- Plastics, Polymers & Resins

- BOPA Film Market

BOPA Film Market Size, Share, and Growth Forecast, 2026 - 2033

BOPA Film Market by Product Type (Nylon 6, Nylon 66, Others), Application (Food Packaging, Pharmaceutical Packaging, Industrial Packaging, Electronics), End-user (Food & Beverages, Healthcare, Electronics), and Regional Analysis for 2026-2033

BOPA Film Market Share and Trends Analysis

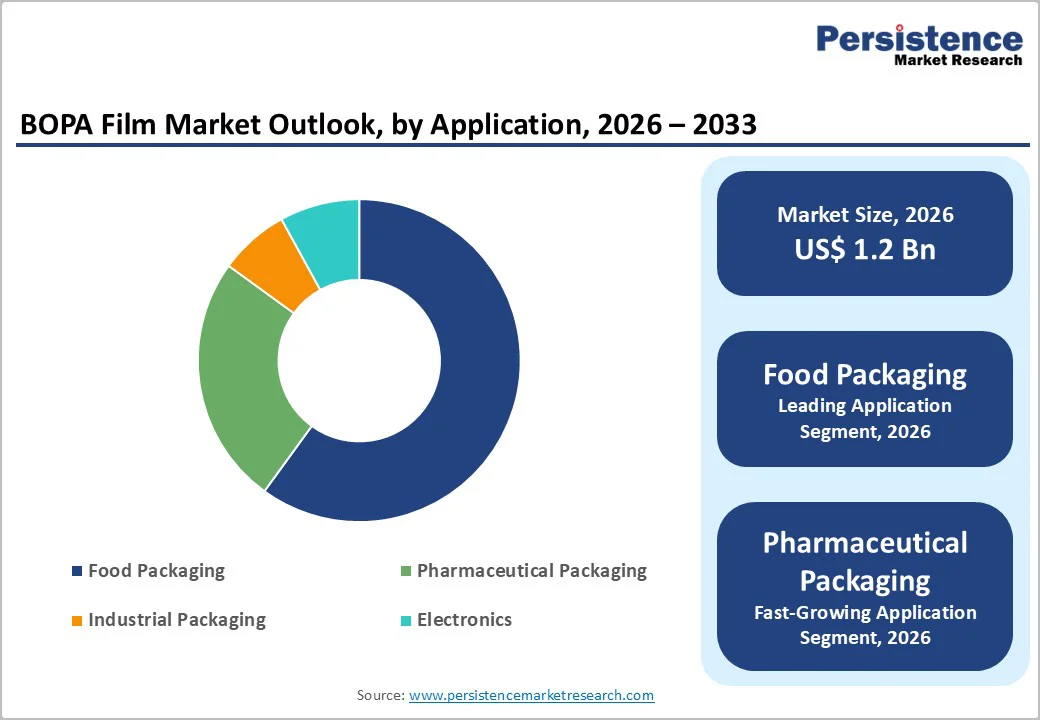

The global BOPA film market size is likely to be valued at US$ 1.23 billion in 2026, and is projected to reach US$ 1.80 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026−2033. This growth reflects the expanding use of high barrier flexible packaging in food, pharmaceutical, and electronics supply chains, alongside rising hygiene and shelf life requirements in both developed and emerging markets. Demand is further supported by regulatory focus on food safety, ongoing substitution of rigid packaging formats, and investments in advanced multilayer film lines in Asia Pacific and North America.

