ID: PMRREP4458| 197 Pages | 30 Oct 2025 | Format: PDF, Excel, PPT* | Healthcare

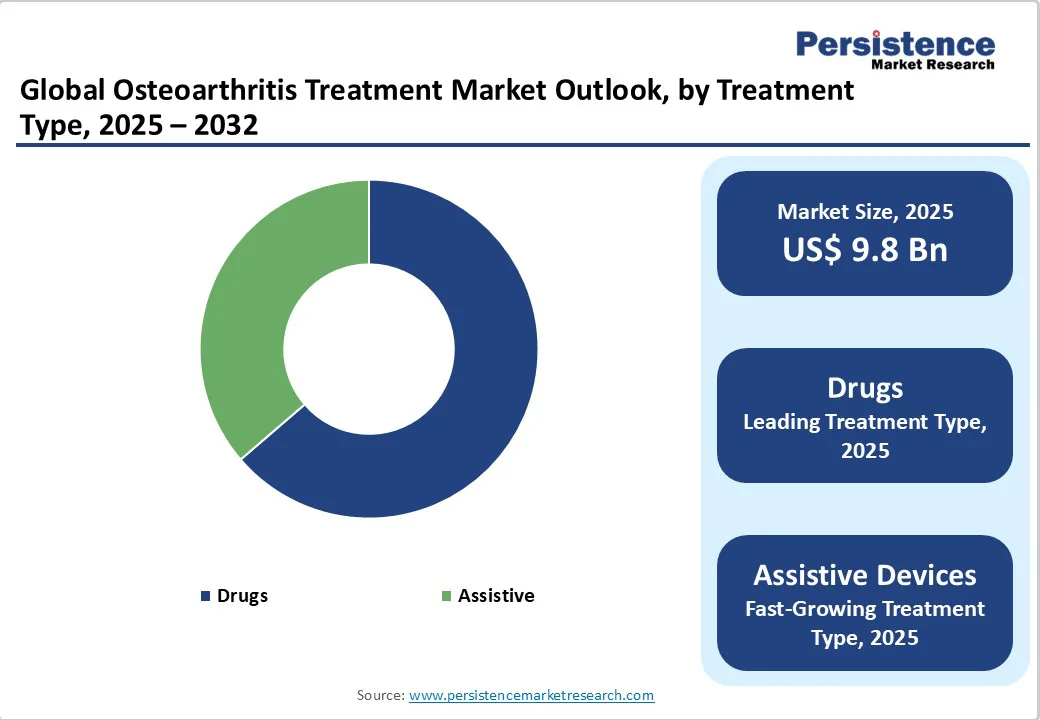

The global osteoarthritis treatment market size is likely to value US$ 9.8 billion in 2025 and is projected to reach US$ 15.3 billion by 2032, growing at a CAGR of 6.6% during the forecast period from 2025 to 2032.

Global demand for osteoarthritis treatment is rising as pharmaceutical and medical device companies expand the development of advanced drugs, regenerative therapies, and orthopedic implants.

Increasing disease prevalence, coupled with growing demand for effective pain management and joint preservation solutions, is driving market growth.

| Key Insights | Details |

|---|---|

| Osteoarthritis Treatment Market Size (2025E) | US$ 9.8 Bn |

| Market Value Forecast (2032F) | US$ 15.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.7% |

Rapid advancements in regenerative medicine, biologics, and digital technologies are driving the osteoarthritis treatment market. Development of disease-modifying osteoarthritis drugs (DMOADs), stem cell and gene-based therapies, and next-generation viscosupplements aim to halt disease progression rather than merely alleviate symptoms.

Additionally, the integration of 3D-printed implants, AI-assisted diagnostics, and minimally invasive surgical techniques enhances treatment precision and outcomes. These innovations collectively accelerate adoption rates, attract strategic investments, and drive market growth.

