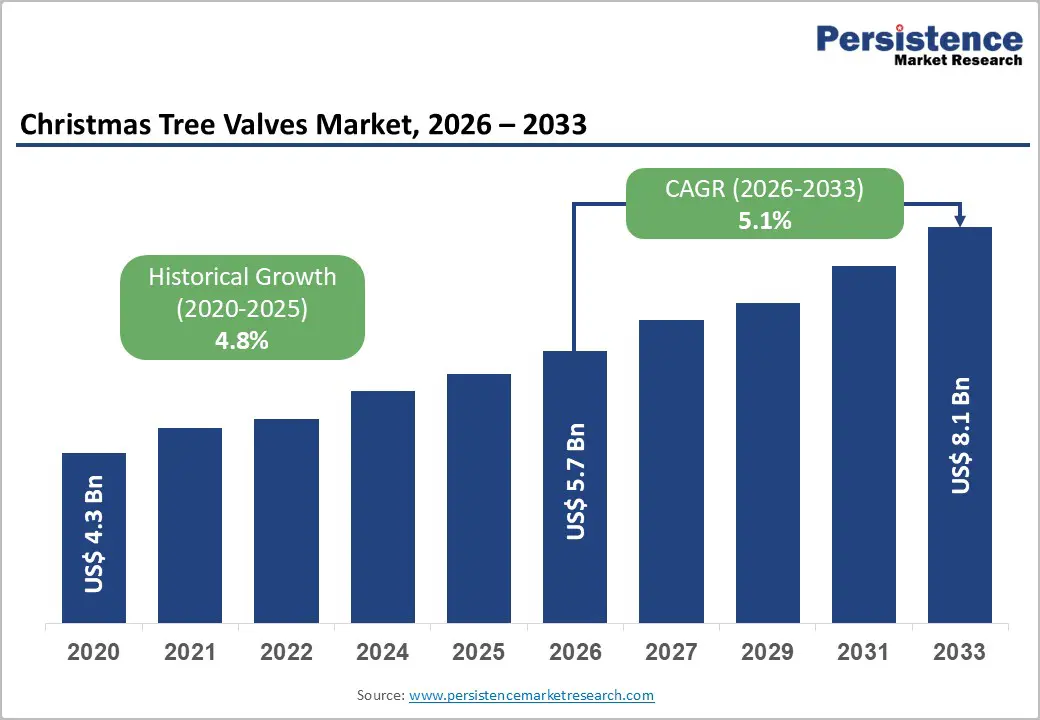

The global Christmas tree valves market size is likely to be valued at US$5.7 billion in 2026 and is expected to reach US$8.1 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2026 to 2033, driven by sustained investments in upstream oil and gas infrastructure.

Rising energy demand, increased exploration and production (E&P) activities, and continued development of onshore and offshore oilfields, particularly in deepwater and unconventional reserves. Advancements in wellhead automation, digital monitoring, and high-pressure valve technologies have enhanced the adoption of advanced Christmas tree valve systems, improving operational safety and production efficiency. Stringent regulatory frameworks focused on well integrity, emission control, and operational safety are accelerating the replacement of legacy equipment with modern, compliant valve solutions. Industry initiatives aimed at reducing downtime and improving asset reliability are also contributing to market expansion.

Key Industry Highlights:

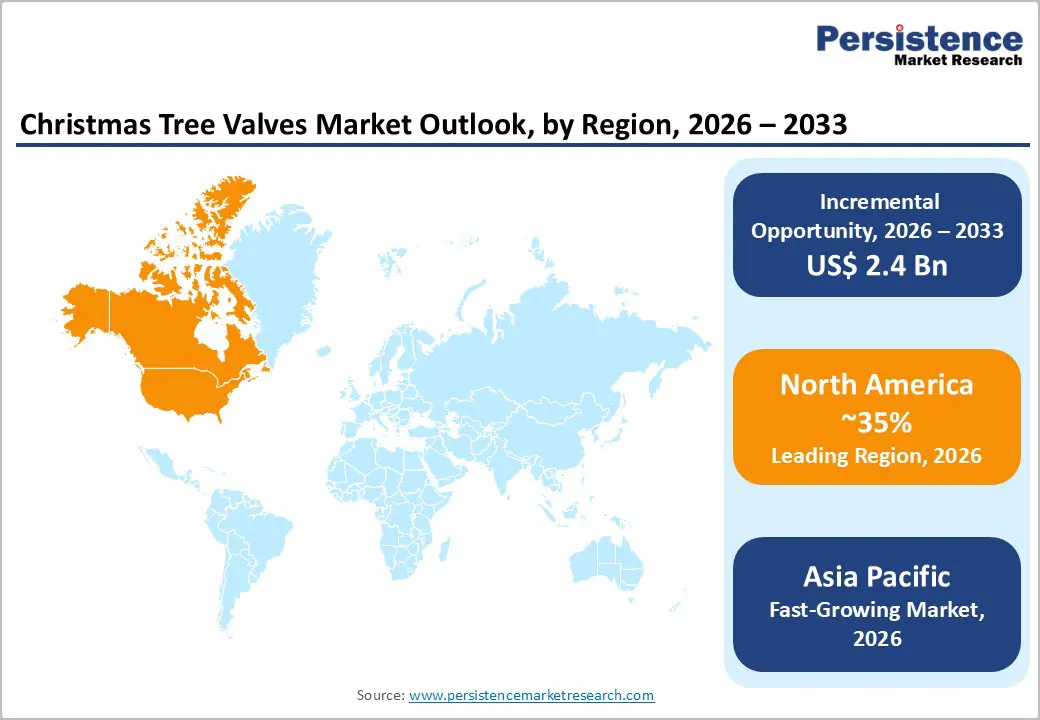

- Leading Region: North America is expected to be the leading region, accounting for a 35% market share in 2026, driven by strong upstream oil and gas activity, advanced shale development, and stringent regulatory standards that support the adoption of modern wellhead equipment.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the Christmas tree valves in 2026, supported by expanding oil and gas activities, strong manufacturing capabilities, and rising infrastructure and industrial development across major regional economies.

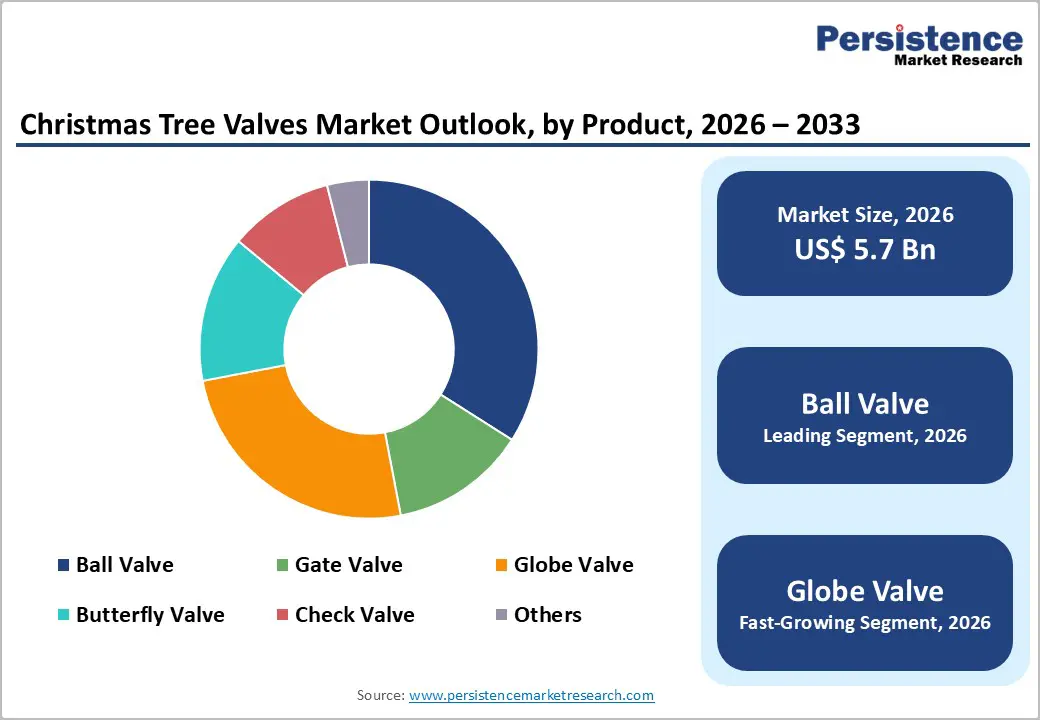

- Leading Product Type: Ball valves are projected to be the leading product type in 2026, accounting for 28% of revenue, driven by superior sealing and suitability for high-pressure and subsea applications.

