- Animal Feed & Additives

- Bird Food Market

Bird Food Market Size, Share, and Growth Forecast, 2026 – 2033

Bird Food Market by Product Type (Seeds, Feed, Treats, Carpets, Suet, Others), Sales Channel (Economical, Mass, Premium), End-User (Veterinary Specialty, Households, Animal Shelter), and Regional Analysis for 2026-2033

Bird Food Market Share and Trends Analysis

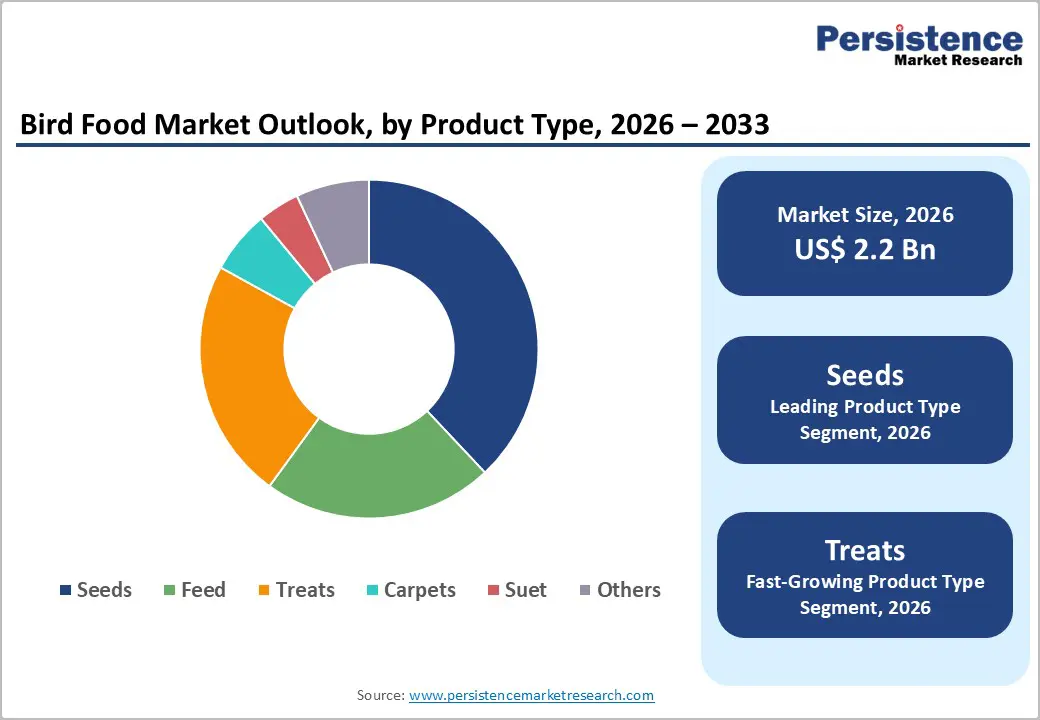

The global bird food market size is likely to be valued at US$ 2.2 billion in 2026, and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 3.5% during the forecast period 2026−2033. Market expansion is expected to remain steady, supported by rising household pet ownership, increasing urban engagement with companion animals, and growing awareness of nutrition as a determinant of avian longevity and vitality.

Consumer behavior indicates a clear transition from generic feed toward nutritionally balanced formulations aligned with veterinary guidance and standardized feeding practices. This shift enables higher per-unit value realization across organized retail channels and specialty distribution networks, reinforcing premiumization trends within the category. Regulatory frameworks governing animal welfare and feed safety strengthen quality benchmarks, prompting manufacturers to prioritize traceable sourcing, standardized processing, and compliant labeling practices.