The global prevalence of osteoarthritis (OA) is increasing rapidly due to lifestyle changes, obesity, and longer life expectancy. Growing incidence across younger and middle-aged populations is expanding the overall patient base and intensifying the need for effective management options.

For instance, a recent article published in February 2025 reported that osteoarthritis (OA) remains the most prevalent form of arthritis in the United States, affecting nearly 24% of the adult population driving consistent demand for advanced pharmacological, surgical, and rehabilitative treatment solutions.

The high cost of novel biologics, regenerative cell therapies, and joint replacement surgeries poses a significant restraint to osteoarthritis treatment market. Limited reimbursement coverage and high out-of-pocket expenses restrict patient access, particularly in low- and middle-income countries.

These affordability challenges discourage the uptake of premium treatment options and promote reliance on low-cost conservative care, thereby constraining revenue growth and market penetration for advanced OA therapeutics and surgical interventions.

Moreover, despite their therapeutic potential, many regenerative treatments and disease-modifying osteoarthritis drug (DMOAD) candidates lack conclusive long-term clinical evidence demonstrating sustained structural improvement and symptom relief.

The absence of large-scale, randomized data creates skepticism among clinicians, regulators, and payers, limiting confidence in their real-world effectiveness. This uncertainty has confined several innovative therapies to experimental or niche applications, thereby slowing mainstream adoption and hindering overall market growth.

The expanding commercialization of regenerative solutions, including cartilage repair and tissue-engineered products such as scaffolds, cell-based implants, and 3D-bioprinted constructs, presents a major opportunity in the osteoarthritis treatment market. These innovative modalities aim to restore joint function and delay disease progression by repairing damaged cartilage rather than merely alleviating symptoms.

Targeting younger and early-stage OA patients, they bridge the treatment gap between conservative care and joint replacement. Increasing clinical validation, regulatory approvals, and strategic collaborations among biotech firms and orthopedic manufacturers are further accelerating their market adoption and investments.

The advancement of DMOADs are creating significant opportunities to redefine osteoarthritis treatment by targeting the underlying pathophysiology rather than merely managing symptoms. These agents aim to restore cartilage integrity, modulate inflammation, and prevent structural joint damage, addressing a major unmet clinical need.

Leading candidates such as lorecivivint (SM04690) and sprifermin (FGF18) are progressing through late-stage clinical development. Their successful approval and commercialization would establish a new therapeutic class, and deliver durable efficacy.

The drugs segment is projected to dominate the global osteoarthritis treatment market in 2025, accounting for a revenue share of 63.7%. This is due to the widespread adoption of pharmacological therapies as the primary treatment approach, supported by their affordability, ease of administration, and proven effectiveness in pain management and inflammation control.

Additionally, the growing availability of improved formulations and the strong preference for non-surgical treatment options among patients and clinicians further drive the segment growth.

The knee osteoarthritis segment is projected to dominate the global osteoarthritis treatment market in 2025, accounting for a revenue share of 44.6%. The segment’s strong performance is primarily driven by the high prevalence of knee degeneration, particularly among aging and obese populations.

For instance, according to the Institute for Health Metrics and Evaluation (IHME), the knee is the most commonly affected joint in osteoarthritis cases worldwide. The institute further projects that by 2050, the global prevalence of knee osteoarthritis will increase by approximately 75%, driven by aging populations, rising obesity rates, and sedentary lifestyles.

Increased adoption of viscosupplementation, corticosteroid injections, and total knee replacement procedures, coupled with the availability of advanced implant technologies and favorable reimbursement policies.

The hospitals segment is projected to dominate the global osteoarthritis treatment market in 2025, accounting for a revenue share of 43.6%. This is due to the availability of advanced diagnostic and surgical infrastructure, including imaging technologies, arthroscopy, and joint replacement facilities.

Hospitals also offer comprehensive multidisciplinary care involving orthopedic specialists, physiotherapists, and pain management experts. Furthermore, the rising number of hospital-based outpatient procedures and favorable reimbursement for surgical interventions continue to strengthen the segment’s leading position in the global market.