- Leading Application: The industrial use segment is expected to be the largest application segment, accounting for over 35% of revenue in 2026, driven by extensive deployment across oil and gas operations, petrochemical processing, and heavy industrial infrastructure that requires reliable wellhead flow control and safety systems.

| Key Insights | Details |

|---|---|

| Christmas Tree Valves Market Size (2026E) | US$5.7 Bn |

| Market Value Forecast (2033F) | US$8.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Valve Design and Materials

Modern valve designs incorporate enhanced sealing mechanisms, compact geometries, and low-torque actuation systems, enabling faster response times and precise flow control under extreme pressure and temperature conditions. Innovations such as metal-to-metal sealing, trunnion-mounted ball valves, and advanced gate and globe valve configurations significantly reduce leakage risks and improve well integrity. These improvements are especially critical in high-pressure, high-temperature (HPHT) wells and deepwater offshore environments, where equipment failure can lead to costly downtime and safety hazards. The integration of digital sensors and smart actuators into Christmas tree valves enables real-time monitoring, predictive maintenance, and remote operation, aligning with the industry’s shift toward automated and digitally enabled oilfields. This technological evolution enhances asset life cycles while reducing maintenance frequency and operational risks.

Material innovation strengthens this driver by enabling valves to withstand increasingly harsh operating environments. Advanced alloys, corrosion-resistant coatings, and composite materials are now widely adopted to improve resistance against sour gas, high salinity, erosion, and extreme thermal cycling. Materials such as duplex and super-duplex stainless steel, Inconel, and specialized elastomers enhance durability and ensure compliance with stringent safety and environmental standards. These material advancements support extended service life and lower total cost of ownership, which are critical decision factors for operators managing mature and complex oilfields. Improved material performance supports the growing deployment of Christmas tree valves in offshore, subsea, and unconventional reserves, where operational conditions are more demanding.

Regulatory Hurdles and Certification Delays

Regulatory bodies and industry organizations require extensive testing, validation, and compliance with international standards before valves can be deployed in upstream operations. These processes are time-consuming and often vary by region, creating complexity for manufacturers operating across multiple geographies. Compliance requirements related to pressure ratings, material integrity, fire safety, and environmental protection increase development timelines and delay product commercialization. For operators, prolonged approval cycles can delay drilling and completion schedules, particularly in offshore and deepwater projects where regulatory scrutiny is heightened. Project timelines may be extended, increasing capital expenditure and reducing flexibility in equipment procurement.

Certification delays compound these challenges by impacting supply chains and investment planning within the Christmas tree valves market. Testing and qualification processes for new valve designs or materials often require approvals from multiple authorities, including national regulators and independent certification agencies. Any modification to the design or material composition typically necessitates re-certification, thereby increasing costs and time burdens. This slows innovation adoption, as manufacturers may hesitate to introduce advanced technologies that require lengthy approval cycles. Evolving environmental and safety regulations can lead to retrofitting requirements for existing installations, creating uncertainty for operators and suppliers alike.

3D Printing for Customization

Oil and gas operators increasingly seek flexible, high-performance solutions tailored to complex well conditions. Additive manufacturing enables the rapid production of customized valve components with intricate geometries that are difficult or costly to achieve through traditional machining. This capability is particularly valuable in offshore, subsea, and high-pressure environments where wells often require non-standard designs to meet specific flow, pressure, and temperature requirements. By enabling component-level design optimization, 3D printing improves internal flow paths, reduces material waste, and enhances structural performance. Manufacturers can significantly shorten prototyping and production cycles, enabling faster response to project-specific demands and reducing lead times for critical wellhead equipment.

Beyond customization, 3D printing offers long-term advantages in cost efficiency, supply chain resilience, and lifecycle management for Christmas tree valves. Additive manufacturing allows localized, on-demand production of spare parts, reducing dependence on long supply chains and minimizing inventory holding costs. This is particularly beneficial for remote oilfields and offshore installations, where replacement components are often difficult to source quickly. Advanced printable materials, including high-strength alloys and corrosion-resistant composites, support the demanding performance requirements of wellhead applications while maintaining compliance with industry standards. 3D printing supports iterative design improvements, enabling manufacturers to refine valve performance based on field feedback without extensive retooling.

Category-wise Analysis

Product Type Insights

Ball valves are expected to lead the Christmas tree valves market, accounting for approximately 28% of revenue in 2026, owing to their robust sealing performance, rapid shutoff capability, and suitability for high-pressure oil and gas environments. These valves are widely preferred in both onshore and offshore wellhead systems due to their ability to minimize leakage risks and maintain operational integrity under extreme conditions. Their compact design and durability also minimized downtime and maintenance needs, making them a preferred option for operators managing complex reservoirs. For example, operators widely deploy ball valves in subsea Christmas tree assemblies for offshore fields, relying on their tight shut-off performance to maintain well control and enhance operational safety throughout the production lifecycle.