Key Industry Highlights

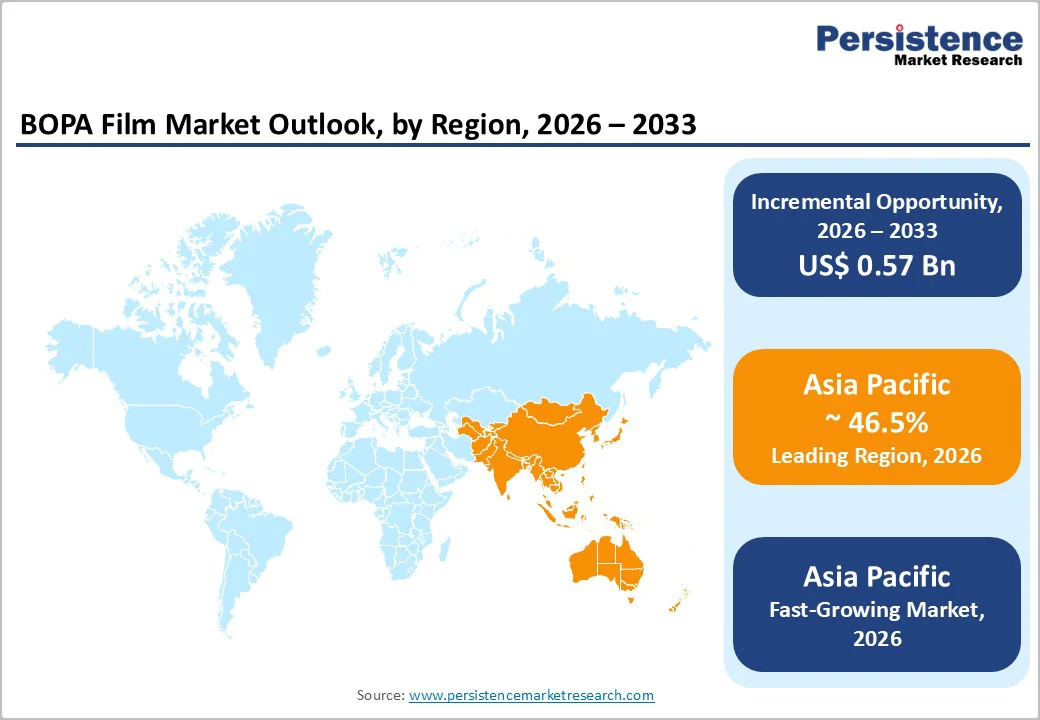

- Dominant Region: Asia Pacific is expected to command about 46.5% market share in 2026, supported by the largest demand base for advanced packaging solutions.

- Fastest-growing Regional Market: Asia Pacific is likely to be the fastest-growing market through 2033, as the region boasts some of the largest production facilities for high barrier flexible packaging.

- Leading & Fastest-growing Product Types: Nylon 6 is set to lead with an approximate 65% revenue share in 2026, while nylon 66 is likely to be the fastest growing segment from 2026 to 2033.

- Leading & Fastest-growing Applications: Food packaging is slated to be dominate with about 60% market share in 2026, whereas pharmaceutical packaging is expected to be the fastest-growing during the 2026-2033 forecast period.

- Key Driver: Rising demand for high barrier food packaging, driven by the mounting need to extend shelf life, cut food waste, and protect quality, is playing a central role in augmenting market growth.

- Key Opportunity: Developing sustainable and eco friendly packaging solutions by using recyclable, bio based, lightweight, and lower carbon materials while still meeting performance and safety requirements can generate high-value opportunities for market players.

| Report Attribute | Details |

|---|---|

|

BOPA Film Market Size (2026E) |

US$ 1.23 Bn |

|

Market Value Forecast (2033F) |

US$ 1.80 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Climbing Demand for High Barrier Food Packaging

Brand owners and retailers are increasingly turning to biaxially oriented polyamide (BOPA) films to protect products throughout extended and multifaceted supply chains while maintaining freshness, safety, and visual appeal. BOPA films deliver exceptional oxygen and moisture barrier properties alongside outstanding puncture resistance and thermal stability, positioning them as the preferred choice for pouches and laminated structures across meat, dairy, snack, frozen food, and ready meal applications. By preserving aromatic compounds, preventing spoilage, and extending product shelf life in both temperature-controlled and room-temperature distribution networks, BOPA-based packaging solutions contribute to measurable reductions in food waste while ensuring consistent quality standards.

The expansion of packaged and convenience food consumption in emerging economies, coupled with the transition from unbranded bulk formats to branded packaged offerings and the proliferation of modern retail channels and digital commerce, is generating sustained demand for enhanced packaging reliability. Simultaneously, stringent regulatory requirements such as European Union (EU) food-contact regulations and national food safety standards across North America and Asia mandate robust, verifiable, and multilayer packaging construction. These converging market and regulatory pressures validate the strategic adoption of high-integrity laminate structures in which BOPA films furnish the requisite mechanical strength and barrier performance to meet evolving industry requirements.

