- Display Technologies

- 8K Technology Market

8K Technology Market Size, Share, and Growth Forecast, 2026 - 2033

8K Technology Market by Product Type (8K Television, 8K Camera, 8K Monitors/Laptops, 8K Projectors and Others), End-user (Consumer Electronics, Media, Advertising & Entertainment, Medical & Healthcare, Education and Others) and Regional Analysis for 2026 - 2033

8K Technology Market Size and Trends Analysis

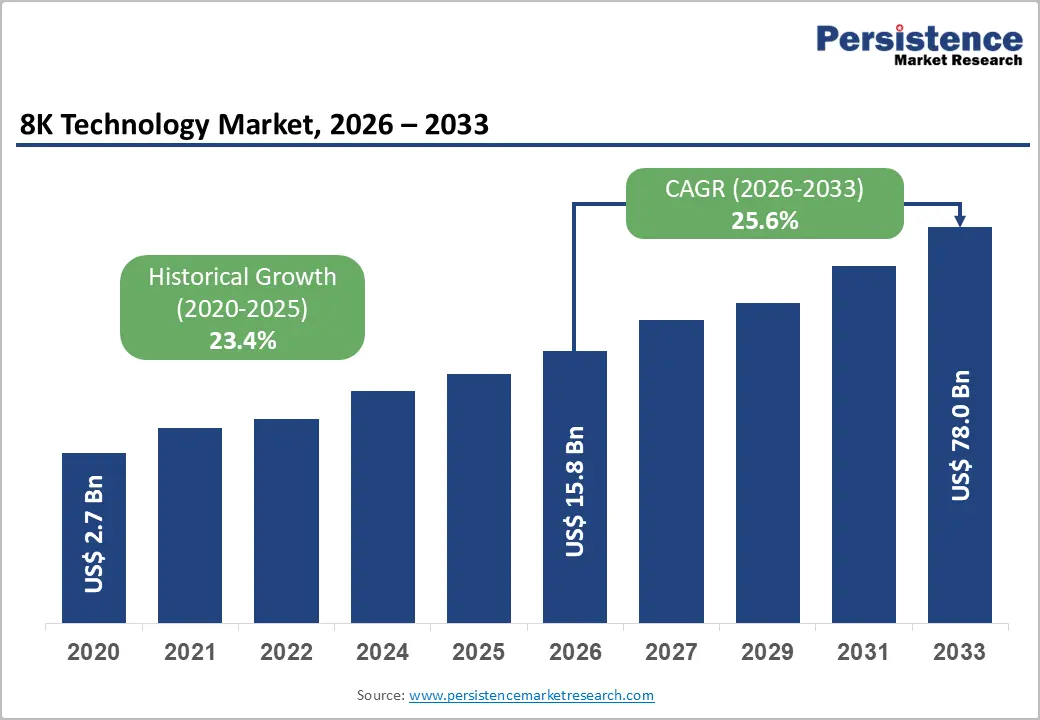

The global 8K technology market is projected to reach US$ 78.0 billion by 2033, growing at a CAGR of 25.6% between 2026 and 2033. The market is likely to be valued at US$ 15.8 billion in 2026. The market is driven by increasing availability of 8K content across streaming platforms and broadcasting networks, technological breakthroughs enabling affordable manufacturing, and expanded infrastructure supporting 8K delivery.

Key Industry Highlights:

- Leading Product Type: 8K televisions dominate with 39.1% market share, driven by consumer preference and a home entertainment focus; 8K projectors are the fastest-growing at a 28% CAGR, driven by expansion in cinema, entertainment venues, and professional applications.

