- Power Generation, Transmission, & Distribution

- Busbar Trunking Systems Market

Busbar Trunking Systems Market Size, Share, and Growth Forecast, 2025 - 2032

Busbar Trunking Systems Market by Conductor (Copper, Aluminum), Insulation (Air/Compact Air, Air-Insulated Sandwich Type), Application (Data Centers & Telecom Rooms, Industrial Plants, Commercial Buildings & Malls, Residential Complexes, Transportation, Utilities & Power Plants, Others), and Regional Analysis for 2025 - 2032

Busbar Trunking Systems Market Share and Trends Analysis

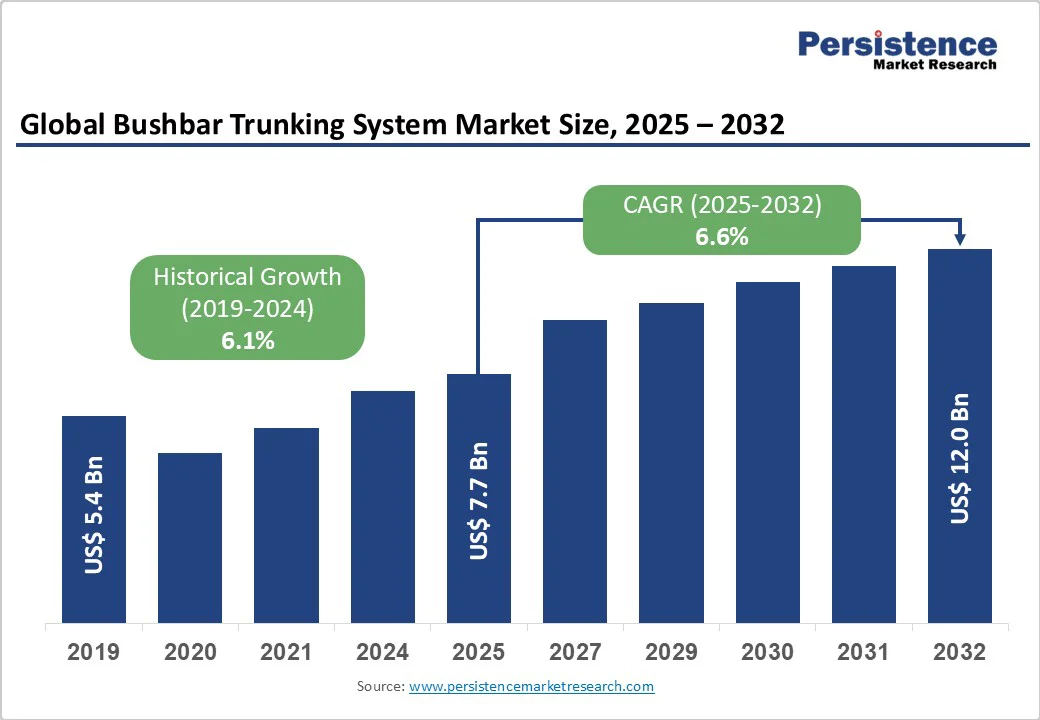

The global busbar trunking systems market size is likely to be valued at US$ 7.7 billion in 2025, and is projected to reach US$ 12.0 billion by 2032, growing at a CAGR of 6.6% during the forecast period 2025 - 2032, driven by infrastructure modernization and implementation of energy efficiency mandates in major world economies.

Digital transformation initiatives across industrial and commercial sectors are catalyzing the adoption of these systems, with data centers alone consuming 4.4% of total U.S. electricity in 2023, projected to reach around 10% by 2028. Renewable energy integration requirements are fundamentally reshaping power distribution architecture, as global renewable capacity additions exceeded 150 GW in China alone during 2024.

Key Industry Highlights

- Leading Conductor: Copper conductor systems are expected to lead with an estimated 65% market revenue share in 2025 due to their superior conductivity and reliability.

- Dominant Insulation: Air-insulated busbar systems are set to dominate in 2025, while sandwich-type insulated systems are the fastest-growing with a projected 35% share by 2025.

