- Specialty & Fine Chemicals

- 1,4-Diisopropylbenzene Market

1,4-Diisopropylbenzene Market Size, Share, and Growth Forecast, 2026 – 2033

1,4-Diisopropylbenzene Market by Product Type (Standard, High Purity), Application (Paints & Coatings, Electrical & Electronics, Chemical Intermediates, Solvents, Graphic Arts), and Regional Analysis for 2026 – 2033

1,4-Diisopropylbenzene Market Size and Trends Analysis

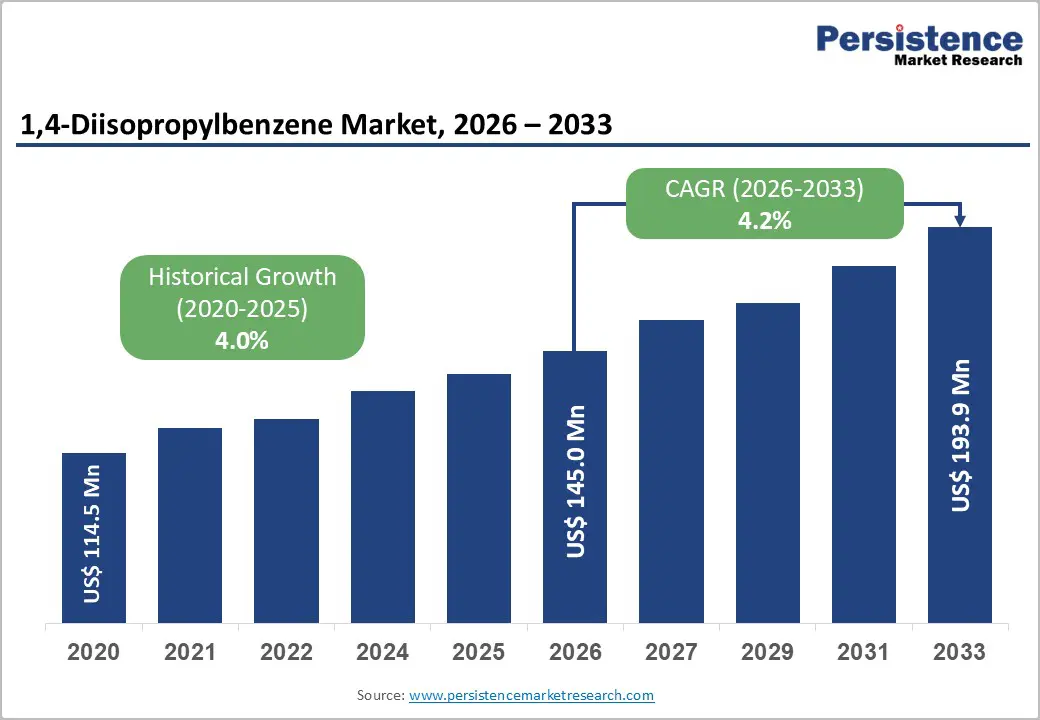

The global 1,4-Diisopropylbenzene market size is likely to be valued at US$145.0 million in 2026 and is expected to reach US$193.9 million by 2033, growing at a CAGR of 4.2% during the forecast period from 2026 to 2033, driven by its expanding role as a key aromatic intermediate in specialty chemical production. The market continues to benefit from stable demand across chemical intermediates and solvent applications, particularly in the manufacturing of antioxidants, polymer stabilizers, hydroquinone derivatives, and performance additives.

Growth is largely driven by industrial expansion in end-user sectors such as high-performance polymers, lubricants, resins, and specialty coatings, where purity and chemical stability are critical. Increasing utilization in paints & coatings and electrical & electronics applications supports sustained volume consumption, as DIPB-based derivatives enhance durability, thermal resistance, and oxidation stability.

Key Industry Highlights:

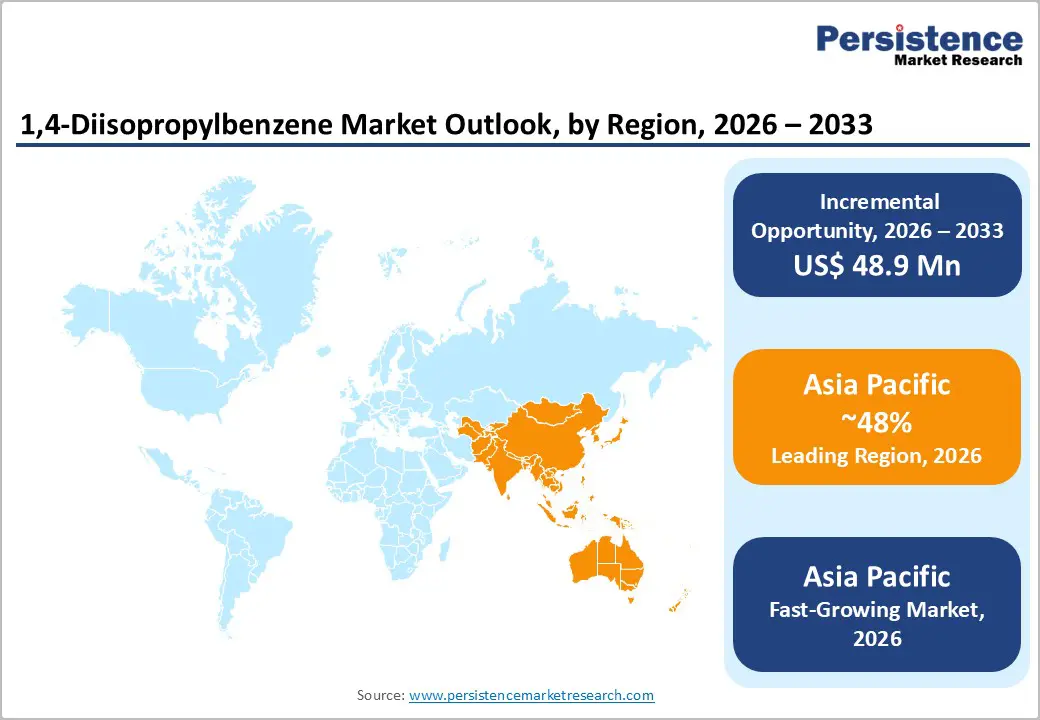

- Leading Region: Asia Pacific, accounting for a market share of 48% in 2026, driven by strong chemical manufacturing growth and expanding industrial demand across China, Japan, India, and ASEAN countries.

- Fastest-growing Region: Asia Pacific, supported by expanding chemical manufacturing capacity, rising demand for high-performance polymers, and specialty intermediates.

- Leading Product Type: The high purity segment, accounting for 78% of the revenue share, is driven by strong demand from high-performance polymer and electronics applications requiring superior purity levels.

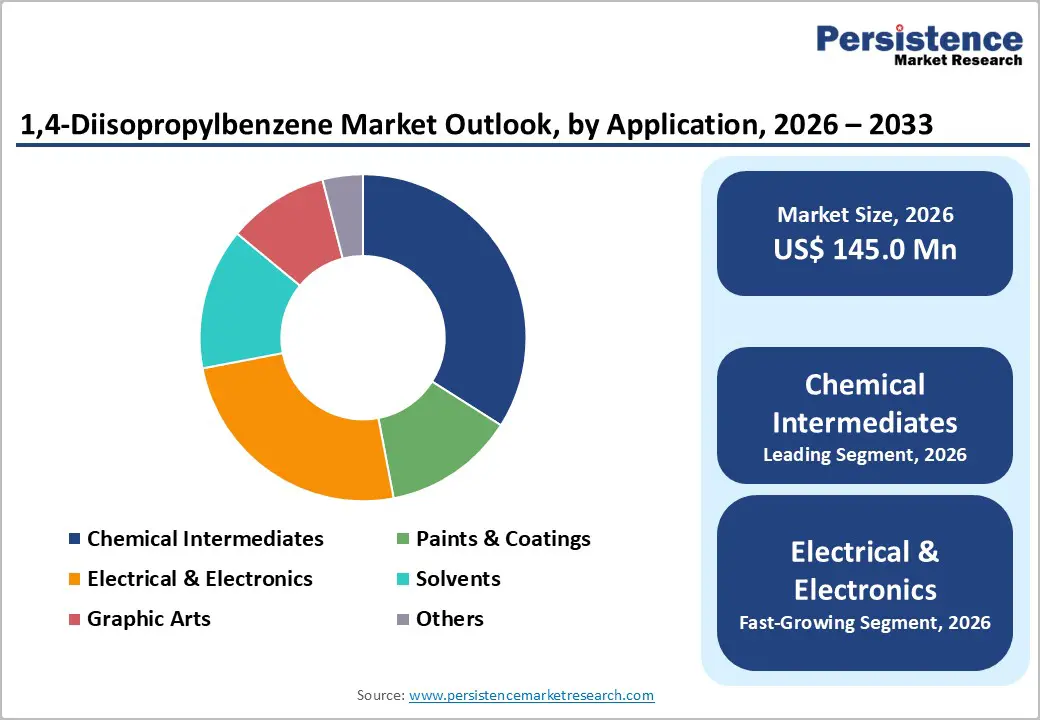

- Leading Application: The chemical segment, accounting for over 35% of the revenue share in 2026, is supported by its extensive use in antioxidant production, polymer stabilizers, and specialty chemical synthesis.

