- Specialty & Fine Chemicals

- 1,4-Dicyclohexylbenzene Market

1,4-Dicyclohexylbenzene Market Size, Share, and Growth Forecast, 2026 - 2033

1,4-Dicyclohexylbenzene Market by Application (Adhesives, Paints & Coatings, Electrical & Electronics, Chemical Intermediate), End-User (Automotive, Aerospace, Electronics Industry, Construction), Purity (Below 99%, Above 99%), and Regional Analysis for 2026-2033

1,4-Dicyclohexylbenzene Market Share and Trends Analysis

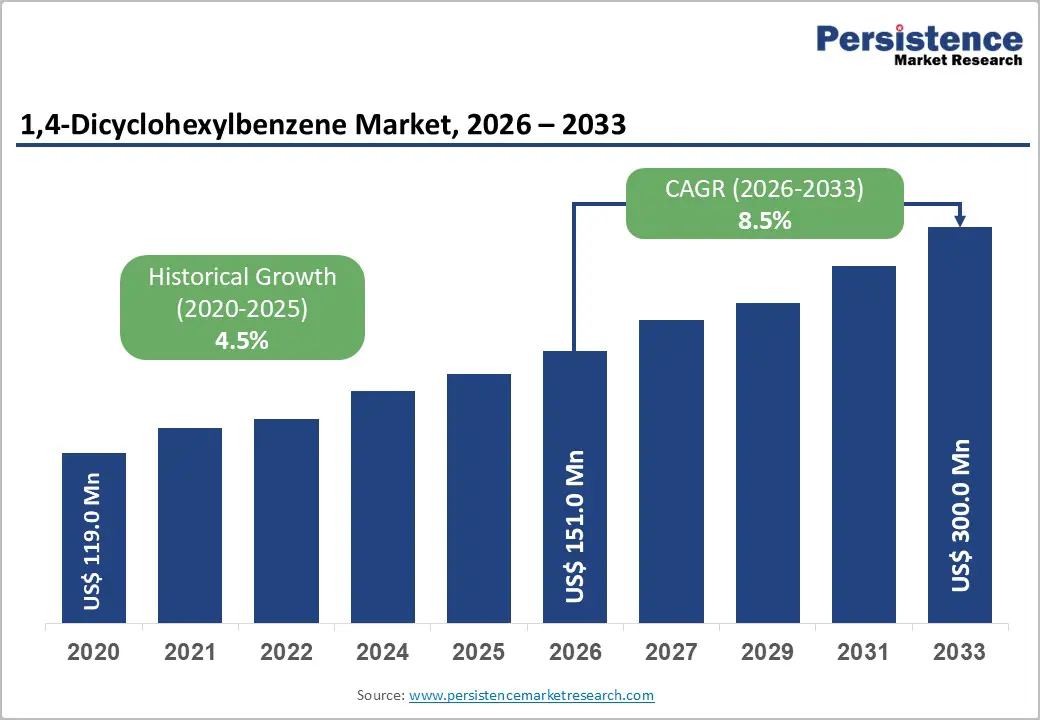

The global 1,4-dicyclohexylbenzene market is expected to grow from US$151.0 million in 2026 to US$300.0 million by 2033, at a CAGR of 8.5%. Growth is driven by increasing use in automotive, aerospace, and electronics for high-performance polymers and insulation materials. Strong thermal stability and chemical compatibility support its use in engineering plastics and performance resins. Expansion in Asia—especially China, South Korea, and India—along with stricter regulatory standards, is encouraging suppliers to invest in high-purity production and quality control.