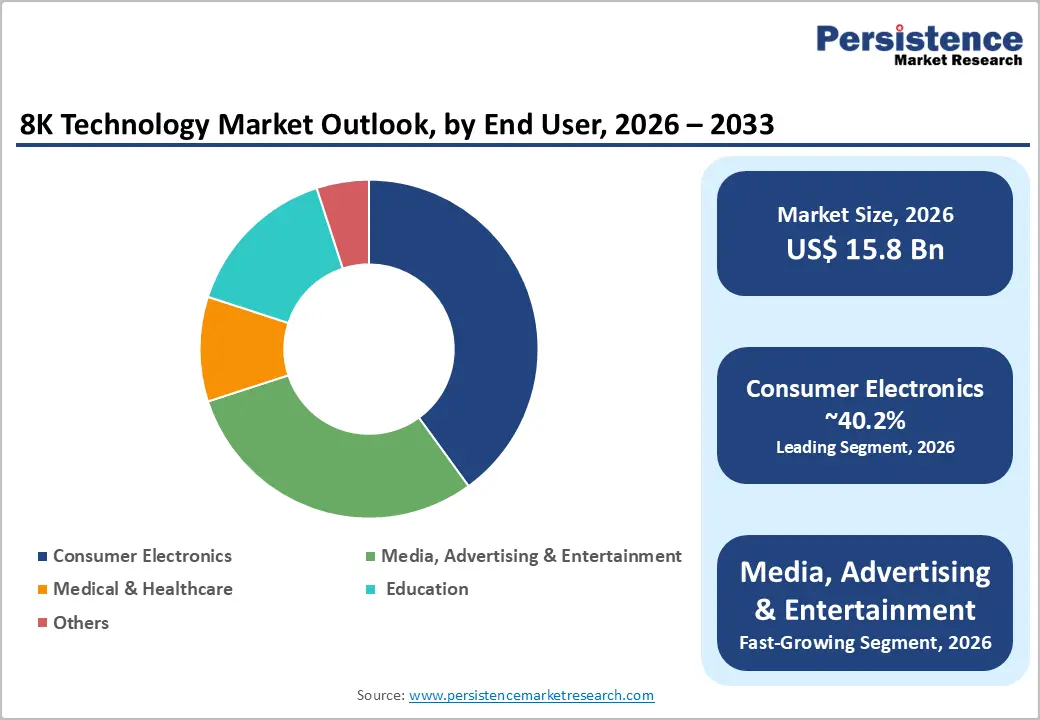

- Dominant End-Use Application: Consumer electronics maintains 40.2% market share through primary device orientation; Media, advertising, and entertainment is the fastest-growing at a 32% CAGR, driven by content production expansion and broadcast infrastructure investment.

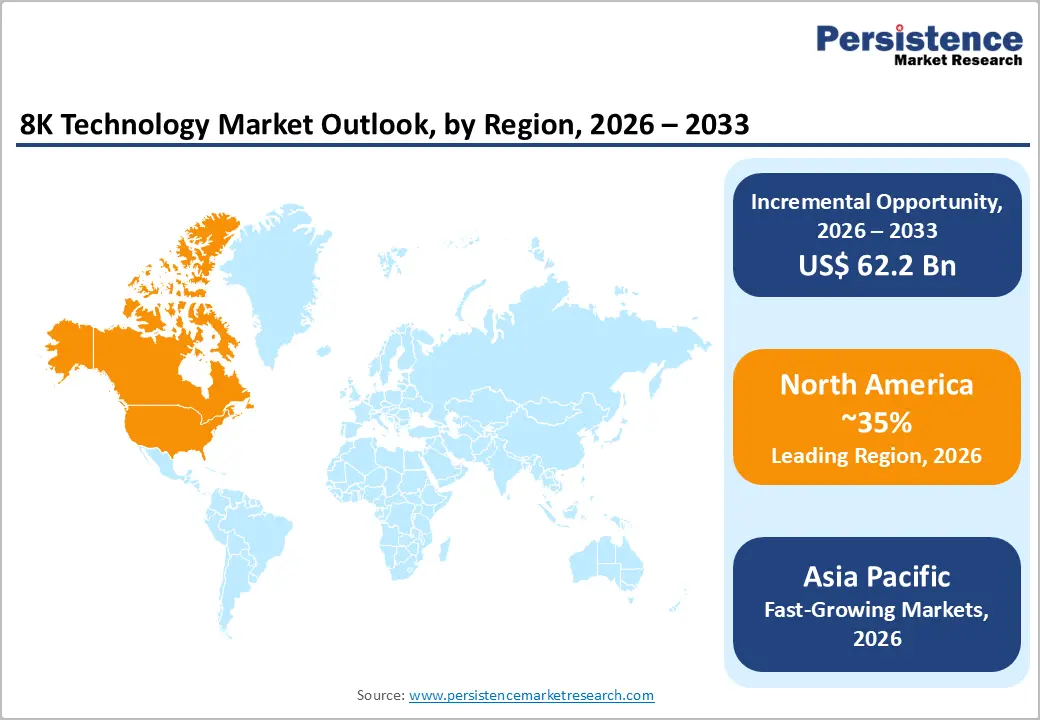

- Regional Market Dominance and Growth: North America maintains 30-35% global market share, driven by a premium consumer base and broadcast investment; Asia-Pacific demonstrates the fastest regional growth at 28-35% CAGR, expanding from 38% current share to 50% by 2033 through manufacturing dominance and emerging market expansion.