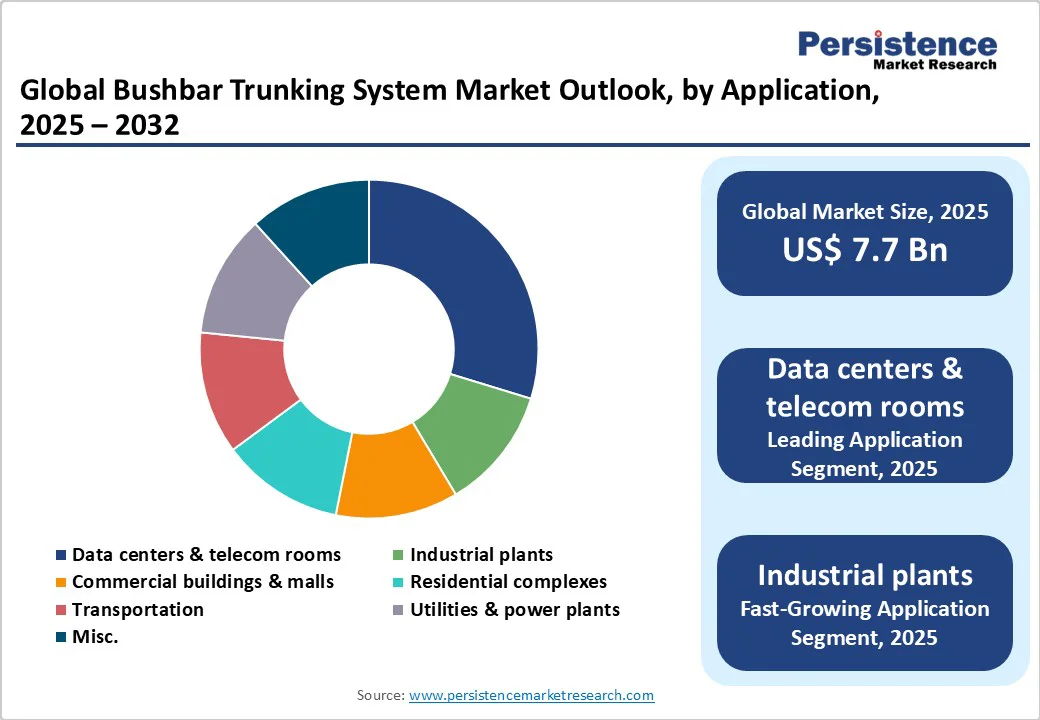

- Largest Application: Industrial plants are likely to remain the largest application segment, holding around 40% of the busbar trunking systems market revenue share in 2025, driven by manufacturing automation and Industry 4.0 expansion.

- Fastest-growing Application: Data centers & telecom rooms are the fastest-growing application, expected to capture approximately 25% share by 2025, reflecting hyperscale digital infrastructure deployment in Asia Pacific.

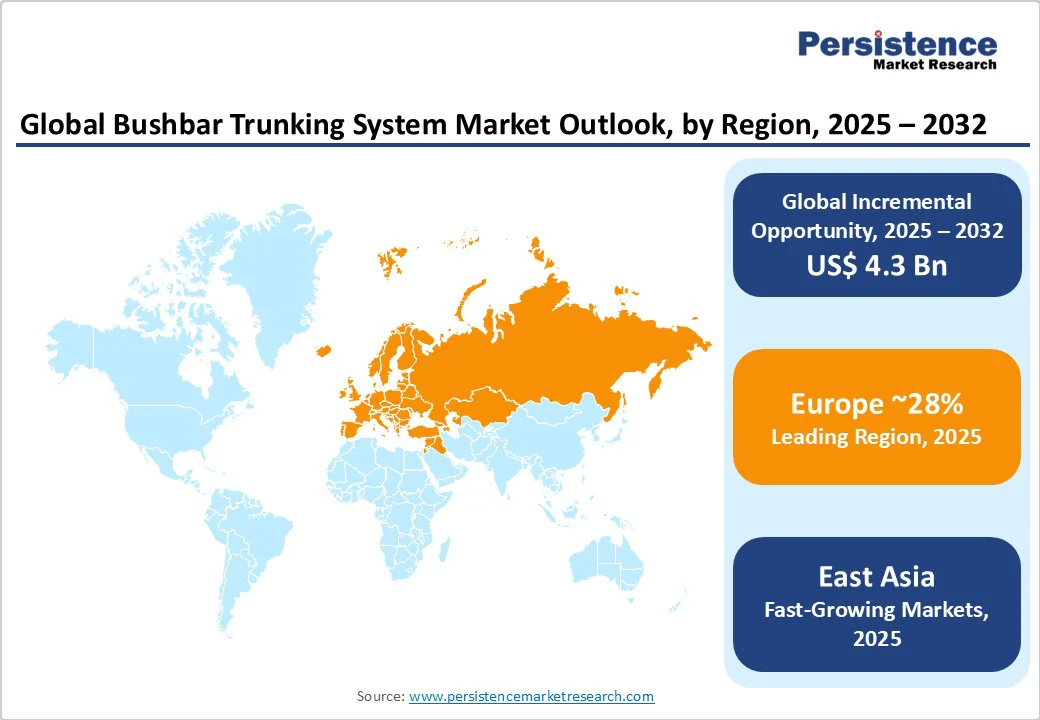

- Leading Region: Asia Pacific is slated to lead with around 38% share in 2025, with East Asia contributing the highest portion, supported by industrial modernization and proliferation of data centers.