Key Industry Highlights

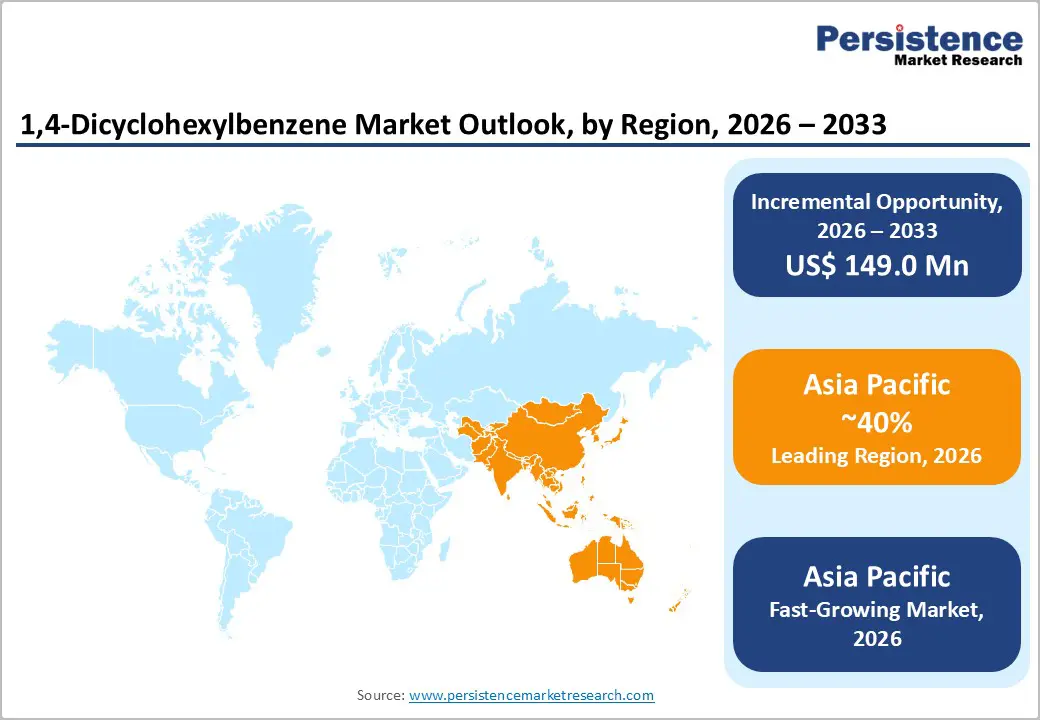

- Dominant Region & Fastest-growing Regional Market: Asia Pacific is poised to be the fastest-growing and the leading market with a projected 40% share in 2026, supported by expansion of production capacities by local manufacturers.

