- Bulk Chemicals

- C5-C8 Normal Paraffin Market

C5-C8 Normal Paraffin Market Size, Trends, Share, and Growth Forecast 2026 - 2033

C5-C8 Normal Paraffin Market by Product Type (C5-C6, C7-C8, Multicomponent C5-C8), by Application (Solvents, Chemical Intermediates, Fuel Components, Extraction & Purification, Rubber & Elastomer Processing, Others), Grade (Industrial Grade, Technical Grade, Solvent Grade, Reagent/Analytical Grade, Pharmaceutical Grade), Industry, and Regional Analysis, 2026 - 2033

C5-C8 Normal Paraffin Market Size and Trend Analysis

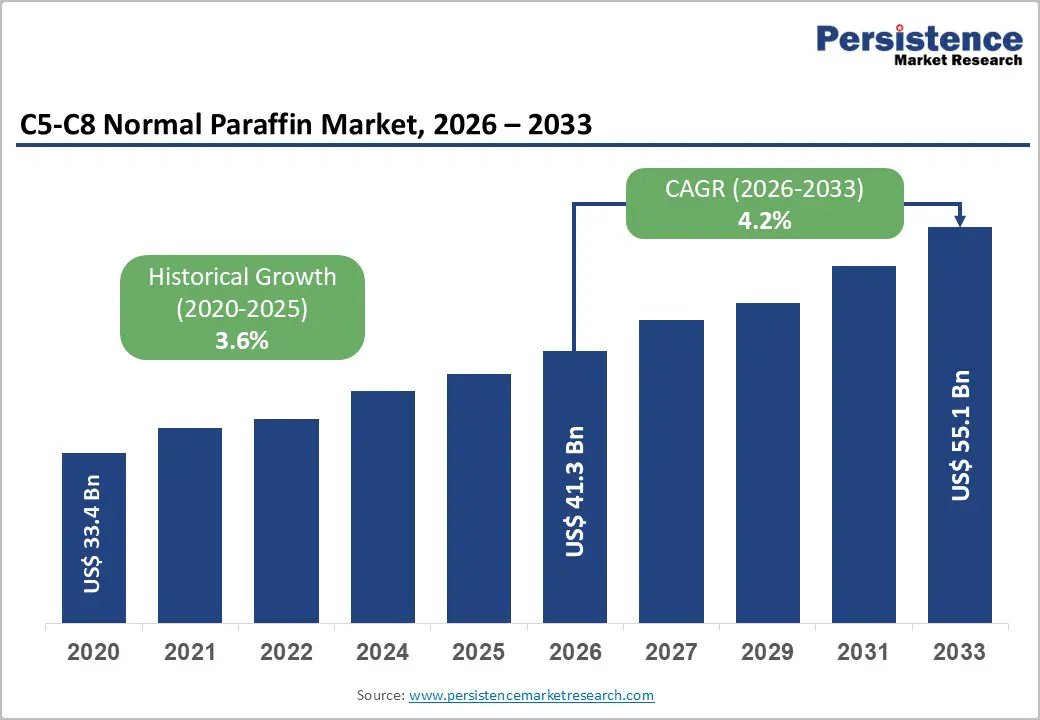

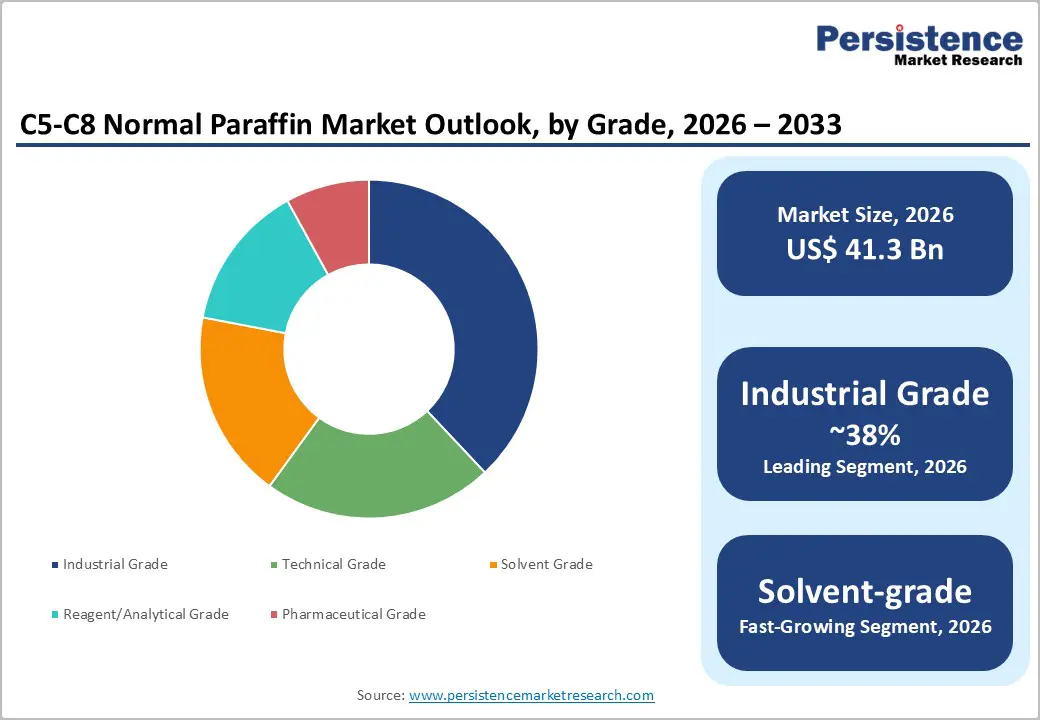

The global C5-C8 normal paraffin market size is likely to be valued at US$ 41.3 billion in 2026 and is expected to reach US$ 55.1 billion by 2033, growing at a CAGR of 4.2% during the forecast period from 2026 to 2033.