- Second-largest Regional Market: North America follows with roughly 26% share in 2025, driven by smart grid modernization, renewable energy integration, and urban infrastructure upgrades.

- Major Growth Factor: Government smart city initiatives in India are creating significant adoption momentum, with busbar systems specified in over 60% of new municipal projects, indicating strong institutional demand.

- Prominent Trend: Renewable energy and grid modernization are generating specialized applications globally, expected to account for 15-20% of new busbar deployments by 2025.

| Key Insights | Details |

|---|---|

| Busbar Trunking Systems Market Size (2025E) | US$ 7.7 Bn |

| Market Value Forecast (2032F) | US$ 12.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Industrial Infrastructure Modernization and Automation

Industrial sector transformation is the primary market catalyst, with manufacturing facilities requiring scalable electrical distribution systems to support Industry 4.0 initiatives. China established over 15,000 new manufacturing plants in 2023, each requiring integrated electrical infrastructure that directly boosts demand for low- and medium-voltage busbar systems.

India's manufacturing FDI exceeded US$ 25 billion in 2023, resulting in the establishment of new production units requiring efficient power distribution solutions. The automotive sector modernization is also expanding specialized applications, creating substantial demand for high-performance busbar configurations.

Hyperscale data center proliferation is fundamentally reshaping electrical distribution requirements. Cloud computing infrastructure buildout requires compact, high-capacity power distribution frameworks that can support dense electrical loads while optimizing space utilization.

Singapore, Japan, and South Korea are witnessing unprecedented hyperscale facility deployment, with data center operators prioritizing modular electrical systems for rapid scalability. Similarly, edge computing deployment is creating new market segments, with telecommunications infrastructure requiring specialized busbar configurations for 5G network equipment and distributed computing nodes.

Another emerging area is the rapid adoption of renewables worldwide. Global renewable energy capacity additions are necessitating advanced electrical distribution infrastructure, with India's solar installations surging 35% in 2024, according to the Ministry of New and Renewable Energy.

High-voltage direct current (HVDC) transmission projects require specialized busbar configurations for efficient long-distance power transmission. Smart grid modernization initiatives across developed economies are driving infrastructure upgrades. Grid stability requirements for variable renewable generation are increasing demand for flexible power distribution systems, enabling real-time load balancing and fault management capabilities.

High Initial Capital Investment and Installation Complexities

Procurement and installation costs represent significant adoption barriers, particularly for small and medium enterprises with limited capital expenditure budgets. Integration of complexity with legacy electrical infrastructure can lead to extended project timelines and increased costs, requiring specialized expertise for seamless deployment.

Retrofitting ageing electrical systems presents technical challenges that may discourage adoption in favor of conventional wiring solutions, especially in regions with limited technical expertise. Furthermore, project financing constraints in emerging markets can delay large-scale infrastructure modernization, where busbar systems provide optimal solutions.

Standardization and compatibility issues across different manufacturer specifications can complicate procurement decisions and increase the total cost of ownership.

Government-led Smart City Initiatives to Open Unprecedented Opportunities

India’s Smart Cities Mission, targeting 100 urban centers for modernization, has become a key catalyst for upgrading electrical and infrastructural systems. By 2024, over 60% of new municipal infrastructure tenders specified busbar-based distribution systems, demonstrating strong institutional momentum for adoption.

Rapid urban population growth and dense infrastructure demands are driving the preference for space-efficient electrical solutions that can support future expansion. Public-private partnership (PPP) frameworks are also facilitating the large-scale deployment of busbar systems across metro stations, airports, and municipal facilities.

The integration of these systems with building management and IoT platforms is enabling predictive maintenance and energy optimization, resulting in new value-added service opportunities for electrical system providers.