Technological integration across supply chains enhances formulation consistency, shelf stability, and ingredient transparency, contributing to stronger consumer confidence. Parallel expansion of organized retail infrastructure and digital commerce platforms improves product accessibility across developed and emerging economies, supporting broader market penetration and sustained demand growth

Key Industry Highlights

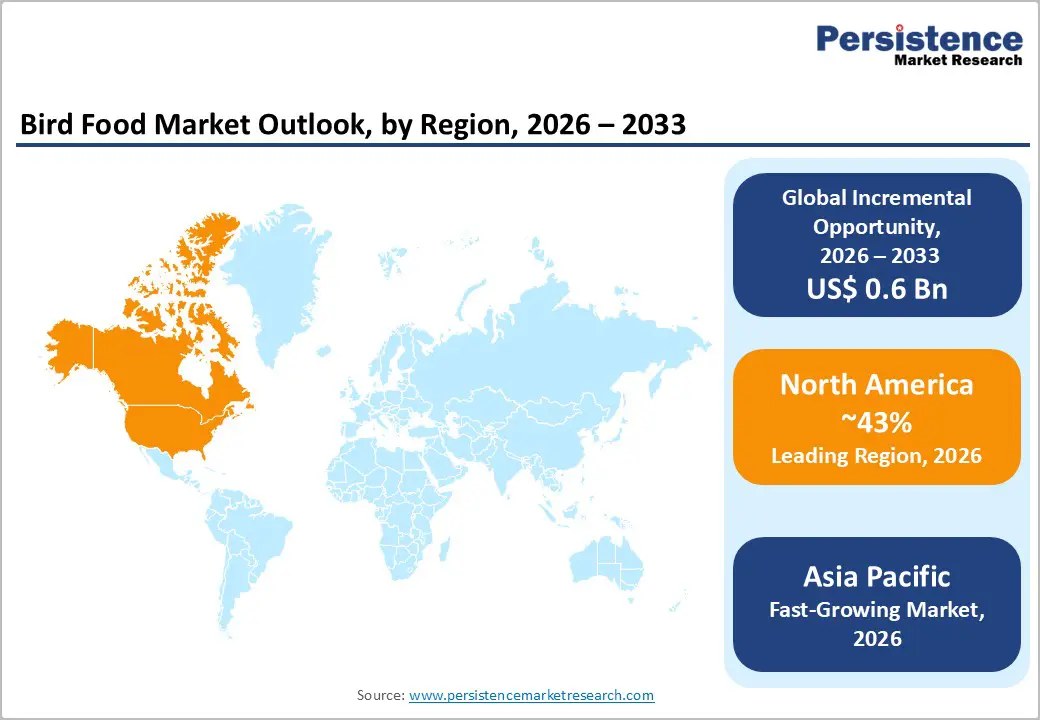

- Dominant Region: North America is projected to hold a 43% share in 2026, driven by premium animal nutrition demand and wide retail and e-commerce access.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market through 2033, fueled by increase in companion bird interest and expanding retail and digital access.

- Leading Product Type: Seed is poised to hold an estimated 38% share in 2026, supported by natural feeding alignment, broad price accessibility, and reliable supply.

- Fastest-growing Product Type: Treats are set to be the fastest-growing segment from 2026 to 2033, propelled by humanization of birds, enrichment-focused feeding, and functional benefits.

- January 2026: The Royal Horticultural Society partnered with Harvest Wildlife Products to launch a licensed range of wild bird food featuring carefully crafted seed blends and high-energy suet treats designed to attract songbirds and other garden species.

| Key Insights | Details |

|---|---|

|

Bird Food Market Size (2026E) |

US$ 2.2 Bn |

|

Market Value Forecast (2033F) |

US$ 2.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Companion Bird Adoption across Urban Households

Urban lifestyle transformation positions companion birds as a practical and emotionally rewarding pet option within high-density residential environments. Apartment-focused housing, structured work schedules, and limited outdoor access encourage preference for pets aligned with space efficiency and predictable care routines.

Birds fit these parameters, leading to greater emphasis on consistent feeding practices that support visible health indicators such as activity levels, feather condition, and lifespan. Nutrition therefore shifts from a basic requirement to a care standard linked with responsible ownership. This dynamic elevates demand for formulated, balanced diets that align with wellness outcomes, supporting regular purchase frequency and stable consumption patterns across urban households.

Urban concentration of companion bird owners strengthens exposure to professional guidance, digital education channels, and specialty retail ecosystems, shaping informed purchasing behavior. Veterinary recommendations and standardized feeding protocols influence trust in branded nutrition solutions positioned around quality, safety, and functional benefits.

A 2023 American Pet Products Association survey reports over 6 million households in the United States maintaining companion birds, validating demand density within developed urban markets. This ownership scale supports predictable repeat sales, encourages premium product adoption, and reinforces reliance on organized retail and e-commerce platforms for accessibility and assortment depth.

