- Medical Devices

- Chlamydia Infection Diagnostics Market

Chlamydia Infection Diagnostics Market Size, Share, and Growth Forecast, 2026 – 2033

Chlamydia Infection Diagnostics Market by Test Type (Nucleic Acid Amplification Test (NAAT), Serology Test, Direct Fluorescent Antibody Test, Culture Test), Infection (Genital, Rectal, Ocular), and Regional Analysis for 2026 – 2033

Chlamydia Infection Diagnostics Market Size and Trends Analysis

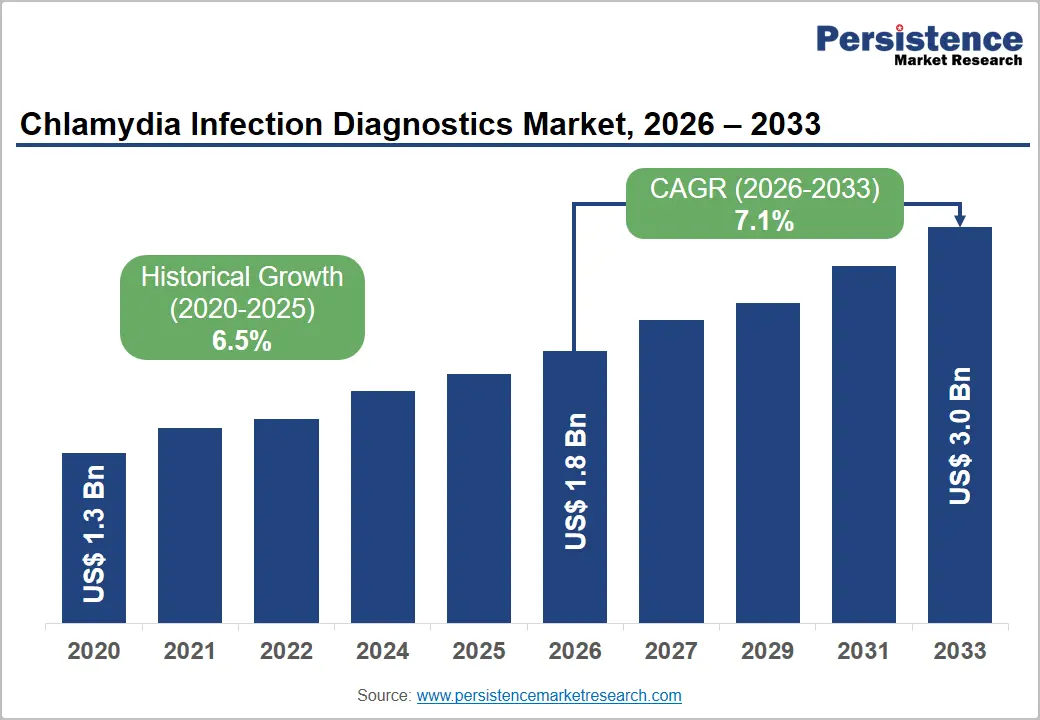

The global chlamydia infection diagnostics market size is likely to be valued at US$1.8 billion in 2026 and is expected to reach US$3.0 billion by 2033, growing at a CAGR of 7.1% during the forecast period from 2026 to 2033, driven by increasing disease surveillance, with WHO reporting millions of new Chlamydia trachomatis infections annually, including an estimated 128 million global cases in 2025, highlighting persistent underdiagnosis due to asymptomatic infections.

According to CDC surveillance data (2023–2024), chlamydia remains the most frequently reported bacterial STI in the United States, with consistently high infection rates among individuals aged 15–24, supporting routine screening guidelines. Growth in the market is strongly influenced by expanding NAAT-based testing adoption recommended by WHO and CDC, improved access to sexual health screening programs, and rising demand for rapid and point-of-care molecular diagnostics.