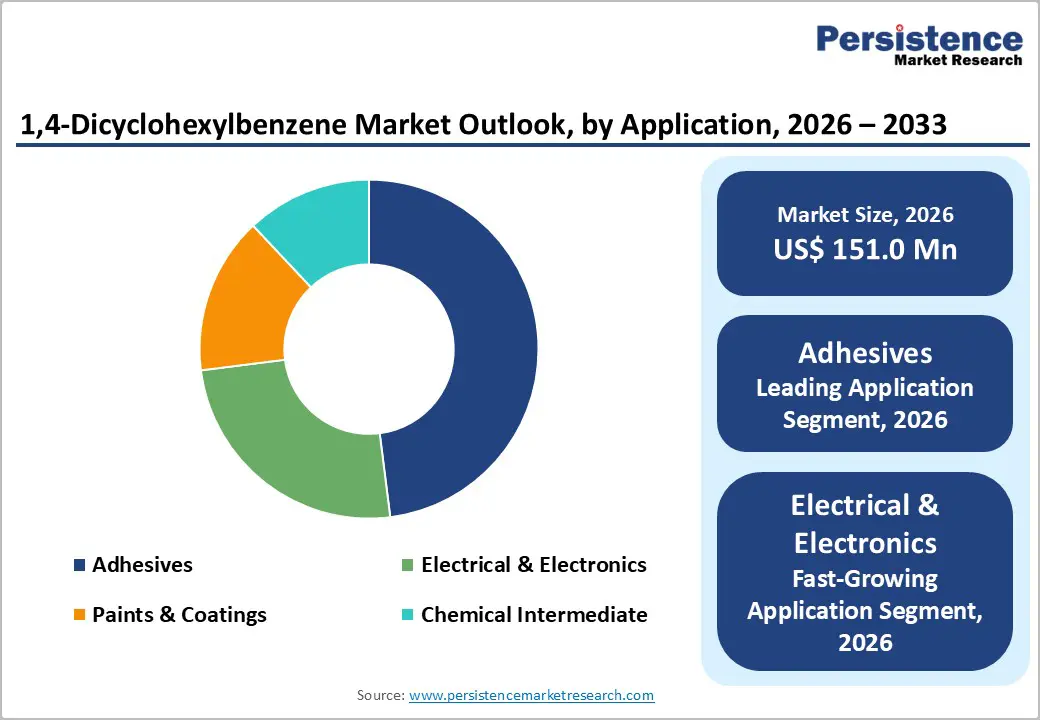

- Leading & Fastest-growing Applications: Adhesives are set to dominate by capturing around 32% of the market revenue share in 2026, while electrical & electronics are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing End-user: Automotive is expected to hold an estimated revenue share of 45% in 2026, whereas electronics is expected to be the fastest-growing segment between 2026 and 2033.

- Market Driver: Technological improvements in selective hydrogenation catalysts have significantly improved yield efficiency and cost optimization for cyclohexyl-based aromatics.

| Key Insights | Details |

|---|---|

|

1,4-Dicyclohexylbenzene Market Size (2026E) |

US$ 151.0 Mn |

|

Market Value Forecast (2033F) |

US$ 300.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

8.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Advancements in Catalytic Hydrogenation Technologies

Technological improvements in selective hydrogenation catalysts have significantly improved yield efficiency and cost optimization for cyclohexyl-based aromatics. Modern continuous-flow hydrogenation systems reduce energy consumption by up to 15–20%, improving production economics. These advancements lower entry barriers for new producers and improve profitability for established players, supporting long-term market scalability. Advancements in selective hydrogenation catalysts have significantly enhanced yield efficiency and cost optimization for manufacturers of cyclohexyl-based aromatics such as 1,4-dicyclohexylbenzene. Modern continuous-flow hydrogenation systems achieve substantial production economic improvements through lower energy requirements and streamlined processing. These technological innovations reduce market entry barriers for emerging producers while simultaneously improving profitability margins for established industry participants, thereby supporting sustainable market scalability expansion.

The implementation of advanced catalyst technologies enables superior control over reaction selectivity and product quality consistency. Producers across different geographic regions can now access cost-effective manufacturing methodologies that were previously limited to large-scale chemical conglomerates. This democratization of production capabilities creates new competitive dynamics and supports broader geographic market penetration without requiring substantial capital investment in specialized infrastructure or proprietary process technologies. Process intensification approaches further enhance operational flexibility by allowing manufacturers to adapt production cycles to fluctuating market demand patterns. Smaller scale operations gain access to competitive manufacturing economics that previously favored only large integrated chemical facilities.

Stringent Environmental and Safety Regulations

Chemical manufacturing regulations related to emissions, hydrogen handling, and aromatic compound exposure place a meaningful burden on operators that must maintain strict compliance programs. Companies need to invest in monitoring systems, containment infrastructure, personal protection protocols, and documentation processes that meet evolving standards. These requirements often call for continuous upgrades to equipment and procedures, as authorities refine expectations for workplace safety and environmental performance. This creates a recurring need to align capital expenditure plans with regulatory roadmaps rather than with production priorities alone.

In more mature regulatory environments, compliance obligations can also constrain how flexibly plants operate. Smaller manufacturers, in particular, may find that each incremental capacity addition triggers additional permitting, audits, and engineering work, which slows execution and complicates timelines. Larger producers can distribute these burdens across multiple sites and larger volumes, while smaller participants must absorb them within a narrower revenue base. This dynamic reinforces the importance of proactive compliance planning, robust environmental, health, and safety (EHS) capabilities, and selective collaboration with third-party experts to preserve agility while meeting regulatory expectations.

Emerging Applications in Advanced Coatings

High-performance industrial coatings are increasingly requiring thermally stable aromatic additives to withstand demanding operating environments. Formulators are selecting materials that retain structural integrity under elevated temperatures and aggressive chemical exposure, which is positioning 1,4-dicyclohexylbenzene as a functional component in advanced coating architectures. Manufacturers are integrating this compound into corrosion-resistant primers, heat-tolerant topcoats, and protective barrier layers used in marine vessels, oil and gas infrastructure, and heavy industrial machinery. In these sectors, coating durability is directly influencing asset lifespan, maintenance frequency, and operational continuity. As regulatory bodies are tightening standards around material performance and environmental resilience, coating systems are being engineered with higher thermal thresholds and chemical resistance profiles. This shift is reinforcing demand for additives that contribute to long-term structural stability without degrading under cyclical stress conditions.