Simultaneously, India’s renewable energy expansion and grid modernization efforts are opening high-growth opportunities for advanced busbar applications. Solar, wind, and energy storage installations are increasingly incorporating specialized busbar configurations to enhance power delivery efficiency.

Policy incentives and government support for clean energy transitions are accelerating this adoption trend, ensuring consistency with India’s broader decarbonization goals. Moreover, as distributed energy resources expand, there is growing demand for busbar systems equipped to manage bi-directional power flows and dynamic load balancing.

Category-wise Analysis

Conductor Type Insights

Copper will continue to dominate the conductor market with a commanding 65% share in 2025, largely due to its unmatched electrical conductivity and superior thermal management properties, both crucial for high-current and mission-critical applications. Industrial facilities and data centers consistently choose copper conductors for their reliability in environments where power interruptions can lead to major operational or financial losses.

Its high performance in dense power networks makes it indispensable for hyperscale data centers, advanced manufacturing plants, and industrial automation systems that demand uninterrupted power delivery and consistent current performance.

Meanwhile, aluminum is emerging as the fastest-growing conductor segment through 2032, driven by its lower cost and lightweight advantages, as it is nearly 60% lighter than copper. This makes it a preferred material in commercial and residential projects where reduced load simplifies installation and minimizes structural reinforcement needs.

Aluminum busbar trunking systems are also gaining traction in large-scale infrastructure projects that prioritize total cost efficiency over maximum conductivity. Their ability to deliver acceptable electrical performance at a lower material cost positions them as an attractive alternative in commercial and industrial spaces with moderate power density requirements.

Insulation Type Insights

Insulated sandwich-type busbars maintain their lead in 2025 with a dominant 60% market share, supported by superior fire resistance, operator safety, and installation efficiency. These systems are widely adopted in high-load environments such as utilities, production facilities, and data centers, where they enhance operational security and reliability.

The multi-layer insulation structure delivers exceptional thermal regulation and electromagnetic shielding, making it ideal for environments that experience variable electrical loads or demand extended uptime under heavy power distribution conditions.

Air and compact air insulation types are registering the fastest growth through 2032, offering compelling advantages for moderate current and humid environment applications. Their enhanced moisture resistance makes them suitable for vertical risers, outdoor installations, and other projects exposed to challenging environmental conditions.

These systems are particularly valued for their affordability and flexibility, making them ideal for installations where ease of maintenance, accessibility, and layout adaptability take priority over extreme energy density or compact system design.

Application Insights

Data centers and telecom rooms are set to lead the market in 2025, capturing about 30% of total share, as global cloud computing and hyperscale infrastructure continue to expand rapidly. The surge in artificial intelligence and machine learning workloads is amplifying the need for high-capacity electrical systems capable of supporting GPU clusters and high-performance computing operations.

The rollout of 5G network infrastructure is further intensifying the demand for efficient power distribution that supports extensive telecom hardware and edge computing networks. This trend is reinforced by enterprise digital transformation initiatives driving continuous data center construction and modernization.

Industrial plants represent the fastest-growing application segment, fueled by the manufacturing sector’s transformation under Industry 4.0. Automation and robotics adoption require agile, modular power distribution systems that can handle fluctuating loads and production shifts.

The rapid rise of electric vehicle manufacturing has also created specialized demand for busbar systems in battery production plants and charging networks. Similarly, expanding activity in chemical and pharmaceutical industries is elevating the need for reliable, regulation-compliant power infrastructure that guarantees operational safety, precision, and energy efficiency within highly controlled process environments.

Regional Insights

Asia Pacific Busbar Trunking Systems Market Trends

Asia Pacific is anticipated to hold the largest portion of the busbar trunking systems market share in 2025 at around 28%, driven primarily by China’s industrial expansion and aggressive infrastructure modernization efforts. In 2024 alone, China added over 150 GW of renewable energy capacity, significantly boosting demand for advanced electrical distribution systems capable of managing power connectivity across large-scale solar and wind farms.

This growth is reinforced by the government’s continued focus on industrial electrification under the Made in China 2025 strategy, which emphasizes automation and intelligent manufacturing. More than 80% of new commercial buildings in Tier-1 cities now incorporate plug-in busbar systems, highlighting the country’s shift toward scalable and space-efficient electrical frameworks in urban development.

Japan’s leadership in hybrid and electric vehicle (EV) production further contributes to regional demand, creating a specialized market for high-performance busbar solutions in automotive manufacturing. Meanwhile, South Korea’s commitment to building a digital economy, under initiatives such as the Digital New Deal, continues to fuel demand for advanced electrical distribution within data centers, transportation hubs, and smart grid networks.