Market expansion is driven by rising LAB demand for biodegradable detergents, refinery optimization for gasoline blending, and increasing consumption of lubricants, pharmaceuticals, and specialty solvents in emerging economies.

Key Industry Highlights:

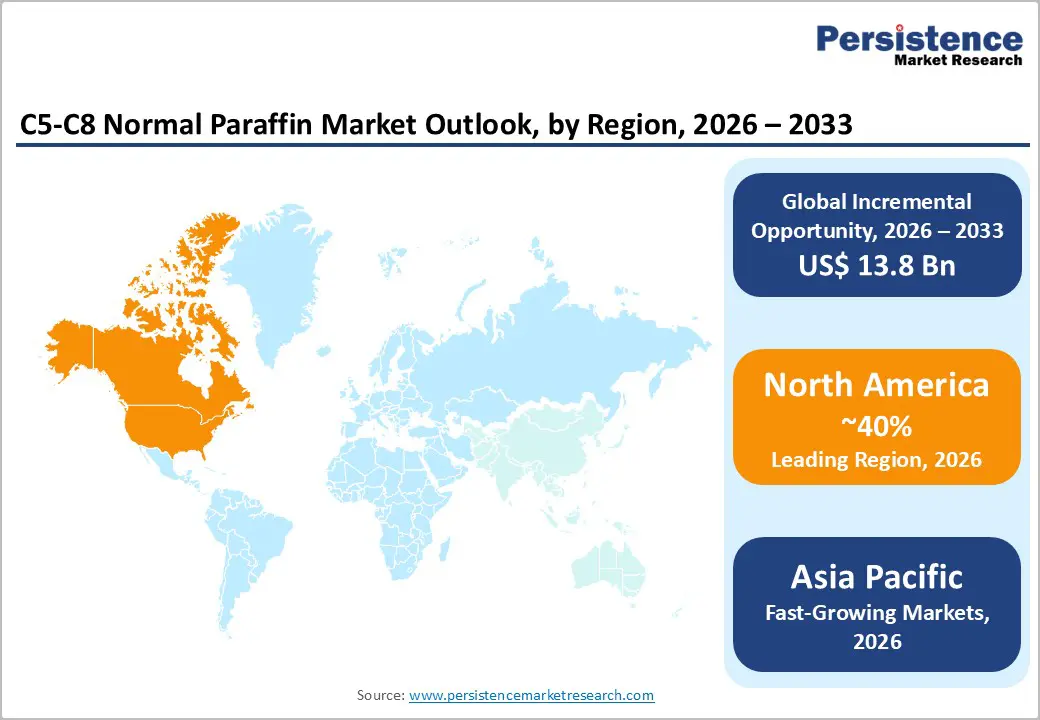

- Leading Segment: North America commands approximately 40% of the global C5-C8 Normal Paraffin market share, valued at US$ 5.8 billion, supported by mature industrial infrastructure, advanced refining capacity, and stringent fuel quality standards driving demand for premium normal paraffin products meeting technical performance specifications.