| Key Insights | Details |

|---|---|

| 1,4-Diisopropylbenzene Market Size (2026E) | US$145.0 Mn |

| Market Value Forecast (2033F) | US$193.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand in Chemical Intermediates and Polymer Production

It plays an important role in the production of hydroquinone, antioxidants, polymer stabilizers, and specialty additives used across high-performance plastics and engineered materials. Increasing demand for durable polymers in automotive, packaging, electrical components, and industrial equipment supports steady uptake. As polymer manufacturers focus on improving oxidation resistance and thermal stability, the requirement for reliable intermediate compounds continues to strengthen, reinforcing long-term growth prospects for DIPB producers worldwide.

Expanding downstream petrochemical and specialty chemical industries across Asia Pacific and other emerging regions stimulates demand. Rapid industrialization, infrastructure projects, and rising manufacturing output create consistent requirements for polymer-based materials. DIPB’s compatibility with advanced synthesis processes enhances its value in producing performance-enhancing additives. As industries emphasize material efficiency and extended product lifespan, consumption of polymer stabilizers and intermediates rises accordingly.

Growth in Paints & Coatings and Solvents Sectors

1,4-Diisopropylbenzene (DIPB) based derivatives contribute to improved durability, chemical resistance, and performance of coatings used in construction, automotive, and industrial equipment. Rising infrastructure development and refurbishment activities increase demand for protective coatings. Industrial solvent consumption in manufacturing, cleaning, and formulation processes strengthens baseline demand, supporting consistent market momentum across mature and emerging economies.

Urbanization trends and increased investments in residential and commercial projects amplify coatings consumption. Manufacturers are increasingly seeking high-performance additives that enhance oxidation resistance and long-term stability in harsh environments. DIPB-derived intermediates support these functional improvements, making them attractive for premium coating formulations. Growth in the marine, aerospace, and heavy machinery sectors also stimulates demand for specialized protective layers.

Barrier Analysis - Regulatory Hurdles on Aromatic Hydrocarbons

Stringent environmental and safety regulations concerning aromatic hydrocarbons pose challenges to the 1,4-Diisopropylbenzene market. Regulatory agencies increasingly enforce stricter emission standards, workplace exposure limits, and waste disposal requirements. Compliance with these standards raises operational costs for manufacturers, particularly in regions with advanced environmental policies. Monitoring, reporting, and adherence to chemical safety frameworks require continuous investment, potentially affecting profit margins and slowing capacity expansions in certain developed markets.

Growing environmental awareness among consumers and industries encourages the shift toward safer or bio-based alternatives. Regulatory scrutiny on volatile organic compounds and hazardous chemicals can limit the application scope in specific end-use sectors. Producers must invest in cleaner production technologies and improved handling practices to meet compliance requirements. These additional expenditures may reduce competitiveness for smaller players.

Availability of Substitutes

In antioxidant and polymer stabilization applications, manufacturers may substitute DIPB-derived intermediates with compounds such as di-tert-butylbenzene derivatives, cumene-based intermediates, or butylated hydroxytoluene (BHT) systems, depending on performance requirements and cost considerations. In certain hydroquinone production routes, alternative feedstock such as phenol-based or aniline-based chemistries can also reduce dependency on DIPB. When raw material prices fluctuate or supply disruptions occur, end users often shift toward these substitutes to maintain operational continuity and cost control.

In polymer and lubricant formulations, phosphite antioxidants, hindered amine light stabilizers (HALS), and other phenolic antioxidant blends may partially replace DIPB-based stabilizers where compatibility allows. Advancements in bio-based stabilizers and low-VOC additive systems are gaining traction in environmentally regulated markets, particularly in Europe and North America. Large chemical manufacturers increasingly diversify sourcing strategies to avoid over-reliance on a single intermediate, increasing substitution potential.

Opportunity Analysis - Technological Convergence in High-Purity Grades

Increasing demand from electronics, specialty polymers, and precision synthesis requires materials with minimal impurity levels. Innovations in catalytic processes and separation technologies enable manufacturers to produce ultra-refined grades efficiently. This capability enhances product differentiation and supports premium pricing strategies in quality-sensitive applications. Technological improvements in catalytic alkylation and multi-stage vacuum distillation are enabling tighter purity control and higher product consistency.