Globe valves are likely to represent the fastest-growing segment, supported by increasing demand for precise flow control and throttling capabilities in modern oil and gas operations. These valves are gaining traction as operators prioritize enhanced process control, compatibility with automation systems, and real-time flow regulation across upstream and midstream facilities. Their design supports improved pressure regulation and reduced energy loss, aligning with the industry’s shift toward efficiency optimization. For example, the growing use of globe valves in automated wellhead control systems, where integration with smart actuators enables precise modulation of production flow, supports safer and more efficient field operations.

Application Insights

The industrial use segment is projected to lead the market, accounting for approximately 35% of revenue in 2026, supported by extensive deployment across oil refineries, petrochemical complexes, and upstream oil & gas production facilities. Industrial environments demand high-performance valves capable of withstanding extreme pressures, temperatures, and corrosive fluids, making Christmas tree valves essential for maintaining process safety and operational continuity. These valves play a critical role in well control, production regulation, and emergency shutdown systems, ensuring compliance with strict safety and operational standards. For example, the widespread use of christmas tree valves in the production phase, where precise regulation of hydrocarbon flow is essential for stable and safe industrial processing.

Commercial use is likely to be the fastest-growing application in 2026, driven by expanding commercial infrastructure and increasing adoption of advanced flow control systems. Growth is supported by rising demand for reliable valve solutions in large commercial facilities, including energy distribution hubs, utility management systems, and commercial HVAC installations associated with oil and gas support operations. Commercial users increasingly prioritize energy efficiency, operational reliability, and system automation, which aligns with the advanced capabilities of modern Christmas tree valves. These valves support consistent flow management and system safety in complex commercial environments. For example, growing integration of advanced valve systems in commercial energy management facilities, where reliable flow control is essential for supporting downstream industrial and utility operations.

Regional Insights

North America Christmas Tree Valves Market Trends

North America is expected to be the leading region, accounting for 35% in 2026, driven by strong upstream activity and a strategic shift toward automation and digitalization in oil and gas operations. Industrial operators are increasingly investing in advanced wellhead control systems that integrate real-time monitoring, remote actuation, and predictive diagnostics to enhance safety and minimize unplanned downtime. This trend was especially evident in projects across the Permian Basin and the Gulf of Mexico, where operators aimed to optimize production from both unconventional and deepwater reservoirs. For example, Schlumberger’s digital valve solutions integrated advanced sensors with sophisticated analytics to enhance performance and deliver proactive maintenance alerts, driving adoption across both mature and newly developed well sites.

The market trend toward supply chain resilience and localized manufacturing is gaining traction in North America, driving growth in the Christmas tree valves market. Operators and valve manufacturers are reducing dependence on long supply chains by leveraging regional fabrication facilities and additive manufacturing to cut lead times and improve responsiveness to project needs. This localized strategy helps mitigate the risk of shipment delays, enhances quality control, and supports customization. Investment in training and certification programs is helping accelerate workforce readiness for sophisticated valve technologies, ensuring that the adoption of advanced systems is matched by skilled operators in the field.

Europe Christmas Tree Valves Market Trends

Europe is likely to be a significant market for Christmas tree valves in 2026, driven by sustained investments in North Sea offshore oil and gas developments and the region’s strong focus on upgrading aging upstream infrastructure. Operators in key markets such as Norway, the U.K., and Germany are prioritizing reliability, corrosion resistance, and serviceability when procuring Christmas tree valves, reflecting the region’s complex offshore conditions and regulatory environment. European oil and gas companies are also increasingly integrating digital monitoring and remote actuation capabilities into their valve systems to enhance operational oversight and reduce intervention costs, especially in subsea and deepwater environments.

The European market is experiencing the growing adoption of innovative valve technologies designed to support sustainable operations and regulatory compliance, with manufacturers tailoring solutions specifically for the region's unique needs. For example, Aker Solutions has been active in supplying high-performance subsea control systems and valve assemblies that enhance reliability and enable predictive maintenance for North Sea projects, reflecting the industry shift toward smarter and more durable wellhead configurations. Operators are increasingly valuing digital integration that enables real-time data analytics and remote diagnostics, helping optimize production performance while complying with environmental and safety regulations.