- Technology and Market Innovation Momentum: Top 10 suppliers control 50% market share (Samsung, LG, Sony leading); Display technology breakthroughs (QLED, OLED, Micro-LED) enabling superior 8K quality; AI-enabled upscaling improving content library utilization; 8K content libraries expanding 40-50% annually with streaming platforms and broadcasters.

- Manufacturing and Infrastructure Expansion: Asian manufacturers controlling 75% of display panel production, enabling cost reduction; Broadcasting infrastructure investment of US$ 10-15B annually, supporting 8K transmission capability; Content production investment of US$ 5-8B annually by streaming platforms, expanding addressable content library.

| Key Insights | Details |

|---|---|

|

8K Technology Market Size (2026E) |

US$ 2.8 Bn |

|

Market Value Forecast (2033F) |

US$ 6.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

13.5% |

|

Historical Market Growth (CAGR 2020 to 2024) |

12.8% |

Market Dynamics

Drivers - Explosive Growth in 8K Content Creation and Streaming Availability

Global streaming platforms and broadcasters have allocated approximately US$ 5-8 billion annually for 8K content production and infrastructure expansion, establishing systematic demand for 8K-compatible devices. Major streaming platforms, including Netflix, Amazon Prime Video, YouTube, and Apple TV+, are progressively expanding their 8K-compatible content libraries, with estimated 8K content availability expanding by 40-50% annually through 2033. Live sports broadcasting demonstrates major growth catalyst, with international sports organizations including the Olympics, FIFA World Cup, and professional leagues testing 8K transmission reaching 20-30 million concurrent viewers annually.

Content production acceleration, with Hollywood studios, independent producers, and streaming platforms investing in 8K cameras and equipment, creates 60-70% annual growth in professional 8K content libraries. Broadcast infrastructure investment, with governments and private companies allocating US$ 10-15 billion annually for broadcasting network upgrades supporting 8K transmission, establishing a delivery infrastructure foundation.

Revolutionary Advances in Display Panel Technology and Manufacturing Capabilities

Display panel technology breakthroughs, with QLED, OLED, Mini-LED, and Micro-LED technologies, enable superior 8K visualization, delivering 30-40% improved brightness and color accuracy versus previous generations, driving consumer preference. Manufacturing cost reduction trajectory, with 8K television prices declining 25-35% annually through 2024-2026 and projected to reach price parity with 4K by 2030, expand addressable consumer market. Production capacity expansion, with major manufacturers including Samsung, LG, Sony, and Chinese competitors establishing combined production capacity exceeding 15-20 million units annually, enables rapid market scaling.

Quality consistency improvement, with manufacturing process standardization and yield rate improvement reaching 85-90% for premium quality units, establish reliability confidence. Supply chain optimization, with component sourcing and manufacturing efficiency, improves cost structures by 15%, compresses pricing while maintaining margin expansion.

Restraints - Limited 8K Content Availability and Bandwidth Infrastructure Constraints

8K content scarcity, with available native 8K content representing <5% of total streaming libraries and requiring 15-25 years for proportionate content ecosystem development, constrains consumer value justification. Production cost barriers, with professional 8K content production consuming 40-50% higher budgets than 4K equivalents due to specialized equipment and production requirements, limit content creator participation. Infrastructure limitations, with existing broadband infrastructure in 60-70% of developed markets and <20% of emerging markets supporting consistent 4K streaming versus 8K requirements, create delivery constraints.

Bandwidth requirements escalation, with 8K streaming requiring 100-150 Mbps versus 25-50 Mbps for 4K, exceeding the capacity of standard consumer connections in many regions. Technology standardization delays, with competing transmission standards and encoding protocols, create interoperability challenges that delay infrastructure deployment.

High Capital Equipment Costs and Consumer Price Barriers

Consumer electronics pricing, with premium 8K televisions commanding US$ 5,000-15,000+ versus US$ 1,500-4,000 for high-quality 4K equivalents, restricts the addressable market to affluent consumers (top 15-20% income tier). Professional equipment costs, with broadcast-grade 8K cameras, projectors, and display systems costing US$ 50,000-500,000+, limit adoption to well-capitalized organizations.

