- Bulk Chemicals

- Asphalt Additives Market

Asphalt Additives Market Size, Share, and Growth Forecast 2026 - 2033

Asphalt Additives Market by Product Type (Polymeric Modifiers, Emulsifiers, Anti-strip and Adhesion Promoters, Chemical Modifiers, Rejuvenators, Others), Technology (Hot Mix, Cold Mix, Warm Mix, Oil & Gas, Others), Application (Road Construction & Paving, Roofing, Airport, Industrial, Other), and Regional Analysis for 2026 - 2033

Asphalt Additives Market Size and Trend Analysis

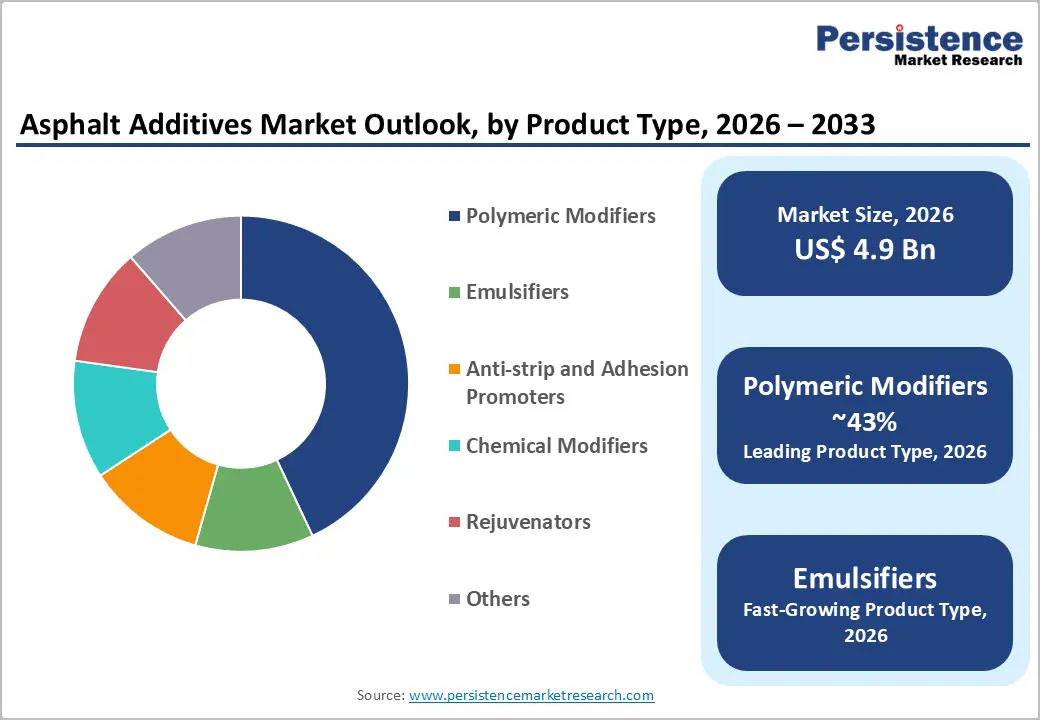

The global Asphalt Additives market size is valued at US$ 4.9 billion in 2026 and is projected to reach US$ 8.2 billion by 2033, growing at a CAGR of 7.7% between 2026 and 2033.

Accelerating investments in road and highway infrastructure across global markets, particularly in emerging economies, remains the principal driver of the asphalt additives market. Governments are allocating unprecedented budgetary resources to modernize transportation networks, reduce logistics inefficiencies, strengthen economic connectivity, and address aging pavement systems. These advanced solutions require specialized additive formulations, thereby generating steady, incremental demand throughout the value chain and reinforcing the market’s long-term growth trajectory.

Key Industry Highlights:

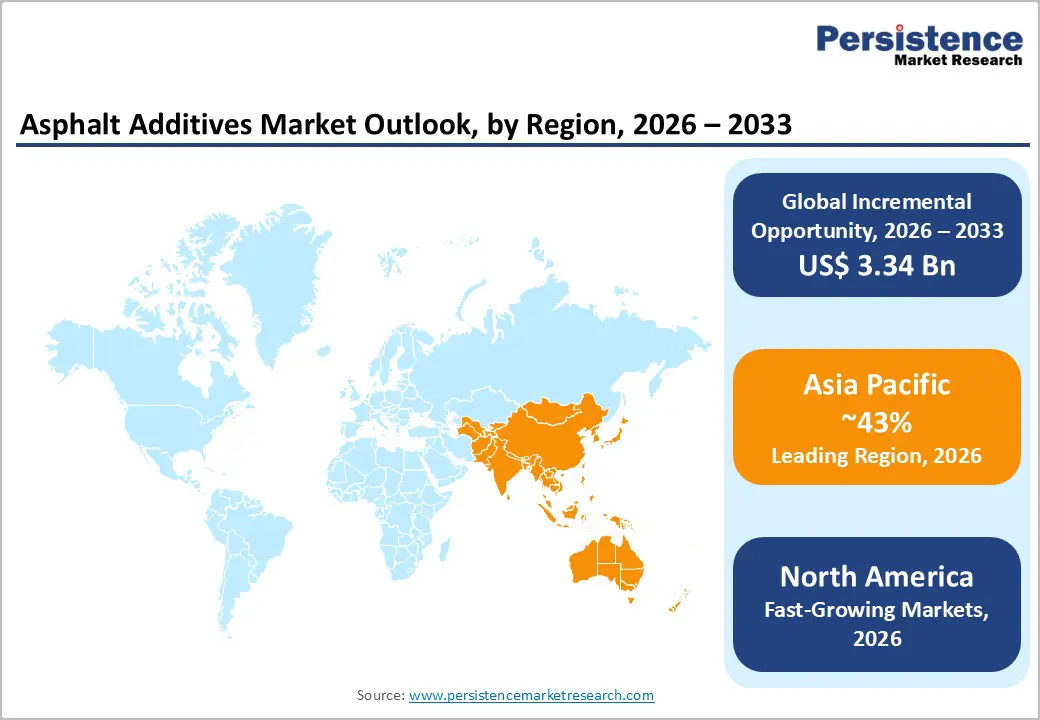

- Leading Region: Asia Pacific dominates the global asphalt additives market, accounting for 43% of revenue, underpinned by massive road construction programs in China, India, and ASEAN economies, extensive government investment, and rapidly expanding manufacturing infrastructure.

- Fastest-Growing Region: North America is the fastest-growing region in the Asphalt additives market, driven by

- a highly developed regulatory ecosystem, including performance-based standards established by AASHTO and the Federal Highway Administration (FHWA).

- Dominant Segment: Polymeric Modifiers lead the Product Type category with approximately 43% market share, owing to their superior pavement performance characteristics, including high rutting resistance and fatigue-crack prevention, which are critical for heavy-traffic road infrastructure globally.

- Fastest-Growing Segment: Warm Mix Asphalt (WMA) technology is the fastest-growing segment, gaining momentum due to

- lower energy consumption, reduced greenhouse gas emissions, and strong policy tailwinds from the EU Green Deal and global decarbonization commitments.

- Key Opportunity: Integration of Reclaimed Asphalt Pavement (RAP), driven by circular-economy mandates and EAPA's target of 50%+ RAP content by 2050, creates a substantial structural growth opportunity for rejuvenator and bio-based additive manufacturers globally.

| Key Insights | Details |

|---|---|

|

Asphalt Additives Market Size (2026E) |

US$ 4.9 Bn |

|

Market Value Forecast (2033F) |

US$ 8.2 Bn |

|

Projected Growth CAGR (2026–2033) |

7.7% |

|

Historical Market Growth (2020–2025) |

6.6% |

Market Dynamics

Drivers - Surge in Global Infrastructure Investment

The primary driver of the asphalt additives market is the significant expansion of infrastructure investment undertaken by governments across both developed and developing regions. In the United States, the Infrastructure Investment and Jobs Act (IIJA) allocates approximately US$1.2 trillion toward national infrastructure, including nearly US$379.3 billion designated for highway programs for fiscal years 2022–2026, marking the largest federal commitment to road development in the country’s history.

Similarly, India has accelerated its national highway initiatives, with the National Highways Authority of India (NHAI) constructing 5,614 kilometers of highways in FY 2024–25, surpassing its target by 9% and achieving a record capital expenditure of INR 2.5 lakh crore. Furthermore, the Bharatmala Pariyojana program aims to develop around 34,800 kilometers of economic corridors, collectively driving increased demand for asphalt additives to enhance pavement durability and performance.

Rising Demand for High-Performance and Durable Pavements

Modern road infrastructure requirements have substantially elevated the performance specifications for asphalt. Urban networks are now subjected to heavier axle loads, significant thermal variation, and increased chemical exposure, necessitating asphalt mixtures enhanced with advanced additives. Studies show that more than 45% of global road infrastructure incorporates such additives to reduce deterioration, extend service life, and limit long-term maintenance needs.