- Fastest Growing Region: Asia Pacific expands fastest at 7.0% CAGR, driven by China and India's industrial expansion, growing pharmaceutical manufacturing, and rising detergent consumption from urbanization and middle-class population growth, making the region the primary growth driver through 2033.

- Leading Segment: C7-C8 Normal Paraffin segment maintains 43% market leadership through superior performance in automotive lubricants, gasoline blending, and chemical intermediate applications, supported by optimal boiling point and thermal stability.

- Fastest Growing Segment: Industrial Grade Normal Paraffins command 38% market share through cost-effectiveness and widespread detergent and lubricant applications, while Pharmaceutical and Solvent-grade segments grow 5.5-6.5% annually, driven by pharmaceutical expansion and specialty solvent demand across emerging economies.

- Key Opportunities: Chemical Intermediates application, driven by Linear Alkylbenzene (LAB) production for biodegradable detergents, represents 44% market demand and 4.6% CAGR growth, with Asia Pacific detergent markets commanding 42.9% share and supporting sustained feedstock demand through 2033.

| Key Insights | Details |

|---|---|

| C5-C8 Normal Paraffin Market Size (2026E) | US$ 41.3 Billion |

| Market Value Forecast (2033F) | US$ 55.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 4.2% |

| Historical Market Growth (2020 - 2025) | 3.6% |

Market Dynamics

Drivers - Rising LAB production and global shift toward biodegradable detergents are driving sustained demand for C5-C8 normal paraffin feedstocks

Linear alkylbenzene (LAB) production remains the primary growth driver for the C5-C8 normal paraffins market, as these materials serve as essential feedstock for manufacturing linear alkylbenzene sulfonate (LAS), the most widely used surfactant in global detergent formulations. The global LAB market was valued at approximately US$9.3 billion in 2024 and is projected to reach US$14.6 billion by 2034, with a CAGR of 4.6%. The growth is strongly supported by rising consumer preference for biodegradable and environmentally responsible cleaning products. Asia Pacific leads global LAB consumption with nearly 42.9% market share, driven by rapid urbanization in China and India and expanding middle-class populations. Increasing environmental regulations discouraging branched surfactants are accelerating the shift toward LAB-based formulations. As a result, demand for normal paraffin feedstock continues to grow steadily across household, industrial, and personal care detergent applications.

Growing automotive, industrial lubricant, and rubber processing applications are accelerating the consumption of high-performance normal paraffin products

The expanding automotive and industrial lubricants sectors are generating strong demand for C5-C8 normal paraffins, supported by increasingly advanced performance and sustainability requirements. Modern automotive engines, hybrid vehicles, and electric-vehicle thermal management systems require high-quality synthetic and semi-synthetic lubricants, with conventional paraffin-based oils playing a critical role. Industrial lubricant consumption is also increasing due to growing automation, the modernization of manufacturing equipment, and infrastructure development in emerging economies.

Applications such as hydraulic fluids, compressor oils, and gear oils continue to rely on paraffinic base stocks for thermal stability and performance consistency. Companies such as Calumet Specialty Products Partners supply CALPAR paraffinic base oils globally, highlighting strong commercial demand. In addition, rubber and elastomer processing industries utilize C5-C8 normal paraffins as softeners and processing aids, with tire manufacturing and specialty rubber production further supporting sustained market growth.

Restraints - Crude oil price volatility and unstable feedstock costs continue to pressure producer margins and disrupt long-term planning strategies

Volatility in crude oil prices remains a major constraint on the C5-C8 normal paraffin market, as feedstock costs account for nearly 60% of total production costs. Frequent fluctuations in crude oil benchmarks, such as West Texas Intermediate (WTI), create uncertainty in cost planning and directly affect producer margins. Supply disruptions resulting from OPEC+ production decisions, geopolitical tensions, and refinery maintenance schedules further intensify price instability.