Key Industry Highlights:

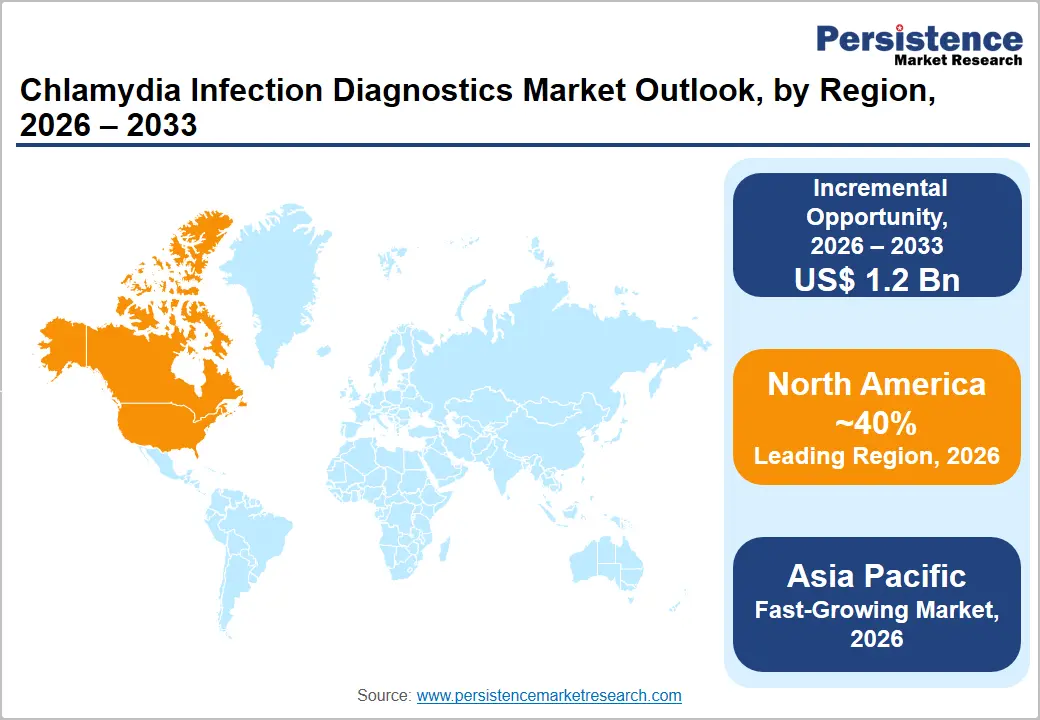

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong screening programs, advanced molecular diagnostic adoption, and well-established healthcare infrastructure.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by the rising STI prevalence, expanding healthcare access, and increasing screening initiatives.