Polymer modifiers, especially Styrene-Butadiene-Styrene (SBS) copolymers, significantly improve viscoelastic behavior and resistance to rutting and fatigue, extending pavement lifespan by approximately 40–50% compared with unmodified asphalt. Additionally, the growing scale and technical complexity of infrastructure projects, including multi-lane expressways, bridge decks, and airport runways, is accelerating the adoption of specialized additives such as anti-strip agents, rejuvenators, and fiber reinforcements, thereby supporting sustained market demand over the forecast period.

Restraints - Volatility in Raw Material Costs

A significant restraint for the Asphalt Additives market is the substantial volatility in petrochemical-derived raw materials. Polymers and synthetic rubbers, key inputs, remain highly sensitive to fluctuations in crude oil prices. The U.S. Bureau of Transportation Statistics reported that asphalt was the leading contributor to quarterly increases in the National Highway Construction Cost Index from late 2021 through mid-2022, a period during which U.S. crude oil prices rose nearly 594% from their 2020 lows. Such volatility compresses manufacturers' margins and complicates long-term budgeting for road agencies, ultimately hindering the adoption of additive manufacturing in cost-sensitive public-sector projects.

Regulatory and Specification Fragmentation Across Geographies

The asphalt additives market is challenged by highly fragmented regulatory frameworks across global regions. Performance specifications vary considerably across ASTM standards in North America, EN standards in Europe, and diverse regional requirements in Asia and the Middle East, resulting in significant inconsistencies. This regulatory divergence compels manufacturers to undertake extensive product reformulation, restricts cross-border standardization, and prolongs approval timelines for new additive technologies.

As companies navigate differing jurisdictional mandates, compliance expenditures rise substantially and are often transferred to end users. Consequently, adoption rates, particularly for emerging bio-based and nanotechnology-enhanced additives, are adversely affected due to increased costs and elongated market entry processes.

Opportunity - Warm Mix Asphalt Technology as a Sustainability-Driven Growth Avenue

The accelerating adoption of Warm Mix Asphalt (WMA) technology presents a significant growth opportunity for asphalt additive manufacturers. WMA is produced and compacted at temperatures approximately 30-50°C lower than conventional Hot Mix Asphalt (HMA), operating around 110-140°C compared with 150-180°C, thereby achieving notable reductions in fuel consumption, greenhouse gas emissions, and worker exposure to fumes.

The European Asphalt Pavement Association (EAPA) indicates that WMA, when combined with the incorporation of reclaimed asphalt, could enable an additional 2.2% reduction in CO emissions by 2050. With the European Union’s Green Deal mandating at least a 55% decrease in emissions from 1990 levels by 2030, demand for advanced WMA additives, including chemical surfactants, organic waxes, and zeolite-based formulations such as Evotherm, Sasobit, and Rediset, is expected to rise substantially across developed markets.

Reclaimed Asphalt Pavement (RAP) Integration and Rejuvenator Demand

The growing emphasis on circular-economy principles in the road construction sector is creating a significant opportunity for producers of rejuvenator additives. Reclaimed Asphalt Pavement (RAP) usage is increasing rapidly as governments implement sustainability-focused construction mandates. In 2024, RAP constituted an average of 13.2% of asphalt mixes in Europe, while the EAPA’s Net Zero Decarbonisation Roadmap (2024) targets raising this share to 50% or more by 2050.

Similarly, the National Asphalt Pavement Association (NAPA) reports that RAP is recycled into new manufactured products at a higher rate than any other construction and demolition material in the United States. Rejuvenators play a critical role by restoring oxidized bitumen in high-RAP mixtures, enabling performance comparable to virgin asphalt and driving sustained demand growth as global recycled-asphalt requirements continue to expand.

Category-wise Analysis

Product Type Insights

Polymeric Modifiers represent the leading product segment in the asphalt additives market, accounting for roughly 43% of the global market share. This dominance stems from their superior ability to enhance elastic recovery, minimize permanent deformation, and extend the fatigue life of asphalt pavements subjected to heavy and repetitive loads.

Among available systems, SBS and SBR remain the most widely adopted due to their seamless compatibility with established hot mix asphalt processes. Continued R&D investment by leading companies further strengthens this position, including Kraton Corporation’s planned 24 kiloton annual expansion of its SBS production by 2025 and Arkema’s development of specialized polymer systems tailored for diverse climatic conditions worldwide.