Asia Pacific Christmas Tree Valves Market Trends

The Asia-Pacific region is likely to be the fastest-growing, driven by an expanding upstream rig count, accelerating LNG export infrastructure, and a broader shift toward modernizing wellhead equipment across both offshore and onshore oil and gas assets. As operators expanded into deeper and more technically challenging fields, interest increased in valves that delivered higher performance, greater corrosion resistance, and digital integration for remote monitoring and automation. For example, Cameron, a Schlumberger brand, actively supplied subsea Christmas tree systems tailored for Asia Pacific deepwater projects, integrating advanced sensor and actuation technologies to enable real-time diagnostics.

In the Asia-Pacific market, adoption of digital and smart valve technologies increased as operators sought predictive maintenance capabilities and improved lifecycle performance for critical wellhead components. Operators placed growing value on solutions that reduced unplanned downtime and optimized production, particularly as aging fields in Southeast Asia and Australia required retrofit programs and capacity upgrades. In response, vendors embedded advanced analytics, IoT connectivity, and condition-based monitoring into Christmas tree valve packages that transmitted performance data to central control systems, enabling faster fault detection and more efficient maintenance planning. At the same time, a stronger focus on environmental compliance and safety drove the deployment of valves with enhanced sealing and emissions-reduction features, supporting overall market expansion.

Competitive Landscape

The global christmas tree valves market exhibits a moderately fragmented structure, driven by the coexistence of large multinational oilfield equipment manufacturers and emerging regional specialists competing for share across diverse upstream and midstream applications. Established companies leverage extensive product portfolios, service networks, and strong relationships with major oil and gas operators to secure long-term supply contracts, while smaller players differentiate through niche solutions and localized support services. Market activity is shaped by innovation in automation, digital monitoring, and materials technology that improve valve reliability under extreme pressures and temperatures, and by strategic investments in offshore and deepwater projects that demand specialized wellhead control systems.

With key leaders including Schlumberger Limited, Baker Hughes Company, TechnipFMC plc, and Aker Solutions ASA, the landscape reflects both scale and technological diversity among top competitors. These players compete through differentiated product innovation, integration of advanced digital features, and expanded service offerings that enhance operational efficiency and lifecycle support for Christmas tree valve systems. Strategic partnerships, mergers, and geographic expansion initiatives characterize the competitive landscape as companies seek to broaden their presence in high-growth markets such as North America, Asia-Pacific, and the Middle East.

Key Industry Developments:

- In February 2025, Baker Hughes announced the launch of three new electrification technologies for onshore and offshore operations, aimed at enhancing reliability, efficiency, and reducing emissions. The innovations include the Hummingbird™ all-electric land cementing unit, the industry’s first 100% electric solution for onshore cementing, replacing diesel engines with grid- or battery-powered motors, lowering emissions and maintenance requirements. SureCONTROL™ Plus interval control valves (ICVs) enable remote electrical operation for subsea and dry-tree wells, simplifying installation, reducing rig time, and improving zonal production control through digital telemetry for proactive maintenance.

- In February 2025, Oliver Valvetek announced it would supply high-performance valves for Chevron’s Jack St. Malo field development in the Gulf of Mexico. These valves are designed for integration into subsea Christmas Tree systems and will include a Position Indicator for ROV verification, enabling real-time monitoring of valve operation to enhance safety and precision in deepwater production. The multi-turn design ensures accurate open/close status feedback, critical for safe subsea operations. The Jack St. Malo field, located approximately 280 miles off the coast of Louisiana, represents one of Chevron’s flagship deepwater projects, where maximizing production while maintaining stringent safety and environmental standards is essential.

Companies Covered in Christmas Tree Valves Market

- Schlumberger Ltd. (SLB)

- Baker Hughes Company (BKR)

- Halliburton Company (HAL)

- TechnipFMC plc (FTI)

- National Oilwell Varco, Inc. (NOV)

- Weatherford International plc (WFRD)

- The Weir Group PLC (WEIR)

- Dril‑Quip, Inc.

- Stream‑Flo Industries Ltd.

- Cameron (Schlumberger brand)

- Aker Solutions ASA

- Neway Valve

- Shengji Group

- Worldwide Oilfield Machine (WOM)

- American Completion Tools

Frequently Asked Questions

The global christmas tree valves market is projected to reach US$5.7 billion in 2026.

Growing oil and gas exploration, production activities, and the adoption of advanced automated and digitally integrated wellhead systems.

The christmas tree valves market is expected to grow at a CAGR of 5.1% from 2026 to 2033.

Key market opportunities in the christmas tree valves market lie in digitalization, 3D-printed custom valves, deepwater and subsea developments, and retrofitting aging wellhead infrastructure.

Schlumberger Ltd. (SLB), Baker Hughes Company (BKR), Halliburton Company (HAL), and TechnipFMC plc (FTI) are the leading players.