Manufacturers often face challenges in passing sudden cost increases to customers, particularly in price-sensitive and contract-based markets. Limited pricing transparency in regions such as Southeast Asia and the Middle East & Africa increases margin pressure, especially for small and mid-sized producers. Companies lacking vertical integration or long-term supply agreements are more vulnerable to these fluctuations, which restrict investment planning, inventory optimization, and long-term capacity expansion strategies across the normal paraffin value chain.

Tightening environmental regulations and increasing adoption of bio-based alternatives are challenging conventional petroleum-derived paraffin demand

Increasing environmental regulations are placing growing pressure on conventional petroleum-derived normal paraffins. Initiatives such as the European Union Green Deal, U.S. EPA clean chemical standards, and global circular-economy policies are encouraging a reduction in dependence on fossil-based raw materials. These regulations are accelerating research and investment into bio-based surfactants, renewable solvents, and alternative process oils. In regions such as North America and Europe, sustainability considerations increasingly influence procurement decisions, creating competitive challenges for traditional paraffin products.

Manufacturers developing bio-based LAB substitutes and renewable lubricant formulations are capturing premium market segments. Although conventional C5-C8 normal paraffins continue to play a critical role in performance-driven industrial applications, rising environmental awareness may limit long-term demand growth in select regions. This regulatory shift is gradually reshaping product portfolios and encouraging producers to balance performance efficiency with compliance with sustainability standards.

Opportunity - Development of renewable and bio-based normal paraffins is creating premium growth opportunities aligned with global sustainability goals

Significant growth opportunities are emerging through the development of bio-based and renewable normal paraffins produced from vegetable oils, animal fats, and biomass residues. Technologies such as hydrogenation and Fischer-Tropsch synthesis enable manufacturers to offer sustainable alternatives aligned with evolving regulatory and consumer expectations. Companies such as Neste Oyj have demonstrated commercial success by expanding production of renewable specialty oils and lubricants. This transition is particularly attractive in Europe, where carbon accounting requirements and sustainability disclosures strongly influence supplier selection.

Bio-based normal paraffins are gaining traction in applications such as eco-friendly cosmetics, pharmaceutical formulations, and biodegradable industrial lubricants. These segments often command price premiums of 15% over conventional products, thereby improving profitability. Manufacturers investing in green chemistry, renewable feedstocks, and low-carbon processing technologies are well-positioned to benefit from long-term market transformation while strengthening brand credibility and regulatory compliance.

Rapid industrialization and expanding pharmaceutical manufacturing in the Asia Pacific are unlocking high-growth specialty application opportunities

Asia Pacific presents substantial growth opportunities for C5-C8 normal paraffin suppliers, supported by rapid industrialization and expanding pharmaceutical and specialty chemical manufacturing. Countries such as China, India, and Vietnam are witnessing strong investment in petrochemical infrastructure and downstream chemical production. India’s pharmaceutical and fine chemical sectors are growing at 10% CAGR, driving rising demand for pharmaceutical-grade and reagent-grade normal paraffins.

China continues to expand its petrochemical capacity at a rate of 5% annually, thereby strengthening consumption of detergents, lubricants, and specialty solvents. Strategic acquisitions, including Savita Oil Technologies’ purchase of Petrogal’s paraffin division in Q3 2024, underscore consolidation and regional expansion. Pharmaceutical ointments, topical treatments, and specialty solvent applications are among the fastest-growing segments, supported by rising healthcare expenditure and growing domestic chemical manufacturing across South and Southeast Asia.

Category-wise Analysis

Product Type

The C7-C8 normal paraffin segment accounts for approximately 43% of the total market share, owing to its balanced volatility, solvency, and thermal performance. This carbon range provides optimal performance across a wide range of industrial applications, particularly in automotive lubricants, where viscosity stability and thermal resistance are critical. Refineries also prioritize C7-C8 fractions for gasoline blending due to favorable boiling points and octane enhancement properties.

Applications of chemical intermediates, including solvent extraction and specialty lubricant formulations, benefit from the segment’s intermediate volatility profile. Its versatility allows manufacturers to serve both high-volume industrial markets and specialty chemical applications. Additionally, C7-C8 products offer cost advantages compared to ultra-high-purity alternatives, making them commercially attractive for large-scale operations. This combination of performance efficiency, application flexibility, and economic viability is expected to sustain segment dominance through 2033.