Technology Insights

The Hot Mix Asphalt (HMA) segment holds the dominant share of the Asphalt Additives market, representing approximately 62% of technology-based demand. HMA has long served as the foundation of global road construction due to its proven structural reliability, adaptability across diverse traffic conditions, and compatibility with a wide range of additives, including polymer modifiers, anti-strip agents, and fiber reinforcements. Its extensive and well-established manufacturing infrastructure, particularly in developed regions, continues to support sustained, high-volume consumption of related additives.

In contrast, the Warm Mix Asphalt (WMA) segment is the fastest-growing technology category, propelled by stringent environmental regulations and sustainability objectives. Research published in Innovative Infrastructure Solutions (2025) demonstrates that WMA significantly reduces greenhouse gas emissions and energy usage by enabling asphalt production at lower temperatures, thereby strengthening demand for chemical surfactants and organic wax additives.

Application Insights

The Road Construction & Paving segment remains the leading application area in the Asphalt Additives market, accounting for approximately 45% of total application-based revenue. This dominance is driven by the scale of global road development, as highways and arterial networks constitute the largest end-use category for asphalt. Enhancing pavement durability, safety, and lifecycle performance under rising traffic loads has made the use of additives essential rather than optional.

In the United States, road construction represents the largest share of IIJA highway allocations, reinforcing sustained additive consumption. In India, the Pradhan Mantri Gram Sadak Yojana-IV (2024–29) program aims to construct 62,500 kilometers of rural roads with an investment of US$8.21 billion, further accelerating demand. Additionally, additive-intensive applications such as airport runways and roofing are emerging as secondary growth segments due to requirements for high load tolerance and improved weather resistance.

Regional Insights

North America Asphalt Additives Market Trends

North America maintains a strategic position in the global asphalt additives market, led primarily by the United States. The region benefits from a highly developed regulatory ecosystem, including performance-based standards established by AASHTO and the Federal Highway Administration (FHWA), which mandate the use of advanced asphalt technologies in federally funded projects. The Infrastructure Investment and Jobs Act (IIJA) further strengthens long-term demand by allocating US$110 billion specifically for roads, bridges, and major infrastructure initiatives.

Furthermore, the National Asphalt Pavement Association (NAPA) continues to promote Warm Mix Asphalt adoption through its “The Road Forward” sustainability program. The U.S. also leads globally in Reclaimed Asphalt Pavement (RAP) recycling, creating favorable conditions for rejuvenator and bio-based additive producers. Innovation in polymer modification and warm mix technologies remains concentrated domestically, supported by companies such as Kraton Corporation, Ingevity Corporation, and Honeywell International.

Europe Asphalt Additives Market Trends

Europe represents a mature yet highly innovation-driven market for Asphalt Additives, with Germany, France, the United Kingdom, and Spain constituting the region’s largest national markets. The European Asphalt Pavement Association (EAPA), comprising 16 national associations and 23 equipment and material suppliers, actively promotes advanced asphalt technologies and their environmental benefits. The European Green Deal has further strengthened sustainability mandates across the construction sector, compelling asphalt producers to reduce lifecycle carbon emissions and accelerating the adoption of Warm Mix Asphalt additives, reclaimed asphalt rejuvenators, and bio-based emulsifiers.

EAPA’s Decarbonisation Roadmap (2024) targets increasing reclaimed asphalt content in European mixes to over 50% by 2050, up from 13.2% in 2024, reinforcing demand for rejuvenators and adhesion promoters. Regulatory harmonization under EN standards is also supporting market consolidation and cross-border product standardization, while the 2024 entry of Shrieve Chemical with its PROGILINE® ECO-T range underscores rising competition and ongoing product innovation.

Asia Pacific Asphalt Additives Market Trends

Asia Pacific represents the largest regional market for Asphalt Additives, with 43% market share, supported by the extensive scale of infrastructure development across China, India, and ASEAN economies. China remains the world’s leading asphalt consumer, driven by its expansive national expressway network and Belt and Road Initiative-linked road programs. ASEAN countries, such as Vietnam, Indonesia, and Thailand, are undertaking major road densification programs. BASF SE’s 2024 expansion of its Nanjing additives plant underscores the region’s strategic manufacturing importance and sustained growth outlook.

India continues to advance its national highway construction at an average pace of approximately 29 km per day during 2024–25, with the highway network expanding 60% over the past decade to reach 146,195 km as of January 2025. The Union Budget 2024–25, which allocated US$32.68 billion to the Ministry of Road Transport and Highways, further reinforces long-term demand.