Volatility in Agricultural Raw Material Supply Chains

Procurement stability remains a structural challenge as feed manufacturers depend heavily on grains, oilseeds, and natural additives sourced from agriculture-intensive regions. Climatic variability, shifting cultivation patterns, and export policy fluctuations disrupt predictable input availability, creating frequent cost swings.

Such instability complicates long-term supplier contracts and inventory planning, limiting pricing predictability across production cycles. Manufacturers face margin pressure when raw material costs rise faster than retail price adjustments, particularly within value-sensitive consumer segments. Inconsistent supply quality further affects formulation uniformity, raising risks related to nutrient balance and product performance expectations.

Operational complexity intensifies when supply disruptions force rapid reformulation or supplier substitution. Compliance with feed safety standards requires rigorous testing and validation, extending lead times and increasing working capital requirements. Smaller producers encounter greater exposure due to limited hedging capacity and lower bargaining power within upstream procurement networks.

Volatile input costs reduce investment flexibility for innovation, packaging upgrades, and brand-building initiatives, slowing category development. Retail partners experience downstream impacts through irregular product availability and price revisions, influencing consumer trust and repeat purchasing behavior.

Expansion of Premium and Specialized Formulations

Sophistication in pet care decisions positions premium and specialized nutrition as a high-impact growth lever. Bird owners increasingly evaluate feed through the lens of species specificity, life stage requirements, and functional health outcomes such as plumage quality, immunity support, and digestive balance.

Generic seed mixes no longer align with these expectations, leading to demand for fortified blends, organic ingredients, and veterinarian-aligned formulations. This preference shift supports margin expansion, stronger brand differentiation, and reduced price sensitivity, aligning commercial value with perceived health benefits. Premium offerings also fit well within specialty retail and curated online channels, where informed purchasing behavior dominates and education-driven merchandising increases conversion efficiency.

Product specialization further unlocks opportunity through alignment with regulatory standards, transparency expectations, and lifestyle-driven consumption patterns. Controlled ingredient sourcing, clean-label positioning, and traceable supply chains reinforce trust among urban consumers with higher disposable income. Innovation in formulation science enables targeted solutions for exotic species, breeding birds, and aging populations, expanding addressable demand beyond traditional segments.

Specialized portfolios encourage repeat purchasing through tailored feeding regimens and subscription-led digital models. Strategic investment in research, formulation consistency, and packaging differentiation elevates perceived value while insulating portfolios from commodity pricing pressures.

Category-wise Analysis

Product Type Insights

Seeds are poised to lead with a forecasted 38% of the bird food market revenue share in 2026, owing to their widespread acceptance as a staple dietary component across multiple bird species. Seeds align with natural feeding behaviors, supporting strong palatability, habitual intake patterns, and feeding routine stability across household and aviary settings. Broad availability across economy, mid-range, and premium price tiers sustains high-volume adoption among diverse consumer groups.

Established sourcing networks and standardized processing practices enable cost efficiency and supply reliability for manufacturers. Veterinary guidance positions balanced seed blends as foundational nutrition when formulated correctly. Ongoing innovation in fortified seed mixes enriched with vitamins, minerals, and probiotics improves nutritional adequacy while retaining consumer familiarity and trust.

Treats are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by increasing humanization of companion birds and demand for enrichment-focused feeding. Consumption patterns increasingly emphasize engagement, reward-based interaction, and behavioral stimulation as part of daily care routines. Functional treats designed for training, mental activity, and stress reduction strengthen emotional bonding between owners and birds.

Retail strategies highlight attractive packaging and point-of-sale placement that encourages impulse purchases and trial behavior. Product development centered on natural ingredients, texture variation, and health-oriented functionality supports premium positioning, repeat purchases, and higher average selling prices within organized retail and digital channels.

Sales Channel Insights

Economical channels are likely to be the leading segment with a projected 46% of the bird food market share in 2026, due to affordability and extensive retail penetration. Price accessibility enables consistent adoption across diverse income groups, reinforcing high-volume purchasing patterns and stable demand cycles. Wide distribution through traditional pet shops, agricultural supply stores, and local cooperatives strengthens reach across urban and semi-urban areas.