The North America market is expected to dominate globally with a value share of 40.2% in the 2025, with the U.S. leading the region due to the high prevalence of osteoarthritis, increasing obesity rates, and an aging population that significantly elevates disease burden.

The region benefits from a well-established healthcare infrastructure, widespread access to advanced diagnostic and surgical facilities, and strong reimbursement frameworks supporting joint replacement and injectable therapies.

Moreover, research and development investments, early adoption of innovative treatment modalities including regenerative medicine and digital health platforms and the presence of major pharmaceutical and medical device companies further boosts market growth in the region.

The Europe market is expected to grow steadily, driven by the rising prevalence of joint disorders among the aging population, increasing awareness of early diagnosis and treatment, and expanding adoption of minimally invasive surgical procedures. Supportive government healthcare initiatives, favorable reimbursement policies, and advancements in regenerative and pharmacological therapies further drives to market growth.

Additionally, the strong presence of leading medical device manufacturers and growing clinical research collaborations across major countries such as Germany, the U.K., and France are fostering continuous innovation in osteoarthritis care.

For instance, the European Project on Osteoarthritis (EPOSA) serves as a key initiative assessing the personal and societal impact of OA among Europe’s aging population. Utilizing data from six large-scale cohort studies across the region, EPOSA investigates determinants of knee, hip, and hand osteoarthritis.

By including both affected and non-affected individuals, the project provides valuable insights into OA’s broader burden on quality of life, healthcare utilization, and social participation supporting policy development and resource allocation in Europe’s healthcare systems.

The Asia Pacific market is expected to register a relatively higher CAGR of around 23.4% between 2025 and 2032, fueled by the rising prevalence of osteoarthritis due to sedentary lifestyles, obesity, and expanding geriatric populations across countries such as China, Japan, and India. Increasing healthcare expenditure, improving access to advanced orthopedic care, and growing awareness of early diagnosis are further driving market growth.

Additionally, the growing presence of domestic manufacturers producing cost-effective implants, viscosupplementation products, and assistive devices is also strengthening regional competitiveness and affordability. In addition, the rise of medical tourism particularly in India, Thailand, and South Korea alongside advancements in minimally invasive orthopedic procedures, is attracting international patients.

The global osteoarthritis treatment market is highly competitive, with major players such as ABIOGEN PHARMA S.p.A, Assertio Holdings, Inc, Abbott, Bayer AG, and Johnson & Johnson dominating the industry through extensive product portfolios and strong global distribution networks. These players are actively investing in novel pharmacological therapies, regenerative medicine, and minimally invasive surgical solutions to enhance treatment efficacy and patient outcomes.

Strategic initiatives such as mergers & acquisitions, licensing agreements, and collaborations with biotechnology firms are enabling these companies to strengthen their R&D pipelines and expand therapeutic offerings. Additionally, increasing focus on digital health platforms, real-world evidence generation, and patient-centric care models is helping market leaders maintain a competitive edge.

The global osteoarthritis treatment market is projected to be valued at US$ 9.8 Bn in 2025.

The rising disease prevalence due to obesity, sedentary lifestyles, and aging populations, alongside growing demand for effective pain management and regenerative therapies are driving the global market.

The global osteoarthritis treatment market is poised to witness a CAGR of 6.6% between 2025 and 2032.

Government initiatives, increasing investments in biopharmaceutical and medical device manufacturing, and the expansion of vaccine and sterile injectable production are creating significant growth opportunities in the market.

ABIOGEN PHARMA S.p.A, Assertio Holdings, Inc, Abbott, Bayer AG, Johnson & Johnson are some key players.

| Report Attribute | Details |

|---|---|

| Historical Data/Actuals | 2019 - 2024 |

| Forecast Period | 2025 - 2032 |

| Market Analysis | Value: US$ Bn |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

By Treatment Type

By Indication

By End-use

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author