Volatility in Raw Material Prices and Alternative Packaging Material

Price instability in raw materials, especially nylon resins sourced from petrochemical feedstock, represents a major challenge for the BOPA films market growth. Since nylon resin prices are closely linked to crude oil markets, fluctuations caused by geopolitical tensions, supply interruptions, or changes in global demand can lead to sharp cost increases. These swings compress profit margins for manufacturers and introduce uncertainty into both pricing strategies and long-term supply agreements, making cost management and planning more complex.

Competitive pressures are also mounting from alternative packaging solutions, including biodegradable films and advanced polymers. Biodegradable films are gaining popularity because they break down naturally, minimizing environmental impact, reducing landfill waste, lowering microplastic pollution, and decreasing carbon emissions. Advanced polymers, particularly those offering high performance and biodegradability, are increasingly used in packaging due to their enhanced strength, durability, and sustainability. These emerging options are challenging the traditional dominance of BOPA films and prompting industry players to reassess their material choices in response to growing environmental and regulatory demands.

Advent of Sustainable and Eco-Friendly Packaging Solutions

Sustainable and environmentally responsible packaging solutions represent a compelling opportunity within the BOPA films market, as regulatory bodies, brand owners, and consumers demand packaging that delivers robust barrier performance alongside reduced environmental footprint. BOPA films inherently enable sustainability through down-gauging and weight reduction, as well as shelf-life extension capabilities, which collectively lower material usage, minimize food waste, and decrease transportation-related emissions throughout product lifecycles.

Stricter global and regional policies governing plastic waste, recyclability requirements, and carbon reporting mechanisms, including EU packaging directives and national extended producer responsibility (EPR) schemes, are driving accelerated demand for high-barrier films that demonstrate superior life-cycle performance and alignment with recycling standards. This regulatory landscape directly benefits innovation-driven BOPA producers positioned to meet these requirements. Simultaneously, brand owners across food, pharmaceutical, and personal care sectors are actively seeking high-barrier, recyclable, and lower-carbon flexible packaging solutions and are committed to partnering with suppliers on sustainably designed laminate structures. This collaborative approach creates pathways for BOPA films to enter premium sustainable product portfolios and secure positions within environmental, social, & governance (ESG)-aligned procurement initiatives.

Category-wise Analysis

Product Type Insights

Nylon 6 is expected to occupy the commanding position, holding approximately 65% of the BOPA film market revenue share in 2026, as it delivers the optimal value proposition for converters and brand owners through strong performance, versatile application suitability, and cost-effectiveness. Nylon 6 BOPA provides superior oxygen and aroma barrier capabilities alongside good puncture resistance and optical clarity, which directly address the requirements of mainstream food packaging formats such as vacuum packs, pouches, and retort applications. This integrated performance profile enables manufacturers to achieve necessary shelf-life extension and product protection without requiring expensive specialty materials or unnecessarily complex laminate structures.

Nylon 66 is positioned as the fastest-growing segment throughout the 2026-2033 forecast period. Its elevated melting point, exceptional tensile strength, and superior dimensional stability under thermal stress make it the preferred choice for demanding industrial and electronic packaging applications where films encounter high temperatures, mechanical strain, or rigorous processing conditions. These distinctive properties establish nylon 66 BOPA as the natural solution for industrial and electronic packaging environments, where operational reliability and safety performance are essential requirements that cannot be compromised.

Application Insights

Food packaging is set to remain the dominant application for BOPA films, securing an estimated 60% market revenue share in 2026. In this sector, brand owners and retailers need solutions that protect product quality and safety over extended storage and distribution periods, without compromising convenience or presentation. BOPA films address this requirement by providing strong barrier protection against oxygen, moisture, and other external factors that can reduce freshness, flavor, and texture, which is critical for formats such as vacuum-packed goods, stand-up pouches, and ready-to-eat meals. As consumer lifestyles shift toward higher consumption of convenience foods, demand is rising for reliable, high-performance flexible packaging, and this trend is expected to support sustained growth in BOPA usage within mainstream food applications.