As industries such as semiconductors and advanced materials emphasize reliability and contamination control, the importance of high-purity feedstock continues to grow. Manufacturers investing in upgraded production facilities and quality assurance systems can capture expanding demand in these specialized segments. Integration of digital monitoring and process optimization improves yield consistency and cost management. Companies that upgrade production infrastructure to meet stringent industrial specifications are well-positioned to secure long-term supply contracts in high-margin specialty chemical markets.

Green Chemistry Technology Convergence

Producers are increasingly adopting energy-efficient catalytic alkylation processes, closed-loop solvent recovery systems, and low-emission purification technologies to minimize environmental impact. Optimization of benzene and propylene feedstock utilization reduces waste generation and improves atom economy, aligning with green chemistry principles. Implementation of heat integration systems and reduced volatile organic compound (VOC) emissions enhances environmental performance.

Development of lower-carbon production pathways and exploration of partially bio-based aromatic feedstock are gaining research attention. Integration of digital energy monitoring systems and carbon footprint tracking enables manufacturers to quantify sustainability improvements and meet ESG reporting standards. Strategic collaboration with downstream polymer and coatings producers supports the creation of eco-friendly stabilizer systems with improved lifecycle profiles. As industries prioritize decarbonization, circular economy practices, and responsible sourcing, DIPB manufacturers investing in sustainable process innovation are likely to gain a competitive advantage and secure long-term contracts.

Category-wise Analysis

Product Type Insights

High purity is expected to lead the 1,4-Diisopropylbenzene market, accounting for approximately 78% of revenue in 2026, driven by its strong preference in applications requiring minimal impurity levels and consistent chemical stability. High purity grades are widely used in advanced polymer stabilizers, antioxidant formulations, and electronic chemical intermediates, where trace contaminants can affect performance and durability. For example, in the electronics industry, high-purity DIPB is utilized in the synthesis of specialty additives that enhance oxidation resistance and long-term material reliability, reinforcing its leading market position across quality-sensitive industrial sectors.

High purity is also likely to represent the fastest-growing segment in 2026, supported by rising demand from specialty polymers, precision synthesis, and advanced materials manufacturing. Increasing emphasis on contamination control and product consistency in end-use industries accelerates the adoption of ultra-refined grades. Manufacturers are investing in improved purification and catalytic processing technologies to meet stringent quality specifications. For example, semiconductor-related chemical formulations require highly stable intermediates to maintain process reliability, thereby expanding the consumption of high-purity DIPB and supporting sustained growth momentum in this premium segment.

Application Insights

Chemical intermediates are projected to lead the market, capturing around 35% of the revenue share in 2026, supported by their foundational role in downstream synthesis processes. 1,4-Diisopropylbenzene serves as an essential intermediate in the production of hydroquinone, antioxidants, and polymer stabilizers used across plastics, lubricants, and specialty coatings industries. Broad integration into multiple chemical value chains strengthens its dominant position. For example, hydroquinone production relies on DIPB as a precursor in oxidation processes, supporting applications in polymer manufacturing and performance additives.

The electrical and electronics industry is likely to be the fastest-growing application, driven by expanding production of advanced components and high-performance materials. Increasing demand for oxidation-resistant polymers and thermally stable additives in circuit boards and electronic housings boosts the consumption of high-purity intermediates. As electronic devices become more compact and performance-oriented, material reliability becomes critical. For example, specialty resin systems used in electronic insulation require stable antioxidant intermediates, encouraging greater use of DIPB-derived compounds and accelerating growth within this technologically driven application segment.

Regional Insights

North America 1,4-Diisopropylbenzene Market Trends

North America is likely to be a significant market for 1,4-Diisopropylbenzene in 2026, driven by strong industrial demand from chemical intermediates, specialty polymers, and additive manufacturing sectors. The region benefits from well-established chemical and petrochemical infrastructure, which supports consistent production and supply of aromatic intermediates. Demand for high-purity grades is rising, particularly within electronics and lubricant additive applications that require stringent quality specifications. Regulatory emphasis on product safety and controlled handling also drives manufacturers to adopt cleaner, more precise production practices.

Sustainability and process efficiency are shaping market dynamics in North America. Companies are increasingly focusing on green chemistry and energy optimization within their facilities, aligning production with evolving environmental standards. For example, Eastman Chemical Company has integrated advanced purification and process monitoring systems at its U.S. chemical sites to improve yield and reduce emissions for intermediate chemicals, including aromatic compounds similar to DIPB. Regional players are expanding collaborations with research institutions to innovate lower-impact solvent systems and specialty additives.