Retrofit complexity and cost, with implementing 8K capability requiring infrastructure upgrades, equipment replacement, and operational modifications, consuming 20-40% implementation investment, create adoption friction. Maintenance and support requirements, along with specialized technician expertise and service infrastructure that require 5–10 years of development in many emerging markets, limit accessibility. Technology obsolescence risk, with rapid advancement cycles creating 4–6-year equipment lifecycles, discourages early adoption among price-sensitive consumers.

Opportunity - 8K Gaming and Virtual Reality Integration

Gaming hardware specialization, with gaming console manufacturers and PC makers increasingly supporting 8K resolution at 120+ frame rates, create dedicated gaming application opportunity. VR/AR integration advancement, with virtual reality and augmented reality platforms leveraging 8K resolution for immersive experience enhancement, establishing emerging segment foundation. Esports and streaming, with professional esports tournaments broadcasting at 8K resolution to reach 50-100 million concurrent viewers, drive equipment demand from esports venues.

Gaming display adoption, with gaming-specific 8K monitors incorporating 144+ Hz refresh rates and advanced response times, is attracting competitive gamers, expand gaming segment. Market opportunity estimates suggest 8K gaming segment will expand from US$ 800-1.2 billion (2026) to US$ 4.0-6.0 billion (2033), representing 26-32% CAGR, substantially exceeding overall market growth.

Enterprise and Professional 8K Integration

Digital transformation investment, with enterprises allocating US$100-200 billion annually for advanced visualization and communication infrastructure, creates a significant B2B opportunity. Telemedicine and remote collaboration, with medical consultations, engineering design reviews, and legal proceedings increasingly utilizing 8K video conferencing, providing superior resolution and presence perception, drive B2B adoption. Architectural and design visualization, with architectural firms, product designers, and engineers adopting 8K displays for collaborative visualization, improving design accuracy by 25-35%, establish professional segment foundation.

Data center and analytics applications, with financial services, research institutions, and analytics firms leveraging 8K displays for complex data visualization and monitoring applications, create specialized demand. Market opportunity estimates suggest the enterprise and professional segment will expand from US$ 1.5-2.2 billion (2026) to US$ 5.0-7.5 billion (2033), representing 18-24% CAGR.

Category-wise Analysis

Product Type Insights

The 8K television segment holds 39.1% market share, driven by strong consumer demand for premium home entertainment. Televisions remain the largest consumer electronics category, positioning 8K TVs as the flagship product for ultra-high-resolution viewing. Households spend 3–4 hours daily on home entertainment, encouraging adoption among premium consumers seeking superior visual quality. Established manufacturing ecosystems enable high-volume, cost-efficient 8K TV production, reinforcing market leadership. Content availability is also television-centric, with streaming platforms and broadcasters prioritizing TVs for 8K delivery. Large screen sizes (60–85 inches) maximize the visual benefits of 8K resolution, while well-developed retail channels accelerate consumer adoption.

In contrast, the 8K projector segment is the fastest growing, projected to expand at 29% CAGR through 2033. Growth is driven by demand from high-end cinemas, luxury homes, commercial venues, and professional applications. 8K projectors deliver unmatched impact on 200–400-inch displays, supporting immersive entertainment, corporate visualization, medical training, and architectural design. Improving brightness, reliability, and declining costs are enabling broader commercial deployment, positioning projectors as the fastest expanding 8K product category.

End-user Insights

The consumer electronics sector holds 40.2% market share, driven by its focus on premium consumer devices. 8K televisions dominate, accounting for 65–75% of the consumer electronics 8K market value, positioning TVs as the primary adoption channel. Demand is concentrated among affluent consumers, with the top 15–20% of income groups accounting for 75–85% of segment revenue. Strong emphasis on home entertainment, representing 25–35% of discretionary electronics spending, supports adoption, while streaming platforms prioritize TV and mobile optimization. Well-established retail networks and significant manufacturer investment in 8K consumer education further accelerate market penetration.

The media, advertising, and entertainment segment is the fastest-growing, projected to expand at 32% CAGR through 2033. Growth is driven by rapid investment in 8K content production, expansion of live sports broadcasting, and increased use of 8K digital signage to enhance ad recall. Entertainment venues, content creators, and streaming platforms are investing heavily in 8K displays, cameras, and production infrastructure to deliver immersive experiences and future-proof content libraries.

Regional Insights

North America 8K Technology Market Analysis

Market Scale and Performance: North America commands approximately 35% of global 8K Technology market share, valued at approximately US$ 5.53 billion in 2026 with projections approaching US$ 28.0 billion by 2033. The United States represents dominant regional market contributor, accounting for 75% of the North American market value, driven by premium consumer base and advanced broadcast infrastructure.