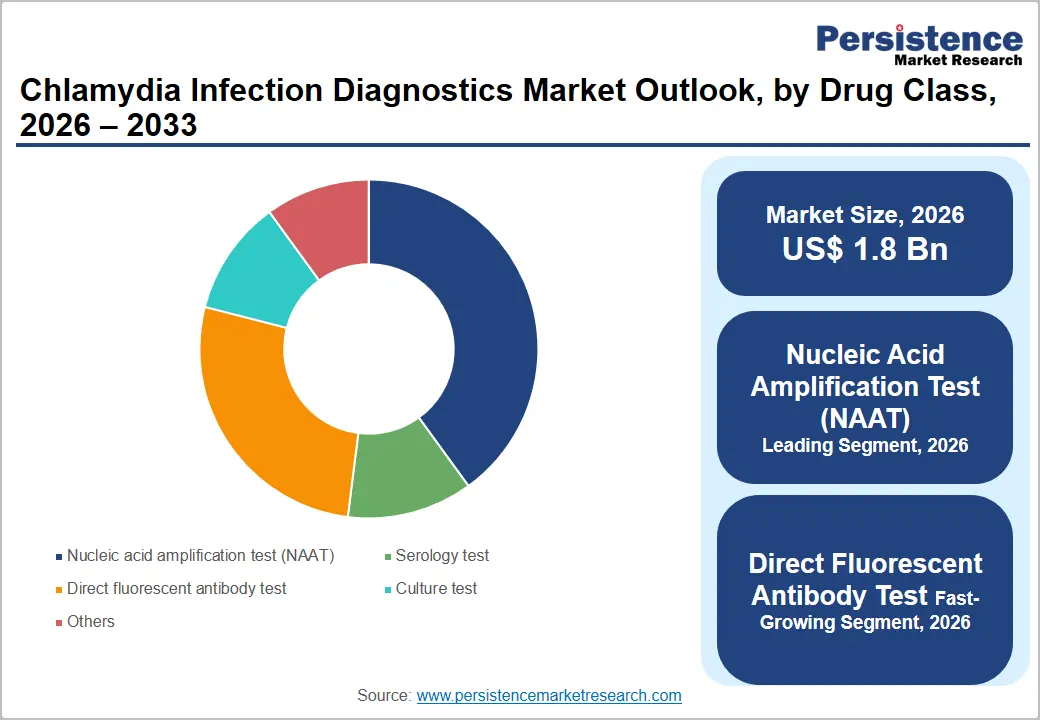

- Leading Test Type: Nucleic acid amplification test (NAAT) is projected to represent the leading test type in 2026, accounting for 60% of the revenue share, for its high sensitivity, specificity, and widespread recommendation as the gold-standard diagnostic method.

- Leading Infection Type: The genital segment is anticipated to be the leading infection type, accounting for over 55% of the revenue share in 2026, supported by the high prevalence of sexually transmitted genital chlamydial infections and extensive routine screening programs.

- Key Opportunity: Expanding adoption of at-home and point-of-care molecular diagnostics, coupled with increasing STI screening initiatives in underserved and emerging markets, is creating significant growth opportunities in the chlamydia infection diagnostics market.

DRO Analysis

Driver - Rising Prevalence and Public Health Screening Initiatives

Chlamydia remains one of the most commonly reported bacterial sexually transmitted infections, creating a substantial demand for reliable diagnostic solutions. A large proportion of infections are asymptomatic, particularly among women, making routine screening essential for preventing long-term complications. Healthcare organizations continue to promote awareness regarding sexually transmitted infections, encouraging individuals to undergo regular testing.

This growing focus on preventive healthcare has increased the utilization of laboratory-based and molecular diagnostic technologies across healthcare settings. Public health screening initiatives strengthen market growth by expanding access to diagnostic services among high-risk populations. Healthcare agencies and non-profit organizations are implementing screening programs targeting sexually active adolescents, young adults, and vulnerable groups.

These initiatives support earlier diagnosis and timely treatment, reducing transmission rates and associated healthcare burdens. Increased funding for sexual health programs and broader integration of STI testing into routine healthcare visits are contributing to higher testing volumes. Advancements in screening protocols and improved healthcare infrastructure in emerging economies are encouraging wider adoption of chlamydia diagnostics.

Restraint - Social Stigma and Low Screening Uptake in Certain Populations

Many individuals hesitate to seek testing due to concerns about privacy, discrimination, embarrassment, or social judgment. This reluctance is particularly evident in conservative societies where discussions related to sexual health remain limited. A significant number of infected individuals remain undiagnosed, contributing to ongoing disease transmission and delayed treatment. Fear of disclosure and misconceptions regarding sexually transmitted infections continue to discourage participation in screening programs, limiting the full potential of diagnostic services despite growing availability and technological improvements.

Low screening uptake among specific population groups also restricts market growth. Individuals living in rural regions, underserved communities, and areas with limited healthcare access often face barriers to testing services. Lack of awareness regarding asymptomatic infections reduces diagnostic adoption rates. In some regions, insufficient sexual health education and inadequate healthcare resources hinder routine screening efforts. Financial constraints and limited availability of specialized diagnostic facilities can additionally impact testing frequency.

Opportunity - Expansion of At-Home and POC Self-Testing

Growing consumer preference for convenient, private, and accessible healthcare solutions is driving demand for self-testing technologies. At-home diagnostic kits allow individuals to collect samples independently, reducing concerns related to stigma and clinic visits. Increasing awareness of sexual health and advances in diagnostic accuracy have improved confidence in self-testing approaches.

Healthcare providers are also recognizing the value of decentralized testing models that support earlier diagnosis and faster treatment decisions. These developments are creating favorable conditions for wider adoption of innovative diagnostic products. Point-of-care testing technologies offer additional growth opportunities by enabling rapid diagnosis in clinical and community healthcare settings.

Faster turnaround times help healthcare professionals initiate treatment promptly, reducing the risk of complications and disease transmission. Technological advancements in molecular diagnostics are improving the sensitivity and reliability of portable testing platforms, making them increasingly suitable for widespread use. Expanding telehealth services complements self-testing solutions by facilitating remote consultation and result interpretation.