Europe 1,4-Diisopropylbenzene Market Trends

Europe is likely to be a significant market for 1,4-Diisopropylbenzene, due to stringent environmental regulations and a strong emphasis on sustainable manufacturing practices. European chemical producers are increasingly adopting cleaner processes and advanced purification technologies to meet high regulatory standards, especially for aromatic intermediates used in specialty chemicals and performance materials. Countries such as Germany, France, and the Netherlands are key contributors to regional demand, supported by well-developed chemical and automotive industries.

Sustainability initiatives and industrial collaborations are critical trends shaping the European DIPB landscape. Companies are investing heavily in energy-efficient technologies and process automation to reduce carbon footprints and improve product quality. For example, Lanxess has undertaken modernization efforts at its European chemical facilities to enhance process control, reduce emissions, and improve the consistency of specialty chemical intermediates used in lubricant and polymer additive production. This strategic focus reflects a broader regional trend toward integrating environmental compliance with technological innovation.

Asia Pacific 1,4-Diisopropylbenzene Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 48% in 2026, driven by rapid industrialization and expanding downstream chemical industries in China, India, Japan, and Southeast Asian economies. Strong demand from polymer production, specialty coatings, and high-performance additives supports steady consumption of DIPB and its derivatives. Increasing investment in automotive manufacturing, electronics assembly, and infrastructure development in the region has also elevated the need for high-quality aromatic intermediates.

Technological adoption and capacity expansion are key trends in the Asia Pacific market, with producers focusing on improving production efficiency and meeting evolving quality standards. Companies are investing in upgraded process controls and advanced separation technologies to deliver consistent purity levels required by high-tech industries. For example, Mitsui Chemicals, Inc. has increased its production capabilities and technical support in Asia to supply high-purity intermediates for specialty polymer and additive applications. Such strategic moves enhance local supply reliability and reduce dependency on imports, positioning regional producers for long-term growth.

Competitive Landscape

The global 1,4-Diisopropylbenzene market exhibits a moderately fragmented structure, driven by the presence of several regional and international chemical manufacturers catering to diverse end-user industries. Market participation ranges from large integrated chemical producers to specialized intermediate suppliers, each focusing on quality, supply reliability, and technological advancement. Asia Pacific holds a significant manufacturing footprint, supported by local players and multinational subsidiaries that leverage low-cost production and tailor products for regional demand.

With key leaders including Eastman Chemical Company, Arkema, Mitsui Chemicals, Inc., Lanxess, and SAGECHEM, the competitive environment continues to evolve with new entrants and tier-2 suppliers strengthening capabilities. These players compete through product innovation, supply chain integration, and differentiated service offerings, particularly in delivering high-purity grades that meet the rigorous specifications of advanced polymer and electronic formulations. Strategic expansions, mergers and acquisitions, and collaborative R&D initiatives help established companies broaden their geographical reach and application portfolios.

Key Industry Developments:

- In August 2025, The Goodyear Tire & Rubber Company announced a definitive agreement to sell the majority of its Goodyear Chemical business, which includes facilities producing aromatic and intermediate chemicals such as 1,4-Diisopropylbenzene, to private equity firm Gemspring Capital Management for approximately US$650 million. The transaction covers chemical production sites in Houston and Beaumont, Texas, as well as an R&D office in Akron, Ohio, under a long-term supply arrangement.

Companies Covered in 1,4-Diisopropylbenzene Market

- Eastman Chemical Company

- Santa Cruz Biotechnology, Inc

- Arkema

- Hangzhou Yuhao Chemical Technology Co., Ltd.

- CHMA Chemical Technology (Shanghai) Co., Ltd

- Mitsui Chemicals, Inc.

- Rhein Chemie Corporation

- Matrix Scientific.

- Merck KGaA

- Lanxess

- SAGECHEM

- The Goodyear Tire & Rubber Company

- Syntechem Co. Ltd.

- TCI Chemical Pvt Ltd

- Biosynth Carbosynth

- Angene

- KANTO KAGAKU

- ABCR GmbH

- BLD Pharma

Frequently Asked Questions

The global 1,4-Diisopropylbenzene Market is projected to reach US$145.0 million in 2026.

Rising demand for high-purity aromatic intermediates in polymer manufacturing, specialty chemicals synthesis, and advanced materials applications.

The 1,4-Diisopropylbenzene Market is expected to grow at a CAGR of 4.2% from 2026 to 2033.

Key market opportunities in the growing demand for high-purity grades, sustainable production technologies, and expanding applications in electronics, polymers, and specialty chemicals.

Eastman Chemical Company, Santa Cruz Biotechnology Inc., Arkema, and Hangzhou Yuhao Chemical Technology Co., Ltd. are the leading players.