Coatings producers are also prioritizing compatibility with advanced resin chemistries, including high-solid and specialty polymer systems, where additive performance must align with viscosity control and application efficiency requirements. 1,4-dicyclohexylbenzene is supporting improvements in film uniformity, adhesion strength, and surface durability while maintaining process consistency during formulation. This functional balance is enabling manufacturers to meet stricter specifications related to weathering resistance and mechanical stability. For business leaders, strategic growth is emerging through collaborative development agreements with coating formulators to tailor performance attributes for sector-specific applications. By aligning product development with evolving industrial standards, suppliers can strengthen their positioning within the expanding protective coatings segment in this market.

Category-wise Analysis

Application Insights

Adhesives are poised to dominate, capturing approximately 32% of the 1,4-dicyclohexylbenzene market revenue share in 2026. This chemical enhances adhesive formulations with superior thermal stability and chemical resistance. This makes it essential for structural bonding agents and high-performance sealants used across automotive assembly, construction bonding, packaging, and industrial maintenance. Manufacturers favor it in pressure-sensitive adhesives (PSAs), hot-melt formulations, and epoxy systems that require durability under mechanical stress and temperature variations. The segment enjoys stable demand across mature and emerging markets, supported by consistent industrial production volumes and infrastructure development. This established leadership reflects proven performance reliability and broad compatibility with diverse resin chemistries.

Electrical & electronics is likely to be the fastest-growing segment during the 2026-2033 forecast period. These applications drive the fastest growth as semiconductor manufacturing expands and consumer electronics proliferate. 1,4-Dicyclohexylbenzene enables thermal interface materials, dielectric fluids, and protective coatings that manage heat dissipation in high-density circuits. Demand accelerates with 5G infrastructure, electric vehicle electronics, and advanced computing systems requiring reliable thermal management solutions. Formulators value the compound's low volatility and high dielectric strength for circuit board protection and semiconductor packaging. This segment commands premium pricing due to stringent purity requirements and performance specifications, positioning it for sustained expansion amid global electronics industry transformation.

End-User Insights

Automotive is expected to hold the highest revenue share at an estimated 45% in 2026 due to the extensive use of 1,4-dicyclohexylbenzene in assembly adhesives, protective coatings, and thermal management components. 1,4-dicyclohexylbenzene enables the formulation of lightweight composites, battery thermal barriers, and corrosion-resistant underbody coatings essential for modern vehicle platforms. Original equipment manufacturers (OEMs) integrate it into structural adhesives for body-in-white assembly and high-durability paint systems. The segment sustains leadership through consistent global vehicle production volumes and ongoing platform development cycles. The global transition toward electric vehicles (EVs) has further reinforced the demand for advanced material solutions that balance weight reduction, thermal performance, and long-term durability.

Electronics is expected to be the fastest-growing segment over the 2026-2033 forecast period, fueled by semiconductor capacity expansion, consumer device proliferation, and data center infrastructure buildout. 1,4-Dicyclohexylbenzene plays a key role in thermal management compounds, conformal coatings, and dielectric materials for printed circuit boards and chip packaging. Rapid adoption of artificial intelligence hardware, 5G networks, and Internet of Things (IoT) devices intensifies requirements for efficient heat dissipation and electrical insulation. Manufacturers prioritize high-purity grades to meet reliability standards in mission-critical applications. This segment benefits from accelerated innovation cycles and substantial capital investments in fabrication facilities worldwide.

Purity Insights

The above 99% segment is set to lead with approximately 65% of the 1,4-dicyclohexylbenzene market share in 2026. Electronics, pharmaceutical intermediates, and advanced coatings manufacturers specify these premium formulations to ensure consistent performance and regulatory compliance. Producers achieve this quality through advanced distillation, purification technologies, and rigorous quality control protocols. The segment commands pricing premiums while serving customers with zero-defect tolerance and stringent certification requirements. Market leadership stems from broad compatibility across high-value applications and established supply chains optimized for purity consistency. Customers value reliable sourcing from certified manufacturers maintaining validated production processes.