Category-wise Analysis

Test Type Insights

Nucleic acid amplification test (NAAT) is expected to lead, accounting for 60% of the revenue share in 2026, due to superior sensitivity, specificity, and the ability to detect infections even when bacterial loads are low. NAAT has become the preferred diagnostic approach across hospitals, diagnostic laboratories, and sexual health clinics because it provides highly accurate results from non-invasive samples such as urine and self-collected swabs. For example, Hologic’s Aptima Chlamydia assay is widely used globally and is recognized for its high diagnostic accuracy in detecting Chlamydia trachomatis infections.

Direct fluorescent antibody (DFA) is likely to represent the fastest-growing segment, supported by increasing interest in rapid diagnostic techniques and expanded screening efforts. The method enables direct visualization of chlamydial antigens in clinical specimens through fluorescent labeling, supporting faster diagnostic assessment compared to some traditional approaches. For instance, DFA assays supplied by Bio-Rad Laboratories have been used in diagnostic laboratories to support the detection of chlamydial infections through fluorescence-based analysis.

Infection Type Insights

Genital infections are projected to lead the market, capturing around 55% of the revenue share in 2026, supported by the high prevalence of sexually transmitted genital chlamydial infections and the widespread implementation of routine screening programs. Most diagnosed chlamydia cases involve the genital tract, making this category the primary source of testing demand across healthcare systems. A notable example is Roche’s cobas CT/NG testing platform, which is extensively used for screening and diagnosing genital chlamydia infections in clinical laboratories worldwide.

Rectal infections are likely to be the fastest-growing infection type due to expanding extragenital screening initiatives and increasing awareness of infection risks among high-risk populations. Healthcare organizations are increasingly recommending comprehensive screening strategies that include rectal testing, particularly for individuals who may not be adequately assessed through conventional genital testing alone. For example, Abbott’s molecular diagnostic platforms support the detection of chlamydial infections from multiple specimen types, including rectal samples used in expanded screening programs.

Regional Insights

North America Chlamydia Infection Diagnostics Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, supported by increasing sexually transmitted infection screening rates, strong public health surveillance programs, and widespread adoption of molecular diagnostic technologies. For example, Hologic Inc. continues to strengthen its molecular diagnostics portfolio through its Aptima platform.

U.S. Chlamydia Infection Diagnostics Market Trends

The U.S. is expected to dominate the regional market, accounting for approximately 80% of the market share in 2026. CDC-supported screening recommendations continue to drive high testing volumes across healthcare facilities. Increased awareness regarding asymptomatic chlamydia infections is encouraging routine screening. Adoption of multiplex STI testing panels is expanding throughout clinical laboratories. Point-of-care molecular testing is gaining popularity due to faster turnaround times. Home-based sample collection programs are receiving greater acceptance among consumers.

Canada Chlamydia Infection Diagnostics Market Trends

Canada is likely to hold approximately 20% of the regional market share in 2026, supported by increasing public health awareness and improved access to sexual health services. Provincial healthcare programs continue to promote routine STI screening. Demand for laboratory-based molecular testing remains strong across major healthcare centers. Expansion of community-based testing services is improving diagnostic accessibility. Self-collection programs are receiving increased attention as convenient screening options.

Europe Chlamydia Infection Diagnostics Market Trends

Europe is likely to be a significant market for chlamydia infection diagnostics, due to strong healthcare systems, growing adoption of advanced molecular diagnostics, and increasing focus on preventive sexual healthcare. Governments and healthcare organizations continue to expand STI awareness programs and screening initiatives aimed at reducing the infection burden. A notable example includes F. Hoffmann-La Roche Ltd, whose cobas molecular diagnostic systems are widely used across European laboratories for chlamydia and other sexually transmitted infection testing applications.

U.K. Chlamydia Infection Diagnostics Market Trends

The U.K. is likely to account for 15% of the Europe market share in 2026, supported by extensive sexual health screening programs and strong public health support. National healthcare initiatives continue promoting early detection of sexually transmitted infections. Adoption of molecular diagnostic technologies is increasing across healthcare facilities. Self-sampling and home-testing services are becoming more widely available. Digital healthcare solutions are improving access to diagnostic pathways.