Competitive Landscape

The global asphalt additives market is moderately fragmented, with top-tier players collectively accounting for approximately one-third of global revenue. Market leaders are pursuing multi-pronged growth strategies encompassing capacity expansions, geographic diversification, strategic partnerships with road construction firms and chemical distributors, and sustained R&D investments in sustainable and bio-based additive formulations. Key differentiators include product portfolio breadth spanning multiple additive categories, technical service capabilities, regulatory approval credentials across major markets, and the ability to supply high-volume infrastructure projects. Emerging business model trends include long-term supply agreements with national road agencies, co-development partnerships with asphalt producers for application-specific solutions, and the integration of digital quality-monitoring tools into additive deployment.

Key Developments:

- April 2025: Kraton Corporation launched the CirKular+ Paving Circularity Series, a purpose-built product line designed to maximize the recycling and reuse of reclaimed asphalt pavement, underscoring its commitment to circular-economy road-construction solutions.

- July 2024: Brenntag SE formalized a strategic distribution partnership with Nouryon to expand the reach of Nouryon's high-quality anti-stripping agents and asphalt emulsifiers across global markets, reinforcing both companies' positions in specialty asphalt chemistry.

- May 2024: BASF SE announced an investment to expand its advanced additives manufacturing plant at its Nanjing, China facility, adding a new production line for high-performance dispersants to meet rapidly growing market demand across Asia Pacific.

Top Companies in Asphalt Additives

Evonik Industries AG (Essen, Germany) is a global leader in specialty chemicals and a consistently top-ranked player in the Asphalt Additives market. The company's advanced additive solutions, including anti-stripping agents, adhesion promoters, and polymer modifiers, are embedded in road construction specifications across Europe, North America, and the Asia Pacific.

Kraton Corporation (Houston, U.S.) is one of the world's leading producers of SBS block copolymers, the workhorse of polymer-modified asphalt globally. The company's strategic capacity expansion announcement in March 2023 committed to adding 24 kilotons per year of SBS production at its Belpre, Ohio, facility by 2025. Its 2025 launch of the CirKular+ Paving Circularity Series positions Kraton at the forefront of the circular economy opportunity in road construction, targeting the fast-growing reclaimed asphalt rehabilitation segment.

Arkema S.A. (Colombes, France) commands a broad and diversified asphalt additive portfolio spanning polymer modifiers, bitumen modifiers, rejuvenators, and adhesion promoters, making it uniquely well-positioned across multiple market segments and climate conditions. The company's proprietary Warmgrip® warm-mix asphalt technology, developed in collaboration with Holcim Group and Boulder County and featured in NAPA Quarterly (2024), exemplifies its technical leadership in sustainable paving innovation.

Companies Covered in Asphalt Additives Market

- Evonik Industries AG

- Kraton Corporation

- Arkema S.A.

- Nouryon Chemicals

- Dow Inc.

- Honeywell International Inc.

- Huntsman Corporation

- Ingevity Corporation

- BASF SE

- AkzoNobel N.V.

- Sasol Limited

- Kao Corporation

- Sinopec

- ExxonMobil Chemical Company

Frequently Asked Questions

The global Asphalt Additives market is valued at US$ 4.9 Bn in 2026 and is projected to reach US$ 8.2 Bn by 2033, expanding at a CAGR of 7.7%. Over the historical period 2020–2025, the market expanded at a CAGR of 6.6%, growing from US$ 3.3 Bn in 2020. Growth is underpinned by surging infrastructure investment across both mature and emerging economies.

The primary demand drivers for the Asphalt Additives market include large-scale government investment in road and highway infrastructure, exemplified by the US$ 1.2 trillion IIJA in the United States and India's US$ 32.68 Bn road budget for 2024–25, alongside escalating demand for durable, high-performance pavements capable of withstanding heavier traffic loads and extreme weather.

Polymeric Modifiers lead the Product Type category, accounting for approximately 43% of market share. Their dominance is attributed to their superior performance enhancement capabilities, specifically in improving pavement elasticity, resistance to rutting, and fatigue cracking resistance. SBS and SBR copolymers remain the most widely deployed systems in both new road construction and rehabilitation applications worldwide.

Asia Pacific holds the largest share of the global Asphalt Additives market, driven by the world's most active road construction programs in China, India, and ASEAN nations. India's national highway network expanded 60% over a decade to 146,195 km by January 2025, while China's extensive expressway development continues at scale. Government-led infrastructure programs, rapid urbanization, and large construction material manufacturing capacity all reinforce the Asia Pacific's leadership.