Grade Insights

Industrial-grade normal paraffins account for approximately 38% of total market consumption, driven by extensive use in detergent manufacturing, lubricant production, and chemical intermediates. With typical purity levels of 98-99%, industrial-grade products deliver adequate performance while maintaining cost efficiency for high-volume applications such as LAB synthesis, rubber processing, and fuel blending. This grade benefits from standardized global specifications and large-scale production efficiencies, making it the preferred choice for commodity manufacturers.

Solvent-grade normal paraffins accounted for more than 950,000 metric tons of global consumption in 2023, reflecting strong demand in extraction solvents, paints, coatings, and specialty chemical applications. While solvent-grade products serve niche and higher-value markets, industrial-grade paraffins are expected to retain market leadership through 2033. Continued expansion of detergent and lubricant manufacturing across developing economies will further reinforce this dominance.

Application Insights

Chemical intermediates remain the largest application segment, accounting for approximately 44% of total C5-C8 normal paraffin demand. This dominance is primarily driven by large-scale LAB production for detergent and surfactant manufacturing. The segment also includes agrochemical formulations and specialty chemical synthesis, creating diversified and stable demand streams. Fuel component applications represent around 26% of total consumption, supported by gasoline blending and refinery optimization requirements aimed at improving fuel performance.

Solvent applications account for nearly 18% of market demand, with use in paints, coatings, pharmaceutical extraction, and industrial cleaning processes. This segment is witnessing comparatively faster growth due to increasing industrial activity and rising pharmaceutical manufacturing in emerging markets. The broad applicability of normal paraffins enhances market stability, while the continued expansion of specialty uses continues to increase overall consumption intensity across industries.

Industry Insights

The chemical and petrochemical sector accounts for approximately 38% of global C5-C8 normal paraffin consumption, driven by detergent intermediates, chemical synthesis, and specialty formulations. The pharmaceutical industry represents the fastest-growing end-use segment, expanding at an estimated 6.5% CAGR. Growth is supported by increasing pharmaceutical production in Asia Pacific and rising demand for pharmaceutical-grade paraffins in ointments, creams, and topical formulations.

Cosmetics and personal care applications are also growing steadily at a 5.8% CAGR, driven by rising disposable incomes and the increasing adoption of premium skincare products. Normal paraffins are widely used as emollients, moisturizers, and formulation stabilizers in cosmetic products. Emerging markets are experiencing rapid lifestyle changes and increasing demand for branded personal care products, thereby further supporting growth. These evolving end-use dynamics are gradually shifting market focus toward higher-value specialty segments.

Regional Insights

North America C5-C8 Normal Paraffin Trends

North America leads the global C5-C8 normal paraffin market, holding nearly 40% share and reaching an estimated value of around US$ 5.8 billion in 2024. The market is projected to grow at a steady CAGR of 3.2% through 2033. This strong position is supported by the region’s well-developed industrial base, advanced refining infrastructure, and mature detergent and lubricant manufacturing industries. According to the U.S. Energy Information Administration, the United States produced approximately 19.9 million barrels of crude oil per day in 2022, ensuring a stable supply of feedstock for normal paraffin production.

The market is highly capital-intensive and technologically advanced, with refiners continuously investing in modern separation and isomerization technologies to improve yield efficiency. Major companies such as Phillips 66 and ExxonMobil are expanding fractionation and hydrocarbon fluid capacities, reinforcing long-term supply strength. Strict environmental and fuel-quality regulations further encourage demand for high-purity normal paraffins, supporting premium pricing and strengthening the market position of integrated producers.

Europe C5-C8 Normal Paraffin Trends

Europe accounts for approximately 30% of global C5-C8 normal paraffin consumption, with the regional market valued at nearly US$ 4.3 billion in 2024 and expected to grow at a CAGR of 3.5% through 2033. The region benefits from a strong chemical manufacturing ecosystem, advanced refining capabilities, and a well-established detergent and specialty chemicals sector. Germany remains the largest producer and consumer, supported by high-end applications in lubricants, pharmaceuticals, and cosmetic formulations. However, Europe’s regulatory landscape plays a defining role in shaping market dynamics.

The European Union Green Deal and related sustainability initiatives are accelerating investments in renewable and bio-based alternatives, exerting gradual pressure on conventional paraffin use. Countries such as the UK, France, and Spain continue to support stable demand through detergent and chemical intermediate production. Increasing focus on circular economy practices has encouraged industry consolidation and innovation. As customers demand transparency in carbon footprint and sustainable sourcing, manufacturers are developing eco-certified and renewable paraffin solutions that command premium pricing despite higher production costs.