The below 99% segment is anticipated to be the fastest-growing between 2026 and 2033. Construction coatings, general industrial adhesives, and basic chemical intermediates increasingly adopt these economical variants for non-critical performance requirements. Producers target price-competitive formulations suitable for mass-market paints, sealants, and polymer additives where ultra-high purity offers marginal benefits. Regional manufacturers in Asia-Pacific optimize production economics to serve infrastructure projects and consumer goods packaging. Growth accelerates as developing economies prioritize affordability over premium specifications, creating substantial volume opportunities for standardized, reliable mid-grade products.

Regional Insights

Asia Pacific 1,4-Dicyclohexylbenzene Market Trends

Asia Pacific is anticipated to be the fastest-growing and leading market with a projected 40% share in 2026. China, Japan, and India are spearheading regional consumption as manufacturers expand production capacities to meet domestic needs and export requirements. Cost-competitive operations paired with growing downstream industries, such as automotive assembly and electronics manufacturing, generate consistent demand. Local producers leverage integrated supply chains and proximity to major consumption centers for competitive advantage. Business leaders view these markets as prime opportunities to build regional presence through localized manufacturing facilities, strategic joint ventures, and dedicated supply chain partnerships. This approach enables companies to capture market share, optimize logistics costs, and establish long-term customer relationships across the region's diverse industrial landscape.

Favorable industrial policies and export-focused production strategies attract substantial capital investments from multinational corporations and regional players alike. Governments actively support chemical manufacturing through infrastructure development, tax incentives, and streamlined regulatory pathways. This policy environment enables producers to optimize facility locations near key feedstock sources and major consumption centers. Asia Pacific also represents the critical growth frontier where strategic positioning through joint ventures, technology transfer agreements, and dedicated sales organizations unlocks disproportionate market share gains and establishes competitive advantages for the coming decade.

Europe 1,4-Dicyclohexylbenzene Market Trends

Europe is expected to maintain a strong position in the specialty chemical landscape through 2033, on the back of a mature manufacturing base and technologically advanced end-user industries. Germany, the United Kingdom, and France are serving as primary demand centers due to their established production ecosystems and engineering capabilities. Specialty coatings manufacturers and high-performance material producers are generating consistent demand for tightly specified aromatic intermediates used in automotive, aerospace, and construction applications. Companies are benefiting from integrated supply chains, close proximity to major industrial customers, and collaborative research partnerships with OEMs. This industrial structure is reinforcing quality control standards and accelerating product innovation. As technical requirements are becoming more stringent, suppliers are strengthening formulation support and process optimization services to maintain competitive differentiation. Europe is therefore functioning as a reference market where performance benchmarks and technical compliance are shaping procurement decisions.

Regulatory harmonization under European Union (EU) chemical frameworks, including Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH), is influencing material selection and formulation strategies. Producers are prioritizing EHS compliance to secure uninterrupted market access and long-term customer approval. Sustainability targets are shaping competitive positioning, as manufacturers are developing lower-emission production methods and incorporating circular economy principles into sourcing and waste management practices. Policy alignment with climate objectives is encouraging innovation in green chemistry and safer compound alternatives. For strategic planners, Europe is offering demand stability combined with regulatory clarity, which is reducing uncertainty in capital allocation decisions. Companies that are integrating sustainability performance with technical excellence can deepen their partnerships with industrial clients seeking compliant and future-ready chemical solutions, bolstering their growth prospects in the region.

North America 1,4-Dicyclohexylbenzene Market Trends

North America is playing a prominent role in the specialty chemical sector through its established manufacturing infrastructure and technologically advanced end-user industries. The United States is driving regional demand with integrated polymer production facilities and strong research & development (R&D) capabilities that support continuous formulation improvement. Specialty chemical producers are engaging in technical collaboration with automotive, electronics, and aerospace manufacturers to tailor high-performance intermediates for complex applications. Companies are benefiting from integrated logistics networks, regulatory clarity, and proximity to major industrial consumption centers. This environment is enabling reliable production performance and consistent quality assurance across supply chains. As customers are requiring tighter specifications and validated performance data, suppliers are strengthening laboratory support and application engineering services to secure repeat contracts.