Consumer electronics spending leadership, with North American consumers allocating US$ 200-300 billion annually to home entertainment and valuing 8K premium positioning driving purchasing preference. Broadcasting infrastructure investment, with major broadcasters and streaming platforms based in North America (Netflix, Amazon, Apple TV+, Disney+) allocating 30-40% of content budgets to 8K production and distribution. Professional application expansion, with North American hospitals, research institutions, and corporate entities investing heavily in 8K visualization and collaboration technology driving professional segment growth.

Europe 8K Technology Market Insights

Europe represents approximately 22% of global 8K Technology market share, valued at approximately US$ 3.16 billion in 2026. Germany, United Kingdom, France, and Spain collectively represent 65% of European market value, reflecting advanced consumer base and manufacturing infrastructure.

Premium consumer segments, with European consumers demonstrating strong preference for advanced technology and willingness to pay premium pricing for 8K devices, driving per-capita consumption above global average. Broadcasting standards harmonization, with European Union establishing unified broadcasting standards supporting 8K transmission, enable coordinated infrastructure investment across member states. Healthcare and medical technology leadership, with European hospitals and research institutions leading 8K medical imaging adoption, drive professional segment investment. Sustainability and energy efficiency focus, with European consumers and regulators prioritizing energy-efficient 8K devices, create competitive advantage for advanced efficiency technologies.

Asia Pacific 8K Technology Market Analysis

Asia-Pacific demonstrates robust growth dynamics, commanding approximately 30% market share with projections increasing to 45% by 2033. The region valued at approximately US$ 5.2 billion in 2026 is anticipated to reach US$ 35.3 billion by 2033, representing fastest-growing regional market with estimated CAGR of 28-35%.

Manufacturing capability dominance, with China, South Korea, Japan, and Taiwan controlling 75% of global 8K display panel production, enables cost-competitive positioning supporting consumer market penetration. Emerging market consumer growth, with China and India adding 200-300 million affluent consumers annually seeking premium electronics, establish substantial addressable market for 8K consumer devices. Government broadcasting investment, with national broadcasters in China, Japan, South Korea, and Southeast Asia investing US$ 5-10 billion annually in 8K transmission infrastructure supporting Olympic preparation and major event broadcasting.

Competitive Landscape

The global 8K technology market is characterized by the presence of major players including BOE Japan, Canon, Dell Technologies, Hisense, Ikegami Tsushinki, LG Electronics, Panasonic, Red Digital Cinema Camera, Samsung Electronics, and Sharp Corporation. These companies are heavily investing in product innovation, particularly in developing advanced display technologies such as MicroLED and quantum dot integration for enhanced picture quality.

Operational agility is demonstrated through strategic partnerships with content providers and streaming platforms to create and deliver 8K content. Companies are expanding their product portfolios beyond traditional television displays into professional monitors, cameras, and medical imaging equipment.

Key Industry Developments

- In March 2024, Samsung Electronics Singapore announced its 2024 lineup of QLED 8K TVs and OLED displays equipped with AI, offering an enhanced home entertainment experience. These products, along with its latest sound systems, were launched at its Unbox and Discover 2024 Singapore event.

- In April 2023, DJI announced its latest professional-class Inspire 3 drone for aerial cinematography. Its design, sensor, connectivity, and operation feature numerous advancements over its predecessor. The new Inspire 3 includes a full-frame Zenmuse X9-8K Air Gimbal Camera sensor, which is their most delicate yet, and supports DJI's CineCore 3.0 image processing system.

Companies Covered in 8K Technology Market

- Dell Technologies

- Red Digital Cinema

- Viewsonic

- Panasonic

- Ikami Electronics

- Digital Projection

- TP Vision

- Samsung Electronics

- LG Electronics

- Sony Corporation

- Others Key Players

Frequently Asked Questions

The 8K Technology market is estimated to be valued at US$ 15.8 Bn in 2026.

The key demand driver for the 8K Technology market is the growing demand for ultra-high-resolution visual experiences in premium consumer electronics, professional content creation, and large-format display applications.

In 2026, the North America is likely to dominate with an exceeding 35% revenue share in the global 8K Technology market.

Among the End- use, Consumer Electronics accounts for the highest preference, capturing beyond 40.2% of the market revenue share in 2026, surpassing other End- use type.

The key players in 8K Technology are Dell Technologies, Red Digital Cinema, Viewsonic, Panasonic and Ikami Electronics.