Large retail chains support predictable stocking practices and competitive pricing structures, ensuring uninterrupted availability. These factors encourage habitual purchasing behavior and brand continuity, positioning economical channels as a dependable revenue base for manufacturers focused on scale and operational efficiency.

Premium channels are expected to witness the fastest growth between 2026 and 2033, powered by rising nutritional awareness and discretionary spending among urban consumers. Purchasing decisions increasingly reflect emphasis on ingredient quality, formulation precision, and perceived health outcomes.

Veterinary-recommended formulations enhance credibility and justify higher price realization within specialty outlets and curated digital platforms. Distinctive packaging, clear labeling, and controlled sourcing reinforce value perception. Growth momentum is supported by targeted merchandising, digital visibility, and curated product assortments across organized retail formats.

End-User Insights

The household segment is slated to hold a dominant position, with an anticipated 62% of market share in 2026, driven by routine consumption patterns and recurring purchase cycles. Companion bird ownership maintains steady demand through daily feeding requirements and long-term care commitments. Broad product diversity across seeds, pellets, and functional blends enables alignment with varied species and life stages.

Strong retail accessibility through local pet stores, mass merchants, and online platforms ensures convenient replenishment. Price tier flexibility supports sustained participation across income groups, reinforcing volume stability and repeat purchasing behavior within this end-user category.

The veterinary specialty segment is forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by increasing reliance on professional nutritional guidance. Pet owners increasingly seek expert recommendations to address health management, recovery, and preventive care needs.

Veterinary clinics serve as credible advisory points shaping purchasing decisions toward specialized and fortified formulations. Structured feeding protocols and condition-specific nutrition enhance product credibility and adherence. Integration of nutritional counseling within clinical services expands exposure to advanced formulations and supports higher-value product uptake.

Regional Insights

North America Bird Food Market Trends

North America is projected to capture an estimated 43% share of the bird food market in 2026, reflecting high adoption of companion birds and mature consumption patterns. Routine feeding practices and recurring purchase behavior underpin steady demand, while a preference for fortified, species-specific, and functional nutrition supports premium segment growth. High penetration of organized retail chains, veterinary clinics, and e-commerce platforms ensures wide product accessibility, enabling consistent replenishment across urban and suburban households.

Advanced supply chain infrastructure facilitates rapid distribution of perishable and specialized formulations, minimizing stockouts and maintaining product quality. Strong consumer education on health outcomes associated with nutrition drives selection of fortified seed mixes, pellets, and enrichment-focused treats, establishing a robust pipeline for both volume and high-margin products.

Key factors driving dominance include widespread integration of professional nutritional guidance and stringent quality compliance standards. Veterinary-recommended formulations reinforce adoption of high-value products, while adherence to feed safety and labeling regulations builds consumer confidence. Household income levels and discretionary spending power further allow premium product experimentation, supporting differentiation through innovative blends, functional additives, and eco-friendly packaging.

Established sourcing networks enable cost-effective procurement of high-quality seeds and natural ingredients, optimizing operational efficiency for manufacturers. Technological adoption in formulation, packaging, and digital marketing enhances engagement with informed buyers, driving brand loyalty.

Europe Bird Food Market Trends

Europe demonstrates a stable and mature landscape in the bird food sector, supported by high awareness of avian nutrition, long-standing companion bird ownership, and well-established retail infrastructure. Consumers prioritize quality, safety, and formulation transparency, favoring fortified seeds, pellets, and functional treats that address species-specific needs and life stage requirements.

Organized retail channels, including specialty pet stores and large supermarket chains, provide consistent access to diverse product portfolios, while e-commerce platforms enhance convenience and support subscription-based purchasing models. Veterinary guidance plays a key role in shaping purchasing decisions, reinforcing adoption of nutritionally balanced formulations and functional products designed to support plumage quality, immunity, and digestive health.

Sustainability and regulatory compliance are significant drivers in product development and distribution. Compliance with feed safety regulations, labeling standards, and animal welfare policies ensures high-quality sourcing, processing, and packaging practices.

Consumers increasingly prefer products with traceable ingredients, eco-friendly packaging, and natural additives, which drives premiumization and differentiation across the sector. Innovation in functional formulations, enrichment-focused treats, and clean-label options aligns with lifestyle-driven consumption patterns and urban households’ willingness to invest in companion bird well-being.