Asia Pacific C5-C8 Normal Paraffin Trends

Asia Pacific is the fastest-growing region in the global C5-C8 normal paraffin market, currently holding around 23% market share and projected to expand at a strong CAGR of 7.0% through 2033. Growth is driven by rapid industrialization, expanding manufacturing bases, and rising demand from pharmaceutical and specialty chemical industries. China leads regional production and consumption, accounting for nearly 35% of the Asia Pacific demand, supported by large-scale detergent manufacturing and lubricant applications. India is emerging as a high-growth market, with pharmaceutical and fine chemical sectors expanding at 10% annually, increasing demand for pharmaceutical-grade and reagent-grade paraffins.

Rising urbanization and improving living standards across the region are boosting household and personal care consumption, supporting strong growth in LAB-based detergents. Southeast Asian countries such as Vietnam and Thailand are investing heavily in petrochemical infrastructure, creating new opportunities for suppliers. Japan continues to lead in high-purity and specialty-grade applications, strengthening the region’s technological competitiveness.

Competitive Landscape

The global C5-C8 normal paraffin market exhibits moderate consolidation, with approximately 12-15 major players controlling the majority of global supply. Leading companies including ExxonMobil Corporation, Royal Dutch Shell, Sinopec, Sasol Limited, and BP Plc collectively account for larger share of total market share. These companies benefit from integrated refining operations, proprietary separation technologies, and strong downstream linkages. Players such as Phillips 66, Calumet Specialty Products Partners, and INEOS focus on specialty grades and customer-specific formulations, enabling higher margins.

Competition is intensifying in Asia Pacific, driven by expanding Chinese and Indian producers offering cost advantages and regional proximity. Strategic priorities include vertical integration, technology leadership, and regulatory compliance. Increasing merger and acquisition activity, such as Savita Oil Technologies’ acquisition of Petrogal’s paraffin division, highlights ongoing consolidation aimed at geographic diversification and long-term competitiveness.

Key Developments:

- In September 2024: ExxonMobil Corporation announced an expansion of hydrocarbon fluid production capacity by 250,000 tons annually across its facilities in Antwerp, Singapore, and Texas, strengthening supply for high-performance normal paraffin derivatives and specialty lubricant applications across automotive and industrial end-use sectors.

- In December 2024: Phillips 66 increased its 2026 capital expenditure plan to US$ 2.4 billion, prioritizing NGL fractionation expansion and construction of a new 100,000 barrels-per-day Corpus Christi fractionator by 2028 to enhance light hydrocarbon output and normal paraffin production capacity.

Companies Covered in C5-C8 Normal Paraffin Market

- ExxonMobil Corporation

- BP Plc

- Royal Dutch Shell plc

- China Petroleum & Chemical Corp

- Phillips 66 Company

- Calumet Specialty Products Partners, L.P.

- Indian Oil Corporation Ltd

- Sasol Ltd

- Petrobras

- Rompetrol Rafinare S.A

- Thai Oil Public Company Ltd

- Bharat Petroleum Corporation Limited

- The Linde Group

- Air Liquide S.A.

- Neste Oyj

Frequently Asked Questions

The global C5-C8 normal paraffin market is expected to reach US$ 55.1 billion by 2033, growing at a 4.2% CAGR driven by detergents, lubricants, and specialty chemical demand.

Market growth is driven by rising LAB production for biodegradable detergents, expanding automotive and industrial lubricants, and increasing pharmaceutical and specialty chemical manufacturing in emerging markets.

The C7-C8 normal paraffin segment leads the market with around 43% share, supported by strong demand from lubricants, gasoline blending, and LAB-based chemical intermediates.

North America leads in market share, while Asia Pacific is the fastest-growing region driven by rapid industrialization, pharmaceutical expansion, and rising detergent consumption.

Major opportunities include bio-based and renewable normal paraffin development and expanding pharmaceutical and specialty chemical applications across high-growth Asia Pacific markets.

The market is led by ExxonMobil, Shell, Sinopec, Sasol, and Phillips 66, with growing competition from Indian Oil Corporation and renewable-focused producer Neste Oyj.