Across the Asia Pacific, expanding industrial bases, smart city programs, and renewable energy integration are collectively creating sustained growth momentum, positioning the region as both the largest and fastest-growing market for busbar trunking systems worldwide.

North America Busbar Trunking Systems Market Trends

North America is expected to account for roughly 24% of the global market in 2025, supported by rising investments in grid modernization and the acceleration of data center development projects. The United States leads regional demand, with data center electricity consumption projected to reach between 6.7% and 12% of national power use by 2028.

This surge is fueling the adoption of high-efficiency electrical distribution systems designed for scalability, reduced power losses, and improved thermal control in data-intensive environments. The Biden Administration’s infrastructure investment programs are reinforcing this trend by channeling funds into renewable energy integration, grid upgrades, and resilient power systems for commercial and industrial facilities.

Canada’s growing industrial capacity also underpins regional expansion, particularly within manufacturing, energy extraction, and processing sectors that require dependable, high-capacity power networks.

Federal and provincial incentives supporting energy efficiency and sustainability goals are accelerating the shift toward modern busbar technologies that ensure operational reliability while reducing carbon footprints. As North America continues electrifying its industrial and urban infrastructure, the region remains a key market for advanced, code-compliant, and eco-friendly busbar trunking systems.

Competitive Landscape

The competitive environment of the global busbar trunking systems market features a balanced mix of consolidation and fragmentation, with characteristics trending toward an oligopolistic structure in developed economies.

Multinational corporations dominate technologically advanced and high-value product segments, while regional and local firms cater to cost-sensitive and specialized applications across emerging markets. Global leaders such as Siemens, Schneider Electric, Legrand, EAE Electric, and C&S Electric hold strong positions due to their extensive product portfolios, continuous innovation, and global distribution networks.

Domestic players, including Godrej Enterprises Group and Lauritz Knudsen Electrical & Automation, also maintain solid regional standings through localization strategies and competitive pricing.

The market’s multifaceted nature encourages continuous product innovation, strategic alliances, and the introduction of tailored solutions for diverse industrial, commercial, and renewable applications. These dynamics are shaping a competitive yet collaborative landscape, where technological advancement, sustainability integration, and digitalization define long-term differentiation among suppliers.

Key Industry Developments

- In May 2025, Schneider Electric launched Canalis for EV, a modular busbar trunking system specifically designed for electric vehicle (EV) charging infrastructure. The plug-and-play, prefabricated system enables quick installation, reduced civil work, and scalability to meet evolving EV charging demands. Supporting over 20 charger types, the solution provides a flexible, future-proof, and maintenance-free power distribution system for outdoor EV charging applications.

- In July 2024, Siemens officially launched its BD2 Busbar Trunking System in Ho Chi Minh City, marking a major step toward smarter and more efficient power distribution. Designed for use in commercial buildings, data centers, and industrial facilities, the BD2 system offers enhanced flexibility, faster installation, and easier configuration for changing electrical loads. Its modular design and compact structure simplify maintenance while improving safety and energy efficiency. This launch underscores Siemens’ ongoing commitment to advancing digitalized electrification solutions that support sustainable infrastructure development in Vietnam and beyond.

Companies Covered in Busbar Trunking Systems Market

- C & S Electric

- EAE Electric

- Lauritz Knudsen Electrical & Automation

- Godrej Enterprises Group

- Siemens

- Schneider Electric

- DTM Elektroteknik

- WEG Electric Corp.

- Legrand

- Naxso Srl

- Blutronic W.L.L.

- Anord Mardix Inc.

- JRC Powertech

- KDH Engineering Ltd.

- NORELCO

- DBTS Africa

- Eaton

- Jiangsu Wetown Busway Co., Ltd.

- Shanghai ZHENDA

Frequently Asked Questions

The global busbar trunking systems market is projected to reach US$ 7.7 billion in 2025.

Industrial infrastructure modernization, automation, data center expansion, and renewable energy integration are driving strong demand for efficient and scalable busbar trunking systems.

The market is poised to witness a CAGR of 6.6% from 2025 to 2032.

Opportunities lie in government-led smart city initiatives, urban infrastructure expansion, renewable energy projects, grid modernization, and integration with IoT-enabled building management systems.

Key market players include C & S Electric, EAE Electric, Lauritz Knudsen Electrical & Automation, Godrej Enterprises Group, Siemens, and Schneider Electric.