Pharmaceutical packaging is poised to be the fastest-growing application over the 2026-2033 forecast period, as healthcare stakeholders seek materials that consistently safeguard drug integrity and patient safety. The sector values packaging structures that maintain efficacy by limiting exposure to oxygen and moisture, while also resisting punctures, tearing, and handling damage throughout complex distribution channels. BOPA films meet these needs through their robust barrier performance and mechanical strength, which makes them well suited for blister formats, sachets, and high-integrity medical pouches where shelf-life stability and contamination control are critical. For packaging converters and pharmaceutical companies, shifting more portfolios into BOPA-based laminates can support risk mitigation, regulatory compliance, and brand trust, particularly in high-value or sensitive product categories.

End-User Insights

Food and beverages are anticipated to represent the leading end-user segment, commanding approximately 60% market share in 2026, with growth primarily driven by the need for packaging that reliably safeguards product safety and extends shelf life. BOPA films deliver strong barrier properties that shield perishable goods from oxygen, moisture, and contamination, thereby preserving freshness and sensory characteristics throughout distribution and storage cycles. As consumer preferences increasingly favor ready-to-eat and convenience food options, the industry relies more heavily on high-performance flexible packaging solutions, positioning food and beverages as a primary growth driver for BOPA film adoption.

Healthcare is projected to be the fastest-growing end-user segment between 2026 and 2033. The sector demands robust and effective packaging solutions for medical devices and pharmaceuticals, where BOPA films provide essential protection against moisture and gaseous exposure. This protective capability is fundamental to maintaining pharmaceutical product integrity, ensuring therapeutic efficacy, and guaranteeing patient safety throughout product lifecycles. With heightened global focus on healthcare infrastructure and expanding worldwide pharmaceutical production, demand for BOPA films within this segment is expected to accelerate significantly, making healthcare a critical opportunity for converters and material suppliers targeting growth trajectories.

Regional Insights

Asia Pacific BOPA Film Market Trends

Asia Pacific is slated to command a dominant 46.5% of the BOPA film market share in 2026, driven by its unique status as both the largest demand base and the most concentrated production hub for high-barrier flexible packaging. Key markets such as China, India, and the ASEAN serve as the engines for this dominance, hosting integrated nylon value chains, large-scale film extrusion capacities, and extensive converter networks that collectively lower production costs while enhancing supply chain reliability. This structural advantage allows regional manufacturers to effectively serve diverse customer bases across food, pharmaceutical, and industrial sectors with speed and cost-efficiency that other regions struggle to match.

Massive scale and high velocity of urbanization, an expanding middle class, and rising disposable incomes across Asia Pacific are fueling robust consumption growth in packaged foods, pharmaceuticals, personal care products, and consumer electronics. China and India specifically are experiencing accelerated adoption of processed and convenience foods, supported by the proliferation of modern retail channels and e-commerce platforms that mandate high-performance flexible packaging to guarantee shelf life and product safety. Beyond consumer goods, the region’s formidable manufacturing infrastructure for electronics and automotive components generates substantial secondary demand for technical and industrial BOPA films, further cementing Asia Pacific’s long-term leadership in the global market.

Europe BOPA Film Market Trends

Europe represents a strategically valuable and stable market for biaxially oriented polyamide films, anchored by rigorous packaging regulations and advanced environmental standards. EU regulators and policymakers prioritize food safety, product traceability, recyclability, and environmental impact reduction, which drives strong preference for high-performance, well-documented materials such as BOPA films in applications where barrier integrity and packaging reliability are non-negotiable. This regulatory framework sustains consistent demand across food, pharmaceutical, and specialty industrial sectors, as brand owners and converters must meet stringent requirements for shelf-life performance, product protection, and packaging waste management throughout their supply chains.

Europe leads the sustainability transformation in flexible packaging, directly influencing how BOPA films are manufactured and specified for use. Under the EU Circular Economy Action Plan (CEAP) and the evolving Packaging and Packaging Waste Regulation (PPWR), significant regulatory pressure exists to reduce packaging weight, enhance recyclability, and minimize climate impact. European film producers and manufacturers are responding by developing recyclable laminate structures that incorporate thinner BOPA layers or integrate nylon into mono-material or advanced recycling pathways, while simultaneously exploring bio-based and low-carbon BOPA grades that align with brand owners' ESG commitments and carbon-reduction objectives. This strategic alignment positions European suppliers to capture premium market opportunities with sustainability-focused customers.