Asia Pacific Bird Food Market Trends

Asia Pacific is forecasted to be the fastest-growing market for bird food between 2026 and 2033, stimulated by rising urbanization, increasing disposable income, and growing interest in companion birds among metropolitan households. Expansion of modern retail formats, specialty pet stores, and digital commerce platforms enhances product accessibility and drives penetration of premium and specialized feed offerings.

Consumers increasingly seek fortified, species-specific, and functional formulations that support avian health, plumage quality, and behavioral enrichment. Exposure to veterinary guidance, social media education, and influencer-driven content reinforces informed purchasing decisions, accelerating adoption of higher-value products.

Shifts in consumer preferences toward health-conscious and enrichment-focused feeding further support rapid market growth. Functional treats, clean-label blends, and eco-friendly formulations are gaining traction, aligning with evolving lifestyle and sustainability priorities. Localized production and optimized regional supply chains reduce costs, improve lead times, and allow faster response to emerging demand trends.

Strategic collaborations between feed manufacturers, veterinary services, and digital platforms strengthen credibility and encourage repeat purchasing. Rising awareness of mental stimulation, behavioral enrichment, and preventive nutrition drives uptake of specialized products, creating a high-growth environment that combines volume expansion with premiumization potential.

Competitive Landscape

The global bird food market structure demonstrates moderate fragmentation, characterized by the presence of both regional operators and multinational corporations. Key players, including Kaytee Products, Inc., Lafeber Company, Versele-Laga NV, ZuPreem, The Higgins Group Corp., and Mars, Incorporated and its Affiliates, collectively account for roughly one-third of total revenue.

This indicates a competitive environment where smaller regional manufacturers maintain relevance through niche offerings, local distribution networks, and tailored product formulations. Market dynamics favor companies capable of combining scale with product specialization, enabling both broad reach and targeted consumer engagement. Innovation in nutritional content, functional additives, and species-specific feed remains a critical differentiator, shaping consumer preferences and purchasing behavior.

Competitive positioning in this landscape emphasizes brand trust, distribution efficiency, and formulation expertise. Established players leverage recognized brand equity and veterinary endorsements to influence purchasing decisions, particularly for premium and specialized offerings. Extensive distribution networks across organized retail, specialty outlets, and e-commerce platforms ensure consistent product availability, reinforcing repeat purchase behavior.

Investment in research and development enables formulation optimization, functional enrichment, and adherence to regulatory standards, supporting product credibility and premiumization. Regional operators often differentiate through local ingredient sourcing, cost-effective production, and tailored marketing strategies that resonate with domestic consumer bases.

Key Industry Developments

- In January 2026, Birdbuddy unveiled its next-generation smart bird feeders featuring enhanced AI species recognition and integrated solar power, debuting upgraded models that combine advanced imaging, sustainable energy and intelligent connectivity at CES2026.

- In November 2025, Bird Foods announced plans to aggressively expand its footprint by launching the experiential Freddo Bakehouse café format and targeting 100 outlets across malls and high streets in metros as well as tier-2 and tier-3 cities over the next two to three years.

- In February 2025, Harvest unveiled a new premium wild bird food brand called The Little Birdhouse with nine crafted seed mix variations at the National Garden Press Event, aiming to enhance nutrient-rich feeding options for garden birds and expand its retail presence.

Companies Covered in Bird Food Market

- Kaytee Products, Inc.

- Lafeber Company

- Versele-Laga NV

- ZuPreem

- The Higgins Group Corp.

- Mars, Incorporated and its Affiliates.

- Vitakraft pet care GmbH & Co. KG

- roudybush

- Pretty Bird International, Inc.

- Harrison’s Bird Foods

- Spectrum Brands, Inc.

Frequently Asked Questions

The global bird food market is projected to reach US$ 2.2 billion in 2026.

The market is driven by rising companion bird ownership, increasing nutritional awareness, premiumization trends, and expanding retail and digital distribution channels.

The bird food market is poised to witness a CAGR of 3.5% from 2026 to 2033.

Key market opportunities include premium and specialized formulations, digital and e‑commerce integration, functional and enrichment-focused products, and expansion into fast-growing urban and emerging regions.

Some of the key market players include Kaytee Products, Inc., Lafeber Company, Versele-Laga NV, ZuPreem, The Higgins Group Corp., and Mars, Incorporated and its Affiliates.