Federal environmental and safety regulations are maintaining elevated compliance requirements, which are strengthening the competitive position of established manufacturers. Larger operators are distributing compliance expenditures across diversified production assets and are leveraging economies of scale to protect margins. Smaller firms are facing higher proportional regulatory costs, which is influencing consolidation trends within niche segments. Companies are investing in advanced process optimization, digital manufacturing control systems, and specialty compound development to sustain competitive differentiation. The region is likely to establish itself as a stable innovation platform where regulatory adherence and technical capability will shape procurement preferences during the 2026-2033 forecast period. This scenario is expected to unlock opportunities for value-based pricing and long-term partnerships in high-specification markets across automotive, aerospace, and electronics industries.

Competitive Landscape

The global 1,4-dicyclohexylbenzene market exhibits a moderately fragmented structure, with a group of multinational chemical producers holding a combined share of approximately 35-45%. Competition is centering on manufacturing efficiency, product purity control, and the ability to secure stable multi-year supply agreements with downstream customers. Producers are differentiating through process optimization, yield improvement, and stringent quality assurance systems that ensure batch consistency. High-purity grades are serving electronics and pharmaceutical applications where impurity thresholds are tightly regulated, enabling premium pricing strategies. Standard industrial grades are competing primarily on cost competitiveness and delivery reliability. Buyers are prioritizing suppliers that can demonstrate traceability, consistent specifications, and scalable output capacity. As application requirements are becoming more specialized, suppliers are investing in purification technologies and analytical testing infrastructure to strengthen customer confidence and reduce substitution risk.

Asia Pacific manufacturers are maintaining strong positions due to production cost advantages, vertically integrated supply chains, and close proximity to expanding end-use industries. Regional producers are aligning output with domestic demand growth in advanced materials and specialty coatings while also supporting export-oriented chemical value chains. Global chemical leaders are competing through technical depth, application development support, and established brand credibility across regulated industries. Regional players are leveraging operational agility and faster response times to address localized customer needs. This competitive balance is encouraging continuous investment in process innovation and supply chain resilience.

Key Industry Developments

- In February 2026, Henkel strengthened its adhesives division by agreeing to acquire a portfolio of industrial adhesives and sealants businesses from Stahl Holdings in a multi-billion-euro transaction, reinforcing its position in high-growth markets such as automotive and electronics assembly.

- In February 2026, AkzoNobel Aerospace Coatings introduced AeroBase Single Coat Primer/Finish, a combined primer and topcoat solution for maintenance, repair, and overhaul (MRO) paint facilities that reduces process steps, improves turnaround times, and maintains corrosion protection and durability.

- In December 2025, Beacon introduced Magna-Tac® E645, a heat-cured epoxy adhesive formulated to bond lamination stacks in electric motors, generators, and transformers while maintaining insulation and mechanical integrity under thermal cycling and vibration.

Companies Covered in 1,4-Dicyclohexylbenzene Market

- BASF SE

- Covestro AG

- Huntsman Corporation

- Wanhua Chemical Group

- Celanese Corporation

- Arkema SA

- Mitsubishi Chemical Corporation

- Solvay SA

- LG Chem Ltd.

- Dow Inc.

- Mitsui Chemicals, Inc.

- Ascend Performance Materials

- SABIC

- LyondellBasell Industries

- Evonik Industries AG

- Henkel AG & Co. KGaA

- Sinopec Shanghai Petrochemical Company

- AdvanSix Inc.

- Tosoh Corporation

- Lanxess AG

Frequently Asked Questions

The global 1,4-dicyclohexylbenzene market is projected to reach US$151.0 Mn in 2026.

The market is driven by rapid automotive/electronics manufacturing expansion, high-performance polymer demand, and catalytic process technology improvements.

The market is poised to witness a CAGR of 8.5% from 2026 to 2033.

Industrialization of Asia Pacific economies, green chemistry innovations, and electronics thermal management applications create substantial growth potential.

BASF SE, Covestro AG, Huntsman Corporation, Wanhua Chemical Group, and Celanese Corporation are some of the key players in the market.