North America BOPA Film Market Trends

North America functions as a vital and consistently expanding market for BOPA films, merging robust demand from premium end-use sectors with sophisticated advancements in packaging innovation and sustainability practices. The United States and Canada maintain expansive food and beverage industries alongside healthcare operations that depend on high-barrier flexible packaging to secure product safety, extend shelf life, and fulfill stringent regulatory mandates. These dynamics directly promote BOPA films in formats such as vacuum packs, retort pouches, and pharmaceutical structures, where reliability underpins brand confidence and compliance success.

North American producers actively invest in cutting-edge orientation equipment, multilayer designs, and coating systems to boost barrier effectiveness, support material thinning, and streamline manufacturing processes while customizing outputs for local brand and retailer needs. The region also prioritizes automation, digital tools, and Industry 4.0 integration to elevate production precision and quality oversight, establishing BOPA films as a reliable staple in regulated domains such as healthcare and upscale food packaging. Converters targeting this market can leverage these investments to differentiate offerings, align with sustainability goals, and capture steady growth amid evolving consumer and policy expectations.

Competitive Landscape

The global BOPA films market structure exhibits moderate consolidation, with dominant players including Toray Industries, Inc., Mitsubishi Chemical Corporation, Honeywell International Inc., and Green Seal Holding Ltd. collectively commanding 35-40% market share. The competitive environment is characterized by relentless innovation and deliberate strategic actions from these and emerging competitors. Leading firms prioritize product quality, technical performance, and sustainability credentials to address the varied requirements of food, pharmaceutical, industrial, and electronics end-users. Continuous technological advancement and material investments position these players to sustain market relevance and competitive advantage while maintaining pricing power in their respective segments.

Market dynamics are constantly evolving as key competitors expand global operations and enhance product portfolios to capture incremental share and support long-term profitability. Companies investing in advanced manufacturing capabilities, sustainability-aligned offerings, and customized solutions for regional or application-specific needs create differentiation opportunities in a market where end-users increasingly demand performance, reliability, and environmental responsibility. For converters, material suppliers, and brand owners, this competitive environment presents pathways to engage with innovation-focused partners who can deliver tailored solutions, support supply chain resilience, and align with evolving regulatory and consumer expectations across geographies and sectors.

Key Industry Developments

- In November 2025, Toppan and its India-based subsidiary Toppan Specialty Films installed a hybrid manufacturing line in India that can produce both biaxially oriented polypropylene (BOPP) and biaxially oriented polyethylene (BOPE) films on the same machine, increasing efficiency and production capacity for flexible packaging films.

- In July 2025, Chemical firm SRF Ltd invested nearly INR 750 crore to set up an agrochemical intermediate plant at Dahej in Gujarat and a BOPP film manufacturing facility in Indore as part of its expansion strategy.

- In March 2025, JPFL Films, a subsidiary of Jindal Poly Films, became the first Indian manufacturer to produce BOPA nylon films, investing in a new Nasik facility to support Make in India, reduce import dependence, and enhance flexible packaging capabilities.

Companies Covered in BOPA Film Market

- Toray Industries, Inc.

- Mitsubishi Chemical Corporation

- Unitika Ltd.

- TOYOBO Co., Ltd.

- Honeywell International Inc.

- DOMO Chemicals

- Green Seal Holding Ltd.

- Cangzhou Mingzhu Plastic Co., Ltd.

- A.J. Plast Public Company Limited

- Triton International Enterprises

- Impak Films

- NOW Plastics Inc.

- Biaxis Oy Ltd.

- Kunshan Yuncheng Plastic Industry Co.

Frequently Asked Questions

The global BOPA film market is projected to reach US$ 1.23 billion in 2026.

Growing demand for high‑barrier, lightweight flexible packaging in food, pharmaceutical, and industrial applications, widespread popularity of convenience foods, and stricter safety standards are driving the market.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Introduction of sustainable and recyclable BOPA solutions, bio‑based and eco‑designed films, and expanding use of advanced packaging solutions in high‑value sectors such as healthcare and electronics are key market opportunities.

Toray Industries, Inc., Mitsubishi Chemical Corporation, Honeywell International Inc. and Green Seal Holding are some of the key players in the market.