Germany Chlamydia Infection Diagnostics Market Trends

Germany is anticipated to dominate, accounting for around 37% of the Europe market share in 2026. The country benefits from a highly developed healthcare infrastructure and strong laboratory networks. Molecular diagnostic testing remains widely adopted across hospitals and diagnostic centers. Growing awareness regarding reproductive and sexual health supports screening participation. Healthcare providers continue expanding preventive testing initiatives. Increased use of automated laboratory platforms is improving testing efficiency.

Asia Pacific Chlamydia Infection Diagnostics Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by the rising STI awareness, expanding healthcare infrastructure, and increasing adoption of modern diagnostic technologies. Governments across the region are investing in disease surveillance and reproductive health programs, supporting broader access to testing services. For example, Abbott Laboratories continues expanding access to molecular diagnostic platforms that support sexually transmitted infection testing.

China Chlamydia Infection Diagnostics Market Trends

China is projected to dominate, holding around a 30% share of the regional market in 2026. Expansion of healthcare infrastructure is improving access to advanced diagnostic services. Molecular diagnostics adoption is increasing across hospitals and laboratories. Rising awareness regarding sexually transmitted infections is encouraging earlier diagnosis. Urban healthcare centers are expanding screening capabilities. Investments in laboratory automation are improving testing efficiency.

India Chlamydia Infection Diagnostics Market Trends

India is expected to account for approximately 22% of the regional share in 2026, due to increasing awareness of sexual health and improving healthcare accessibility. Expansion of diagnostic laboratory networks is enhancing testing availability across urban and semi-urban regions. Demand for affordable and accurate molecular diagnostic solutions continues to rise. Government healthcare initiatives are supporting broader disease screening efforts. Increased healthcare spending is improving access to advanced testing technologies. Private diagnostic providers are expanding their service offerings nationwide.

Competitive Landscape

The global chlamydia infection diagnostics market exhibits a moderately fragmented structure, driven by the presence of multinational diagnostic companies, specialized molecular testing providers, and regional laboratory technology developers. Market competition is shaped by continuous advancements in nucleic acid amplification technologies, increasing demand for rapid and point-of-care diagnostics, and expanding screening programs for sexually transmitted infections.

With key leaders, including Abbott Laboratories, Hologic, Inc., F. Hoffmann-La Roche Ltd, BD, Thermo Fisher Scientific Inc., DiaSorin S.p.A., and QuidelOrtho Corporation, the competitive environment remains innovation-focused. These players compete through product portfolio expansion, development of high-performance molecular assays, regulatory approvals, laboratory automation integration, strategic partnerships, and geographic expansion initiatives.

Key Industry Developments:

- In May 2026, Roche Diagnostics announced continued expansion of its molecular diagnostics menu and PCR platform strategy, reinforcing investment in sexually transmitted infection testing capabilities and next-generation molecular diagnostics development.

- In January 2025, F. Hoffmann-La Roche Ltd received U.S. FDA 510(k) clearance and CLIA waiver for its cobas liat STI multiplex assay panels, enabling point-of-care molecular testing for sexually transmitted infections, including chlamydia. The development strengthened Roche’s position in rapid STI diagnostics by supporting faster diagnosis and treatment decisions in decentralized healthcare settings.

Companies Covered in Chlamydia Infection Diagnostics Market

- Abbott

- BD

- Bio-Rad Laboratories, Inc.

- DiaSorin S.p.A.

- F. Hoffmann-La Roche Ltd

- Hologic, Inc.

- QuidelOrtho Corporation.

- Siemens Healthineers

- Thermo Fisher Scientific Inc.

- Trinity Biotech Plc.

Frequently Asked Questions

The global chlamydia infection diagnostics market is projected to reach US$1.8 billion in 2026.

Rising prevalence of chlamydial infections, expanding public health screening programs, and increasing adoption of highly sensitive molecular diagnostic tests drive market growth.

The chlamydia infection diagnostics market is expected to grow at a CAGR of 7.1% from 2026 to 2033.

Expansion of at-home testing kits, point-of-care diagnostics, and increasing access to STI screening in emerging markets present significant market opportunities.

Abbott, BD, Bio-Rad Laboratories, Inc., DiaSorin S.p.A., F. Hoffmann-La Roche Ltd and Hologic, Inc. are the leading players.